European leveraged finance: Choosing the right path

European leveraged finance: Choosing the right path

European leveraged finance markets paused for breath in 2022, due to rising interest rates, volatile geopolitics and a tightening of financial markets across the board—but what can we expect in 2023?

Foreword

Heading into 2023, European leveraged finance markets continue to deal with fierce headwinds, following 12 months of economic and geopolitical volatility that has prompted a general slowdown in issuance. What does this mean for the months ahead?

After the record-setting leveraged finance activity seen in 2021—as companies scrambled to refinance, M&A activity spiked and private equity (PE) went on a shopping spree—it was clear that pace was not likely to continue.

But in 2022, as the tail end of the pandemic worked its way through markets, companies were suddenly faced with a new reality. Conflict erupted in Ukraine, oil prices climbed and supply chains were disrupted. A decade of low inflation and interest rates came to an end across Europe. Financing began to tighten as debt became increasingly expensive.

By the end of 2022, while European leveraged loan and high yield bond markets began to see activity, it was well below normal levels and followed a prolonged period of lower issuances. Leveraged loan issuance in Western and Southern Europe was down 37 per cent year-on-year, while high yield bonds fell by 66 per cent during the same period. The third quarter of the year was one of the lowest quarterly totals for leveraged finance issuance in the region on Debtwire Par record.

In both cases, higher pricing was a major factor as it continued to climb throughout the year. On leveraged loans, almost 40 per cent of all deals saw original issue discounts (OIDs) of two or more points from par—by Q4, it was not unheard of for there to be OIDs in the low 90s on term loan B facilities. On the bond side, pricing seemed to finally peak by the end of the year, but only after six quarters of consistent rises.

Eye on the prize

At the same time, there were a few bright spots for leveraged finance markets throughout the year.

First and foremost, buyout activity remained active in the first half of 2022 before dropping off in the second half. Notable deals include KKR’s €3.4 billion-equivalent acquisition of independent beverage bottler Refresco and Bain’s purchase of human resource consultants House of HR, backed by a €1.145 billion term loan and a €415 million note.

Second, new money financing represented a significant proportion of total issuance early in the year, as issuers raised term loan facilities to partially refinance drawn revolvers and fund new acquisitions. As with everything else, however, headwinds meant that most of the new money facilities issued towards the end of the year were smaller add-ons.

Third, CLOs continued to perform consistently (though they were not immune to the general slowdown in the market). Overall, there was €26.1 billion in issuance in 2022—down 32 per cent year-on-year but, in November alone, there was almost €3 billion in new CLO issuance, well above historical monthly averages, according to Debtwire Par.

The path ahead

While there are still shadows on the horizon, the cyclical nature of leveraged finance means that there are always new opportunities. The key is to be prepared.

For example, inflation is starting to plateau in many jurisdictions, but interest rate rises may continue—in the UK, for example, in December, the Bank of England raised the benchmark to 3.5 per cent, up from 3 per cent. This was the ninth consecutive hike since December 2021, placing the rate at its highest level for 14 years. Companies will need to consider their options carefully to get their costs under control.

For those looking to pro-actively manage their debt, amend-and-extend facilities may be the best place to start. Small add-ons and maturity extensions will help many find their way through the forest until macro-economic conditions improve.

Those with the highest-quality credits will reap the benefits of the liquidity available in the market by upsizing as well as via likely tighter pricing during syndication (when compared to balance sheet lending). For example, Debtwire Par reports that French telephony firm Iliad and automotive supplier Valeo entered the market with €500 million notes, and both were upsized during syndication to €750 million.

While this points to a potentially bifurcated European market in the months ahead, where solid credits remain healthy and those already struggling may face an uphill battle, liquidity on the equity and debt ledgers remains strong, and leveraged finance activity is likely to pick up further to address their respective needs.

Hitting the brakes: European leveraged finance battens down the hatches

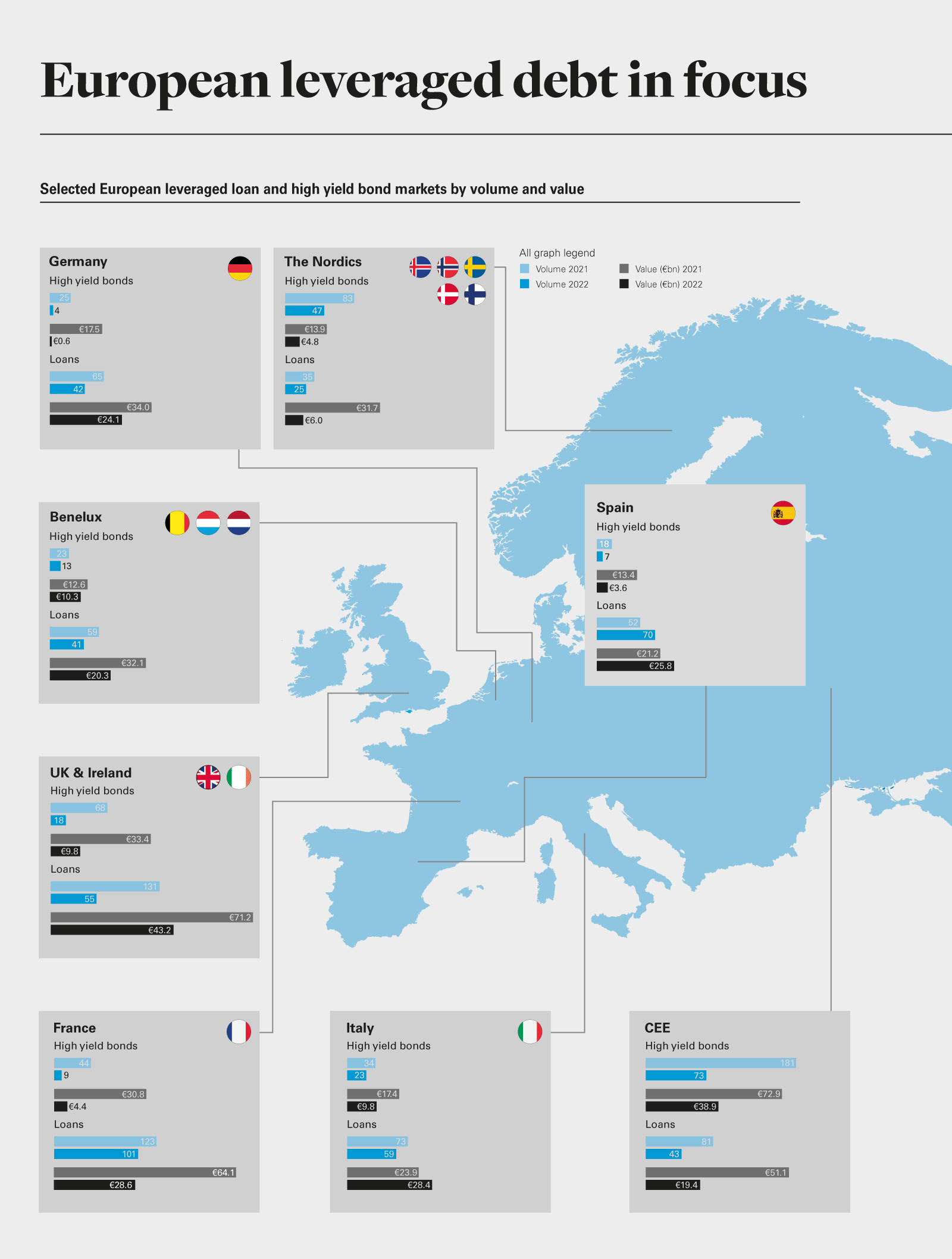

Leveraged loan issuance in Western and Southern Europe reached €183.4 billion in 2022, down by 37 per cent year-on-year

High yield bond activity was down 66 per cent during the same period, at €50 billion

Loan margins were up by 0.64 per cent by the end of the year, while average yields to maturity for high yield bonds climbed by nearly 3 per cent

UK leveraged finance markets have come through a challenging period in 2022, with issuance across leveraged loan and high yield markets declining as rising interest rates, inflation and the conflict in Ukraine hit activity.

UK leveraged finance issuance in 2022 fell by just over 50 per cent year-on-year, tracking the drop off in issuance observed across the wider European market. Private debt lending has proven more resilient but has also felt the impact of rate hikes and geopolitical uncertainty, with fundraising markets and deal flow from M&A targets tightening through the course of the year.

The UK market faced a unique set of challenges. As a result, the Bank of England (BOE) hiked interest rates nine times through the course of 2022 to 3.5, the highest level observed since the 2008 financial crisis. The European Central Bank (ECB), meanwhile, upped rates four times in 2022, with its benchmark rate now sitting at 2.5 per cent to 1 per cent below the BOE level.

UK lenders and borrowers were already contending with political volatility, in the form of successive changes of prime minister and a catastrophic "mini-budget" in late September 2022. This catalysed a slew of collateral calls and forced sales of UK government bonds, requiring the BOE to step in and backstop bond markets to prevent the dislocation from spreading into other parts of the economy. Financing conditions are expected to remain calm in 2023 in the UK, with limited impetus to kickstart markets back into life.

But there are some early signs of green shoots. For example, after raising rates in December 2022, the BOE argued that inflation may have peaked, slowing from the four-decade highs recorded earlier in the year. Assuming inflation has topped out as predicted, there will be more scope for the UK central bank to halt or slow any further interest rate rises.

A change in the direction of travel on rates will provide issuers and investors with more certainty, help debt prices in secondary markets to recover and encourage primary issuers to come forward and test market appetite for new debt issuance.

The drop in corporate valuations and the weaker price of sterling relative to the US dollar and euro, meanwhile, could drive significant interest from overseas buyers on UK take-private deals in 2023.

Appetite for UK take-private deals has remained strong in 2022, despite macro-economic headwinds. According to Dealogic, UK companies valued at more than £40 billion were already taken off UK public markets in the first nine months of 2022. Public-to-private transactions are expected to continue providing a pipeline of M&A deals and financing opportunities in 2023.

Conclusion

Stalled issuance, growing concerns around rising costs, supply chain bottlenecks and the conflict in Ukraine—it's been a whirlwind of a year, with many remaining challenges for the year ahead

Rising interest rates and reduced refinancing options are increasing the likelihood of restructuring and financial distress in the next 12 months

Cov-lite debt packages have given borrowers breathing room, but may conceal underlying distress

Issuers in stable sectors have negotiated amend-and-extend (A&E) deals to push out maturity cliff edges, but not all borrowers have that option

Borrowers and lenders have dusted off their hard hats and rolled up their sleeves in anticipation of an increase in restructuring and distressed debt situations in 2023.

For the first time in more than a decade, European leveraged finance markets, private equity (PE) sponsors and management teams are feeling the pressure from rising interest rates on capital structures, introduced to stem the steady rise in inflation.

The build-up of cash during more benign market conditions in the past 18 months, coupled with the fact that borrowers took advantage of buoyant debt markets in 2021 to refinance and extend maturities, shielded credits from the immediate impact of rising interest rates in 2022.

In 2023, however, market conditions have worsened materially as the full impact of the cost of living crisis and the ongoing war in Ukraine begin to bite. Higher interest payments are now taking a toll on cashflow and the option to refinance out of a tight spot is no longer on the table, with leveraged loan and high yield bond issuance earmarked for refinancing down by 51 per cent and 79 per cent respectively in 2022. High yield funds, meanwhile, have faced significant outflow through the course of 2022, limiting the capital available for refinancing.

According to Refinitiv Lipper, in the first nine months of 2022, the outflow from global bond funds had already reached its highest level in 20 years, at US$175.5 billion.

As these headwinds intensify, many borrowers that were once in a relatively comfortable position when it came to servicing capital structures may find themselves stretched. And borrowers that are running out of cash can no longer bank on raising new financing with relative ease.

Exploring options

Debt packages issued in the past five years have few or no covenants, so lender protections that might have triggered an early warning are not in place, thereby concealing underlying problems

As pressures mount, the first ripples of distress are already being felt. Bankruptcies and corporate insolvencies in the EU and the UK recorded double-digit increases in 2022 and, according to forecasts from Allianz, the UK, France and Germany may see business insolvencies climb by 29 per cent, 10 per cent and 17 per cent respectively in 2023.

According to Fitch Ratings, meanwhile, European credit defaults are expected to more than double in 2023, with high yield defaults forecast to rise from 0.7 per cent in 2022 to 2.5 per cent by the end of 2023, and leveraged loan defaults set to climb from 1.3 per cent to 4.5 per cent during the same period.

There is also likely to be a cohort of borrowers that do not appear to be in obvious distress but may be feeling the squeeze behind the scenes. Debt packages issued in the past five years have few or no covenants, so lender protections that might have triggered an early warning are not in place, thereby concealing underlying problems. As a result, some borrowers may not immediately seek out covenant waivers and facility amendments from their lenders. But when challenging market conditions really take hold, those same borrowers will be facing even more critical concerns as facility maturities approach and cash begins to run out. Restructuring under those circumstances will likely be more difficult and the financial pain suffered by borrower and lender alike could be significant.

The fact that most borrowers took the opportunity to refinance and do not have to meet covenant tests, however, has given them some breathing room. Many are now exploring their options proactively to avoid a potential full-blown restructuring or insolvency down the road.

Borrowers facing maturities in the next 12 to 24 months are already undertaking exchange offers and amend-and-extend deals that offer a mix of higher coupons, refreshed call protection, improved covenant packages, better collateral protection, equity injections and debt paydowns in return for extending maturity runways. PE-backed generic pharmaceuticals group Stada and consumer finance group NewDay were among the first borrowers to bring forward amend-and-extend options, followed by a string of companies taking the same path.

Some PE sponsors may also agree to put additional capital into a portfolio company, but ideally only if that capital can go in at the top of the capital structure as super-senior debt. Lenders are adopting a similar playbook when injecting additional funding into businesses following debt-for-equity swaps.

Barings and Farallon Capital Management, for example, swapped a portion of the debt they held in UK cinema chain Vue for equity, and injected an additional £75 million of cash into the business in the form of a super-senior term loan.

Borrowers that move early to head off restructuring risk early will likely be in the best position to renegotiate debt packages consensually with lenders. The timing may be ideal, as many lenders will be open to supporting liability management plans rather than crystallising losses or facing the reputational risks that come with enforcing a restructuring.

Given the relatively borrower-friendly terms in recent debt documents, it is possible to imagine a wave of "stage 1" restructuring processes in 2023 where lenders agree to a degree of short-term relief. This may include limited debt service relief or injecting new capital on a senior basis in return for more traditional lender protections being re-inserted in the debt documents. These may include financial covenants or allow lenders to trade their debt more freely.

Not all credits, however, will be able to undertake amend-and-extend (A&E) deals. To date, successful A&E transactions have been brought forward by companies that are performing well and based in stable sectors, such as healthcare, infrastructure and TMT. An A&E deal brought forward by French medical diagnostics company Sebia, for example, was well received by existing and new lenders.

Borrowers also must ensure that any amendments to pricing and terms are attractive enough to get lenders onboard. For example, Debtwire Par reports that one lender decided against getting behind an extension deal brought forward by UK sports betting company Entain because the pricing was deemed to be too tight.

PE firms, meanwhile, are expected to triage portfolios and only invest resources in liability management exercises when portfolio companies are expected to return to growth in the medium-to-long term. There will be limited appetite from sponsors to inject equity and time resources into companies that are unlikely to improve in the year ahead. Parties are also grappling with the challenges presented by CLO investors that are unable to extend their investment periods due to underlying constitutional restrictions.

Credits trading at deep discounts to par will also be on the radar of distressed debt investors. Many will be preparing to buy up debt at a discount with a view to selling on the paper when prices recover, or positioning themselves to transfer debt positions into equity ownership if borrowers run aground and run out of cash. Specialist players will also manoeuvre into capital structures by offering to inject more cash into a business if their capital can sit at the top of the structure.

With the likes of J.P. Morgan and Zetland Capital both closing funds focused on investments in troubled businesses in 2022 and established distressed investment players Oaktree Capital Management and GoldenTree Asset Management approaching investors for additional capital, distressed debt players are set to play an increasingly prominent role in debt restructurings in the year ahead.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European leveraged debt in focus (PDF)

View full image: European leveraged debt in focus (PDF)

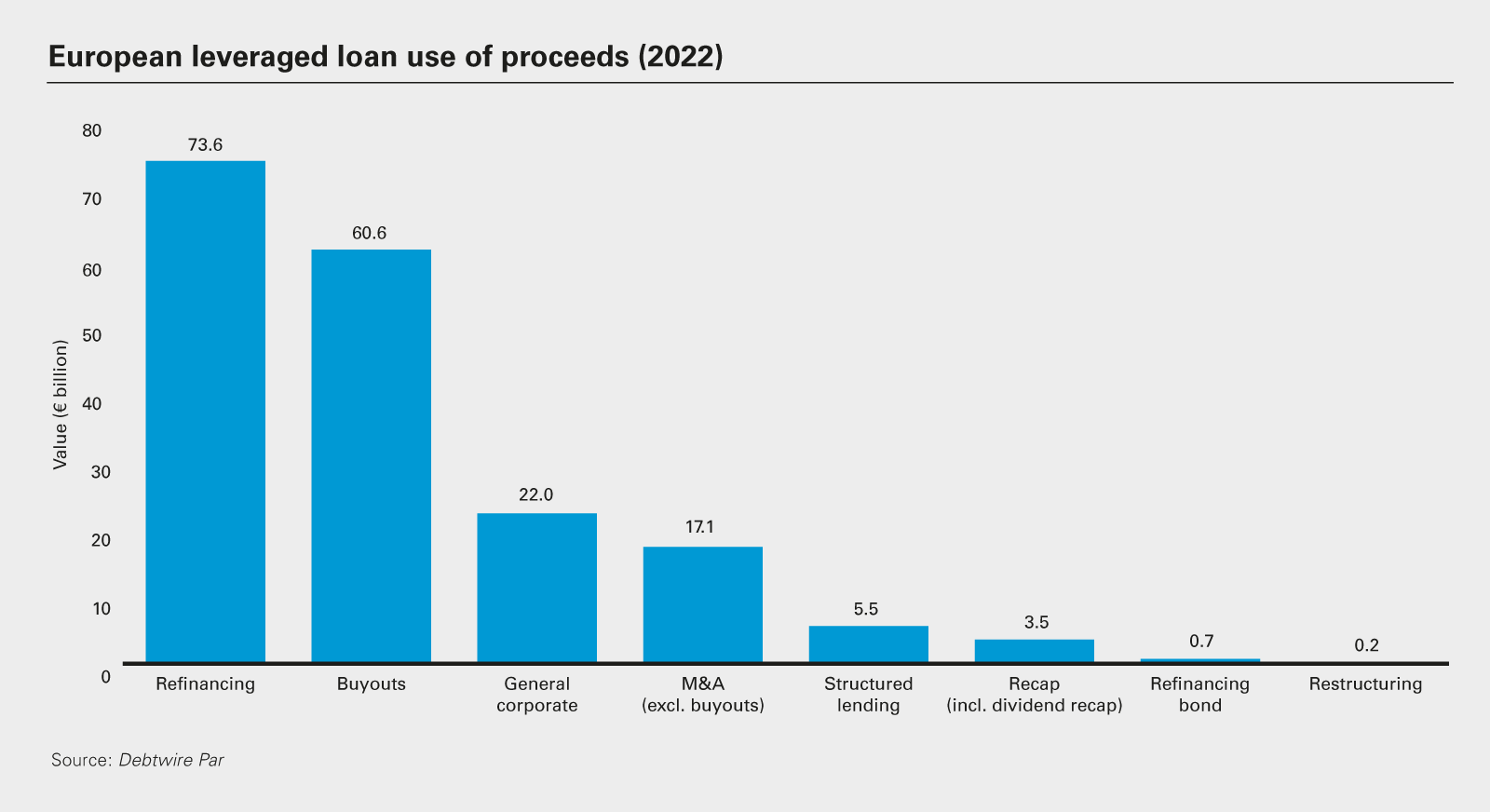

View full image: European leveraged loan use of proceeds (2022)

View full image: European leveraged loan use of proceeds (2022)

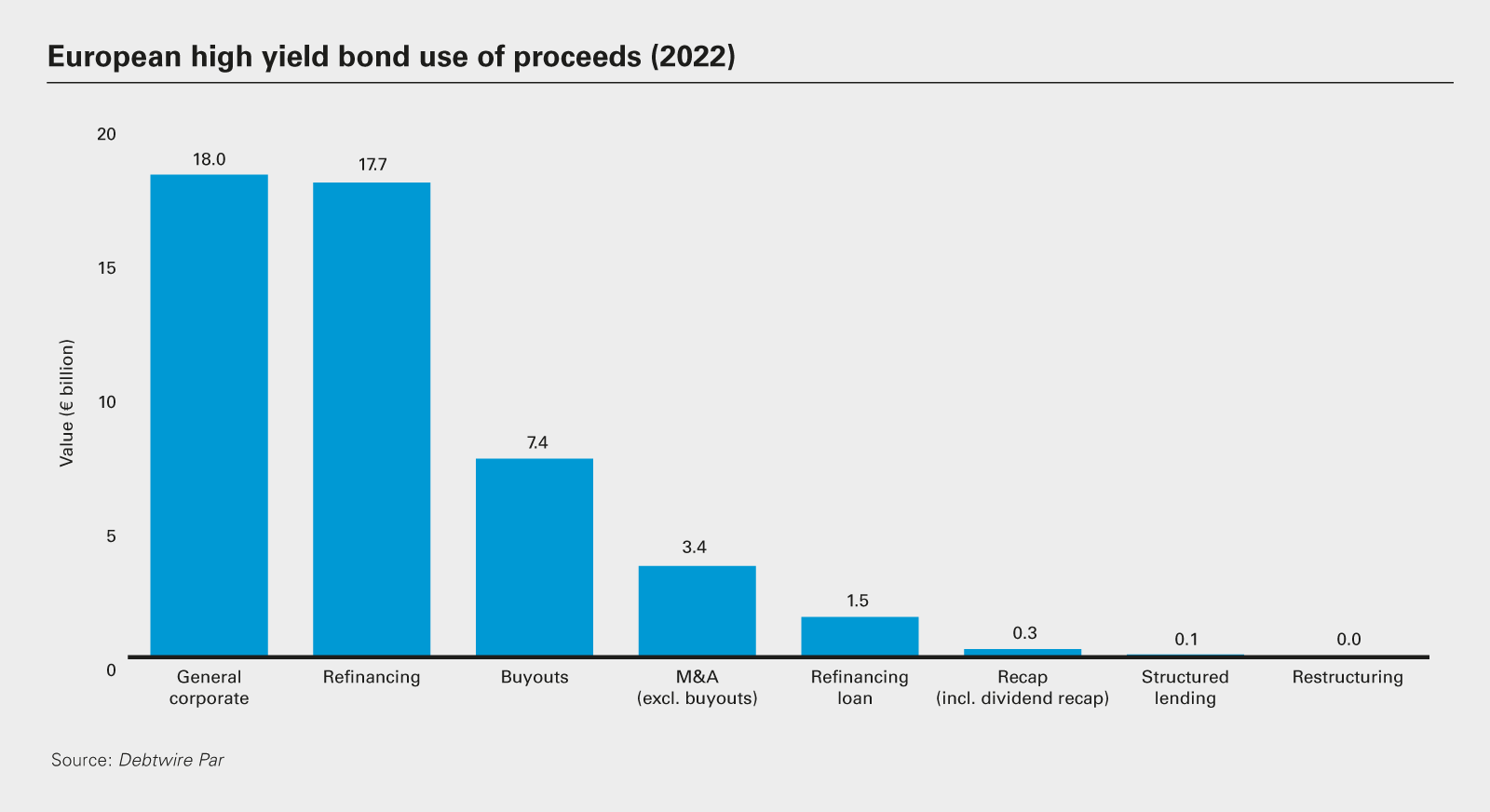

View full image: European high yield bond use of proceeds (2022)

View full image: European high yield bond use of proceeds (2022)