As we embark on our third year of Latin America Focus, the ever-evolving landscape in the region brings fresh opportunities and challenges for local, regional and international businesses.

After an extremely positive post-Covid growth spurt in 2022, so far 2023 has been a bit more challenging for the region with GDP growth slowing and political uncertainty increasing. Nevertheless, we see plenty of bright spots on the horizon and opportunities for those who know where to find them.

In our third compendium of market insight from the Latin America team at White & Case, we look at what those opportunities are and where challenges might arise for investors.

On the opportunity front, we examine the mining & metals industry in detail. Interest in the region's lithium reserves has soared with the continued growing demand for the mineral for the battery manufacturing process. The "lithium triangle" has turned into a "lithium quad" with Brazil joining Chile, Argentina and Bolivia as a significant supplier of lithium. However, the countries' differing approaches to regulation of the industry means that those looking to source lithium in the region will have to understand the market in each country to determine where, when and how to make significant investments.

The lithium market could potentially be the beneficiary of another Latin American trend: Nearshoring. In a world of escalating geopolitical volatility, there is a shift away from broader globalization towards a more localized approach to manufacturing and trade. Several countries in Latin America have implemented investment and tax treaties, which, along with the ongoing geopolitical shift, make the establishment of industrial plants in the region easier and more enticing than ever before.

In this issue, we also take a look at environmental, social and governance (ESG) considerations; compared to their counterparts in North America or Europe, Latin American companies have arguably been slower to respond to the trend to disclose their approach to ESG. However, within the region this varies widely depending on the industry, as our recent survey of private issuers has shown.

As ever in our volatile world, the threat of market shocks and their impact on businesses and industries remains constant. Three major Latin American airlines and a variety of other businesses recently went through lengthy and difficult insolvency procedures following the Covid crisis. The good news is that most of these businesses are now back on track and performing very well, thanks in part to the creative and unprecedented use of Chapter 11 of the US Bankruptcy Code as well as local insolvency regimes to restructure the debt and the capital structures of the effected companies.

Another bright spot for investors in Latin America in recent years is that international arbitration in the region continues to develop in remarkable fashion, providing foreign investors with recourse to fair and impartial justice when investment disputes arise.

We at White & Case continue to believe that the Latin American market holds long-term promise for the savvy investor. We hope that you find this issue of Latin America Focus, which contains articles from our top experts on the subjects referenced above, interesting and useful as you embark on additional business in the region.

Sustainability disclosures gain momentum among Latin American issuers

Navigating turbulence: Latin American airlines in chapter 11

US chapter 11 is a powerful restructuring tool for foreign-based airlines, with effects across the globe. There can be little doubt that, as international companies continue to face financial distress, they will continue to turn to the benefits and protections of the US Bankruptcy Code for relief.

