After the record-setting leveraged finance activity seen in 2021—as companies scrambled to refinance, M&A activity spiked and private equity (PE) went on a shopping spree—it was clear that pace was not likely to continue.

But in 2022, as the tail end of the pandemic worked its way through markets, companies were suddenly faced with a new reality. Conflict erupted in Ukraine, oil prices climbed and supply chains were disrupted. A decade of low inflation and interest rates came to an end across Europe. Financing began to tighten as debt became increasingly expensive.

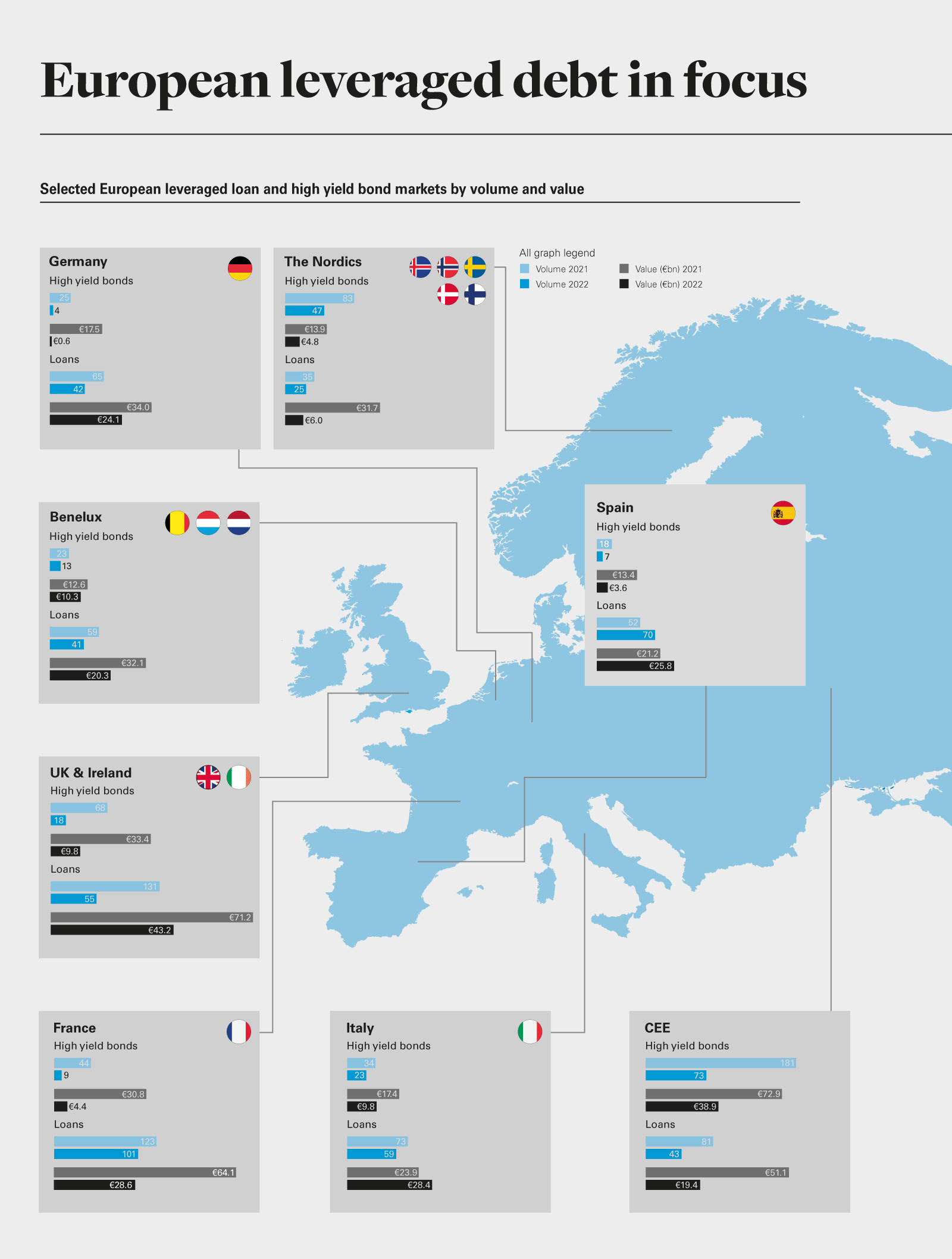

By the end of 2022, while European leveraged loan and high yield bond markets began to see activity, it was well below normal levels and followed a prolonged period of lower issuances. Leveraged loan issuance in Western and Southern Europe was down 37 per cent year-on-year, while high yield bonds fell by 66 per cent during the same period. The third quarter of the year was one of the lowest quarterly totals for leveraged finance issuance in the region on Debtwire Par record.

In both cases, higher pricing was a major factor as it continued to climb throughout the year. On leveraged loans, almost 40 per cent of all deals saw original issue discounts (OIDs) of two or more points from par—by Q4, it was not unheard of for there to be OIDs in the low 90s on term loan B facilities. On the bond side, pricing seemed to finally peak by the end of the year, but only after six quarters of consistent rises.

Eye on the prize

At the same time, there were a few bright spots for leveraged finance markets throughout the year.

First and foremost, buyout activity remained active in the first half of 2022 before dropping off in the second half. Notable deals include KKR’s €3.4 billion-equivalent acquisition of independent beverage bottler Refresco and Bain’s purchase of human resource consultants House of HR, backed by a €1.145 billion term loan and a €415 million note.

Second, new money financing represented a significant proportion of total issuance early in the year, as issuers raised term loan facilities to partially refinance drawn revolvers and fund new acquisitions. As with everything else, however, headwinds meant that most of the new money facilities issued towards the end of the year were smaller add-ons.

Third, CLOs continued to perform consistently (though they were not immune to the general slowdown in the market). Overall, there was €26.1 billion in issuance in 2022—down 32 per cent year-on-year but, in November alone, there was almost €3 billion in new CLO issuance, well above historical monthly averages, according to Debtwire Par.

The path ahead

While there are still shadows on the horizon, the cyclical nature of leveraged finance means that there are always new opportunities. The key is to be prepared.

For example, inflation is starting to plateau in many jurisdictions, but interest rate rises may continue—in the UK, for example, in December, the Bank of England raised the benchmark to 3.5 per cent, up from 3 per cent. This was the ninth consecutive hike since December 2021, placing the rate at its highest level for 14 years. Companies will need to consider their options carefully to get their costs under control.

For those looking to pro-actively manage their debt, amend-and-extend facilities may be the best place to start. Small add-ons and maturity extensions will help many find their way through the forest until macro-economic conditions improve.

Those with the highest-quality credits will reap the benefits of the liquidity available in the market by upsizing as well as via likely tighter pricing during syndication (when compared to balance sheet lending). For example, Debtwire Par reports that French telephony firm Iliad and automotive supplier Valeo entered the market with €500 million notes, and both were upsized during syndication to €750 million.

While this points to a potentially bifurcated European market in the months ahead, where solid credits remain healthy and those already struggling may face an uphill battle, liquidity on the equity and debt ledgers remains strong, and leveraged finance activity is likely to pick up further to address their respective needs.

View full image: European leveraged debt in focus (PDF)

View full image: European leveraged debt in focus (PDF)