UK FDI: Key takeaways from the government's 2024/25 Annual Report and plans for reform

10 min read

The fourth Annual Report on the UK's National Security and Investment Act 2021 (the "NSIA"), covering the period from April 2024 to March 2025 has been released. The Report provides some valuable insights into the review process and how it continues to develop. The Report also neatly coincided with government proposals for reform including a potential exemption for internal restructures and a consultation on changes to the activities that mandate notification under the NSIA.

For a detailed overview of the NSIA, including its operation, notification triggers and timelines, please see our overview from its adoption, available here.

Annual Report: Key Takeaways

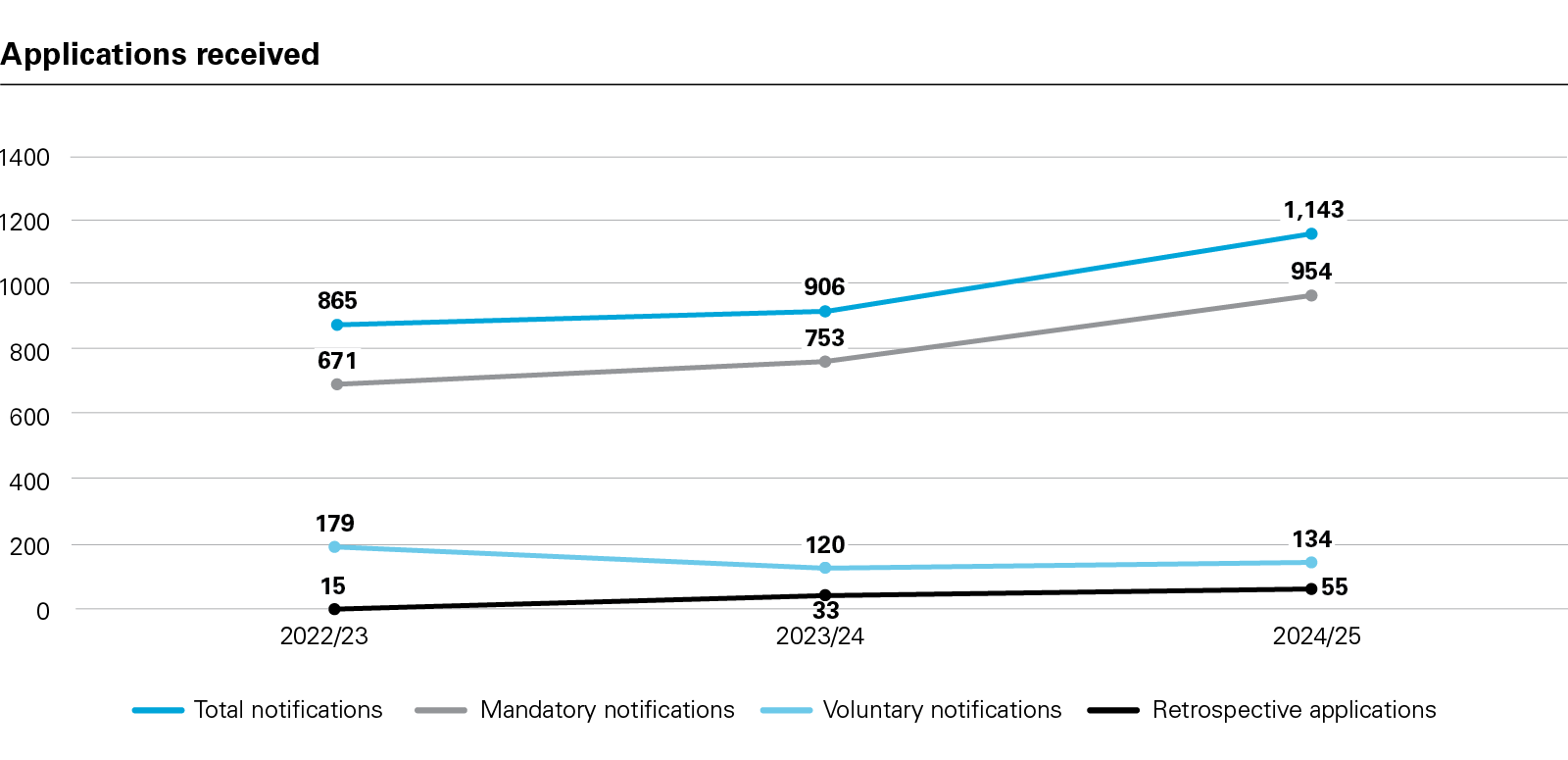

Notifications

During the third full year of the NSIA's operation, the number of notification received by the Investment Security Unit ("ISU") in the Cabinet Office have continued to increase. The total number is up by 26% compared to the previous Report for 2023/24. There are three kinds of notification under the NSIA and all saw an increase in the period between 1 April 2024 and 31 March 2025 covered by the Report (the "Reporting Period"), compared to the preceding twelve months.

- Mandatory Notifications are submitted in respect of qualifying acquisitions in targets that perform certain specified activities in a 'sensitive sector' in the UK, as defined by the National Security and Investment Act 2021 (Notifiable Acquisition) (Specification of Qualifying Entities Regulations 2021 (the "NSIA Regulations"). These notifications are suspensory – closing cannot take place until the notified acquisition is cleared. Mandatory notifications increased by nearly 27% compared to the previous Annual Report.

- Voluntary Notifications are typically submitted in respect of transactions that do not qualify for mandatory notification when one of the parties nevertheless decides it wishes to make a filing. This could be because the transaction is considered likely to be 'called-in', i.e., there is a risk that the government might elect to conduct an ad-hoc review of the transaction under its 'call-in' power. Another reason for making a voluntary notification is to ensure certainty, as the government would otherwise be able to exercise its 'call-in' powers for up to 5 years post-closing. Voluntary notifications also increased in the 2024/25 Reporting Period, with an increase of c. 12%. This is a decrease from the 2022/23 period when the regime reached a high of 179 voluntary submissions, although this is perhaps unsurprising given how new the regime was at the time, and investors' correspondingly cautious approach to it, as the industry was still gathering experience of navigating its requirements.

- Retrospective Validation Applications exist for parties that should have filed a mandatory notification but neglected to do so. As the transaction would otherwise be void, this allows the investor to have the acquisition 'blessed' and secure legal certainty. Retrospective validation applications increased from 33 in 2023/24 to 55 in 2024/25.

View full image: Applications received (PDF)

View full image: Applications received (PDF)

