Efforts to decarbonize the steel industry are unfolding against a backdrop of familiar challenges and shifting global priorities. While technological advancements and regulatory initiatives are creating new possibilities for low-carbon steel, progress remains uneven and often constrained by economic realities, energy costs and evolving geopolitical interests, even where governments express support for greener production. Against this complex landscape, industry participants are navigating both opportunities and obstacles as the sector looks to grow and scale up a viable green steel ecosystem.

Technology solutions for low-carbon steel

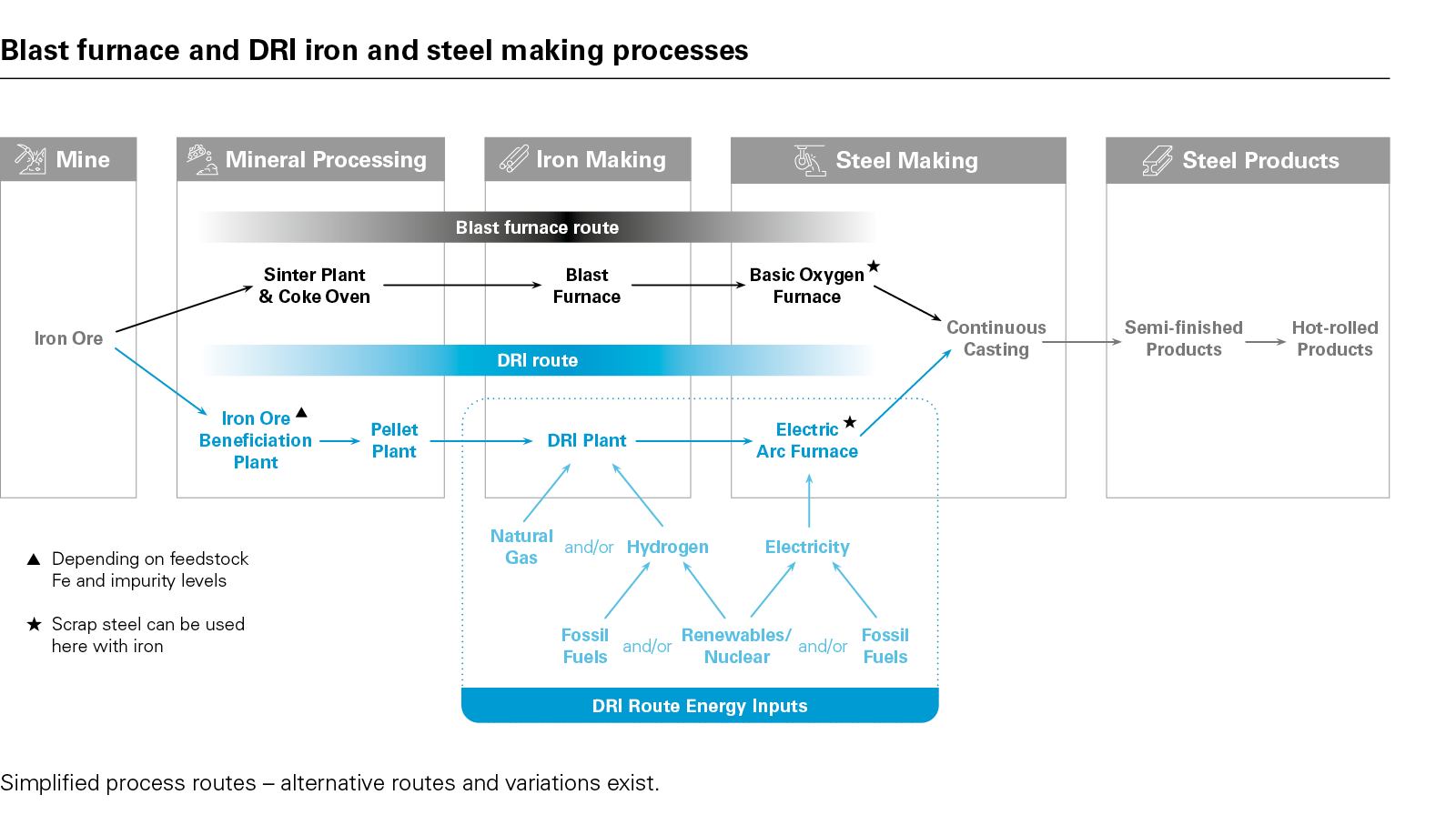

Hydrogen based DRI facilities could potentially curb emissions by up to 90%

Source: OECD

Recent IEA estimates are that steel production contributes more than 8 percent of all annual global carbon dioxide emissions, making it one of the globe's most emitting sectors. Due to the widespread use of coking coal in the blast furnace iron-making process, steel production has generally been classified as a hard to abate sector. However, technologies do exist to produce steel with significantly lower emissions than the traditional blast furnace route, and projects using these technologies are being developed, particularly as more attention and investment is focused on the sector.

The direct reduced iron (DRI) process, where a reducing gas is used to produce sponge iron from iron ore, has emerged as the front-runner technology for low-carbon steel production. First conceived in the late 1960s as an alternative steel-making process for areas short of suitable coking coal, the MIDREX® Process remains the dominant DRI technology, and is experiencing somewhat of a renaissance, due to its use of natural gas instead of coking coal, and the possibility to substitute the natural gas in the process for green hydrogen.

Once sponge iron in the form of pellets has been produced in the DRI process, this feedstock can be further processed and melted into steel via an electric arc furnace (EAF) which, as the name suggests, is a furnace that can be run entirely off electricity (including renewable).

View the full image here (PDF)

View the full image here (PDF)