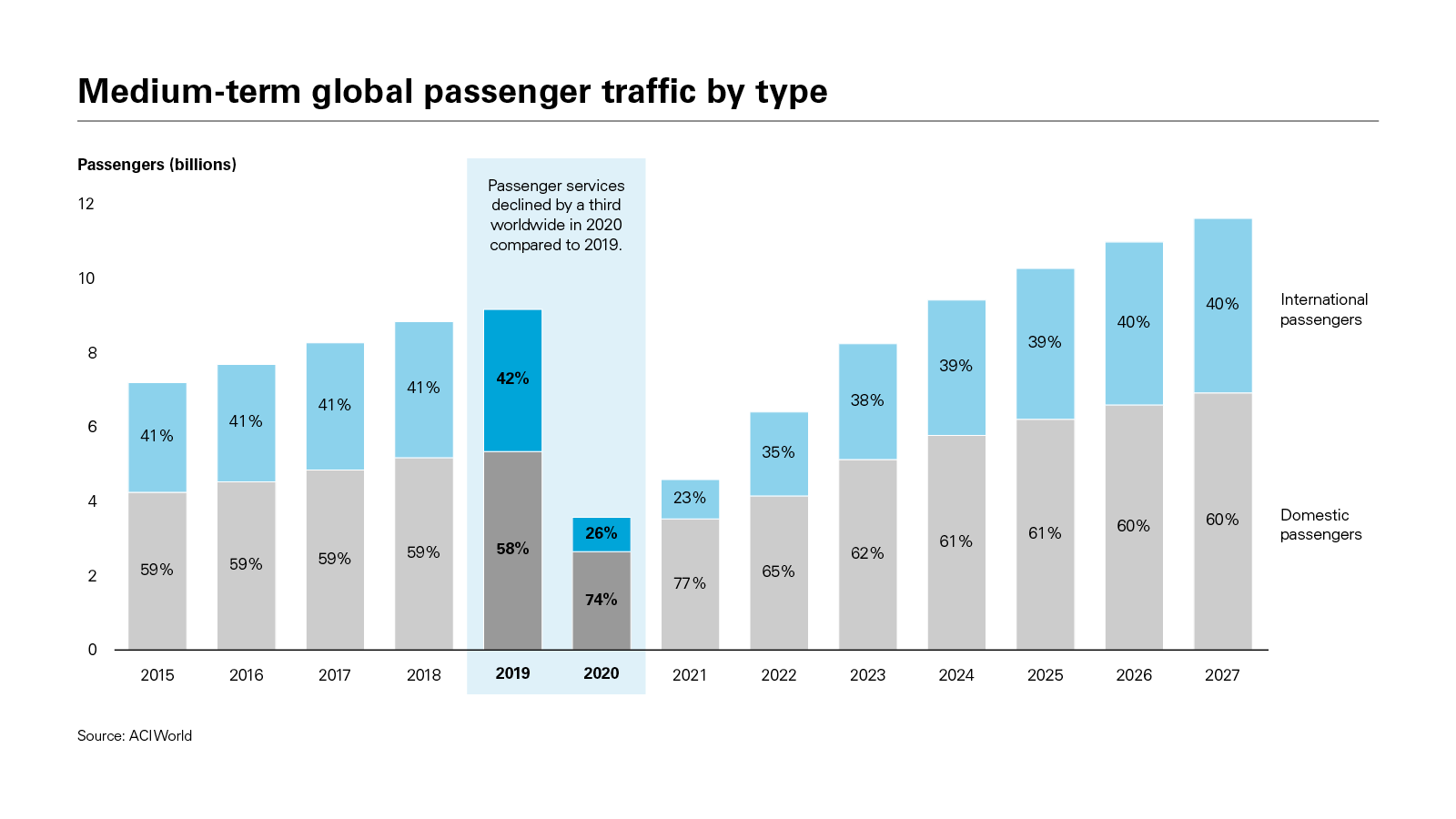

Few sectors were more affected by the global COVID-19 pandemic than passenger air service

US$21 billion

Revenue losses in passenger air travel in Latin America and the Caribbean exceeded US$21 billion between 2019 and 2020

Few sectors were more affected by the global COVID-19 pandemic than passenger air service. With countries around the world in lockdown, passenger services declined drastically—dropping by a third worldwide in 2020 compared to 2019, and almost halving in Latin America and the Caribbean, although the number of cargo flights rose slightly.

