European leveraged finance: Choosing the right path

European leveraged finance: Choosing the right path

European leveraged finance markets paused for breath in 2022, due to rising interest rates, volatile geopolitics and a tightening of financial markets across the board—but what can we expect in 2023?

Foreword

Heading into 2023, European leveraged finance markets continue to deal with fierce headwinds, following 12 months of economic and geopolitical volatility that has prompted a general slowdown in issuance. What does this mean for the months ahead?

After the record-setting leveraged finance activity seen in 2021—as companies scrambled to refinance, M&A activity spiked and private equity (PE) went on a shopping spree—it was clear that pace was not likely to continue.

But in 2022, as the tail end of the pandemic worked its way through markets, companies were suddenly faced with a new reality. Conflict erupted in Ukraine, oil prices climbed and supply chains were disrupted. A decade of low inflation and interest rates came to an end across Europe. Financing began to tighten as debt became increasingly expensive.

By the end of 2022, while European leveraged loan and high yield bond markets began to see activity, it was well below normal levels and followed a prolonged period of lower issuances. Leveraged loan issuance in Western and Southern Europe was down 37 per cent year-on-year, while high yield bonds fell by 66 per cent during the same period. The third quarter of the year was one of the lowest quarterly totals for leveraged finance issuance in the region on Debtwire Par record.

In both cases, higher pricing was a major factor as it continued to climb throughout the year. On leveraged loans, almost 40 per cent of all deals saw original issue discounts (OIDs) of two or more points from par—by Q4, it was not unheard of for there to be OIDs in the low 90s on term loan B facilities. On the bond side, pricing seemed to finally peak by the end of the year, but only after six quarters of consistent rises.

Eye on the prize

At the same time, there were a few bright spots for leveraged finance markets throughout the year.

First and foremost, buyout activity remained active in the first half of 2022 before dropping off in the second half. Notable deals include KKR’s €3.4 billion-equivalent acquisition of independent beverage bottler Refresco and Bain’s purchase of human resource consultants House of HR, backed by a €1.145 billion term loan and a €415 million note.

Second, new money financing represented a significant proportion of total issuance early in the year, as issuers raised term loan facilities to partially refinance drawn revolvers and fund new acquisitions. As with everything else, however, headwinds meant that most of the new money facilities issued towards the end of the year were smaller add-ons.

Third, CLOs continued to perform consistently (though they were not immune to the general slowdown in the market). Overall, there was €26.1 billion in issuance in 2022—down 32 per cent year-on-year but, in November alone, there was almost €3 billion in new CLO issuance, well above historical monthly averages, according to Debtwire Par.

The path ahead

While there are still shadows on the horizon, the cyclical nature of leveraged finance means that there are always new opportunities. The key is to be prepared.

For example, inflation is starting to plateau in many jurisdictions, but interest rate rises may continue—in the UK, for example, in December, the Bank of England raised the benchmark to 3.5 per cent, up from 3 per cent. This was the ninth consecutive hike since December 2021, placing the rate at its highest level for 14 years. Companies will need to consider their options carefully to get their costs under control.

For those looking to pro-actively manage their debt, amend-and-extend facilities may be the best place to start. Small add-ons and maturity extensions will help many find their way through the forest until macro-economic conditions improve.

Those with the highest-quality credits will reap the benefits of the liquidity available in the market by upsizing as well as via likely tighter pricing during syndication (when compared to balance sheet lending). For example, Debtwire Par reports that French telephony firm Iliad and automotive supplier Valeo entered the market with €500 million notes, and both were upsized during syndication to €750 million.

While this points to a potentially bifurcated European market in the months ahead, where solid credits remain healthy and those already struggling may face an uphill battle, liquidity on the equity and debt ledgers remains strong, and leveraged finance activity is likely to pick up further to address their respective needs.

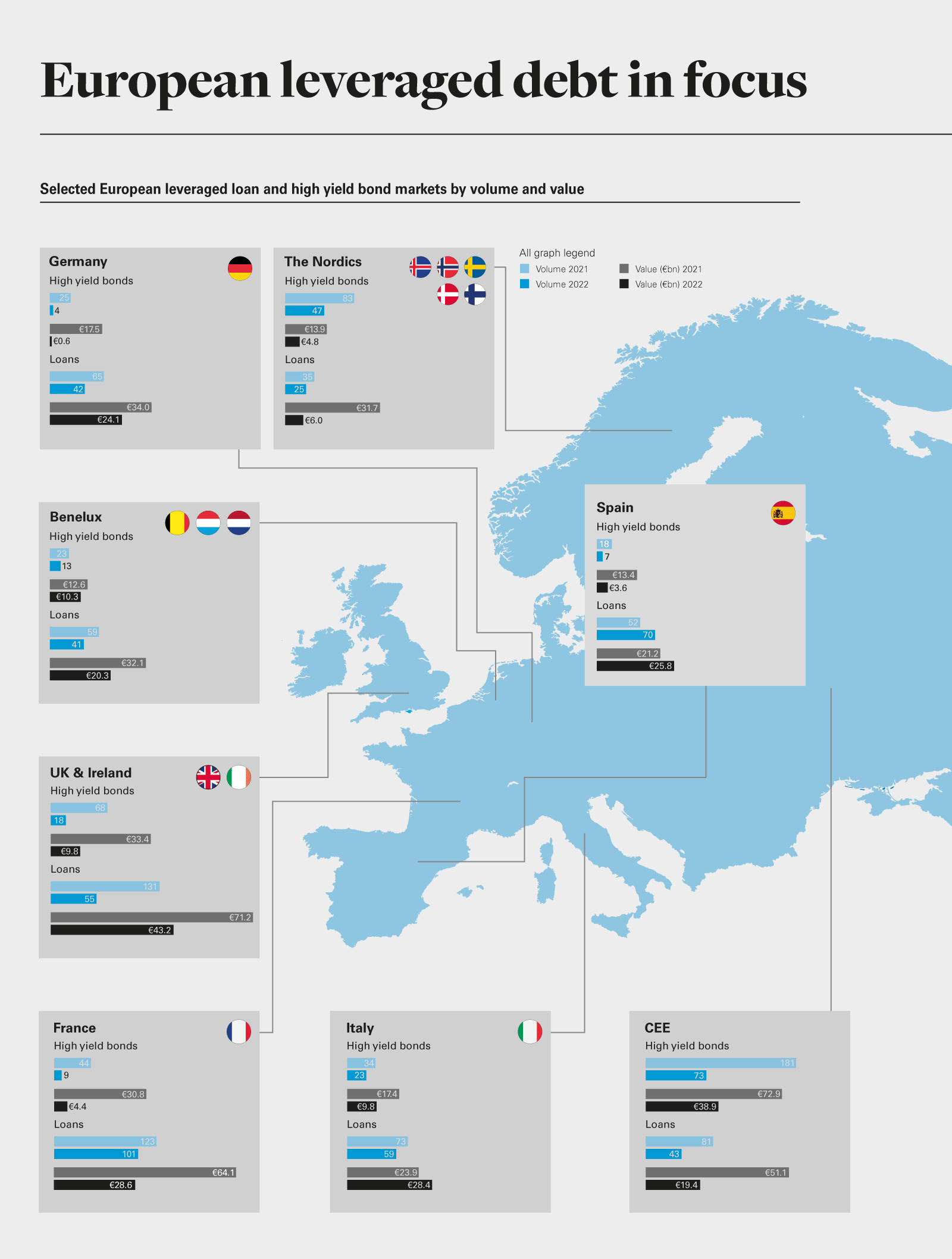

Hitting the brakes: European leveraged finance battens down the hatches

Leveraged loan issuance in Western and Southern Europe reached €183.4 billion in 2022, down by 37 per cent year-on-year

High yield bond activity was down 66 per cent during the same period, at €50 billion

Loan margins were up by 0.64 per cent by the end of the year, while average yields to maturity for high yield bonds climbed by nearly 3 per cent

UK leveraged finance markets have come through a challenging period in 2022, with issuance across leveraged loan and high yield markets declining as rising interest rates, inflation and the conflict in Ukraine hit activity.

UK leveraged finance issuance in 2022 fell by just over 50 per cent year-on-year, tracking the drop off in issuance observed across the wider European market. Private debt lending has proven more resilient but has also felt the impact of rate hikes and geopolitical uncertainty, with fundraising markets and deal flow from M&A targets tightening through the course of the year.

The UK market faced a unique set of challenges. As a result, the Bank of England (BOE) hiked interest rates nine times through the course of 2022 to 3.5, the highest level observed since the 2008 financial crisis. The European Central Bank (ECB), meanwhile, upped rates four times in 2022, with its benchmark rate now sitting at 2.5 per cent to 1 per cent below the BOE level.

UK lenders and borrowers were already contending with political volatility, in the form of successive changes of prime minister and a catastrophic "mini-budget" in late September 2022. This catalysed a slew of collateral calls and forced sales of UK government bonds, requiring the BOE to step in and backstop bond markets to prevent the dislocation from spreading into other parts of the economy. Financing conditions are expected to remain calm in 2023 in the UK, with limited impetus to kickstart markets back into life.

But there are some early signs of green shoots. For example, after raising rates in December 2022, the BOE argued that inflation may have peaked, slowing from the four-decade highs recorded earlier in the year. Assuming inflation has topped out as predicted, there will be more scope for the UK central bank to halt or slow any further interest rate rises.

A change in the direction of travel on rates will provide issuers and investors with more certainty, help debt prices in secondary markets to recover and encourage primary issuers to come forward and test market appetite for new debt issuance.

The drop in corporate valuations and the weaker price of sterling relative to the US dollar and euro, meanwhile, could drive significant interest from overseas buyers on UK take-private deals in 2023.

Appetite for UK take-private deals has remained strong in 2022, despite macro-economic headwinds. According to Dealogic, UK companies valued at more than £40 billion were already taken off UK public markets in the first nine months of 2022. Public-to-private transactions are expected to continue providing a pipeline of M&A deals and financing opportunities in 2023.

Conclusion

Stalled issuance, growing concerns around rising costs, supply chain bottlenecks and the conflict in Ukraine—it's been a whirlwind of a year, with many remaining challenges for the year ahead

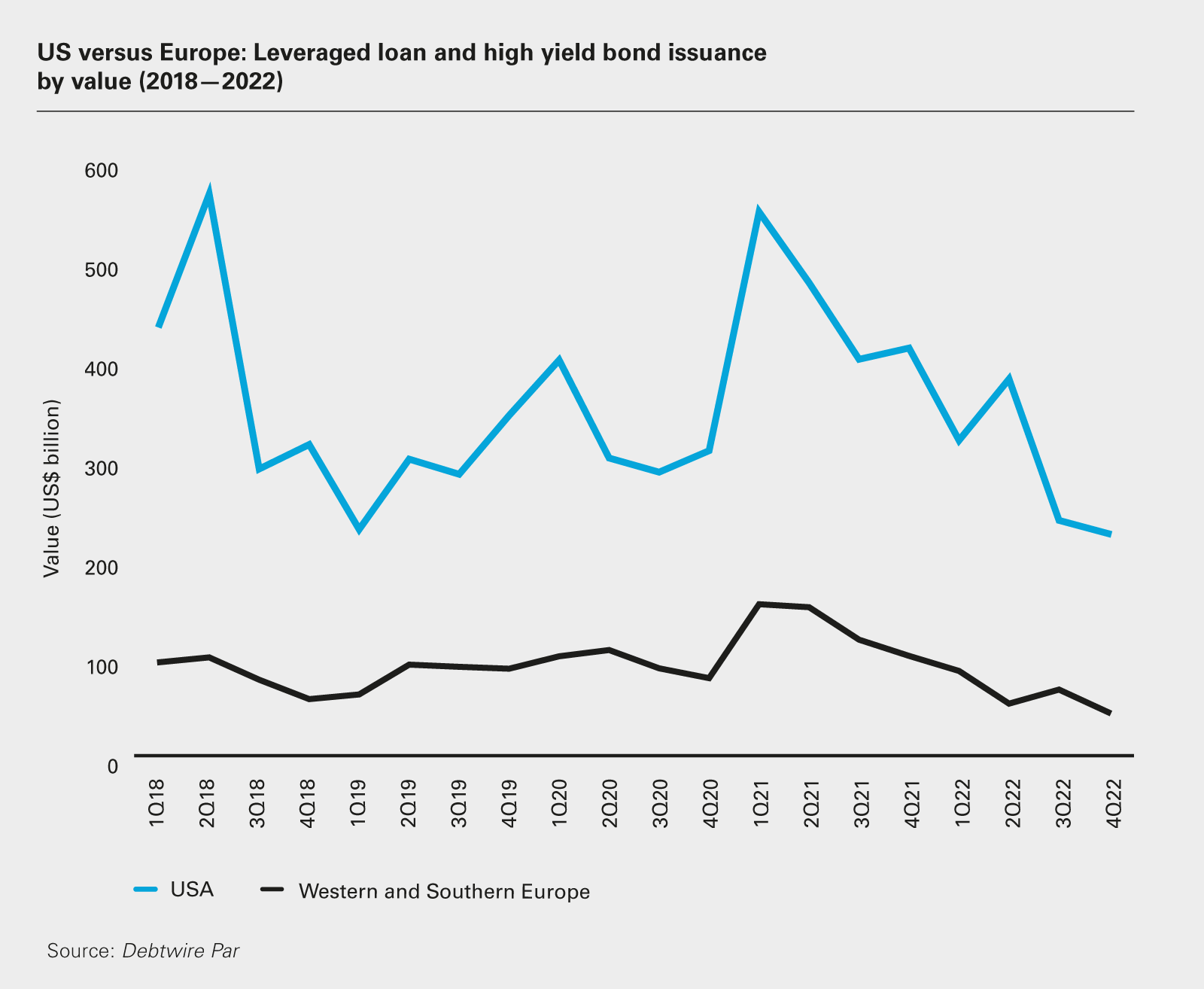

US leverage loan issuance for 2022 fell 24 per cent, year-on-year, reaching US$1.1 trillion

High yield bonds in the US were hit particularly hard, dropping 78 per cent during the same period to US$96.5 billion

Leveraged loan issuance in Western and Southern Europe by comparison was down 37 per cent year-on-year for 2022, at €183.4 billion in 2022

High yield bond activity in Western and Southern Europe dropped 66 per cent during the same period, to €50 billion

Leveraged finance markets in the US and Europe faced similar challenges over the past year, with climbing inflation, rising interest rates and deep discounts in secondary markets putting the brakes on issuance.

Deeper, more-liquid US markets weathered these headwinds better, although activity remains subdued. US leveraged loan issuance dropped 24 per cent year-on-year to US$1.1 trillion, with high yield issuance off 78 per cent over the same period. In Western and Southern Europe, by comparison, leveraged loan and high yield bond issuance fell by 37 per cent and 66 per cent, respectively.

Central banks in the US, UK and EU all lifted interest rates in 2022 to the highest levels observed since the global financial crisis, in a collective effort to curb surging inflation. The pace and scale of rate rises may diverge slightly in 2023, but central bankers in each jurisdiction have signalled that more rate rises are on the horizon, suggesting that high interest rates will continue to shape leveraged finance activity on both sides of the Atlantic for the immediate future.

Rising borrowing costs chill issuance

24%

The decline in leveraged loan issuance in the US in 2022 year-on-year—in Western and Southern Europe, it fell by 37 per cent during the same period

Higher base rates have pushed up borrowing costs across the board. In Europe, the average margins on first-lien institutional loans climbed by almost 1.5 per cent in the first nine months of 2022, reaching 4.73 per cent by year end, according to Debtwire Par. Weighted average yield to maturity for fixed rate bonds was up from 4.73 per cent at the end of 2021 to 8.23 per cent in Q4 2022.

US loan margins escalated at a similar clip, with average margins on first-lien institutional loans climbing from 3.73 per cent in the final quarter of 2021 to 4.24 per cent by the end of 2022, while the weighted average yield to maturity for US senior secured high yield bonds was up to 10.38 per cent at the end of Q4 2022, from 6.71 per cent over the first quarter.

Rising borrowing costs have chilled issuance, which has also been hampered by widening discounts in secondary markets, with investors preferring to buy up existing credits at discounts to par rather than putting money to work via new issuance. In the US, loans in the secondary market changed hands at an average of 91.49 per cent to par in December 2022, with European paper trading at 90.6 per cent in the same month.

US TLA and ABL markets soften the landing

In addition to benefitting from a larger fixed-income investor base, US borrowers have also been helped by the country's more established and sophisticated term loan A (TLA) and asset-based lending (ABL) markets.

According to Debtwire Par, TLA issuance in the US, also known as pro rata debt, was up 55 per cent year-on-year at US$765.7 billion. Unlike term loan B (TLB) debt—which underwriting banks will parcel and sell down to institutional investors, including mutual funds, insurers and CLOs—commercial banks typically fund TLAs and hold them on their balance sheet. These amortise materially over the life of the loan, unlike TLB packages, where loans are subject to only de minimus amortisation prior to maturity, and come with financial covenant protection.

These more lender-friendly characteristics give banks greater protection by providing for potential earlier warning triggers given the additional payment requirements and a financial covenant. In the red-hot debt markets of 2021, borrowers favoured the loose terms available in the TLB space but, as the institutional market has jammed up and syndication risk has intensified, borrowers have pivoted to the more predictable TLA space.

Notable deals in this space in 2022 include debt financing that combines TLA, TLB and high yield facilities for Univision Communications, a Spanish-language content and media company. The financing includes a five-year, US$500 million senior secured TLA facility and a US$500 million TLB, alongside a US$500 million senior secured high yield bond.

ABL activity has also climbed, rising 42 per cent year-on-year to US$111.8 billion. ABL debt is also provided by banks and is secured by more liquid assets (e.g., receivables and inventory), offering a better shield against swings in the credit cycle than cash flow lending, which is driven by interest rates and forecasts for borrower earnings.

While neither TLA or ABL activity contributed to overall lending in Europe in a meaningful way, one area where it mirrored the US is in the private debt space.

In the US and Europe, direct lenders have stepped up to fund credits that would normally have gone down the syndicated loan or high yield bond route. As take-and-hold lenders, private debt funds have provided greater certainty of execution for borrowers in volatile credit markets.

In the US, direct lenders have taken on some jumbo credits, including approximately US$5 billion in financing provided by a Blackstone-led group to fund Hellman & Friedman and Permira's leveraged buyout of software company Zendesk and Ares' and Blackstone's participation in a US$4.5 billion loan to fund an investment in Information Resources. Deals in the €1 billion-plus range in Europe have also found direct lenders open for business, including Astorg's acquisition of drug development company CordenPharma.

Individual direct lenders tapped the brakes somewhat as 2022 progressed, gradually reducing cheque sizes, but private debt players have proven adept at clubbing together to spread the risk while continuing to provide financing for transactions of scale.

In the US and Europe, direct lenders have also moved to buy un-syndicated debt from banks, often at discounts. At the end of 2022, US and European banks were sitting on more than US$40 billion in buyout debt stuck in syndication because of a more risk-averse market, according to Bloomberg. In certain of these situations, some private credit funds came in aggressively as buyers of these loans and bonds, often either taking on the entire tranche at a discount or purchasing large tickets.

For example, in Q3 2022, Los Angeles-based stressed and distressed debt investor Oaktree noted that banks were disposing of hung debt at attractive prices. New York-based private markets manager Apollo raised more than US$2 billion to buy up hung debt paper. In Europe, the direct lending arm of Pimco bought up loans used to fund the buyouts of supermarket Morrisons and payment group Worldline.

It remains to be seen whether direct lenders can defend these gains in market share when syndicated loan and high yield bond markets eventually do revive but, in the US, underwriting banks are anticipating that competition from direct lenders will become a feature of the market in the long term.

In response to the competition for financing deals from private debt, for example, J.P. Morgan has set up a division that, like direct lenders, will hold debt on its own balance sheet to maturity rather than syndicate.

In Europe, meanwhile, the direct lender will sometimes come in as an anchor investor and the remaining debt will then be sold down to more traditional participants. Some underwriting banks, however, are looking to capitalise on momentum in the direct lending space by placing debt with direct lenders rather than going down traditional institutional channels.

Hoping for green shoots… but challenges remain

Moving into 2023, lenders and borrowers in both markets will be hoping that interest rates and inflation peak by the middle of the year, bringing stability to debt prices in secondary markets and encouraging primary markets to reopen.

There are some suggestions that inflation may be peaking in the US and the UK, which will ease the pressure on central banks to up interest rates. In Europe, however, where monetary policy tightened later, it may take longer for inflation and rates to flatten out and for debt markets to spark back to life. And even if the pace of rate rises cools, restructurings and defaults are on the horizon in both jurisdictions as the rate hikes of the past 12 months start to feed through.

Hopes may be rising that conditions for new debt issuance will improve in 2023, but the next 12 months will continue to be challenging for US and European debt markets nonetheless.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European leveraged debt in focus (PDF)

View full image: European leveraged debt in focus (PDF)

View full image: US versus Europe: Leveraged loan and high yield bond issuance by value (2018—2022)

View full image: US versus Europe: Leveraged loan and high yield bond issuance by value (2018—2022)