Rather than the traditional blast furnace steel-making process, which can accommodate various types of iron ore feedstock, the DRI process requires iron ore pellets that are of low impurity and high iron content. This means that the rise in steel-making via the DRI process also requires an increase in the number of iron ore mines and/or beneficiation capability to meet the relatively narrow specifications for the DRI process. While there are different beneficiation technologies available, the exact solution generally needs to be matched to the particular specifications of the iron ore deposit, creating relatively long engineering and project development timelines for these mineral processing facilities. Accordingly, miners with iron ore suitable for DRI and/or companies with advanced beneficiation capability, are expected to be well placed to supply iron ore to the new generation of DRI projects as they enter production in the coming years.

While a green hydrogen DRI process can remove natural gas from the iron-making process, an element of carbon is still required to produce iron; however, companies are actively exploring natural carbon alternatives, such as specialist charcoals, and how these could be sustainably scaled up in the context of a broader shift to DRI and green steel production.

Industry R&D and start-ups are also focusing on how the DRI process can be adapted to work with a wider spectrum of iron ore feedstock, as well as exploring other reduction processes that could be deployed to convert iron ore to iron.

While DRI has perhaps the greatest potential to produce carbon neutral steel, innovation and R&D has also been focused on lowering the carbon emissions of the traditional blast furnace route, whether by improvements to the energy efficiency of furnaces, or more radical project overhauls looking at implementing fast-evolving carbon capture and storage solutions on blast furnace projects.

Tectonic shifts – evolving geographies of steel production

Even when weaned off natural gas, DRI and EAF plants remain hugely energy-intensive, and for steel to be truly "green" these plants require abundant, low-cost and reliable sources of renewable electricity to create green hydrogen for the DRI plants and electricity for EAFs. Given the relatively nascent green hydrogen market, and the technical challenges of transporting hydrogen, DRI projects generally need to be co-located with hydrogen production facilities. Jurisdictions with low-cost renewable energy are therefore particularly well placed to attract investment in low-carbon steel production. As with previous steel projects, port and/or rail access also remain important factors in deciding where to locate new DRI and EAF plants.