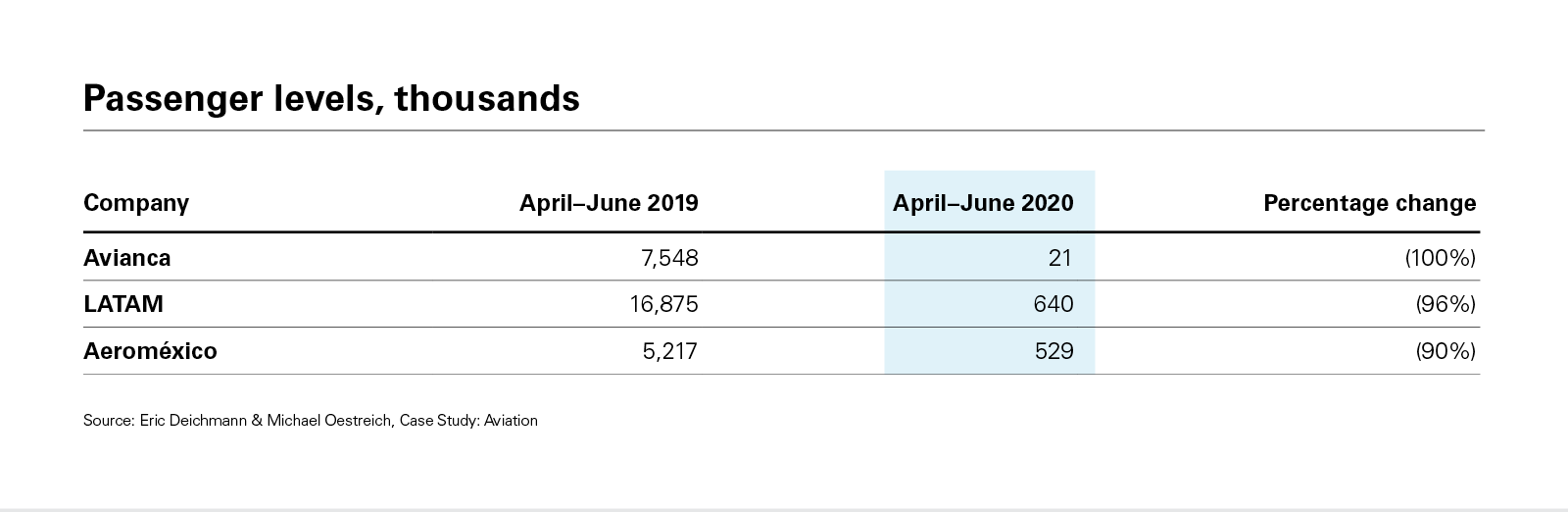

Passenger numbers between April and June 2020 were particularly impacted, with numbers for Latin America's biggest airlines plummeting from millions to just a few thousand in those three months compared to the previous year. International Civil Aviation Organization and ADS-B Flightaware data show revenue losses between 2019 and 2020 exceeded US$372 billion globally and US$21 billion in Latin America and the Caribbean.

In the wake of the pandemic, several foreign airlines have relied on chapter 11 protection in the US to restructure in lieu of local insolvency laws. Chapter 11 enables distressed companies to, among other things, restructure obligations, obtain new funding, renegotiate or reject leases and other burdensome contracts, abandon or sell assets, and stay enforcement actions both within and outside of the United States.

As recent airline cases demonstrate, these are powerful tools for financial and operational restructurings. Despite these benefits, however, proceeding under chapter 11 also presents distinct challenges for non-US carriers with international operations.

Unlike the US and countries in Europe, Asia-Pacific and other jurisdictions, which provided billions of dollars in grants and loans to their aviation industries, Latin American countries provided limited or no state aid to airlines to offset losses from the COVID-19 pandemic. As a result, many Latin American airlines, including Avianca, Aeroméxico and LATAM, have since filed for chapter 11 protection in the US.

Chapter 11 provides useful tools that may not be available, or as tested, in other insolvency regimes, and which may be of particular interest to airlines in financial distress. These essential elements make it an attractive restructuring option for Latin America-based airlines.

Eligibility

The jurisdictional requirements for chapter 11 are easily satisfied. A company may file chapter 11 as long as it owns some property in the US. There is no requirement that the company be domiciled or organized under the laws of the US or that it have significant business operations in the US. Therefore, all of the affiliated entities in a business enterprise regardless, of their jurisdictions—including offshore financing entities—can file together in one court before the same judge. Unlike many Latin American insolvency regimes, a voluntary chapter 11 filing does not require that the company be insolvent, but only that the company be experiencing financial distress.

That said, a chapter 11 petition may be subject to dismissal if filed in bad faith or if connections to the US are too remote to effectively implement reorganization under US law.

Passenger services declined by a third worldwide in 2020 compared to 2019

Debtor-in-possession financing and new money

A valuable tool in chapter 11 is the ability of a debtor to obtain financing while under bankruptcy protection under section 364 of the Bankruptcy Code—commonly referred to as debtor-in-possession (DIP) financing. DIP financing provides a company with sufficient capital to continue operating its business while it attempts to implement a restructuring. DIP financing often takes priority over existing debt and equity claims. Recent chapter 11 cases involving Latin American airlines have relied on DIP financing not only for new money, but also to keep existing shareholders in the capital structure.

Worldwide automatic stay

Upon filing a chapter 11 petition, a statutory automatic stay takes immediate effect to enjoin substantially all creditor enforcement actions against the debtor and its property, wherever located, during the entire case under section 362 of the Bankruptcy Code. An automatic stay is not available in many Latin American jurisdictions, where local law often requires a court order to initiate a limited stay period that is effective only in that country.

Similarly, US bankruptcy protection also allows debtors to bind foreign creditors to the chapter 11 process. In the Avianca case, for example, the Bankruptcy Court imposed sanctions against more than 150 creditors who continued to litigate pre-petition claims in Colombia and Brazil one year after confirmation of the airline's chapter 11 plan. By filing proofs of claim in the chapter 11 cases, those creditors had submitted to the jurisdiction of the Bankruptcy Court. The court determined that it would conditionally disallow such claims unless the creditors discontinued their foreign lawsuits within 30 days of the date of the order.

Tools for fleet restructuring

Critical among the benefits of chapter 11, the Bankruptcy Code also enables an airline to right-size its fleet by eliminating burdensome aircraft-related debt obligations and exercising rights to purchase aircraft on favorable terms. Chapter 11 is particularly useful for fleet restructuring because aircraft lessors and other significant stakeholders are familiar with the process and many aircraft and engine leases, as well as debt agreements, are governed under New York law, and may include New York forum selection clauses.

Generally, section 1110 of the Bankruptcy Code provides special protections for lessors, vendors and secured parties holding interests in aircraft or associated machinery, such as engines, appliances, parts and related documents. These protections mitigate otherwise applicable provisions of the Bankruptcy Code, thereby reducing the risks and lessening the financing costs associated with qualifying aircraft equipment.

Importantly, section 1110 applies only to chapter 11 cases of US air carriers and certain water carriers. Similarly, less robust relief may apply to air carriers in countries party to the Aircraft Protocol to the Cape Town Convention (CTC), if the carrier's home country, or “insolvency jurisdiction,” has adopted the strong “Alternative A” insolvency provision of Article 11 of the Aircraft Protocol.

Although the US is a signatory to the CTC, it has not adopted Alternative A, and the relevant choice of law and treaty rules that would allow the application Alternative A in a chapter 11 case of a non-US air carrier has not been fully opined on by any US Bankruptcy Court.

In the case of Latin America-based airlines and other non-US carriers, aircraft lessors are arguably left only with the substantially weaker protections afforded by section 365(b)(5) of the Bankruptcy Code, which generally applies to all equipment lessors and offers less protection. Creditors with security interests in aircraft equipment may have no special protections at all.

In the face of such uncertainties, foreign-based airlines and their aircraft lessors and financiers often negotiate stipulations to provide some enhanced protection to lessors and secured parties pending ultimate determinations about whether aircraft leases and financing arrangements should continue post-bankruptcy and, if so, in what form.

Unfortunately for financiers and lessors of aircraft equipment during the COVID-19 pandemic, the ordinarily robust demand for such equipment largely disappeared. As a result, most of these protections were of limited value because obtaining surrender of the equipment was no guarantee of a good recovery.

Given this lack of leverage, the stipulations negotiated during the pandemic provided for modified rent payments on a “power-by-the-hour” basis at new market rates, with certain additional payments for maintenance, so that the airline would have to pay only according to usage pending its decision to keep or reject each lease. If an airline decided to keep an aircraft, its lease terms could be renegotiated on market terms. Alternatively, if the aircraft was not needed or the lessor refused to renegotiate, the lease could be rejected and, if needed, replacement aircraft could be sought in the market, with lease rejection damages generally becoming unsecured claims against the bankruptcy estate. Other key agreements were similarly restructured to match changed capacity, including aircraft purchase agreements and associated maintenance contracts.

Recent chapter 11 cases of Latin American airlines

In re Avianca Holdings, S.A., Case No. 20-11133 (Bankr. S.D.N.Y.), Colombian airline Avianca, the second-largest airline in Latin America, filed for chapter 11 on May 10, 2020, citing the pandemic and the Colombian government's shutdown of its airspace. Avianca's plan of reorganization was approved by all classes of creditors and successfully absolved approximately US$3 billion in debt, enabling the airline to infuse fresh capital amounting to approximately US$1.7 billion. It emerged from chapter 11 on December 1, 2021.

In re Grupo Aeromexico, S.A.B. de C.V., Case No. 20-11563 (Bankr. S.D.N.Y.), Mexico's flagship carrier and leading airline, filed for chapter 11 on June 30, 2020, and emerged on March 17, 2022. Through the chapter 11 process, Aeroméxico overhauled, updated and restructured its aircraft fleet, saving almost US$2 billion related to ongoing fleet obligations, and reached comprehensive settlements with all of its unionized labor groups.

In addition, the exit financing approved in the chapter 11 cases provided Aeroméxico with US$720 million of new equity capital through the issuance of new equity and up to US$762.5 million of new debt capital through the issuance of senior secured first-lien notes. The airline also financed a transaction by which the owner and operator of Aeroméxico's loyalty program became a wholly owned subsidiary of Aeroméxico.

In re LATAM Airlines Group S.A., Case No. 20-11254 (Bankr. S.D.N.Y.) commenced chapter 11 proceedings on May 26, 2020. Seeking to restore operational stability, the debtor group sought approval of US$2.45 billion in DIP financing, with a significant portion—US$900 million—to be provided by its largest shareholders, who received a lucrative option to convert their debt into shares of the new LATAM.

A group of LATAM creditors objected to this arrangement. They engaged in a week-long hearing, after which the court ruled against the proposed equity value transfer to existing shareholders.

Subsequently, LATAM introduced a modified DIP financing proposal that was uncontested and successfully secured approval on September 17, 2020. In April 2022, when the debtors sought to extend or refinance its US$2.45 billion DIP facility, members of the bondholder group committed to providing the debtors with more than US$400 million on a junior basis as part of a new DIP Facility. Junior creditors contested the claims held by the senior bondholders, but on the eve of the confirmation hearing, these objections were settled, and the bondholder group received payment in full, plus reimbursement of their expenses.

On November 3, 2022, LATAM Airlines Group officially exited bankruptcy protection following the successful completion of its financial restructuring to emerge as a more efficient group with a modernized fleet, a strengthened financial position of more than US$2.2 billion of liquidity and US$3.6 billion or 35 percent less debt.

Conflicting laws in cross-border insolvency cases

The chapter 11 cases of Avianca, Aeromexico and LATAM best illustrate many of the benefits of chapter 11, as well as the challenges and creative solutions that inevitably arise to resolve conflicts between the Bankruptcy Code and foreign local law applicable to foreign debtors. Fundamental among these conflicts is the tension between the absolute priority rule contained in the Bankruptcy Code on the one hand, and on the other, the exclusive right of existing shareholders under many foreign laws to approve the terms of, or participate in, or exercise preemptive rights in, a capital raise.

Under section 1129(b) of the Bankruptcy Code, a class of creditors or equity holders generally may not recover at the expense of a dissenting class of more senior creditors. Unless creditors are paid in full or agree otherwise, therefore, existing shareholders generally cannot retain value in a chapter 11 case.

Nevertheless, shareholders may buy back into the capital structure by providing new value on market terms. This type of equity conversion has featured prominently in foreign airlines' chapter 11 cases, with varying results. In Avianca and Aeromexico, for example, the debtors obtained approval of DIP facilities containing an equity conversion option—in the first case at the lenders' option and the second at the debtors' option. In Aeromexico, existing shareholders agreed to approve the capital increase required for the DIP conversion.

In LATAM, however, the Bankruptcy Court declined to approve a similar structure. Agreeing with the objections raised by the Ad Hoc Group of LATAM bondholders, who held New York law-governed notes, the Bankruptcy Court determined that LATAM's proposed equity subscription election gave rise to improper sub rosa plan treatment in violation of the absolute-priority rule. As initially proposed, the DIP facility included an equity conversion option, which was reserved solely for the tranche provided by shareholders in exchange for, among other things, a waiver of their preemptive rights under Chilean law to participate in any issuance of equity.

As proposed, the DIP would have provided new equity to existing shareholders at a pre-determined discount to plan value, and, because this discount applied regardless of the plan proposed by the debtors, controlled by the same shareholders, the DIP facility constituted a sub rosa plan. This is a rare instance of a US bankruptcy court denying a DIP financing request based on an illegal sub rosa plan, and the decision is expected to have a dramatic impact on future bankruptcy cases.

As demonstrated most recently in the cases of three of the largest airlines in Latin America, chapter 11 is a powerful restructuring tool across a variety of circumstances and with effects across the globe. There can be little doubt that, as international companies continue to face financial distress, they will continue to turn to the benefits and protections of the US Bankruptcy Code for relief.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Medium-term global passenger traffic by type (PDF)

View full image: Medium-term global passenger traffic by type (PDF)

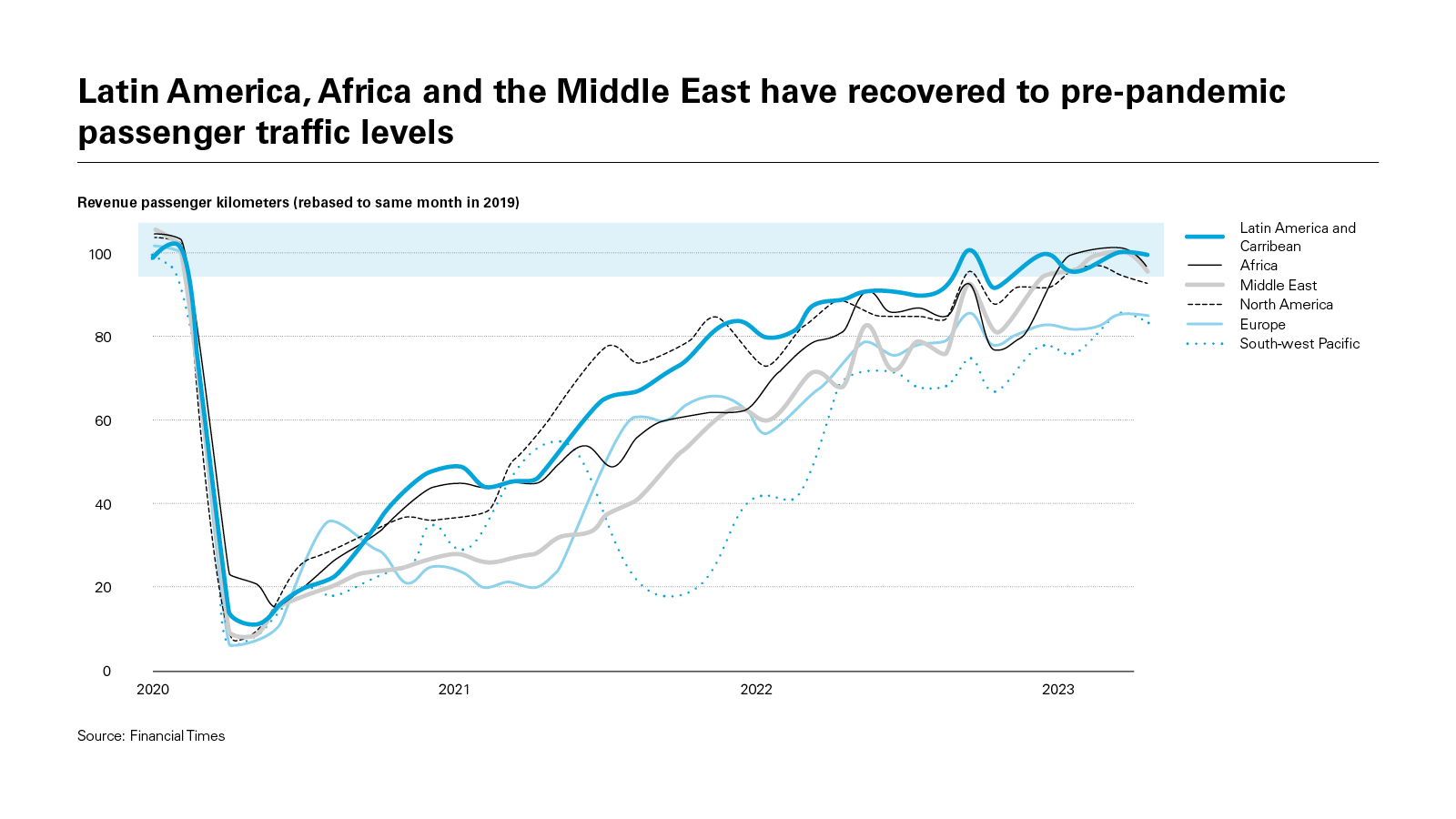

View full image: Latin America, Africa and the Middle East have recovered to pre-pandemic passenger traffic levels (PDF)

View full image: Latin America, Africa and the Middle East have recovered to pre-pandemic passenger traffic levels (PDF)

View full image: Passenger levels, thousands (PDF)

View full image: Passenger levels, thousands (PDF)