Discover key findings from the Currents of Capital 2025 Report

The water sector faces unprecedented challenges: escalating water scarcity, deteriorating infrastructure and intensifying climate impacts. These pressures have elevated water from a niche concern to a strategic priority for governments, corporations and institutional investors. Given that funding gaps for global water infrastructure are estimated to be in the trillions of dollars, solutions must be efficient, scalable, collaborative and financeable.

The Currents of Capital 2025 Report provides insights into how investment is flowing into water infrastructure and water-related technology and services worldwide. Our research draws on the perspectives of over 300 senior decision-makers across the global water value chain, including water utilities, multinational corporations, investment funds, engineering firms and technology providers.

Our findings reveal a growing recognition of the fundamental importance of water to economic security and sustainable development. In 2025, 96 percent of respondents plan to maintain or increase their investments in the water sector compared to 2024. This commitment is substantial. Thirty percent of respondents have deployed more than US$500 million in 2024.

However, challenges persist. Regulatory uncertainty can result in delayed investment decisions and project timelines, while the fragmentation of the water markets complicates efforts to scale solutions. The dual nature of water—as both a public good and an economic input—requires specialized investment approaches that differ from traditional infrastructure models.

In the coming years, how water is valued, managed and financed will continue to evolve. Organizations that can navigate the regulatory complexities and uncertainties in the market while harnessing technological innovation will find themselves well positioned to capture value.

More importantly, this rising tide of capital presents a historic opportunity to address global water challenges if investments are channeled toward solutions that balance economic returns with sustainability and equitable access. Our Currents of Capital 2025 Report provides insights for stakeholders seeking to navigate these currents of capital toward a sustainable water future that benefits communities, ecosystems and investors.

Methodology

Our Currents of Capital 2025 Report draws on insights from an experienced respondent base that represents the full spectrum of water sector stakeholders. Our survey captured perspectives from more than 300 respondents—spanning water utilities, multinational corporations, investment funds, engineering, procurement and construction (EPC) firms and technology providers—creating a unique cross-sectional view of decision-making across the entire water value chain. The respondents have substantial financial influence, with 29 percent representing organizations managing assets or generating turnover exceeding US$10 billion, 37 percent falling within the US$1-9.9 billion range and 33 percent generating between US$500 million and US$999 million. This financial diversity ensures perspectives from both industry giants and nimble mid-market players are included.

The geographic breakdown highlights a dominance of Western markets (45 percent Western Europe and 34 percent North America) while still incorporating significant representation from East Asia (8 percent), Oceania (5 percent) and emerging regions, including the Middle East (3 percent), Southeast Asia (2 percent), Africa (2 percent) and Latin America (1 percent). Most critically, these respondents have genuine decision-making authority within their organizations—81 percent of the respondents indicated they have a strong influence over water investments or priorities within their organization, while 19 percent have the ultimate decision-making authority in these areas. This combination of financial scale, geographic diversity and decision-making seniority creates a comprehensive view into the actual capital flows and strategic priorities shaping the global water sector in 2025.

Contacts

Partner|Sydney

Partner|New York

Partner|Abu Dhabi

Partner|London

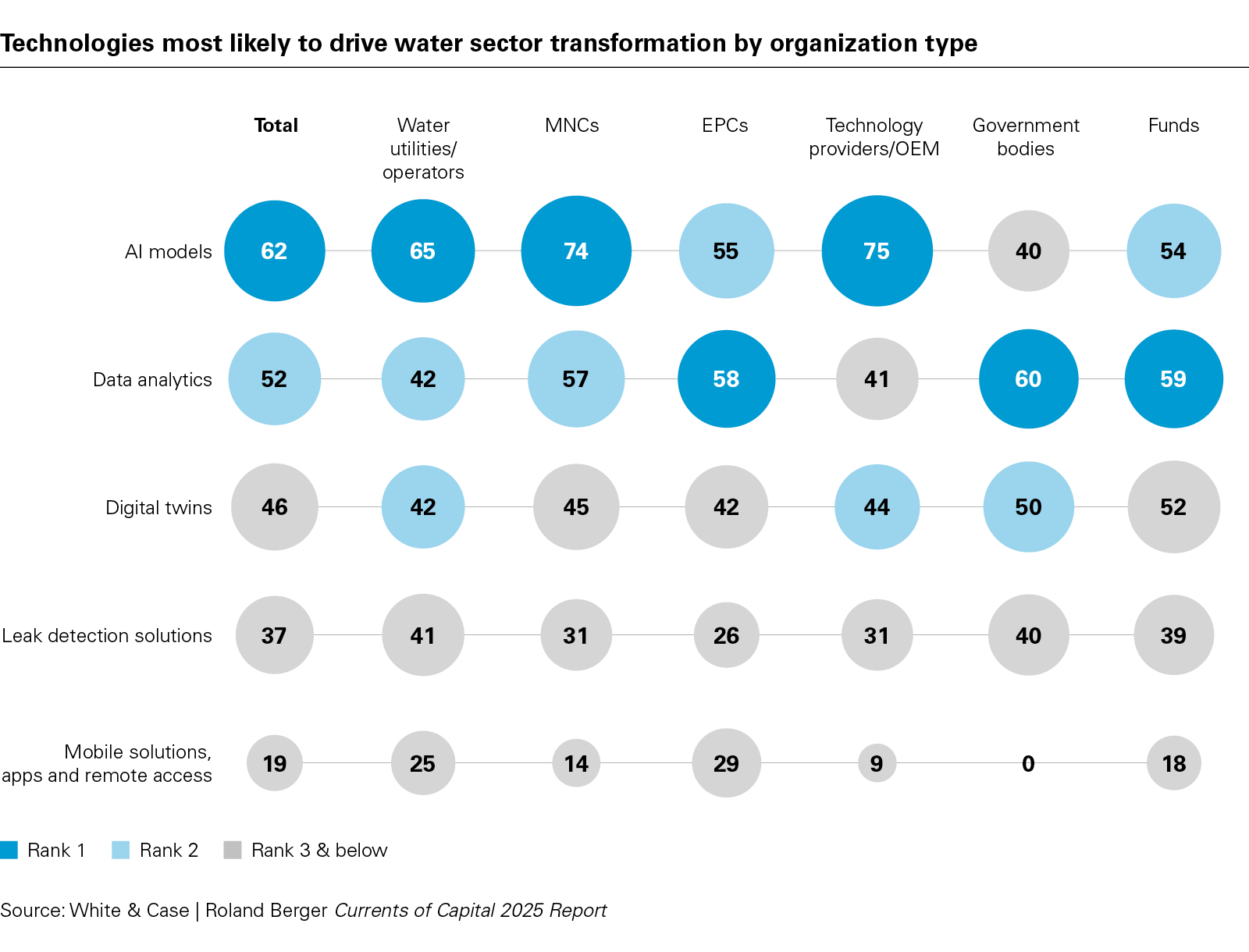

View full image: Technologies most likely to drive water sector transformation by organization type (PDF)

View full image: Technologies most likely to drive water sector transformation by organization type (PDF)

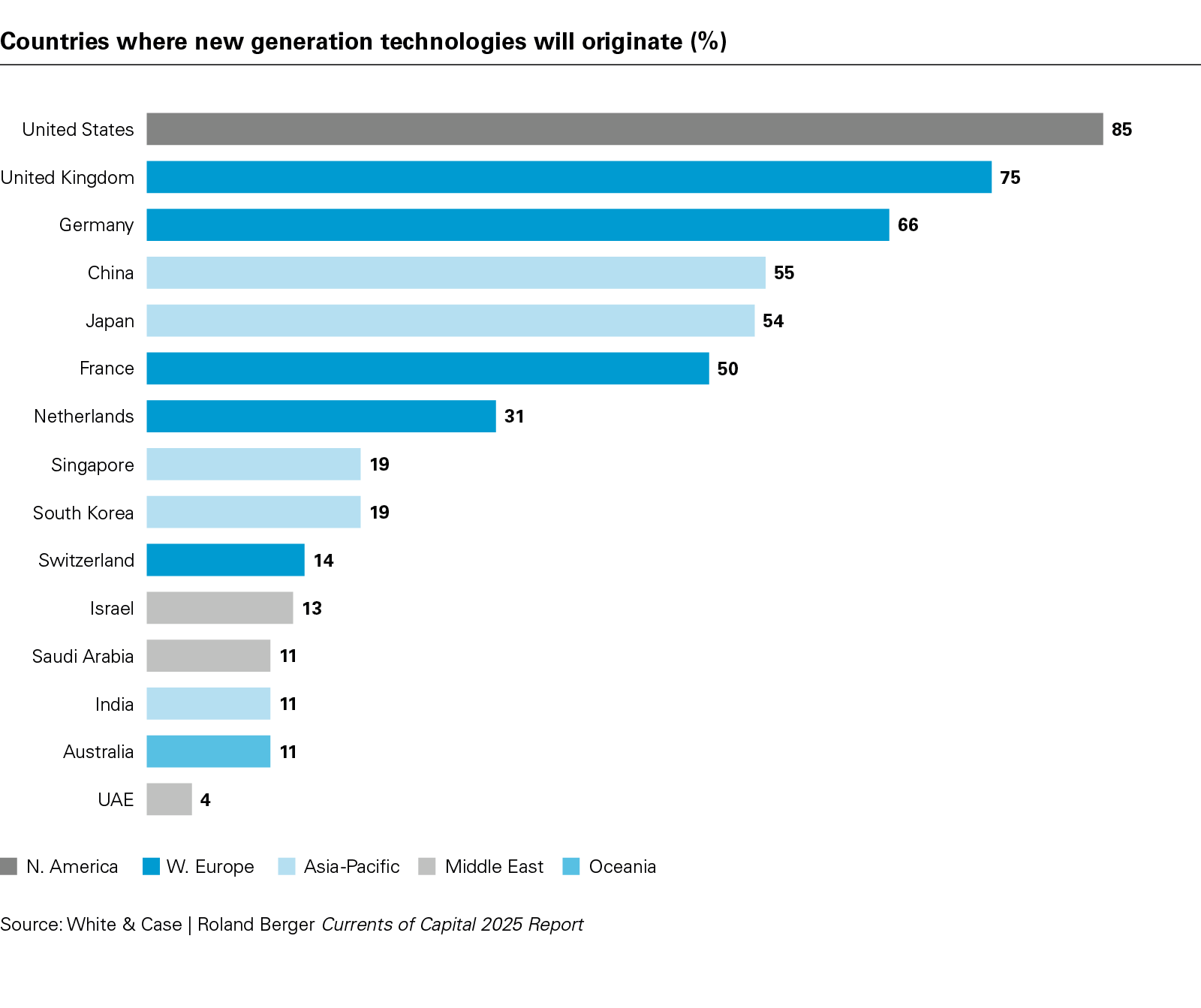

View full image: Countries where new generation technologies will originate (%) (PDF)

View full image: Countries where new generation technologies will originate (%) (PDF)