Green hydrogen will play important roles in Africa's transition to renewable energy and as an exportable commodity. But is the current focus on the areas that will deliver the most value for Africa and its people? Carina Radford and Alex Field explain green hydrogen's potential for diversifying the continent's industrial base and contributing to bridging Africa's energy deficit—as well as for growing exports.

Disputes related to climate change are growing steadily, but most so far have been in North America, Europe and Australia. Markus Burianski and Federico Parise Kuhnle explain why these will likely ramp up in Africa, too. Disputes could involve liability and compensation for damages caused by climate change, how environmental regulations aimed at mitigating climate change are implemented and enforced, and investment disputes.

Sustainable finance is a perennially important topic in Africa, as is sovereign debt. Olga Fedosova and Max Turner combine these two, explaining Gabon's Blue Bond issuance (the first on the African mainland), exploring lessons from that innovative and important debt-for-nature swap, and outlining how such swaps might be deployed elsewhere in Africa.

In our third article, Marcus Booth and James Ateh interview Sam Senbanjo, Managing Director at private equity fund A.P. Moller Capital, about his experiences in Africa. The interview covers A.P. Moller Capital activities in Africa (including its approach to ESG), prospects for African PE generally and some very practical pointers for those considering investing on the continent.

The Koeberg Nuclear Power Station in South Africa is currently the only nuclear power station in Africa, but that is changing. The International Atomic Energy Agency (IAEA) forecasts between a five-fold and ten-fold increase in African nuclear power generation by 2050, compared to 2022. Ximena Vasquez-Maignan explains the process defined by the IAEA for developing new nuclear power stations, and the challenges involved.

Our final article examines exciting new oil & gas discoveries in Namibia. These are of a scale that could transform Namibia's economy and the livelihoods of its people, propelling the country to middle-income status. Gary Felthun and Tariq Kajee, collaborating with Irvin Titus of leading Namibian law firm Koep, explore implications for foreign direct investment into Namibia—especially into green hydrogen and mining projects.

Our eleventh edition of Africa Focus, delves into key aspects of Africa’s shift towards renewable energy and sustainable economic growth

Green hydrogen in Africa: A continent of possibilities?

There is huge interest in the development of green hydrogen projects in Africa, building on the continent's vast potential for renewable energy. But are these the right projects to achieve success, both for investors and for African populations?

A new wave of African climate change disputes on the horizon

Africa's heavy reliance on fossil fuels for economic growth, set against the backdrop of strict environmental regulations and emissions-reduction targets, creates a perfect storm of factors that could give rise to climate change-related disputes in Africa.

Debt-for-nature swaps: A viable alternative for vulnerable economies amid global challenges

Debt-for-nature swaps convert debts of low- and middle-income countries, unable to service external debts, into commitments related to nature. In the face of recent geopolitical tensions, economic challenges and growing environmental concerns, DFNSs offer a promising alternative to traditional financing sources when access to international capital markets or commercial loans is limited.

In an exclusive interview, Marcus Booth and James Ateh discuss Africa's infrastructure, renewable energy and investment landscape with Sam Senbanjo, A.P. Moller Capital.

Africa’s quest for universal electricity access and net- zero through small modular reactors

Africa needs to significantly increase its electricity production to ensure universal access to its expanding population. It also needs to achieve net-zero emissions by 2050. Small modular reactors (SMRs) offer a potentially accessible and sustainable solution, but financing and regulatory hurdles must be addressed for widespread adoption.

Namibia's regulatory environment, stable economy and rich mineral resources make it an attractive investment destination in Africa. Investors should view Namibia as a key emerging investment hub on the continent.

Debt-for-nature swaps: A viable alternative for vulnerable economies amid global challenges

Debt-for-nature swaps convert debts of low- and middle-income countries, unable to service external debts, into commitments related to nature. In the face of recent geopolitical tensions, economic challenges and growing environmental concerns, DFNSs offer a promising alternative to traditional financing sources when access to international capital markets or commercial loans is limited.

The concept of debt-for-nature swaps (DFNSs) was first introduced in the 1980s for conversion of debt owed to creditors by developing countries that were unable to service their external debt. Over the past 30 years, a whole range of different debt treatment operations has been developed under the umbrella of DFNSs involving both commercial debt and debt to official creditors that could be swapped for commitments related to nature. Since the early 2000s and until several years ago, DFNSs have not had much traction, partially due to a shift toward supporting developing countries through various initiatives such as HIPC/MDRI or DSSI, and partially due to a fairly long period of low interest rates. However, recent geopolitical, economic and climate changes brought the DFNSs back into the spotlight and here is why:

In the current global economic context, sovereigns face multiple geopolitical pressures (such as military conflicts in Ukraine and Israel), economic challenges (post-COVID-19 financial impact, high interest rates, inflation and food prices) and environmental concerns, including climate change and biodiversity loss. The low- and middle-income countries are more rapidly and more severely exposed to these challenges due to their lower resilience and higher socio-economic vulnerability. For these countries, DFNSs might serve as a promising alternative to traditional sources of financing at times when access to the international capital markets (Eurobonds) or commercial loan markets might be limited or even closed to them.

Broadly speaking, DFNSs represent financial transactions aimed at refinancing a country's debt at lower relative interest rates in return for a commitment to spend a portion of savings on nature conservation. While DFNSs can take different forms, the purpose of this article is to specifically look into the Gabonese Republic's debt-for-nature swap transaction in August 2023 and the lessons learned from it.

The first-of-its-kind in mainland Africa DFNS initiative echoes the stories of Belize, the Seychelles and Barbados or, most recently, Ecuador, which have successfully implemented DFNSs to free up financial resources to support nature- and conservation-related projects.

Gabon's US$500 million DFNS represents a complex set of transactions, including new money, marine conservation and refinancing components.

The new money

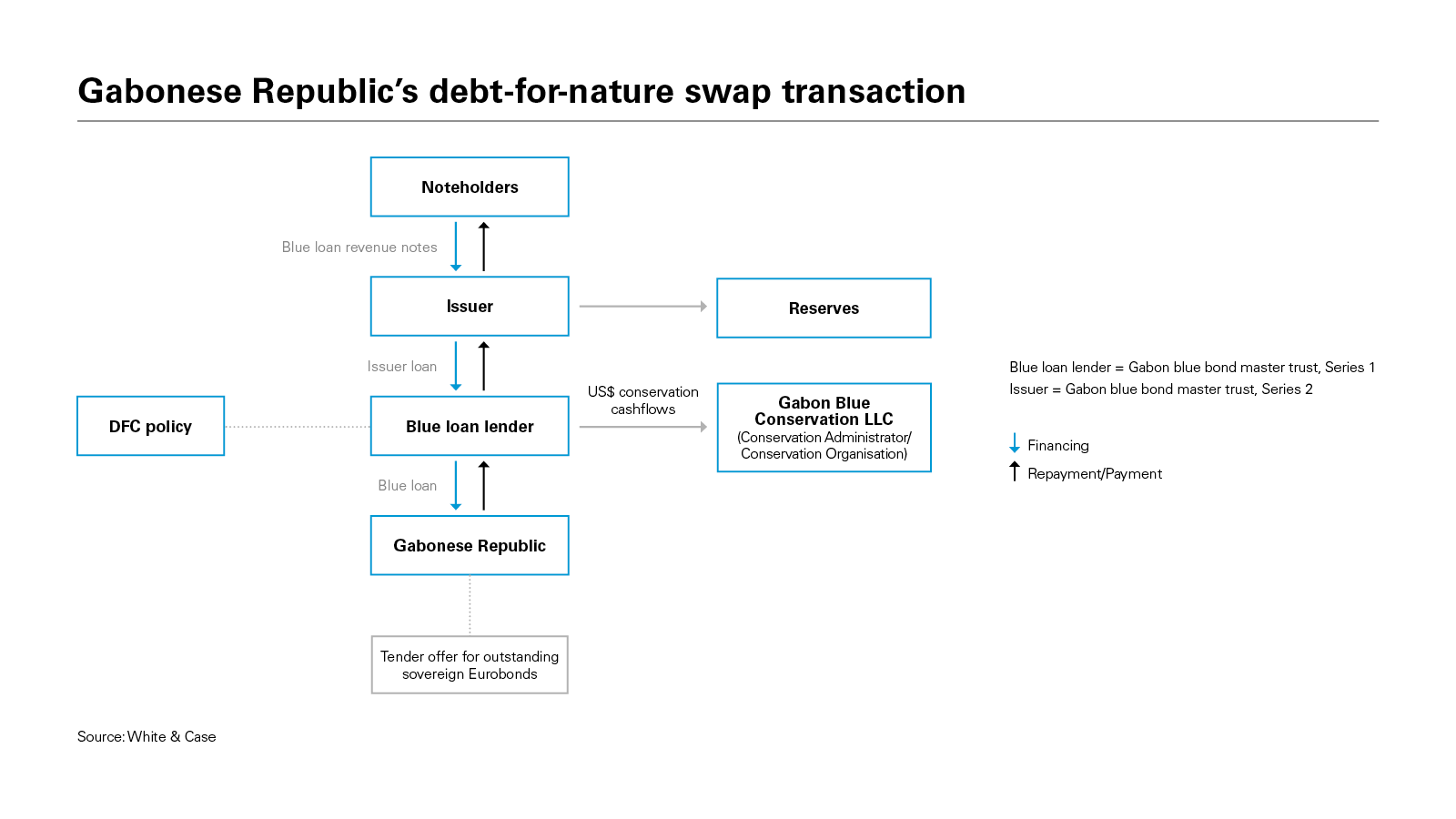

The transaction was structured as an issuance of US$500 million amortizing notes due 2038 by Gabon Blue Bond Master Trust Series 2, the proceeds of which were used to fund a loan to Gabon Blue Bond Master Trust Series 1. The blue loan lender used the proceeds of the issuer loan to fund a 15-year US$500 million loan to Gabon under a loan agreement.

The blue bond issuance was arranged by Bank of America. Unlike previous DFNSs, the blue bonds were marketed and issued in the context of a Rule 144A/Regulation S offering aimed at institutional investors in the primary market (rather than a "bought deal" that is subsequently privately placed by the arranging bank). In this sense, the Gabon DFNS demonstrated that such deals can be successfully syndicated in a similar manner

to traditional Eurobonds and offered to a wide spectrum of new money investors.

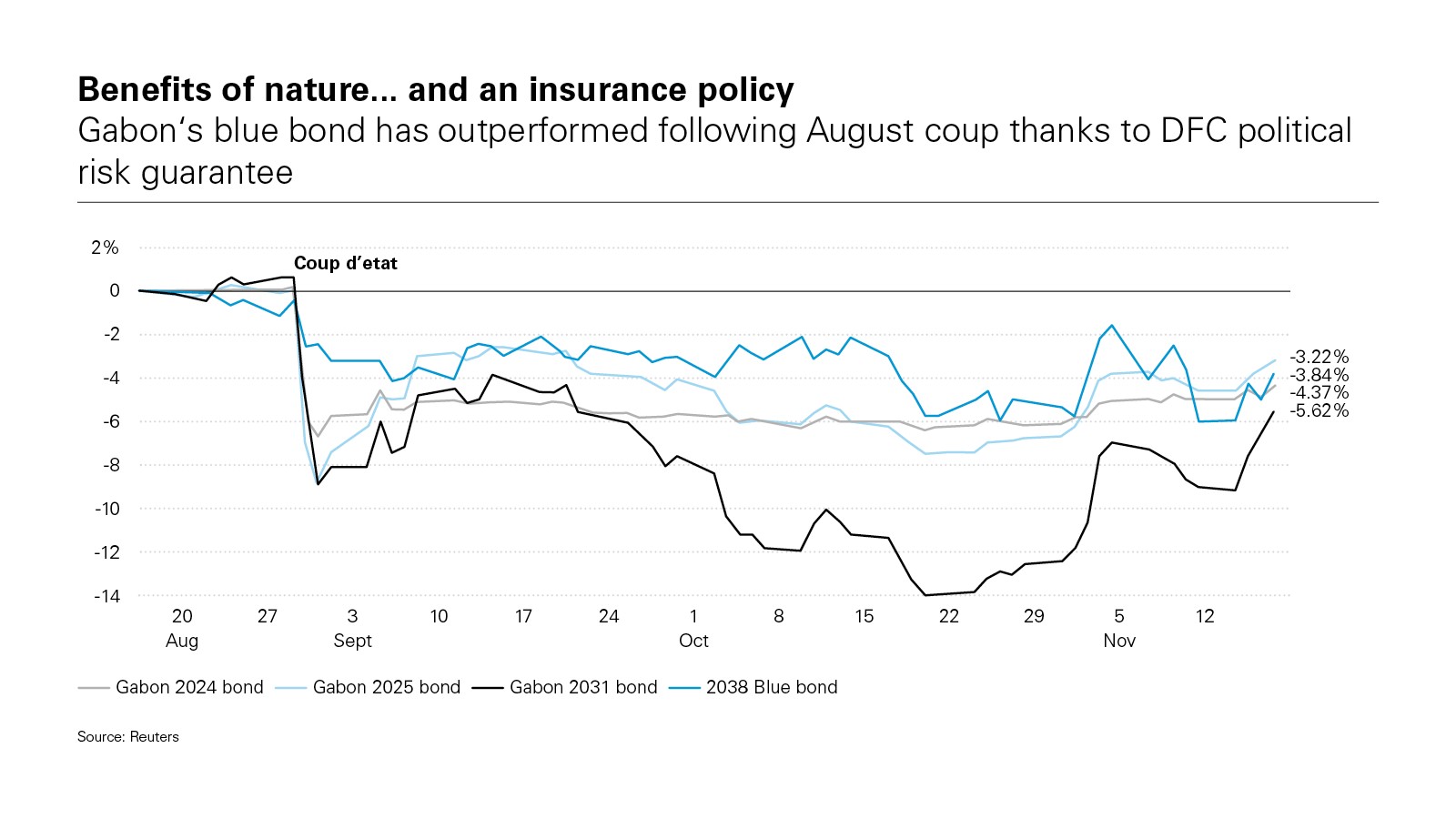

Central to the success of this transaction was the political risk insurance (PRI) provided by the US International Development Finance Corporation (DFC). The PRI is a specific DFC credit enhancement product that represents an insurance contract issued for the benefit of the blue loan lender and limited to non-payment of an eventual arbitral award and denial of recourse. The DFC PRI coverage is limited to the principal amount of the blue loan and seven months of interest thereunder, but does not include default interest, indemnity payments or make-whole amounts under the blue loan. This credit enhancement enabled the blue bonds to receive an Aa2 rating (far higher than Gabon's sovereign debt rating of Caa1), resulting in a lower coupon on the blue bonds and consequently a lower coupon on the blue loan for Gabon compared to prevailing commercial lending conditions that would have applied to the sovereign borrower.

Debt-for-nature-swaps (DFNSs) could serve as a promising alternative to traditional sources of financing at times when access to the international capital markets (Eurobonds) or commercial loan markets might be limited to them

Gabon's interest payments under the blue loan are divided into three components: financial interest, the largest component, which is applied to payments owed under the blue bonds; conservation interest, which generates funds for conservation fund activities; and endowment interest, which is used to fund the endowment account for long-term conservation projects. The Gabon DFNS transaction effectively represents a pass-through structure whereby Gabon's payments of financial interest and principal under the blue loan are passed via the blue loan lender to the issuer and ultimately to the holders of the blue bonds. The protection of blue bond investors is enhanced by ensuring the bankruptcy remoteness of the issuer and, in the case of a default of Gabon, by the DFC PRI, as the benefit of any pay-out under the policy is effectively passed on to the blue bond investors. It is important to note that a default under the blue loan will not automatically accelerate the blue bond. Instead, it will start a 24-month moratorium on the blue bond interest payment during which period steps will be taken to activate the DFC PRI. A specifically created reserve account funded by Gabon is designed to provide additional protection to the blue bond investors as, under certain conditions, its funds may be used to make blue bond interest payments during the moratorium period.

Gabonese Republic’s debt-for-nature swap transaction is Africa’s first

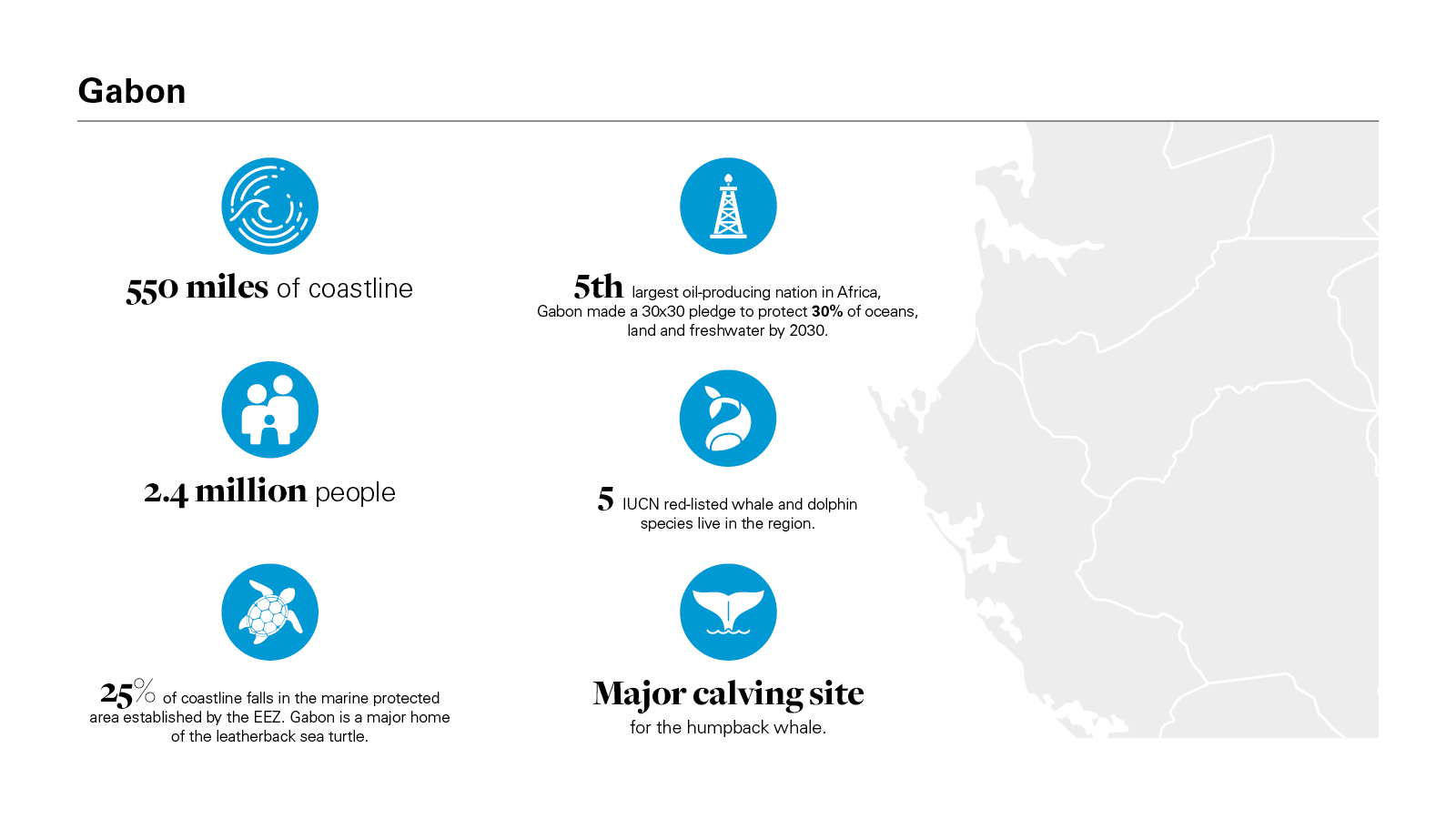

Gabon is an equatorial nation on the west coast of Africa with a diverse coastal and marine ecosystem, including a breeding ground for humpback whales and home to more than 120 of the world's most endangered or threatened marine species. Traditionally focused on oil production as a main driver of its economy, Gabon has shown strong interest in conservation in recent years, notably with the launch of the "Gabon Bleu" marine conservation project in 2013, which has since been complemented by other conservation initiatives.

The Gabon DFNS is designed to further support the country's conservation initiatives in two ways: (i) by committing to generate approximately US$125 million worth of dedicated conservation funding over the life of the blue loan in the form of the conservation interest component and the endowment interest component; and (ii) by undertaking compliance with certain conservation commitments under the blue loan agreement as further described below.

The Nature Conservancy (TNC) played a key role in providing structuring assistance in the context of the Gabon DFNS and helping develop the conservation milestones under the blue loan. In addition, during the life of the blue loan, TNC will oversee Gabon's compliance with conservation milestones, supervise the endowment account funding and oversee the activities of Fonds de Preservation de la Biodiversité au Gabon Inc. (Conservation Fund) founded by Gabon and TNC.

In terms of conservation funding, Gabon committed to make periodic payments during the life of the blue loan to Gabon Blue Conservation, LLC (Conservation Organisation). These payments constitute the conservation interest component to generate funds for the Conservation Fund activities and the endowment interest component that will be used by the Conservation Organisation to fund the endowment account. The endowment account is intended to continue to fund Conservation Fund initiatives after the blue loan is repaid to provide long-term support to marine conservation, nature-based strategies for climate adaptation and sustainable economic development in Gabon. Both the conservation and endowment interest components represent savings from the refinancing and credit enhancement under the DFNS.

The Gabon DFNS will also help finance a marine spatial plan to increase the area of ocean under protection, improve management in currently protected areas and all new protected areas, and support Gabon's sustainable blue economy. In addition, this project will help Gabon strengthen and enforce regulations in its fishing industry, which has been weakened by illegal, unreported and unregulated fishing. These objectives are represented by the conservation undertakings (Conservation Milestones) under the blue loan, each of which has a pre-defined framework and timetable.

In the event of non-compliance with the Conservation Milestones, Gabon will be required to make periodic payments to the blue loan lender which, if the non-compliance is eventually remedied, will be used to finance Gabon's obligations to pay the remaining conservation interest under the blue loan. In addition, any breach of certain Conservation Milestones beyond defined grace periods may result in a major commitment default, which will be an event of default under the Blue Loan Agreement and, consequently, could trigger cross-default on Gabon's other external debt instruments. Therefore, the Gabon DFNS contains strong financial incentives to respect the Conservation Milestones. Furthermore, these incentives are arguably stronger compared to those contained in classic sustainability-linked instruments, where a failure to reach the pre-defined sustainability performance targets would not trigger an event of default and would normally result in a coupon step-up or, more rarely, increased principal.

Refinancing via the tender offer

The proceeds of the blue loan were mainly used by Gabon to finance its tender offer for a portion of its outstanding US$700 million 6.950% amortizing notes due 2025, US$1 billion 6.625% amortising notes due February 2031 and US$800 million 7.000% amortising notes due November 2031 (Notes). Gabon purchased the Notes at a discount to par for a total amount of approximately US$442 million.

Lessons learned for future debt-for-nature swaps in Africa

Gabon's DFNS set a precedent for other African countries that have both sovereign debt trading at discount and significant environmental priorities. It has also provided valuable insights for the successful execution of similar transactions in future.

Total value of Gabon’s first debt-for-nature swap transaction

DFNS use case

The DFNS remains a relatively niche product for now. It is widely acknowledged that DFNSs cannot replace a comprehensive restructuring for countries with unsustainable debt levels unless the DFNS is able to refinance a much larger portion of the sovereign's outstanding debt while still generating meaningful savings on interest expense. In addition, DFNSs may not be the most cost- and time-efficient method to tackle challenging conservation projects compared to concessional loans and grants. However, grants and concessional loans are fairly limited, particularly for middle-income countries that normally do not qualify for grants, while the need for nature financing remains high.

The most suitable candidates for a DFNS transaction would appear to be sovereigns with credible nature projects and debt trading at significant discount, but not necessarily close to restructuring. The buyback of existing debt at a discount and a lower new money interest rate procured by credit enhancement help generate savings and can have a positive impact both for a sovereign's public debt management and conservation agenda. For instance, in the cases of Belize and Ecuador, their respective bonds traded at a fairly significant discount, which translated into a higher amount of pure buyback-related savings under their DFNSs.

However, Gabon's DFNS demonstrated that it is not all about buyback discount and that this product can gain traction well beyond distressed debt situations. Whether a DFSN is the right debt management solution ultimately comes down to a policy analysis of a given country. In particular, access to new money in a complex market, maximizing the credit enhancement benefits via coupon savings, and dedicating funds to a conservation agenda could make DFNSs attractive to a wide range of sovereigns.

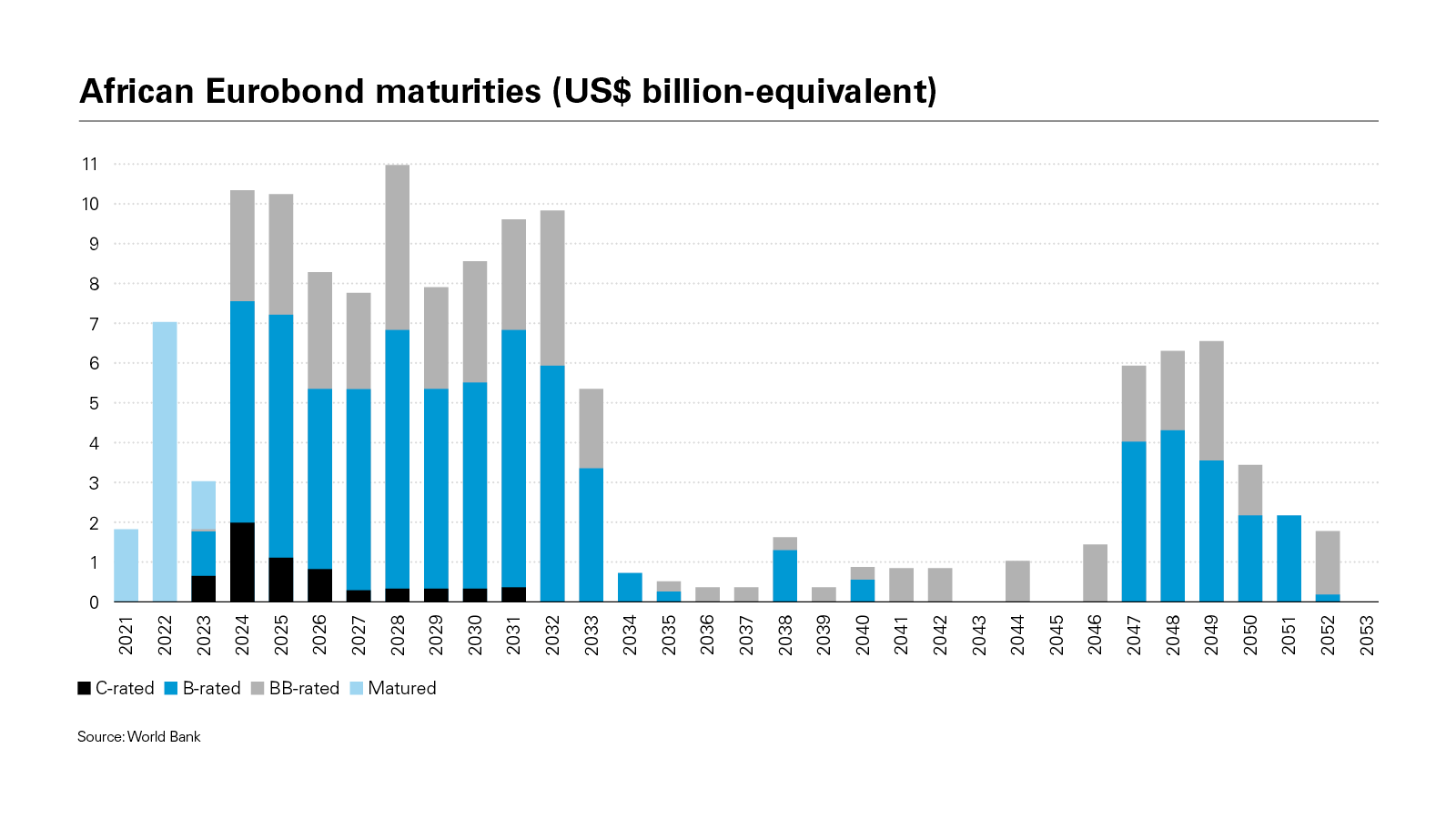

In Africa specifically, 2024 and 2025 are expected to be years of sovereign Eurobond maturity spikes in the context of an increasing level of distressed debt situations. In addition, many of these countries are in tropical areas severely impacted by climate change. While DFNSs are unlikely to be a silver bullet to address debt and climate challenges, they can certainly be an arrow in the quiver of refinancing options,

and present an attractive opportunity for both non-distressed and distressed sovereigns.

Teams, timing and costs

A DFNS is a complex transaction that involves multiple parties (the sovereign, the non-governmental entity (NGO) helping to structure the conservation aspects, the investment banks that will place the bonds with investors, the credit enhancement providers, and legal, financial and other advisers, as well as the creation of various special purpose vehicles and dedicated funds). The necessity of careful calibration of financial, conservation and legal elements and negotiations between multiple stakeholders make the execution costly and long. A DFNS can easily take several years from inception to closing.

At the sovereign level, it is important to have a dedicated team for a project that typically involves both the ministry of finance and ministry of environment to ensure full coordination of the country's financial and conservation objectives.

Success of the transaction heavily depends on an experienced and credible NGO. So far, TNC has been very active in this area, leading the DFNSs of Barbados, Belize and Gabon. Pew Charitable Trusts led the Ecuador DFNS. The choice of the credit enhancement is also a critical decision, affecting the structuring, documentation and marketing of the transaction. DFC provided credit enhancement in Belize, Ecuador and Gabon, while the Inter- American Development Bank served this role in the Ecuador and Barbados DFNSs. For DFNSs to have a real impact on both conservation and debt management generally, it will need to be scaled upward. Involvement of a wider range of NGOs and credit enhancement providers could help bring this financial product to a wider pool of potential borrowers and investors.

Accountability and transparency should be the cornerstones of a DFNS. As noted by the OECD, debt swap facilities should be centers of "professional excellence," in order to maintain creditors' trust and, eventually, attract additional financing.

In this sense, Gabon's deal set a good standard for conservation governance. Under the Gabon DFNS, conservation funding is managed by the Gabonese Conservation Fund founded by Gabon and TNC. The Conservation Fund is subject to clear governance rules to ensure its independence from the founders, in particular the sovereign, transparent decision-making and allocation of funds, and exclusive focus on the conservation projects in and for the benefit of the country, with the participation of independent experts and stakeholders as well as the involvement of the Gabonese nationals.

1980s

The concept of debt-for-nature swaps (DFNSs) was first introduced in the 1980s

To further increase the transparency and credibility of future DFNS transactions, a sovereign could introduce public reporting on its progress achieving the Conservation Milestones, similar to the approach taken for ESG use-of-proceeds or sustainability-linked instruments.

Clear labeling

As with any financial product that is nature- or climate-related, it is important to pay specific attention to appropriate labeling. In particular, DFNS terminology applies terms such as "blue bond" and "blue loan," alluding to the marine conservation focus (or other similar terms depending on the particular conservation or social-interest focus).

However, it is important to differentiate these products from use-of-proceeds bonds, including traditional "blue bonds," as defined in the September 2023 ICMA Bonds to Finance the Sustainable Blue Economy, a Practitioner's Guide. While DFNS documentation is very clear on the fact that the proceeds of the new money component will be used to refinance existing debt (and not for conservation projects), and that conservation activities will be financed purely through interest expense savings from the lower coupon, references to "blue bond" and "blue loan" in the context of a DFNS may lead to confusion among investors and other stakeholders, and may need to be revisited going forward.

Unlocking the potential of debt-for-nature swaps

Debt-for-nature swaps are not a universal solution for distressed debt countries, some of which may require a traditional restructuring. Nor can DFNSs offer the most cost-effective response to climate changes and biodiversity loss. But they can serve as a strong complementary instrument to address both debt and climate challenges simultaneously, especially in a context where grants are not forthcoming and debt relief is not necessarily on the table. In this sense, the Gabon DFNS could, and hopefully will, serve as an inspiration for other African nations seeking to tackle their debt burdens while prioritizing conservation.

The next logical steps in the evolution of DFNSs would be their scaling-up through an increased number of deals, volume of debt refinanced and attraction of a wider pool of NGOs, credit enhancement providers, and private and official sector creditors. In addition, DFNSs can be further expanded to address "debt for health," "debt for education," "debt for climate" or, as proposed by the IMF, structured around broad climate and environmental goals such as de-carbonizing the energy industry or investing in adaptation, and linking swaps to simple-to-monitor metrics such as carbon emissions, deforestation or ocean exploitation.

It remains to be seen whether DFNSs will continue their momentum and evolve further, but in the current economic and climate context, there is definitely a strong case for them among the African sovereigns and beyond!

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Benefits of nature... and an insurance policy (PDF)

View full image: Benefits of nature... and an insurance policy (PDF)

View full image: Gabon (PDF)

View full image: Gabon (PDF)

View full image: Gabonese Republic’s debt-for-nature swap transaction (PDF)

View full image: Gabonese Republic’s debt-for-nature swap transaction (PDF)

View full image: African Eurobond maturities (US$ billion-equivalent) (PDF)

View full image: African Eurobond maturities (US$ billion-equivalent) (PDF)