Ireland has published its first annual report on the operation of its FDI screening regime. Statistics show that Ireland is taking a restrained approach to determining which transactions merit screening and is clearing the vast majority of those that do.

The Irish FDI regime

Ireland's first foreign direct investment (FDI) regime came into force on 6 January 2025 in the form of the Screening of Third Country Transactions Act 2023 (STCTA). For more information on the STCTA regime, White & Case's 2026 summary of its operation is accessible here.

In May, the Department of Enterprise, Tourism and Employment (DETE) published the first annual report on the operation of the regime, including general trends and key statistics.

Notifications

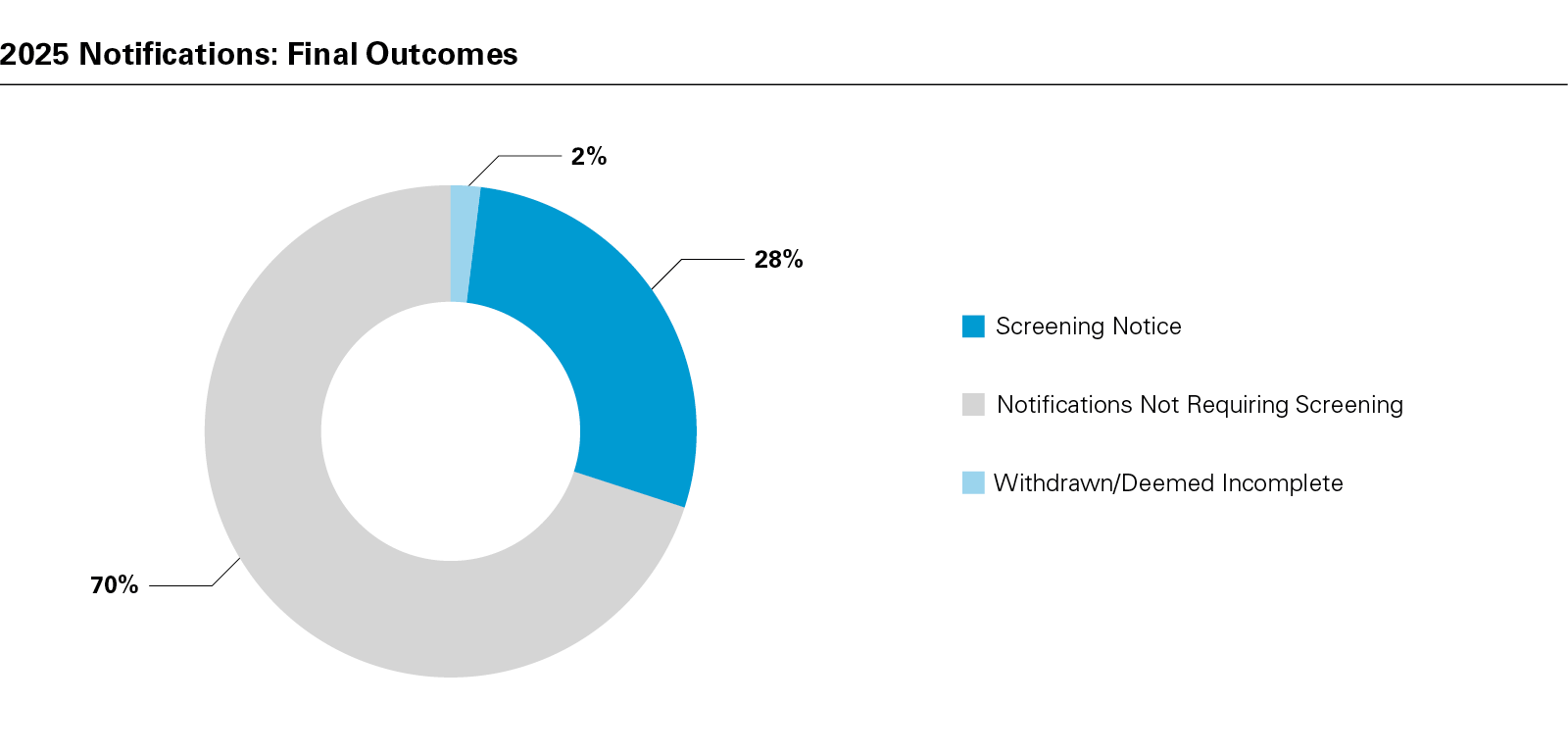

The report covers the period from the STCTA's entry into force until 31 December 2025. The STCTA regime mandates notification of eligible investments in defined sectors by investors from third countries, i.e., any country that is not a member of the European Union, the European Economic Area, or Switzerland. During the period covered by the report, 102 notifications were submitted to DETE's Investment Screening Unit.

Screening notices

Once a notification is submitted, DETE will determine whether or not to issue a Screening Notice. If a Screening Notice is issued, the transaction will be subject to a screening review during which the Minister will assess whether or not the transaction affects, or would be likely to affect, the security or public order of the State. Closing must be suspended until that review is complete.

The decision to issue a Screening Notice is based on the extent to which a notification is deemed to meet the criteria in section 9 of the STCTA, which defines what constitutes a notifiable transaction. The majority of these criteria are objective, including, for example, whether the investor is from a third country, whether the transaction constitutes a change of control, and whether the deal meets the transaction value threshold.

There is an element of subjectivity, however, as to whether a transaction "relates to, or impacts upon" one of the sensitive sector headings, i.e., critical infrastructure, critical technologies and dual use items, supply of critical inputs, access to sensitive information, and the freedom and pluralism of the media.

During the period covered by the report, 102 notifications were received. Of these, Screening Notices were issued in respect of 26 of those notifications; 66 were not formally screened as they were determined not to have met all of the criteria for mandatory notification. [Note: figures to be verified, 26 + 66 = 92, leaving 10 notifications unaccounted for in the report.] It will typically be readily apparent when the objective criteria are met, but given the broad potential for a transaction to be deemed capable of "relating to" or "impacting upon" the sensitive sectors, this likely reflects a practical approach being taken by DETE in terms of the transactions deemed proximate enough to sensitive activities to satisfy that requirement.

2025 notifications: final outcomes (PDF)

Screening outcomes

Upon completion of a screening review, the Minister may clear a transaction, impose conditions, or prohibit the transaction. During the period covered by the report, two transactions were subject to conditions and none were prohibited.

Screening of non-notified transactions

The Minister also has the power to issue a Screening Notice, and thus initiate a review, in respect of transactions that were not subject to mandatory notification under the STCTA, where satisfied that there are "reasonable grounds for believing that it would be manifestly contrary to the security or public order of the State."1

The Minister did not exercise this power during the period covered by the report.

Sectoral focus

The STCTA creates a mandatory notification obligation in respect of transactions where the activities of the target "relate to, or impact upon"2 any one of five sensitive sectors drawn from Article 4 of EU Regulation (EU) 2019/452 on the screening of foreign direct investments into the Union (the FDI Regulation). These are:

- critical infrastructure;

- critical technologies and dual use items;

- supply of critical inputs;

- access to sensitive information; and

- the freedom and pluralism of the media.