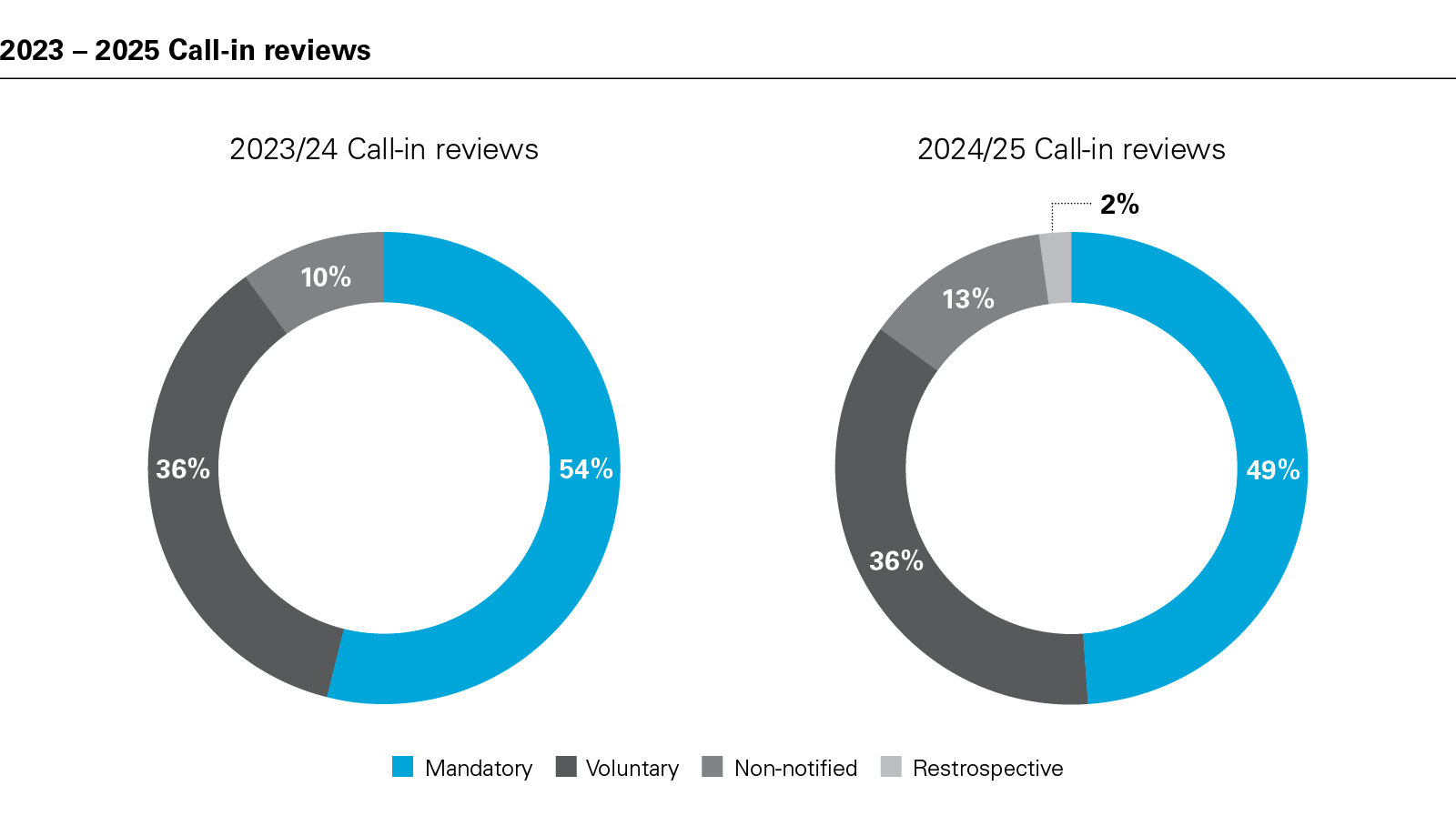

Call-In Review

A call-in notice signifies that a transaction will be subject to a more detailed national security review. This triggers a 30-working day 'assessment period' (which may be followed by another 45-working day 'additional period', that can be further extended with the notifying party's consent). The issue of a call-in notice signifies that the government has determined that a transaction may present potential for immediate or future harm to the national security of the UK and so requires a more detailed review.

During the Reporting Period, call-in notices increased to 56, compared to 41 during 2023/24. As a proportion of the total number of notifications this is largely consistent with 2023/24, and it remains the case that clearance post-notification remains the norm, with nearly 96% of all notifications received being cleared without call-in review.

The breakdown in terms of the types of notifications that have been deemed to merit call-in review, has also remained largely consistent, with mandatory notifications continuing to account for at least half of all call-ins. The headline for investors, however, is that just over 10% of call-in notices relate to unnotified transactions.

View full image: 2023 – 2025 Call-in reviews (PDF)

View full image: 2023 – 2025 Call-in reviews (PDF)

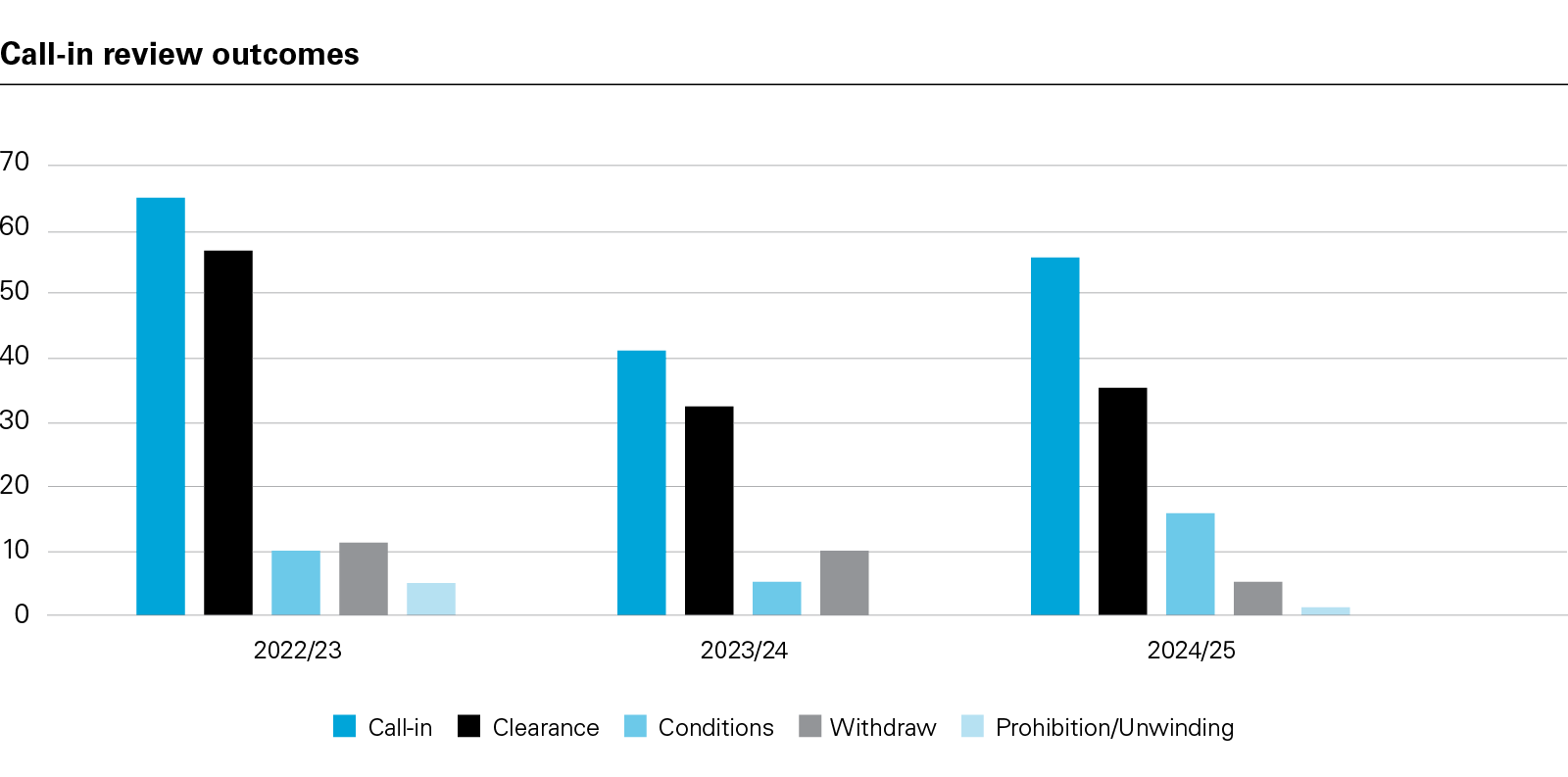

Final Orders: Conditional and Prohibition Decisions

Following a call-in review, there are three potential outcomes:

- A final notification confirming no further action will be taken and so effectively clearing the deal unconditionally;

- A final order imposing conditions; or

- A final order prohibiting the transaction (or, in the case of unnotified deals that have already been completed, unwinding the deal).

In 2023/24 there were five final orders issued, all of which imposed conditions; no deals were blocked or unwound. In 2024/25 this rose to 17, with all but one (which required a divestment) imposing conditions. This does not account for the extra five final orders that have been issued since 31 March 2025. The likelihood of a final order following call-in review has increased noticeably: just 12% of call-in reviews resulted in conditions 2023/24 compared to over 30% resulting in conditions or prohibition in 2024/25.

View full image: Call-in review outcomes (PDF)

View full image: Call-in review outcomes (PDF)

Sectoral Focus

The Report also provides a breakdown of the sectors triggering the most mandatory notifications, voluntary notifications, call-ins, final notifications (i.e., clearance after call-in), and final orders (i.e., the imposition of conditions or prohibition). Notifications were most common in relation to defence, accounting for over half with 56% of notifications received. This is no doubt a function of the broad scope of the Defence sector definitions, which are capable of capturing even indirect subcontractors to the Ministry of Defence, operating in a broad range of activities.

Other prominent sectors included Critical Suppliers to Government (21%), Military & Dual-use (19%), Artificial Intelligence (15%), and Advanced Materials and Data Infrastructure (with 14% each). Transactions can be notified based on multiple sectors, with, for example, the Defence and Military & Dual-use sectors often triggering simultaneously, so the figures by sector will be somewhat skewed due to the overlapping definitions.

Unsurprisingly, a similar sectoral focus is also evident in the sectors most subject to call-in with Defence again accounting for the majority (36%), followed by Military and Dual-use (29%), and Advanced Materials (27%). There are discrete outliers: the Energy sector accounted for just 9% of notifications, for example, but 25% of all call-in reviews.

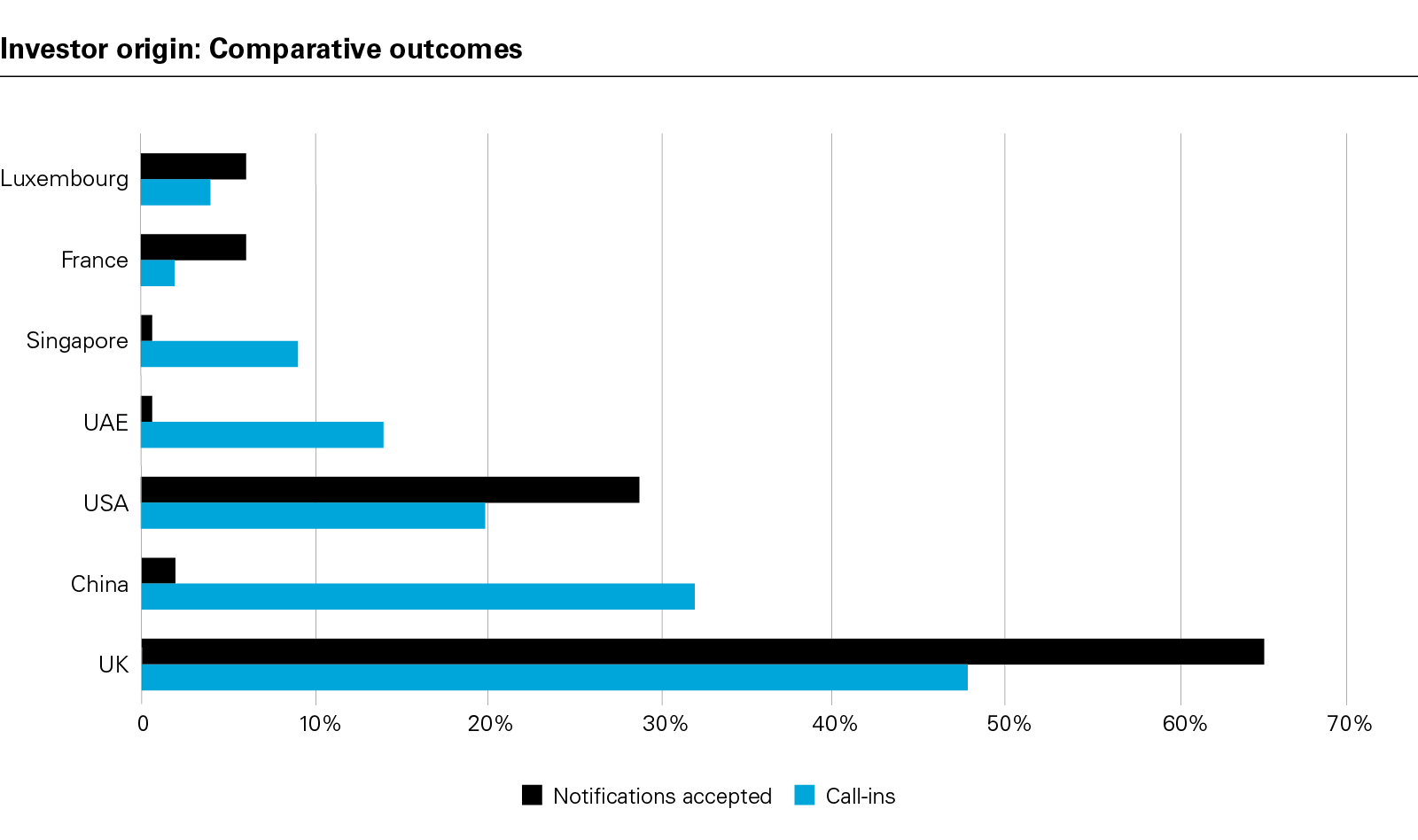

Investor Origin

Unlike many other FDI regimes, the NSIA is agnostic as to an investor's origin when it comes to the obligation to notify a transaction. UK investors are, therefore, subject to the same notification requirements as overseas investors. Indeed, investors from the UK represent both the highest number of notifications received and the highest number of call-in reviews, as well as receiving 11 final orders. Acquirers from China, however, while representing just 2% of notifications received, accounted for 32% of call-ins and Chinese investors received 7 final orders.

View full image: Investor origin: Comparative outcomes (PDF)

View full image: Investor origin: Comparative outcomes (PDF)

Penalties

The NSIA sets out various offences, including the completion of a notifiable transaction without approval. Such offences can attract penalties of up to £10 million or 5% of turnover (whichever is the higher). The NSIA Report states that, once again, no penalties were issued during the NSIA Reporting Period. Encouragingly, even though the government reports identifying 60 offences of completing a notifiable acquisition without approval, no penalties were issued, with the Cabinet Office instead satisfied to procure assurances that steps had been taken to prevent any recurrence.

This means that since its introduction in January 2022, no penalty has been imposed under the NSIA for failing to notify a transaction that was subject to a mandatory filing. It would be wrong to interpret that as the government not being vigilant but, rather, seeking to foster an attractive investment environment by only taking remedial action (e.g., imposing conditions) if deemed necessary to protect national security interests.

…as this Annual Report makes clear, our focus will always be on fostering a business environment conducive to growth. One where inward investment is welcomed and our businesses feel protected. The National Security Investment Act helps make that possible.

What's next? Proposed changes to the NSIA

Internal Restructures and the Appointment of Liquidators

Encouragingly, the government has announced its intention to "reduce unnecessary red tape for businesses" by exempting the appointment of liquidators and certain internal restructures from mandatory notification, although which internal restructures will qualify for this exemption is still being decided.

Changes to the Sensitive Sectors

The government is also consulting on changes to the NSIA Regulations, which set the scope of activities that require mandatory notification. The consultation will run until 14 October 2025.

The consultation will propose amendments to ensure that regulatory requirements remain targeted and proportionate, protecting national security and giving certainty to investors

Department of Business and Trade's UK Industrial Strategy, June 2025

New Sector: Water

As predicted in our last update, the consultation proposes the addition of a new Water sector, capturing all 17 of the regional water and/or sewage monopolies. As drafted, however, changes in ownership to water retailers would not be subject to mandatory notification.

Creation of Standalone Sectors from existing NSIA areas

1. Critical Minerals

Critical Minerals already appears as a sub-sector within the Advanced Materials sector of the existing NSIA Regulations. The proposal being consulted upon would see Critical Minerals migrate to a standalone sector. The new sector would harmonise the list of critical minerals with the Critical Mineral Intelligence's Centre's latest criticality assessment, adding aluminium, borates, hafnium, helium, iron, magnesite, magnesium, manganese, natural graphite, nickel, phosphorous, rare earth elements1, rhodium, silicon, sodium, tin, titanium and zinc to the list. The scope of activities related to Critical Minerals would also be expanded to add extraction, processing and recycling.

2. Semiconductors and Computing Hardware

The consultation proposal would also see Semiconductors move from the Advanced Materials sector into its own standalone sector along with Computing Hardware. The scope of activities would potentially expand significantly, to add activities involving wider design and analysis of semiconductors, chips, and processing units, as well as advanced packaging techniques.

Changes to existing Sectors

1. Advanced Materials

As well as moving Critical Minerals and Semiconductors out of this sector, discrete changes have been proposed to clarify definitions. The proposal would also expand the scope of the advanced 'metal and alloys', 'polymers', 'ceramics', and 'optical devices' captured. There is also an expansion of the activities related to rare earth elements contemplated, which would remain within the Advanced Materials sector.

2. Artificial Intelligence ("AI")

The proposal would definitively remove the use of 'off the shelf' AI from mandatory notification but will add the development or enhancement of non-consumer AI systems and testing of AI systems with specified purposes.

3. Communications

The proposal for the Communications sector would see a minimum turnover threshold of £5 million being introduced for the provision of certain types of associated facilities, and the removal of the current £50 million turnover threshold for activities relates to submarine cable systems and cable landing stations.

4. Critical Suppliers to Government

The Critical Suppliers to Government sector could undergo a significant overhaul. Under the proposal any acquisition target that has a contract with any one of 24 Ministerial Departments for the provision of defined services, which will be expanded to include, amongst others, bookkeeping, payroll processing, recruitment, etc., could be captured where that provision involves access to OFFICIAL – SENSITIVE information. Holding 'List X' Accreditation for government subcontractors would also be replaced as a trigger criterion, with a requirement to have either Facility Security Clearance and/or Industry Personnel Security Assurance.

5. Data Infrastructure

The proposal for the Data Infrastructure sector would also undergo expansion, with the addition of all third party- operated data centres, alongside certain cloud service providers and managed service providers. The proposal would see public sector authorities carved out, however.

6. Energy

The changes proposed to the Energy sector would see holders of a multipurpose interconnector licence included under the mandatory notification activities. The consultation also foresees a reduction to the cumulative capacity threshold (currently 1GW) to 500 MW, which would also apply at every 500MW increment beyond 500MW.

7. Suppliers to the Emergency Services

The proposal being consulted upon would see one discrete addition to this sector by adding any immediate sub-contractor to an entity that supplies emergency services with in-scope goods or services.

8. Synthetic Biology

The Synthetic Biology sector would also receive a discrete addition, with an extra qualifying activity for entities that develop or produce certain types of gene therapy.

1 Two new Rare Earth Elements, lanthanum and promethium, would be added, to sit alongside the existing list of cerium, praseodymium, neodymium, samarium, europium, gadolinium, dysprosium, holmium, erbium, ytterbium, lutetium, scandium, and yttrium.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP