European leveraged finance: Choosing the right path

European leveraged finance: Choosing the right path

European leveraged finance markets paused for breath in 2022, due to rising interest rates, volatile geopolitics and a tightening of financial markets across the board—but what can we expect in 2023?

Foreword

Heading into 2023, European leveraged finance markets continue to deal with fierce headwinds, following 12 months of economic and geopolitical volatility that has prompted a general slowdown in issuance. What does this mean for the months ahead?

After the record-setting leveraged finance activity seen in 2021—as companies scrambled to refinance, M&A activity spiked and private equity (PE) went on a shopping spree—it was clear that pace was not likely to continue.

But in 2022, as the tail end of the pandemic worked its way through markets, companies were suddenly faced with a new reality. Conflict erupted in Ukraine, oil prices climbed and supply chains were disrupted. A decade of low inflation and interest rates came to an end across Europe. Financing began to tighten as debt became increasingly expensive.

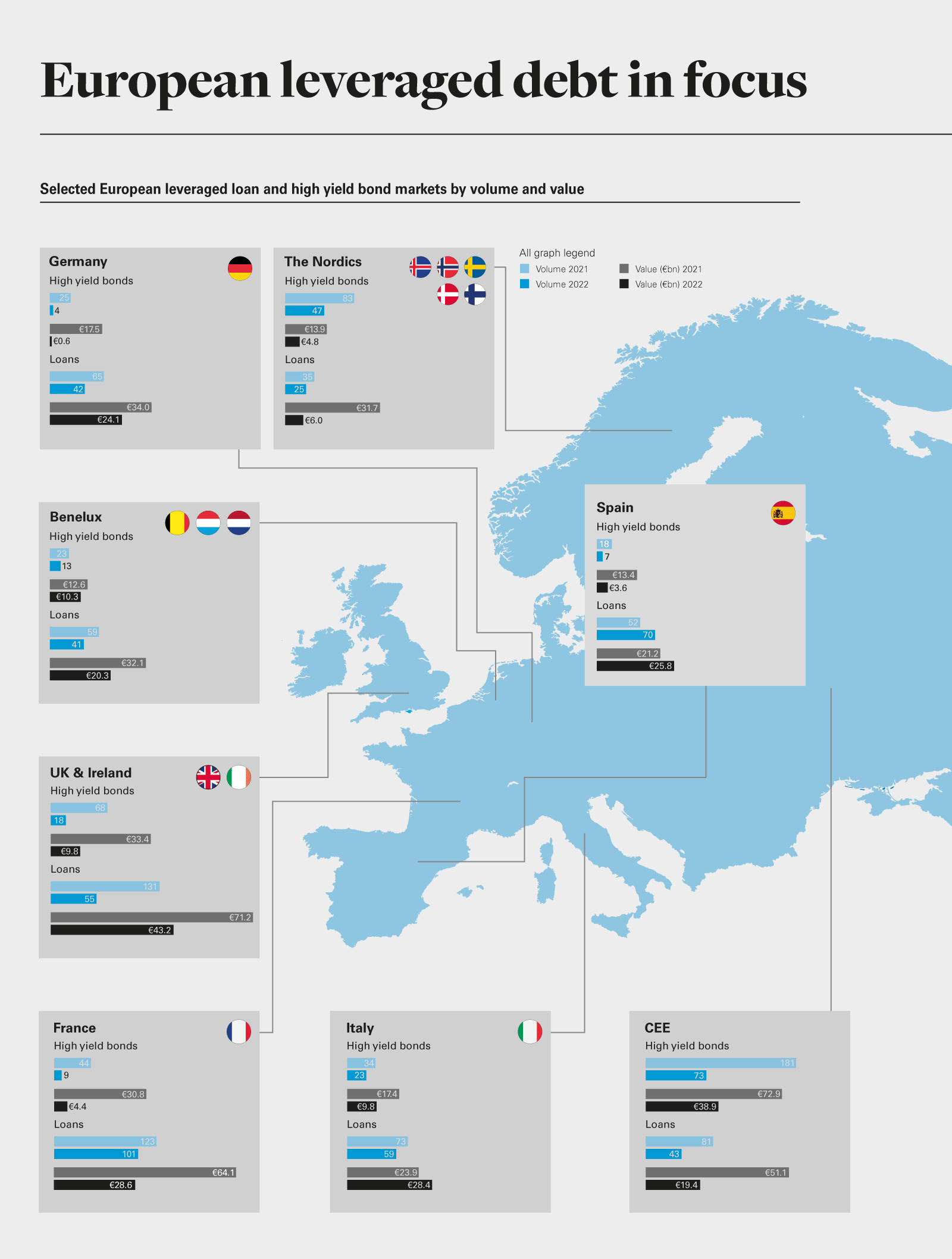

By the end of 2022, while European leveraged loan and high yield bond markets began to see activity, it was well below normal levels and followed a prolonged period of lower issuances. Leveraged loan issuance in Western and Southern Europe was down 37 per cent year-on-year, while high yield bonds fell by 66 per cent during the same period. The third quarter of the year was one of the lowest quarterly totals for leveraged finance issuance in the region on Debtwire Par record.

In both cases, higher pricing was a major factor as it continued to climb throughout the year. On leveraged loans, almost 40 per cent of all deals saw original issue discounts (OIDs) of two or more points from par—by Q4, it was not unheard of for there to be OIDs in the low 90s on term loan B facilities. On the bond side, pricing seemed to finally peak by the end of the year, but only after six quarters of consistent rises.

Eye on the prize

At the same time, there were a few bright spots for leveraged finance markets throughout the year.

First and foremost, buyout activity remained active in the first half of 2022 before dropping off in the second half. Notable deals include KKR’s €3.4 billion-equivalent acquisition of independent beverage bottler Refresco and Bain’s purchase of human resource consultants House of HR, backed by a €1.145 billion term loan and a €415 million note.

Second, new money financing represented a significant proportion of total issuance early in the year, as issuers raised term loan facilities to partially refinance drawn revolvers and fund new acquisitions. As with everything else, however, headwinds meant that most of the new money facilities issued towards the end of the year were smaller add-ons.

Third, CLOs continued to perform consistently (though they were not immune to the general slowdown in the market). Overall, there was €26.1 billion in issuance in 2022—down 32 per cent year-on-year but, in November alone, there was almost €3 billion in new CLO issuance, well above historical monthly averages, according to Debtwire Par.

The path ahead

While there are still shadows on the horizon, the cyclical nature of leveraged finance means that there are always new opportunities. The key is to be prepared.

For example, inflation is starting to plateau in many jurisdictions, but interest rate rises may continue—in the UK, for example, in December, the Bank of England raised the benchmark to 3.5 per cent, up from 3 per cent. This was the ninth consecutive hike since December 2021, placing the rate at its highest level for 14 years. Companies will need to consider their options carefully to get their costs under control.

For those looking to pro-actively manage their debt, amend-and-extend facilities may be the best place to start. Small add-ons and maturity extensions will help many find their way through the forest until macro-economic conditions improve.

Those with the highest-quality credits will reap the benefits of the liquidity available in the market by upsizing as well as via likely tighter pricing during syndication (when compared to balance sheet lending). For example, Debtwire Par reports that French telephony firm Iliad and automotive supplier Valeo entered the market with €500 million notes, and both were upsized during syndication to €750 million.

While this points to a potentially bifurcated European market in the months ahead, where solid credits remain healthy and those already struggling may face an uphill battle, liquidity on the equity and debt ledgers remains strong, and leveraged finance activity is likely to pick up further to address their respective needs.

Hitting the brakes: European leveraged finance battens down the hatches

Leveraged loan issuance in Western and Southern Europe reached €183.4 billion in 2022, down by 37 per cent year-on-year

High yield bond activity was down 66 per cent during the same period, at €50 billion

Loan margins were up by 0.64 per cent by the end of the year, while average yields to maturity for high yield bonds climbed by nearly 3 per cent

UK leveraged finance markets have come through a challenging period in 2022, with issuance across leveraged loan and high yield markets declining as rising interest rates, inflation and the conflict in Ukraine hit activity.

UK leveraged finance issuance in 2022 fell by just over 50 per cent year-on-year, tracking the drop off in issuance observed across the wider European market. Private debt lending has proven more resilient but has also felt the impact of rate hikes and geopolitical uncertainty, with fundraising markets and deal flow from M&A targets tightening through the course of the year.

The UK market faced a unique set of challenges. As a result, the Bank of England (BOE) hiked interest rates nine times through the course of 2022 to 3.5, the highest level observed since the 2008 financial crisis. The European Central Bank (ECB), meanwhile, upped rates four times in 2022, with its benchmark rate now sitting at 2.5 per cent to 1 per cent below the BOE level.

UK lenders and borrowers were already contending with political volatility, in the form of successive changes of prime minister and a catastrophic "mini-budget" in late September 2022. This catalysed a slew of collateral calls and forced sales of UK government bonds, requiring the BOE to step in and backstop bond markets to prevent the dislocation from spreading into other parts of the economy. Financing conditions are expected to remain calm in 2023 in the UK, with limited impetus to kickstart markets back into life.

But there are some early signs of green shoots. For example, after raising rates in December 2022, the BOE argued that inflation may have peaked, slowing from the four-decade highs recorded earlier in the year. Assuming inflation has topped out as predicted, there will be more scope for the UK central bank to halt or slow any further interest rate rises.

A change in the direction of travel on rates will provide issuers and investors with more certainty, help debt prices in secondary markets to recover and encourage primary issuers to come forward and test market appetite for new debt issuance.

The drop in corporate valuations and the weaker price of sterling relative to the US dollar and euro, meanwhile, could drive significant interest from overseas buyers on UK take-private deals in 2023.

Appetite for UK take-private deals has remained strong in 2022, despite macro-economic headwinds. According to Dealogic, UK companies valued at more than £40 billion were already taken off UK public markets in the first nine months of 2022. Public-to-private transactions are expected to continue providing a pipeline of M&A deals and financing opportunities in 2023.

Conclusion

Stalled issuance, growing concerns around rising costs, supply chain bottlenecks and the conflict in Ukraine—it's been a whirlwind of a year, with many remaining challenges for the year ahead

Direct lenders were able to take on large-cap financings in 2022 as loan and bond markets pulled back

Nimble managers are taking out hung bridges and buying up debt in non-conventional syndication processes

Direct lending moves into 2023 in good shape, but pressures on portfolios and tighter fundraising markets could slow deployment

Inertia across European leveraged loan and high yield bond markets in 2022 opened a window of opportunity for direct lenders to fund larger credits and strengthen their core mid-market franchises.

Despite the challenges posed by rising inflation and interest rates, as well as supply chain bottlenecks and the fallout from the Ukraine conflict, direct lending activity sustained high levels of deal flow.

According to Debtwire Par, European direct lending issuance came in at €51.6 billion in the first nine months of 2022, well ahead of the €38.8 billion posted in 2021. Deal count of 705 transactions for the period, while down from the 899 deals in 2021, also held up well ahead of pre-pandemic levels.

These levels of direct lending activity—particularly in the first half of the year—stood in contrast to the double-digit declines observed in syndicated loan and high yield bond markets, where issuance has slumped in the face of macro-economic headwinds and investors have preferred buying up discounted credits in the secondary market to new deals.

Filling the gap

Despite the challenges posed by rising inflation and interest rates, as well as supply chain bottlenecks and the fallout from the Ukraine conflict, direct lending activity sustained high levels of deal flow

The slowdown across capital markets has given direct lenders an opportunity to fund larger credits that would normally have been funded with loans and bonds.

Replete with dry powder following a strong run of fundraising in the past 24 months, direct lenders have routinely stepped in to take on credits that shelved or shunned public bond and leverage loan plans and opted for private debt solutions instead.

Advent International, for example, initially lined up a €430 million floating rate note to partially finance its acquisition of Italian ingredients manufacturer IRCA, but switched to a senior acquisition finance package provided by CVC Credit Partners as public credit markets turned.

Other examples of deals switching to direct lenders include France-based buyout firm Astorg's acquisition of drug development company CordenPharma, where banks were initially expected to provide financing. Instead, Astorg went with a €1.5 billion financing from a club of four private debt providers.

Direct lending clubs, like the one that funded the CordenPharma, have become increasingly common, as direct lenders band together to diversify risk and combine their financial firepower to take down jumbo credits. The £3 billion refinancing of software company Access and the debt provided for Clayton, Dubilier & Rice’s acquisition of the UK, Ireland and Asia operations of French services business Atalian have both been financed by clubs of direct lenders.

Direct lenders have also taken advantage of the flexibility and nimbleness of the private debt model to provide banks and borrowers with variations on classic syndicated deals.

In the acquisition of Danish pharmaceutical company Norgine, by the private equity arm of Goldman Sachs, for example, the financing was underwritten by Jefferies, KKR Capital Markets and Goldman Sachs with a plan to syndicate directly to private credit firms rather than institutional investors, according to Bloomberg.

Private debt funds have also stepped in to provide liquidity for underwriting banks stuck with debt that they have not been able to syndicate. At the end of 2022, US and European banks were sitting on approximately US$42 billion of buyout debt stuck in syndication because of the more risk-averse market, according to Bloomberg.

Direct lenders have seen an opportunity to buy up this paper and help banks clear their books. Specialist debt fund manager Pimco, for example, bought more than €1 billion of loans from banks that underwrote the buyout of French payments business Worldline as well as €500 million of debt used to back the buyout of UK supermarket chain Morrisons.

In addition to the opportunities presented at the large-cap end, the mid-market—a core market for direct lenders—has continued to tick over. Mid-market M&A involving companies valued at less than €1 billion has proven more resilient to the deteriorating economic backdrop than mega-deal activity, ensuring a steady flow of transactions to finance for direct lenders.

Maintaining momentum

With syndicated loan and high yield bond markets expected to remain relatively moribund into 2023, direct lenders are well positioned to continue winning market share in the large-cap market, strengthening their position as the go-to option for mid-market deals.

The next 12 months, however, will not be without their challenges.

There are signs that direct lender bandwidth will be shifted from new deals to portfolio management. According to Debtwire Par, there are hints that borrowers across European direct lending portfolios are already bracing for squeezes on profitability that could see credits push up against covenants.

Amend-and-extend and refinancing deals may stave off some covenant breaches, and direct lender credits are also parsing through their accounts to identify EBITDA add-backs and so-called "exceptional items" that could help them squeeze through covenant tests.

Nevertheless, in a mid-market lender survey conducted by Debtwire Par, 15 per cent of respondents say they expect between a fifth and half of their portfolios to be vulnerable. More than 40 per cent expect covenant waivers to be the main restructuring mitigation strategy in the next three to six months.

Anecdotal reports are also emerging that direct lenders are starting to tap the brake on the pace of deployment more generally after a frenetic period of activity through both 2022 and 2021.

Fundraising across all private markets has slowed in 2022, with increasingly risk-averse investors scaling back their exposure to alternative assets. As most direct lenders are well ahead of deployment schedules, there is no rush to fully deploy existing vehicles and face a choppier fundraising market earlier than necessary, according to Deloitte.

Direct lenders are still open for business but can afford to be choosier about the credits they back.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European leveraged debt in focus (PDF)

View full image: European leveraged debt in focus (PDF)