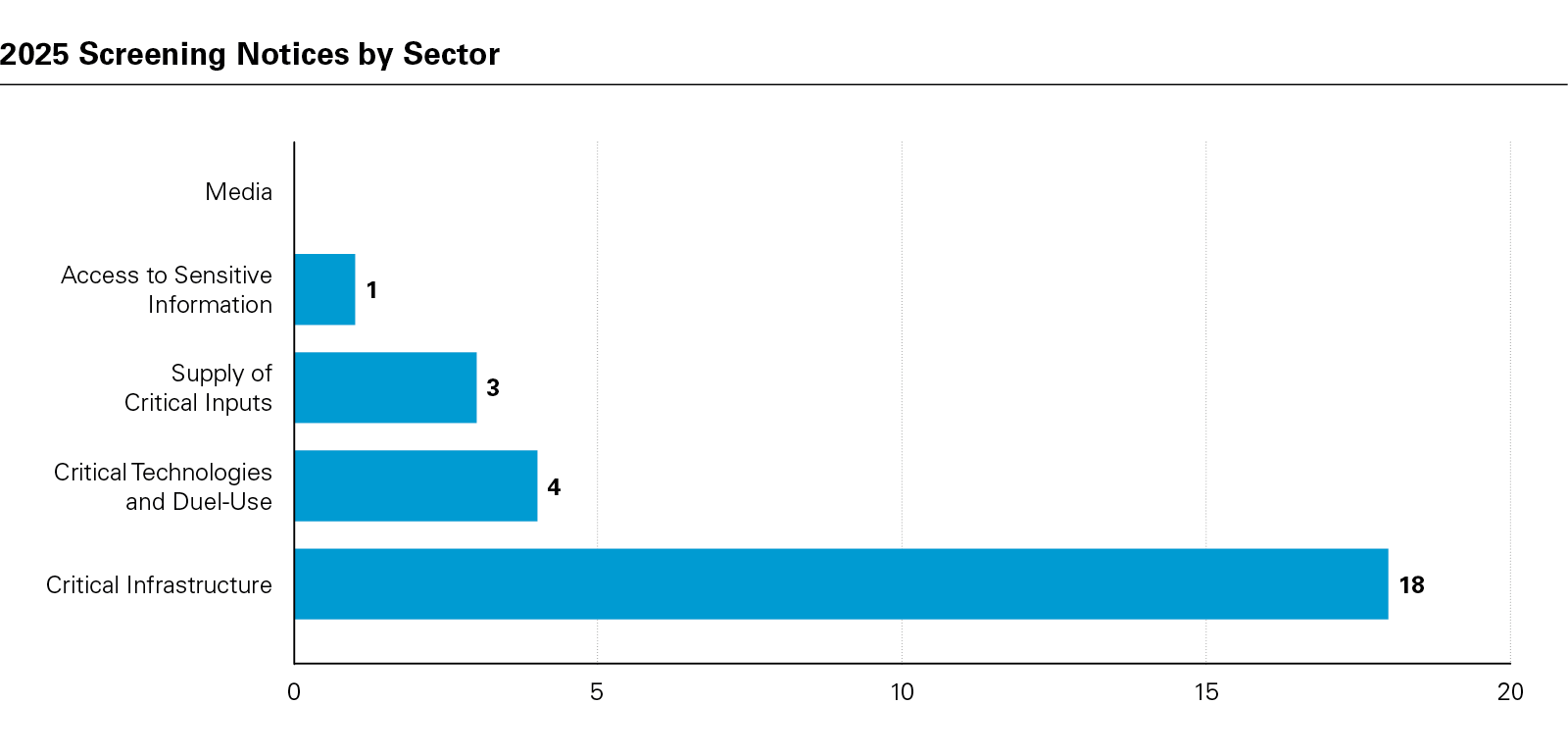

In terms of the transactions that progressed to a screening review via the issue of a Screening Notice, the sectoral breakdown shows that the vast majority related to critical infrastructure. This is not defined under the STCTA, but DETE guidance confirms that it encompasses both physical and virtual infrastructure "essential for the maintenance of vital societal functions," including energy, transport, water, health, communications, media, data processing or storage, aerospace, defense, electoral or financial infrastructure, and sensitive facilities, as well as land and real estate crucial for the use of such infrastructure.

2025 Screening Notices by Sector (PDF)

Within these, the energy segment accounted for the most Screening Notices (8), followed by telecommunications (6), information and communication technologies (6), health (4), and pharmaceuticals (3), noting that some transactions may touch on more than one segment.

Investor origin

The report also provides a breakdown of the origin of investors involved in transactions that received Screening Notices. It should be noted, however, that there is no risk assessment involved in the decision to issue a Screening Notice, any such assessment forms part of the review conducted after the Screening Notice is issued.

2025 screening notices by investor origin | |

|---|---|

| UK | 10 |

| USA | 9 |

| UK & USA | 2 |

| UAE | 2 |

| China | 1 |

| Japan | 1 |

| Monaco | 1 |

Review timing

The report provides an overview of DETE's performance against key timing metrics. DETE aims to make a determination on whether or not to issue a Screening Notice within 10 days. With an average determination timeframe of 9.76 days, DETE achieved this in two-thirds of transactions, although the maximum timeframe extended to 47 days.

In terms of reviews conducted following the issue of a Screening Notice, there is a statutory deadline of 90 days. This may be extended to 135 days if required, but that option was not utilized during the period covered by the report. DETE is frequently clearing transactions well in advance of the standard 90-day deadline, achieving an average timeframe of 40 days in two-thirds of cases. The maximum timeframe recorded was 85 days.

These clearance statistics do not account for time during which reviews were paused to respond to any request for information (RFI) issued by the Department and therefore do not represent the total elapsed timeframe. The report does not detail the timescales for satisfaction of RFIs, but does provide useful background on their typical focus, confirming that the majority of RFIs sought to probe the activities of the target company. RFIs regarding investors were also issued, covering topics including the activities of the investor, customers and/or end-users, alternative providers, the sensitivity and security of data, compliance with export controls, participation in EU programs and projects, ownership structures, market share, financials, and distribution/supply chains.

Engagement with the European Commission

Under the EU FDI Regulation, Ireland participates in the EU Cooperation Mechanism, a forum through which Member States and the European Commission may query and comment on transactions notified under national screening regimes. The approach Member States take on which transactions to refer to the Cooperation Mechanism varies.

The report details that Ireland referred 23 transactions for review, indicating that DETE has adopted a policy of referring almost all transactions deemed to merit a Screening Notice. This is significant because the likelihood of RFIs, and thus potential timing impacts, will be higher for transactions subject to such referral.

Outlook: Anticipated reform - The new EU FDI regulation

Although the STCTA is a relatively new regime, it will nonetheless require updating following the adoption of the new EU FDI Regulation. The STCTA's list of sensitive sectors was drawn directly from Article 4 of the current FDI Regulation. The new EU FDI Regulation extends this list to incorporate new headings covering critical raw materials, semiconductors and quantum technology, artificial intelligence, and certain categories of financial service providers. It also introduces a standardized two-phase review structure and updates to the Cooperation Mechanism. The new EU FDI Regulation will shortly be published in the Official Journal of the European Union and is expected to take effect from early 2028.

1 STCTA, Section 12(1)(b).

2 STCTA, Section 9(1)(d).

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2026 White & Case LLP