With hydro and solar PV currently being among the lowest-cost sources of renewable energy, we are seeing new low-carbon steel projects cluster in locations where this energy is plentiful and where a stable baseload power supply can also be accessed, particularly Scandinavia in Europe, with its abundant hydro resources and baseload nuclear power, and the GCC states in the Middle East, with their high levels of solar irradiation and growing pipeline of energy storage systems. Locations with high energy costs, like much of the rest of Europe, are challenging for new low-carbon steel projects, as evidenced by the decision of ArcelorMittal earlier this year to cancel decarbonization projects and decline €1.3 billion of related public subsidies to convert its German plants to use hydrogen rather than coal in their steel furnaces.

While iron and steel products are more transportable than hydrogen, countries that are able to offer investors opportunities to vertically integrate more parts of the upstream and downstream steel supply chain in the one location, may also be able to create efficiencies and economies of scale to challenge traditional steel-making jurisdictions. Australia, Brazil and Mauritania, for example, are all established iron ore producing countries that have significant natural advantages that could be used to scale up their solar, wind and/or hydroelectricity capacities to support downstream low-carbon metal sectors.

Regulatory drivers, whether borne out of trade policy, protectionism or sustainability targets, will also continue to influence the location of future low-carbon steel plants. The European Union's Carbon Border Adjustment Mechanism is a leader in this space, and from January 1, 2026, will move from its initial purely reporting transitional phase to an implementation stage, where importers into the EU of carbon-intensive products, including iron and steel, will need to buy CBAM certificates to cover the emissions embedded in their imported products. If importers can prove that a carbon price has already been paid in another jurisdiction during the production of the imported iron or steel, the corresponding amount can be deducted. The CBAM regime is designed to be compliant with WTO rules and to create a level playing field for the low-carbon steel industry in Europe, while ensuring that emissions from the European steel industry are not simply moved overseas to meet the EU's climate objective. By rewarding imported products with low embedded emission levels, CBAM will also support the development of low-carbon iron and steel projects across the globe by essentially providing products from these projects with preferential carbon pricing compared to imports from traditional blast furnace projects. Against a backdrop of an oversupply of steel products in the market globally, this is an opportunity for low-carbon projects to distinguish themselves from their competition and the general downward pressure on steel pricing.

The UK is also scheduled to bring into force its own Carbon Border Adjustment Mechanism on January 1, 2027 which, like the EU mechanism, will apply to iron and steel products, and ensure that carbon-intensive products imported from outside the UK face a comparable carbon price to that which would have been payable had they been produced in the UK. The UK government has also earlier this year committed £2.5 billion via the state-owned National Wealth Fund to finance and fund low-carbon steel projects in the UK, which is in addition to the £500 million grant given to Tata Steel by the UK government in 2024 to support the construction of new electric arc furnaces at Port Talbot in Wales.

In the United States, since 2018 there have been high-profile tariffs on steel aimed at protecting the domestic steel making industry, with the Trump administration in 2025 increasing tariffs on imported steel from 25 percent to 50 percent. While the vast majority of iron production in the US is currently produced using the blast furnace, the country has a head start over most other parts of the global steel sector in terms of deployment of electric arc furnace technology, with more than half of US steel produced using electric mini-mills, which proliferated in the 1960s. Despite the political protection currently provided to the US steel industry, American players continue to make important contributions to the global journey toward a low-carbon steel industry, with Midrex continuing to be headquartered in North Carolina, and Massachusetts-based start-up Boston Metal currently developing its own new molten oxide electrolysis process technology to create low-carbon iron via electrolysis.

Despite the green shoots of a low-carbon steel sector currently being focused in other geographies, China remains the most dominant incumbent player in the steel industry, accounting for more than 53 percent of global crude steel production in 2024, with a tiny estimated 1.2 million tons of China's overall 1,005.1 million tonnes of 2024 crude steel production produced using DRI.1 The significant investments that China has made in recent decades expanding its blast furnace steel production capabilities, as well as China being a net exporter of natural gas, has meant limited DRI or low-carbon steel plants being developed in China to-date, though the China Baowu Group and Baotou are reported to be carrying out feasibility studies and demonstration projects for the use of carbon capture and storage as part of the traditional blast furnace steel-making route.

Top-down government support and bottom-up customer support

By 2030-2035, market demand for green steel is likely to exceed the available supply in some regions, such as Europe.

Source: Deloitte Global

Government support and policy intervention in markets such as the UK is crucial to enable an environment for new low-carbon projects to be developed. The capital costs of building new steel plants are high, and financing options can be limited. Governments can support projects in a variety of ways, including subsidies, guarantees of commercial loans, streamlined permitting processes, equity investments and/or preferential loans from sovereign wealth funds or other state-owned entities. De-industrialization and reducing incomes from other sectors, has meant that governments are looking for new future-facing industries and sectors to support, particularly in geographies that are naturally predisposed to low-carbon steel production. Defense and national security considerations also favor government support for domestic steel production, given the paramountcy of steel to the defense sector.

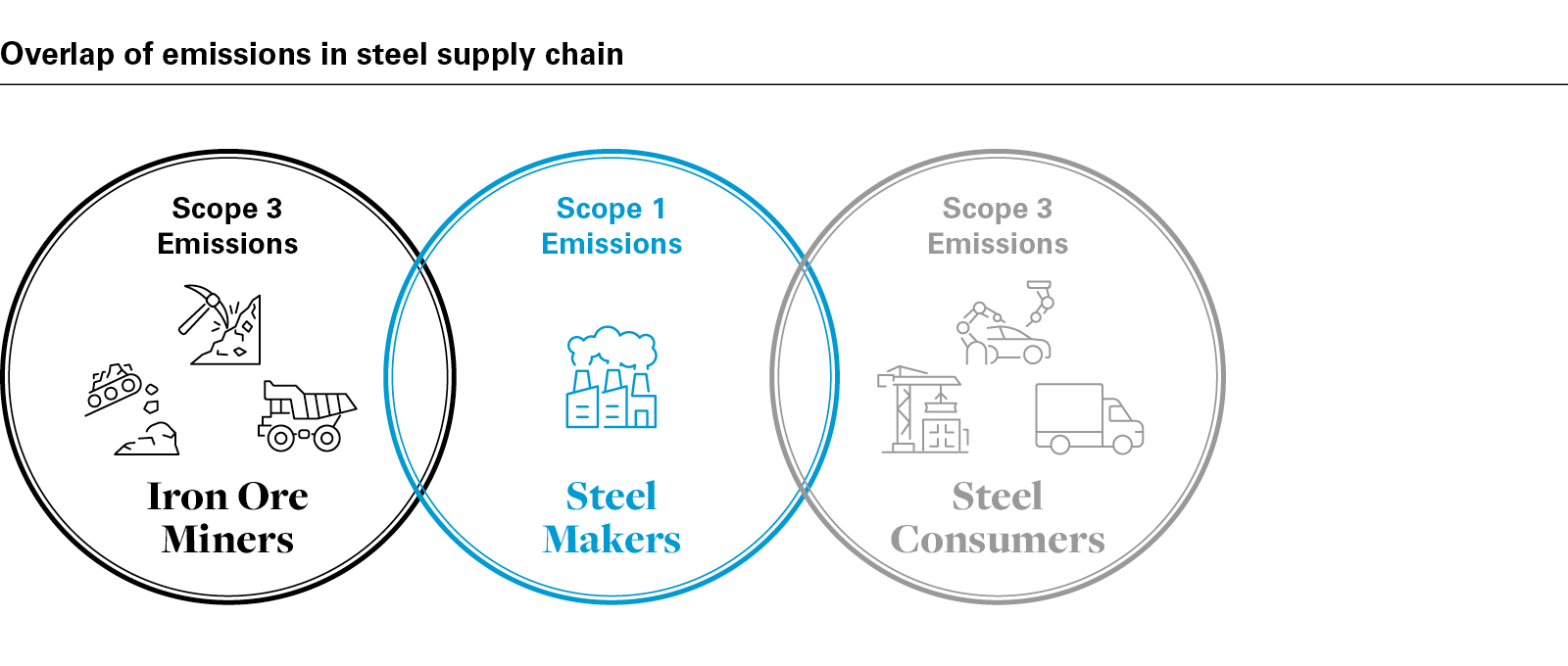

Viability of a low-carbon steel sector will ultimately need to be underpinned by customer demand. A so called "green premium" is already being touted as having been achieved on a number of new green steel projects, such as Stegra's project in Sweden, and industry bodies point to a sustained interest and willingness by consumers to seek out green steel. As carbon markets develop, carbon credits and a price on carbon is also likely to drive interest and investment in low-carbon steel products, particularly given the oversized place that steel production has in terms of global emissions. While the focus is often on the scope 1 emissions of iron and steel producers, these same emissions are a significant part of the scope 3 carbon footprint of iron ore miners and companies with high levels of steel consumption, such as those in the defense, construction and automotive industries.

View the full image here (PDF)

View the full image here (PDF)

British Racing Green – the best shade of green?

Attracting sustained support from governments, customers and other stakeholders is currently impaired by the absence of an industry-wide standard regarding what qualifies as "green" steel, as well as inconsistent methodologies for calculating the embedded carbon in steel products. In the absence of an ISO standard or similar, there is currently no objective or widely accepted certification or qualification that can be given to green steel products. To complicate matters, low-carbon steel products can be "green" to varying degrees.

While there is a natural inclination to insist on the greenest carbon-neutral steel possible, the reality is that the decarbonization of the steel sector will be an evolving process, meaning that projects taking the first steps to carbon neutrality, such as new DRI plants built to operate on natural gas with a medium-term plan to transition to green hydrogen, should not be dismissed out of hand as being "not green." Indeed, new DRI plants initially fired by natural gas are well placed to be foundation customers for new green hydrogen projects, and by serving as a stable hydrogen offtaker, DRI could, in turn, unlock financing options for the construction and development of new green hydrogen facilities.

Collaboration and opportunities across the supply chain

The common goal of low-carbon steel is incentivizing stakeholders across the steel value chain to innovate and collaborate. Companies are investing in their own research and development to create new innovative technologies to abate the industry's emissions and improve the economies of the low-carbon steel sector, as well as in strategic partnerships to gain access to new technology and intellectual property being developed by start-ups and smaller-market participants. These investments in research and development are constantly improving the capabilities and sustainability credentials of green steel projects, whether it be iron ore miners exploring how lower-grade feedstock can be used in the DRI process, original equipment manufacturers optimizing furnaces and key components, or customers researching how more recycled scrap can be used in their specialist steel products that would have traditionally required steel from virgin iron ore.

While collaboration between major industry players can help drive innovation forward, trade policy, tariffs, competition and anti-trust considerations should be carefully analyzed to ensure all applicable regulations are complied with, and the impact of future changes to the policy and regulatory environment are mitigated. Despite these hurdles, spending on research and development in the mining sector is rising, though R&D investments in decarbonization technology remain relatively high-risk due to long lead times for commercial application, and associated uncertainty around returns and commercial viability. Consequently, participants in the mining & metals sector are increasingly forming partnerships and strategic joint ventures to gain access to technology and, crucially, the necessary funding to get projects off the ground. Consolidation in the sector by way of M&A is also a possibility, with tie-ups between start-ups and industry leaders seeming the most likely.

The next chapter

Though iron has been smelted for millennia, the patenting of the Bessemer process in 1856 revolutionized iron and steel-making, enabling mass-produced, low-cost, quality steel at a previously unthinkable scale. In his later years, Sir Henry Bessemer wrote in his autobiography "this is all very simple now that it has been accomplished…but it is, nevertheless, impossible for me to convey any adequate idea of what were my feelings when I saw this incandescent mass rise slowly from the mould: the first large prism of cast malleable iron that the eye of man had ever rested on." Technological, social, geopolitical and regulatory changes are now poised to once again revolutionize the steel industry, and while today the challenges may seem many, the global trajectory is toward a world of low-carbon steel, and industry participants have the opportunity to work together to build that ecosystem and be a part of the next chapter of the steel-making story.

1 World Steel in Figures 2025 | World Steel Association

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP