Global IPOs hit back strongly after COVID-19 crash

IPO activity ground to a halt following the outbreak of the pandemic, but activity in the second half of the year more than made up for the downturn

The impacts of the pandemic were inescapable, but the global IPO market registered significant successes during 2020, ending the year on a high

With much of the world in lockdown, COVID-19 inevitably depressed the global IPO market during the first half of last year. But while both the number and value of listings declined, 2020 was anything but a write-off for new issues, as the second half of the year saw a significant pick-up. A record-breaking year for the special purpose acquisition company (SPAC) market also provided a boost.

Certainly, IPOs slowed to a trickle at times during H1 2020, notably at the height of the pandemic's first wave in Western Europe and North America in early spring. A year that began with promise—IPO activity was robust in January and February—was derailed by a black swan event.

However, certain sectors proved resilient. Technology, media and telecoms businesses, largely immune from the impacts of COVID-19, or even boosted by the pandemic, continued to come to market. The pharma, medical and biotech sector—at the center of the battle against the virus—also performed strongly.

Moreover, even businesses facing difficult market conditions proved that IPOs of attractive companies would continue to win support, and could be executed through the innovative use of technology. The listing of the coffee group JDE Peet's, managed through a three-day virtual roadshow, was a case in point.

This report, which features exclusive data provided by Mergermarket, considers the performance of the global market in 2020, highlighting key regions and trends. It also looks to the year ahead, finding real reasons for optimism, despite the ongoing impacts of COVID-19.

IPO activity ground to a halt following the outbreak of the pandemic, but activity in the second half of the year more than made up for the downturn

After more than a decade of buildup, special purpose acquisition companies (SPACs) have exploded and are gaining momentum in the US and beyond

Early-year highs gave way to a pandemic-driven downturn, which was then followed by a revival in H2

Although COVID-19 hit the region hard, there was a surge of IPOs in the second half of last year, mainly centered around Brazil’s consumer industry

As the pandemic continues to overshadow financial markets and the global economy, the following factors will have a major impact on the IPO market in 2021

IPO activity ground to a halt following the outbreak of the pandemic, but activity in the second half of the year more than made up for the downturn

Stay current on your favorite topics

World in Transition

Our views on changing dynamics in energy, ESG, finance, globalization and US policy.

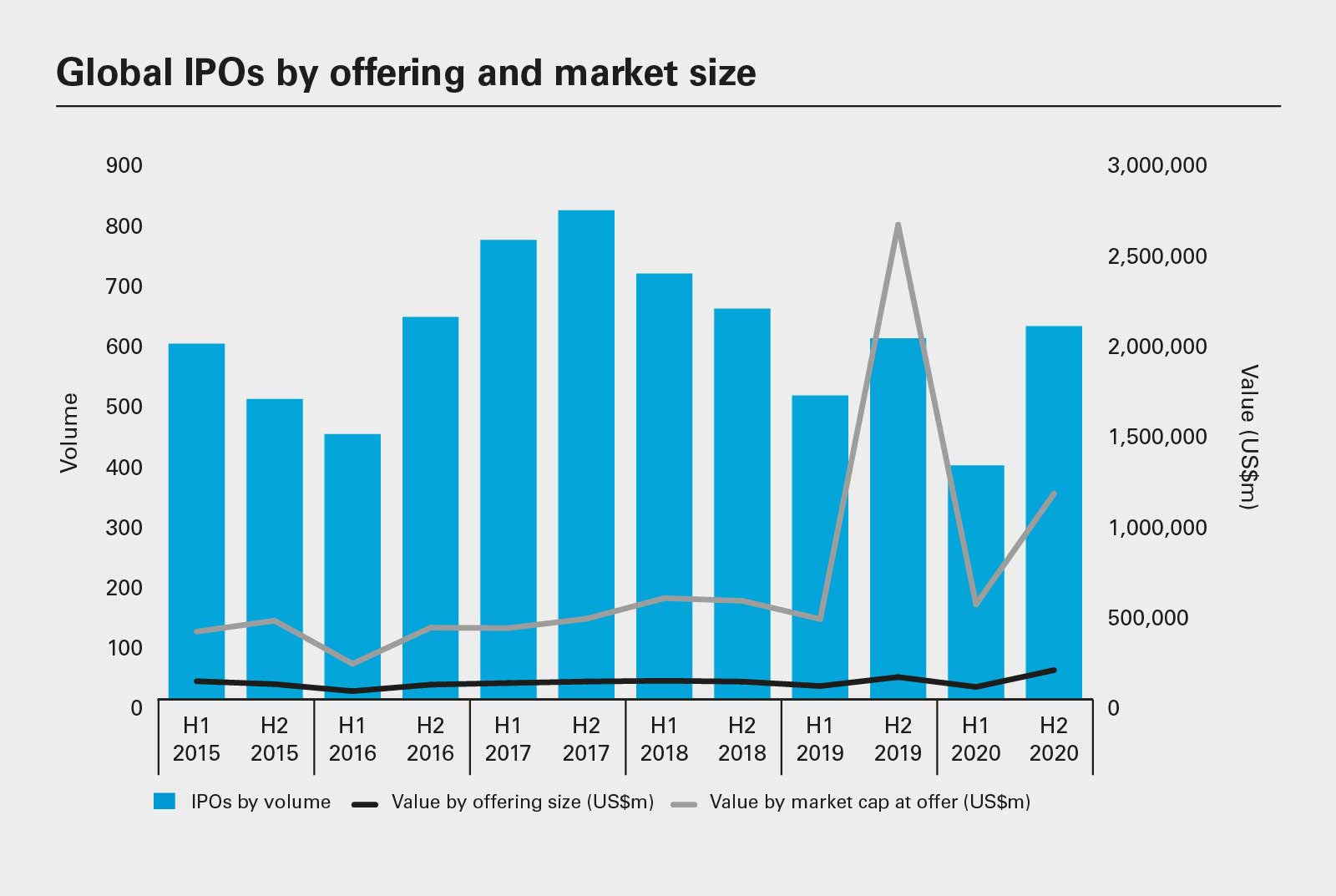

The global initial public offering (IPO) market was very much a game of two halves in 2020. COVID-19 brought activity to a virtual standstill in H1, only for IPOs to stage a remarkable recovery in the second half of the year.

619

The number of global listings in H2 2020

As 2020 began, the IPO outlook was healthy after a record-breaking 2019. Despite some headwinds—for example, China's ongoing trade dispute with the US and Brexit uncertainties—investors' appetite for IPOs was keen, particularly in areas such as technology, media and telecoms (TMT), where they looked forward to blockbuster issuances from well-known names such as Airbnb, Ant Financial and WeDoctor.

However, the rapid spread of COVID-19 around the world soon put the brakes on listings, particularly after the global stock market volatility in March. The virus posed unprecedented challenges for issuers. Companies and financial sponsors alike felt compelled to cancel or postpone their plans.

Only 388 businesses completed their IPOs during H1 2020, raising US$69.6 billion. These figures were down 23 percent and 7 percent, respectively.

In value terms, the first half was the worst-performing half since 2016, and no period has seen such low volumes in the past five years.

The second half of the year was a completely different story. There were 619 listings—an increase of 3 percent on the same period last year—raising a total of US$162.3 billion, the highest H2 value on record. Indeed, this revival brought the total raised to US$231.9 billion, the biggest annual figure since 2015.

Even the overall falling volume figures need to be put into a regional context. IPO volumes fell 33 percent in Western Europe and 15 percent in Asia but increased by 30 percent in North America. Meanwhile, private equity listings increased by 13 percent in volume and raised 48 percent more money than in 2019.

In addition, the unique circumstances of the first half of the year even led to interesting opportunities. For example, the demand for new issuance, combined with the reluctance of many companies considering IPOs to commit to a listing process in an uncertain environment, accelerated the trend toward special purpose acquisition companies (SPACs).

For more on the SPACs boom, see Prime time for SPACs.

US$ 231.9 billion

The total amount raised by global IPOs in 2020

Looking ahead, there are even more reasons to be optimistic about the IPO market in 2021. The rollout of vaccines means that a measure of normality may return over the next few months. And there are a wealth of pandemic-hardened companies, especially in the TMT sector, that are looking to list.

One of the keys to the revival was sectoral resilience—particularly for the TMT and pharmaceuticals, medical and biotech (PMB) industries, which raised total proceeds of US$57.3 billion and US$49.2 billion, respectively. Their cumulative total accounted for 46 percent of all IPO proceeds in 2020. The consumer and industrials and chemicals sectors also performed strongly in terms of value.

July's IPO of Lemonade, for example, underlined the strength of investors' appetite for good-quality technology businesses. The innovative insurtech business raised US$367 million from investors and saw its shares more than double in value on their first day of trading. Other technology IPOs that launched over the summer included business database provider ZoomInfo, and online car sales company Vroom.

And, as the year progressed, the technology listings grew. Household names such as short-stay residential operator Airbnb and food delivery platform DoorDash joined the Nasdaq and NYSE respectively, each raising more than US$3 billion.

Meanwhile, in China, the Shenzhen XFH Technology Co Ltd joined the Shanghai Stock Exchange in an offering that raised US$5.4 billion, while JD.com's IPO on the Hong Kong Stock Exchange picked up US$4.46 billion.

In addition to the resilience of certain sectors, innovation and demand were crucial to unlocking the market after the summer.

A prime example of innovative processes at work comes from Dutch coffee group JDE Peet's. The company's listing on Amsterdam's Euronext exchange raised US$2.9 billion in a deal that was managed via a three-day virtual roadshow to overcome COVID-19 travel restrictions.

That process helped provide a virtual marketing template for subsequent IPOs and paved the way for the successes seen in the second half of the year. The Italian manufacturing business GVS, for example, raised €500 million in its listing in Milan. Like JDE Peet's, GVS showed new offerings can be marketed virtually—video clips of its factories replaced physical visits—and management meetings and presentations were conducted online.

Not only did H2 see an unprecedented turnaround in activity, overall post-IPO performance has been extremely strong. Almost a third (30 percent) of companies that listed in 2020 saw their share prices rise by 51 percent or more after a day of trading, compared to 18 percent of companies that listed in 2019. Forty-six percent of companies listing this year saw their share prices rise by 51 percent or more a month after listing, compared to 35 percent of companies in 2019.

The second-half surge looks to be no one-off. In the first three weeks of 2021, new issuances were at an all-time high year-to-date, with 15 IPOs raising US$7.3 billion in the US alone.

And looking ahead, there are even more reasons to be optimistic about the IPO market in 2021. The rollout of vaccines means that a measure of normality may return over the next few months. And there are a wealth of pandemic-hardened companies, especially in the TMT sector, that are looking to list.

However, until full normality returns, the success of listings such as JDE Peet's and GVS proves that the deal process itself can be completed even where traditional IPO approaches are impossible. Due diligence can be conducted remotely, and meetings can take place online. Indeed, this process may even come with less friction and accelerated speed—traditionally, listings were preceded by weeks-long meetings that required extensive travel.

However, despite the upward trajectory of the market, it is difficult to make definitive predictions about IPO activity in the coming months. Tough challenges remain, but good companies will continue to attract investors' attention, especially if stock market performance remains buoyant.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: Global IPOs by offering and market size (PDF)

View full image: Global IPOs by offering and market size (PDF)