UK FDI | Sector snapshot: Energy - what’s new, what’s not, and what’s next for investors in the UK energy sector?

6 min read

Following the publication of the UK Government's latest Annual Report on the National Security and Investment Act 2021 ("NSIA") and its ongoing consultation on proposals for NSIA reform, we take a look at how energy investments have fared to date and what changes investors in the sector may face under those new proposals.

Our mission is to make Britain the most attractive place for private capital to invest in clean energy. This is not a ‘nice to have’; it is an absolute necessity for our country's energy security and economic future.

Energy Secretary, Ed Miliband MP

The UK government has been clear that in order to meet its clean energy ambitions, unlocking billions in private capital is a pre-requisite. However, investors in the sector must now also navigate the NSIA, which has become a feature of more and more transactions in the UK since its coming into force in January 2022. In the Energy sector, notifications can be mandated for investments in various forms of electricity generation, distribution and transmission, and oil and gas ("O&G") under Schedule 11 (Energy) of the NSIA Regulations.1 The task of the Investment Security Unit ("ISU") in the Cabinet Office, the team responsible for administration of the NSIA regime, therefore, is balancing the UK government's interest in facilitating critical investment in the sector while safeguarding the UK's national interests.

NSIA Operation in the Energy Sector

What types of acquisitions require mandatory notification?

A mandatory notification under the NSIA can only be required in respect of transactions that will involve an Acquirer's shareholder or voting rights in a Target exceeding 25%, 50%, or 75% (for the first time), or which will confer on the Acquirer sufficient rights to secure or prevent the passage of any class of resolution governing the affairs of the Target. These notifications are suspensory, i.e., the deal cannot be closed until clearance is received.2

Other types of acquisition: voluntary notifications and call-in powers

These are not the only kinds of acquisition that can be subject to review by the UK government, however. For example, transactions involving the acquisition of certain rights or interests in real assets do not require mandatory notification but are still considered 'qualifying acquisitions' that are amenable to review by the government under its 'call-in' powers. Via the issue of a 'call-in' notice, the government can initiate a national security review of any qualifying transaction. This power exists for up to five years after closing. In order to enable parties to mitigate this risk, the NSIA also allows for voluntary notifications for these kinds of transactions to secure legal certainty.

The acquisition of "material influence" for the first time

Material influence is a concept that owes its origins to UK merger control and refers to the Acquirer's ability to influence policy relevant to the behaviour of the Target in the marketplace, e.g., management of its business, strategic direction, and/or the Target's ability to achieve its commercial objectives. Such influence may be realised via shareholder or board influence. Material influence is not an objective standard but is assessed on a case-by-case basis. It has been used as the basis for at least six transactions that were ultimately subject to final order following call-in review by the ISU. This included, for example, 'material influence' conferred via the conclusion of a 'strategic relationship' and through the acquisition of a shareholding of 12.8% in a Target.

Acquisition of control over a qualifying asset

An Acquirer is deemed to gain 'control' of a qualifying asset when they acquire a right or interest that allows them to "use the asset" or "use it to a greater extent" than previously, or where they acquire the ability to "direct or control how the asset is used" either for the first time or to a greater extent than previously. This concept has been of particular application in the Energy sector.

From both the cache of final orders that have been published to date, and the Cabinet Office's specific Guidance on the application of the NSIA to new build downstream gas and electricity assets, we now have several examples of how the concept is applied in the sector in practice. All of the following circumstances will be deemed to satisfy the definition:

- Application for a generation licence to Ofgem;

- Application to the National Energy System Operator for a connection agreement to the national grid;

- Participation in a tender round that would enable the realisation of a project. This could include, for example, participation in a Contract for Difference allocation round or a Capacity Market auction; and

- The acquisition of 'development rights' for a generation project.

Given the risks associated with timeline delays to these key milestones (particularly connection agreements), legal certainty considerations become particularly relevant for project-financed assets in development. This perhaps at least partially accounts for the 23 voluntary notifications submitted in the Energy sector between 31 March 2024 and 1 April 2025, according to statistics released with the latest Annual Report on the NSIA.

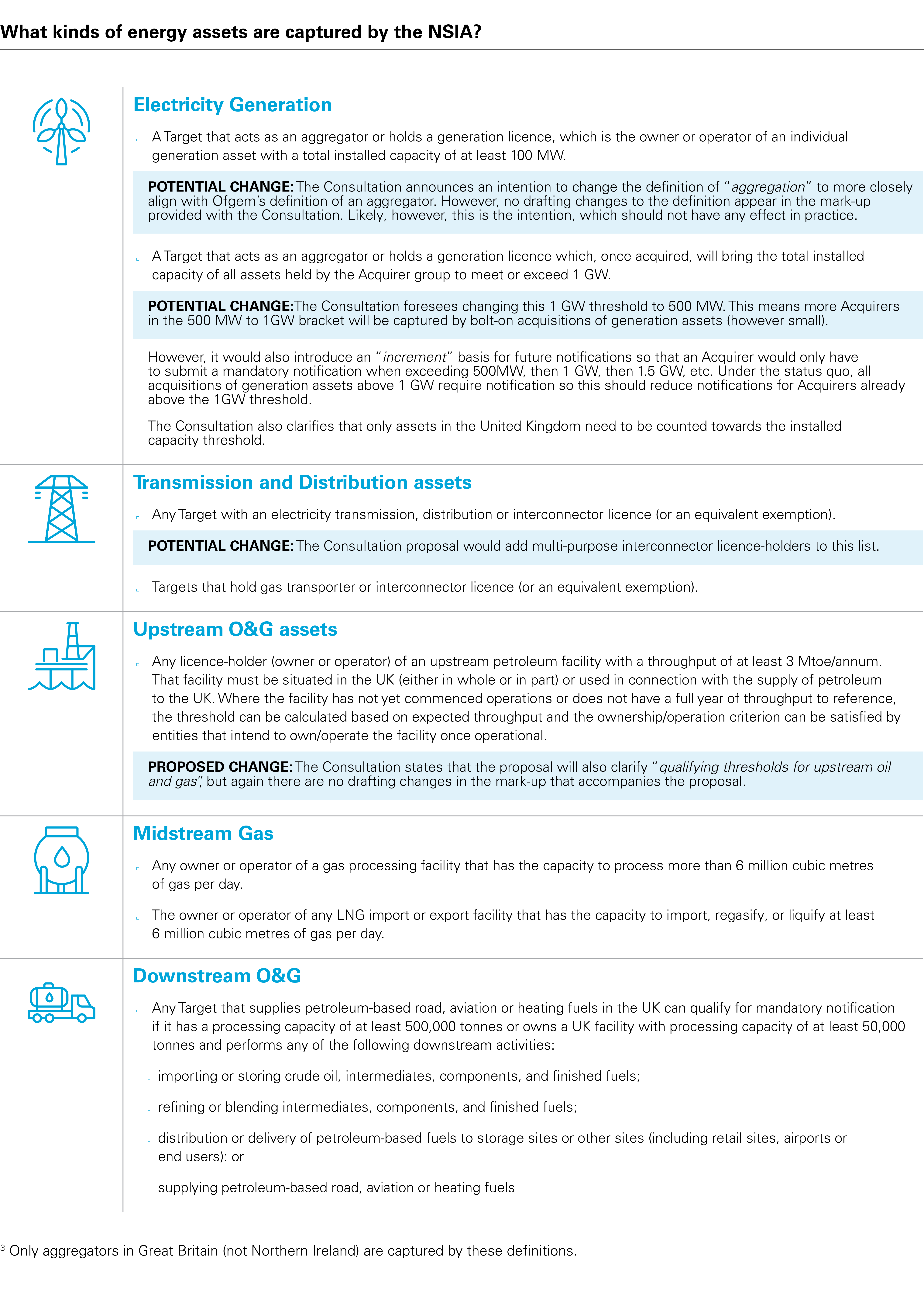

What kinds of energy assets are captured by the NSIA?

In terms of which activities in the Energy sector mandate notification, these can broadly be broken down into the following categories: electricity generation, distribution and transmission, upstream O&G, midstream gas, and downstream O&G. The limits of these activities, along with the changes contemplated by the Government's latest consultation on changes to them, are set out below. A qualifying acquisition in any of these can require a mandatory notification.

View full image: What kinds of energy assets are captured by the NSIA? (PDF)

View full image: What kinds of energy assets are captured by the NSIA? (PDF)

The government estimates that these changes will have no net effect on the number of mandatory notifications in the Energy sector. That remains to be seen. Certainly, the introduction of the 500 MW 'increment' model for acquisitions by Acquirer's with groups that already hold installed capacity in excess of 1GW should reduce their need to make multiple notifications, but the reduction in the threshold to 500MW in the first instance may well bring many more entities active in generation into scope.

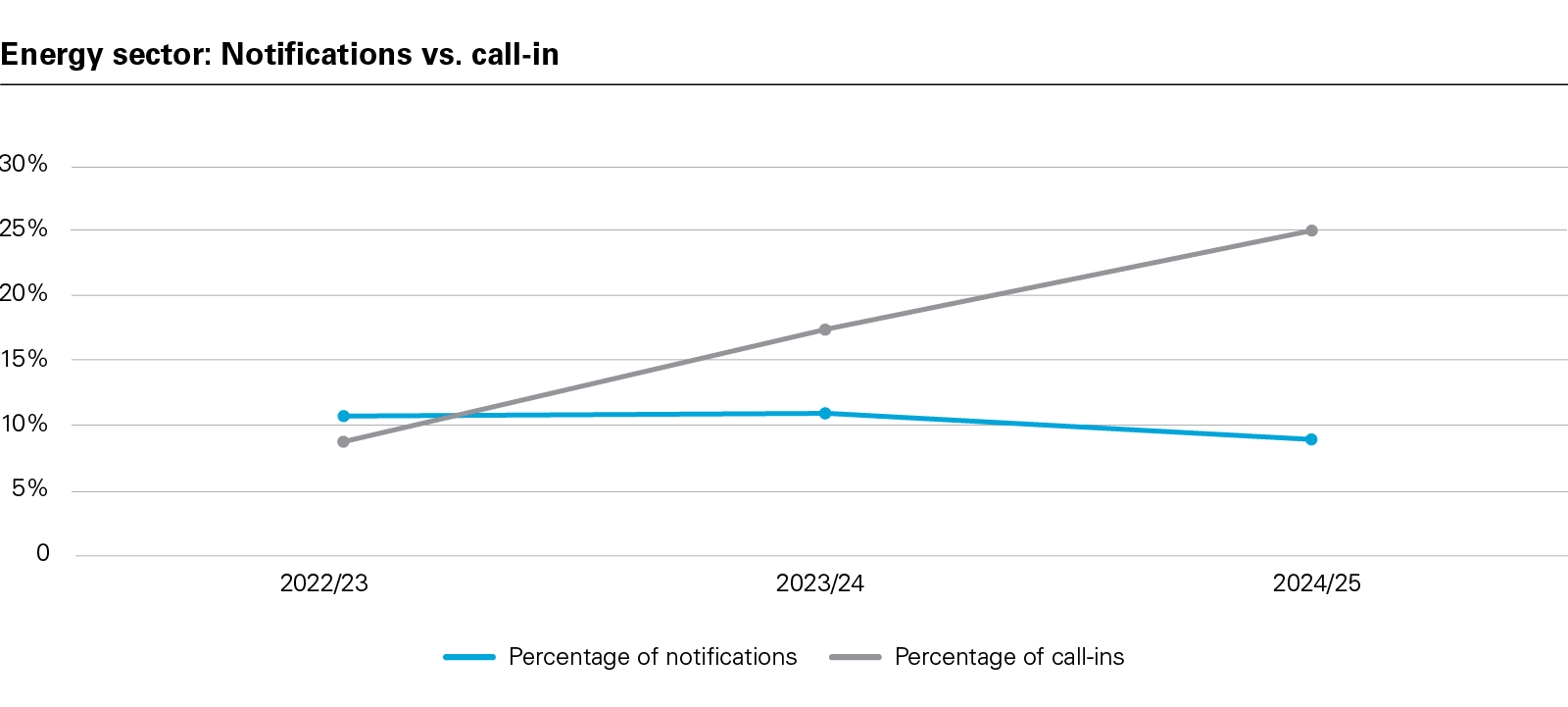

NSIA Notifications in the Energy Sector

Although notifications in the sector have remained relatively steady at around 10% of all notifications received, there is a clear trend in call-in notices in the sector increasing. In 2024/25, the sector accounted for 25% of all call-ins – meaning around 14 call-in notices were issued to energy investors during the Reporting Period.

View full image: Energy sector: Notifications vs. call-in (PDF)

View full image: Energy sector: Notifications vs. call-in (PDF)

Following a call-in review, there are three potential outcomes:

- A final notification confirming no further action will be taken;

- A final order prohibiting the transaction (or unwinding a deal that has already completed); or

- A final order imposing conditions;

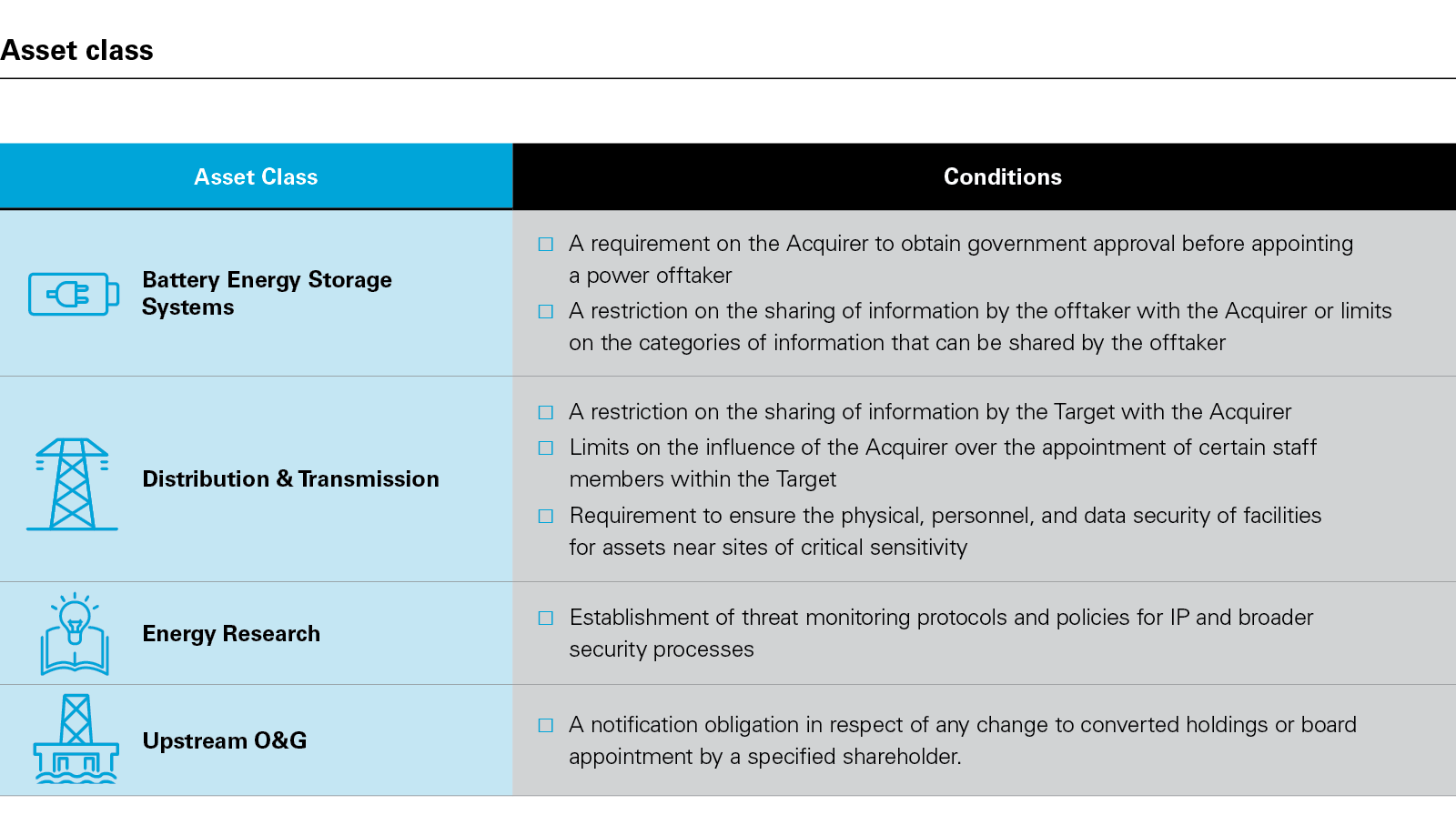

In 2024/25 nearly 70% of all deals subject to call-in review across all sectors were cleared unconditionally via a final notification (although this compares with 88% in 2023/24). No Energy sector deal has been prohibited under the NSIA to date, but eight transactions have been subject to conditions. While the NSIA Report publishes statistics for the sector, final orders are minimal in detail and will not typically disclose the sensitive sector under which the transaction was reviewed. Nevertheless, it is discernible from the minimal details available that final orders arose from transactions within the sector – these give a useful indication of the kinds of conditions that the ISU has considered appropriate since the NSIA came into force. An illustrative sample of these by asset class is extracted below.

View full image: Asset class (PDF)

View full image: Asset class (PDF)

1 Investments in nuclear installations can also fall within the NSIA's auspices under Schedule 4 (Civil Nuclear).

2 Where an investor fails to submit a notification a mandatory notification even though one was required, there is an option to submit a Retrospective Validation Application, which allows the investor to remedy the failure and so preserve the transaction from potential invalidation.

3 Only aggregators in Great Britain (not Northern Ireland) are captured by these definitions.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP