As we embark on our third year of Latin America Focus, the ever-evolving landscape in the region brings fresh opportunities and challenges for local, regional and international businesses.

After an extremely positive post-Covid growth spurt in 2022, so far 2023 has been a bit more challenging for the region with GDP growth slowing and political uncertainty increasing. Nevertheless, we see plenty of bright spots on the horizon and opportunities for those who know where to find them.

In our third compendium of market insight from the Latin America team at White & Case, we look at what those opportunities are and where challenges might arise for investors.

On the opportunity front, we examine the mining & metals industry in detail. Interest in the region's lithium reserves has soared with the continued growing demand for the mineral for the battery manufacturing process. The "lithium triangle" has turned into a "lithium quad" with Brazil joining Chile, Argentina and Bolivia as a significant supplier of lithium. However, the countries' differing approaches to regulation of the industry means that those looking to source lithium in the region will have to understand the market in each country to determine where, when and how to make significant investments.

The lithium market could potentially be the beneficiary of another Latin American trend: Nearshoring. In a world of escalating geopolitical volatility, there is a shift away from broader globalization towards a more localized approach to manufacturing and trade. Several countries in Latin America have implemented investment and tax treaties, which, along with the ongoing geopolitical shift, make the establishment of industrial plants in the region easier and more enticing than ever before.

In this issue, we also take a look at environmental, social and governance (ESG) considerations; compared to their counterparts in North America or Europe, Latin American companies have arguably been slower to respond to the trend to disclose their approach to ESG. However, within the region this varies widely depending on the industry, as our recent survey of private issuers has shown.

As ever in our volatile world, the threat of market shocks and their impact on businesses and industries remains constant. Three major Latin American airlines and a variety of other businesses recently went through lengthy and difficult insolvency procedures following the Covid crisis. The good news is that most of these businesses are now back on track and performing very well, thanks in part to the creative and unprecedented use of Chapter 11 of the US Bankruptcy Code as well as local insolvency regimes to restructure the debt and the capital structures of the effected companies.

Another bright spot for investors in Latin America in recent years is that international arbitration in the region continues to develop in remarkable fashion, providing foreign investors with recourse to fair and impartial justice when investment disputes arise.

We at White & Case continue to believe that the Latin American market holds long-term promise for the savvy investor. We hope that you find this issue of Latin America Focus, which contains articles from our top experts on the subjects referenced above, interesting and useful as you embark on additional business in the region.

Sustainability disclosures gain momentum among Latin American issuers

Sustainability disclosures gain momentum among Latin American issuers

Sustainability disclosures among Latin American issuers vary widely in terms of completeness, granularity and format, impacting their business, financial performance and attractiveness to investors. Investors and regulators are calling for greater standardization, consistency and transparency about the real impact of ESG policies.

In June 2023, White & Case conducted an in-depth review of environmental sustainability disclosures among 92 issuers headquartered in Latin America, who had already filed at leastone annual report with the SEC

As the number of ESG-badged products has grown, so has the number of ESG metrics and benchmarks, driving calls for greater standardization, consistency and transparency

After coming to the forefront in 2021 on the heels of mounting global concerns over climate change and social inequality, addressing environmental, social and governance (ESG) factors became the new normal for investors and businesses in 2022 and 2023. With ESG considerations rooted in mainstream markets, investors and regulators have demanded better reporting and compliance from businesses on their ESG performance.

As the number of ESG-badged equity and debt products has grown, so has the number of ESG metrics and benchmarks. This trend has driven calls for greater standardization, consistency and transparency regarding the real impact of ESG policies. Meanwhile, governments and economic blocs—against the backdrop of their

commitments under the Paris Agreement and subsequent agreements at international climate conferences COP26 and COP27—have incentives to encourage ESG integration through means that include voluntary and mandatory disclosure regimes.

This trend has ushered in a sea change for public securities in various markets. Perhaps the most critical change has been to reporting of environmental metrics. The European Commission advanced proposals for the Corporate Sustainability Due Diligence Directive, which are expected to be adopted by the end of 2023, and which outline requirements for large businesses to conduct due diligence to identify and address adverse impacts on the environment, produce climate plans, and require directors to consider environmental impacts of business decisions.

The US Securities and Exchange Commission (SEC), meanwhile, put out long-awaited proposals to require climate change disclosure in the annual reports and registration statements of public companies. The proposed rules are far more prescriptive in nature than the principles-based regulation the prior administration embraced, and would require integration with the company’s internal controls, audit and oversight functions.

The proposal points to increasing investor demand for disclosure on climate-related risks and the management of such risks. Many companies make these disclosures in their proxy statements, sustainability reports or on their websites, but the SEC has observed that these disclosures can vary widely in terms of completeness, granularity and format, and argues that third-party data providers and voluntary climate reporting frameworks have not met the need for climate risk-related disclosures.

The ESG movement in Latin America is evolving. According to a 2023 survey among more than 400 Latin American companies, a majority of issuers in each of Peru, Mexico, Costa Rica, Colombia and certain other countries consider themselves to have an ESG strategy, but only a minority of them prioritize climate change issues.

To better understand the landscape in environmental reporting for Latin American companies that are public in the US, in June 2023, White & Case conducted an in-depth review of environmental sustainability disclosures among 92 issuers headquartered in Latin America, who had already filed at least one annual report with the SEC.

The vast majority of the surveyed companies have standalone sustainability reports

Factors driving the pace of sustainability in Latin America

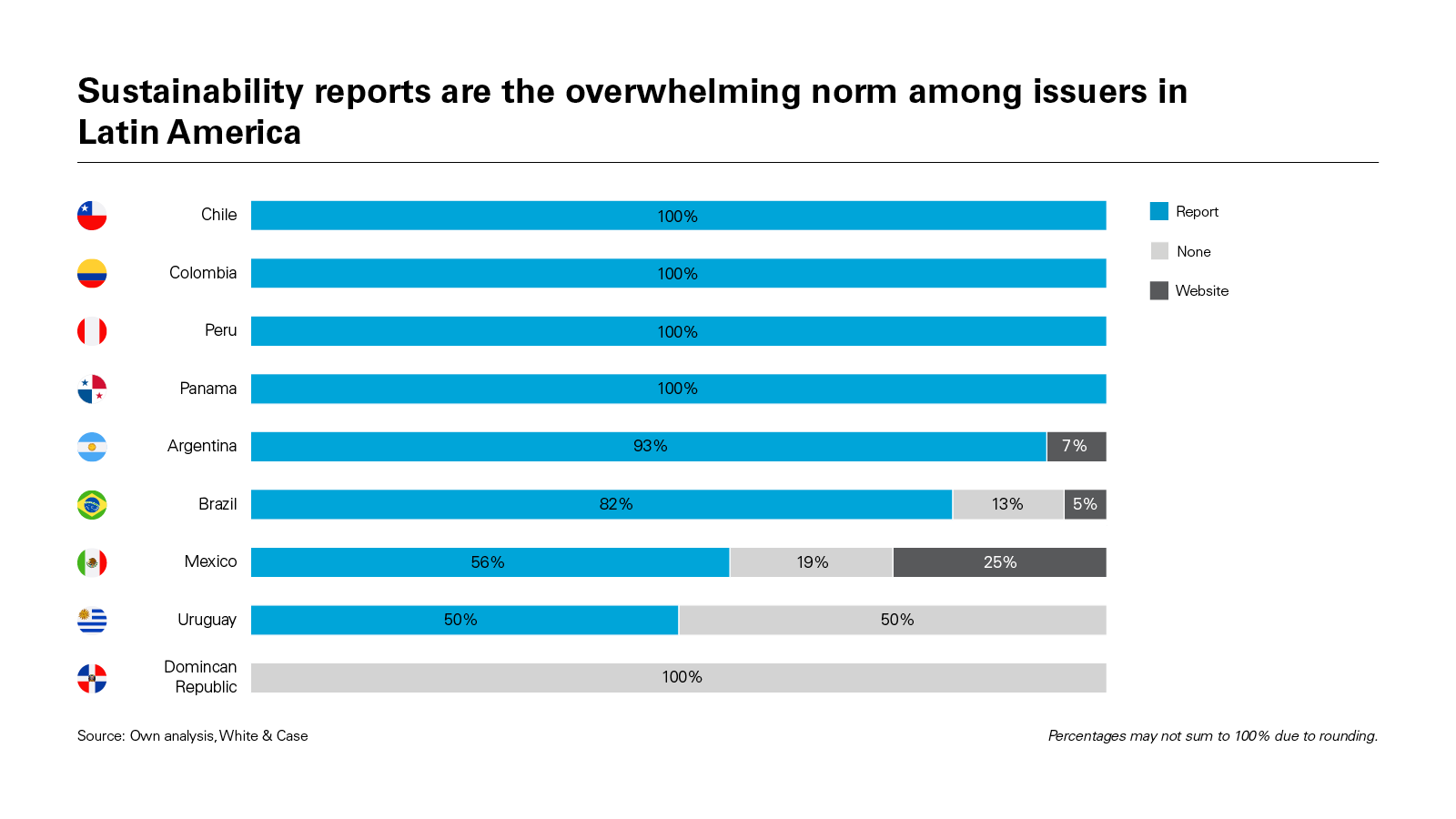

The vast majority (80%) of the surveyed companies already have standalone sustainability reports. Those without sustainability reports generally opt for no sustainability disclosure (12%), with only a small percentage (7%) creating more generic or brief sustainability websites.

Sustainability reports are the overwhelming norm among issuers from large Latin American countries (100% of Chilean, Colombian and Peruvian issuers, 93% of Argentine issuers and 82% of Brazilian issuers), except Mexico, where a narrow majority of issuers published sustainability reports (56%).

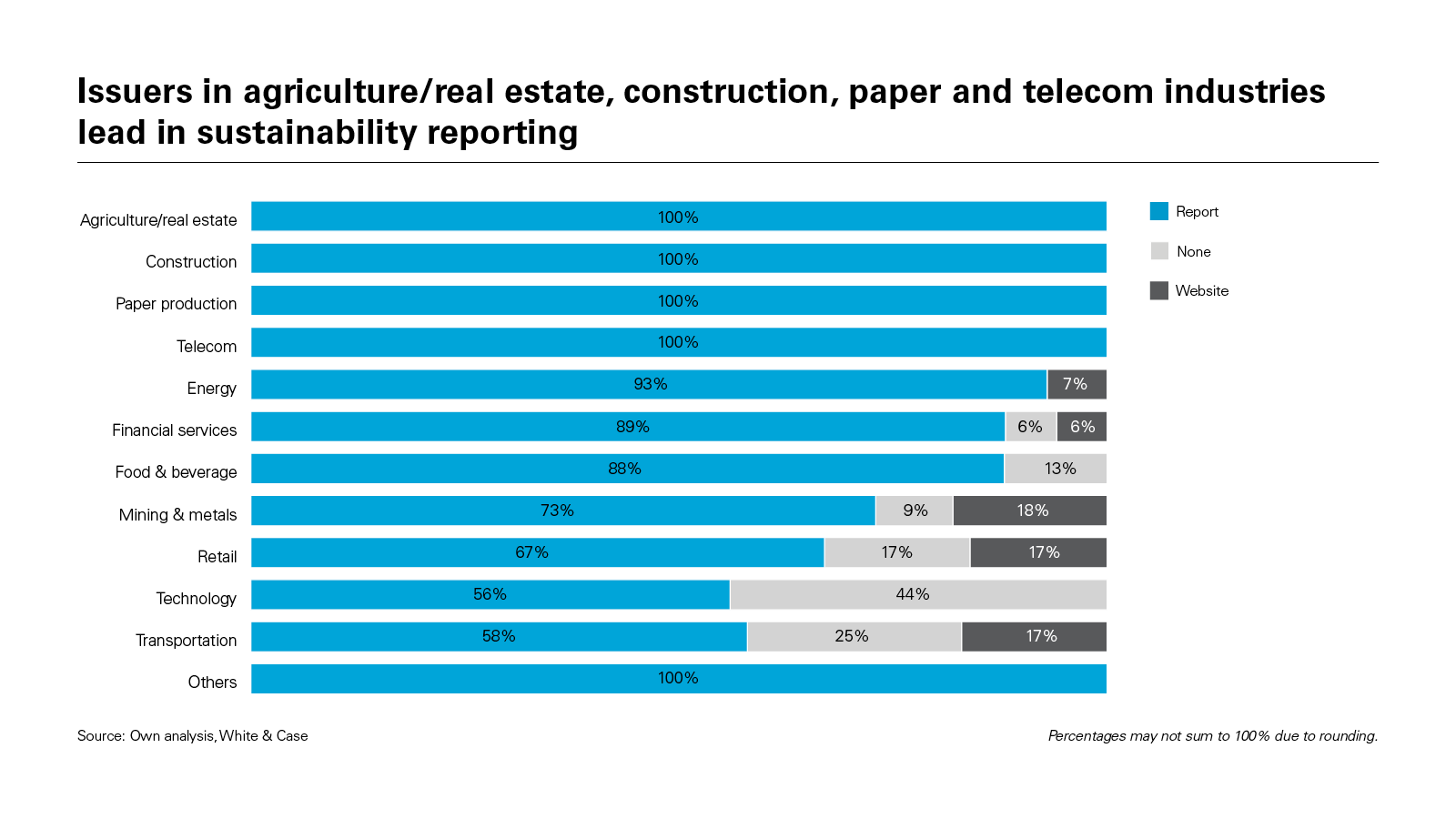

The industries with the greatest proportion of issuers publishing sustainability reports are agriculture/real estate, construction, paper production and telecom (100% each), followed by energy (93%), financial services and food and beverage (88% each), and lastly mining & metals (73%). The industries with the least sustainability reporting are retail (66% issuing a sustainability report) and, in last place, technology (55% issuing a sustainability report).

Risk factor disclosure

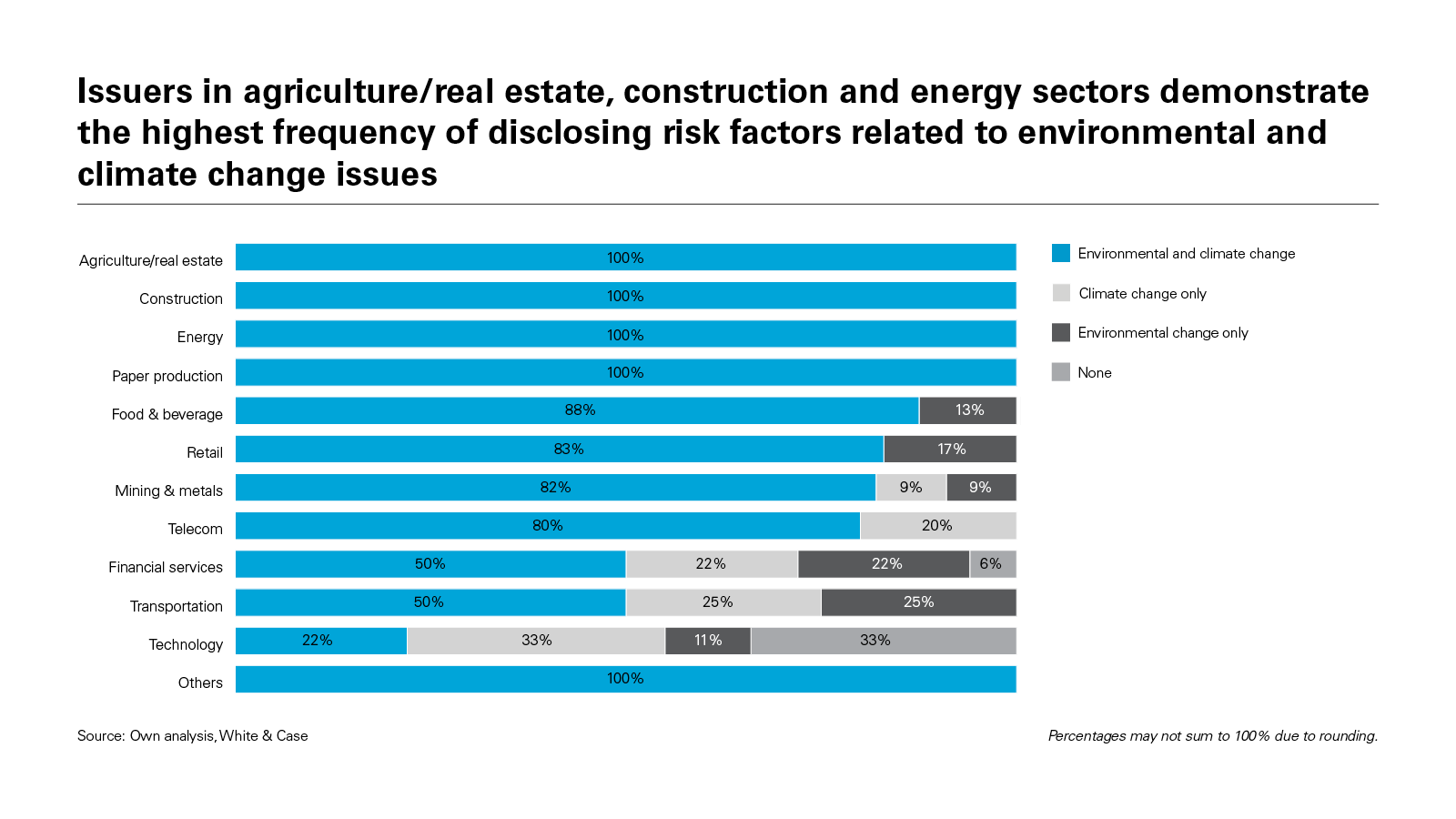

The surveyed companies tend to have robust risk factor disclosure, with a significant majority (80%), including environmental risk factors, and an even greater percentage (84%), including a climate change risk factor. The industries with issuers most frequently including risk factor disclosure are agriculture/real estate, construction and energy (100% for both general environmental and more specific climate change risk factors).

All other industries are very active in this space, with frequency of risk factor disclosure on environmental and climate change topics generally exceeding 70%, other than technology issuers, which disclose climate change risks a narrow majority of the time (55%), and environmental risks only in a minority of cases (33%).

Emissions reporting

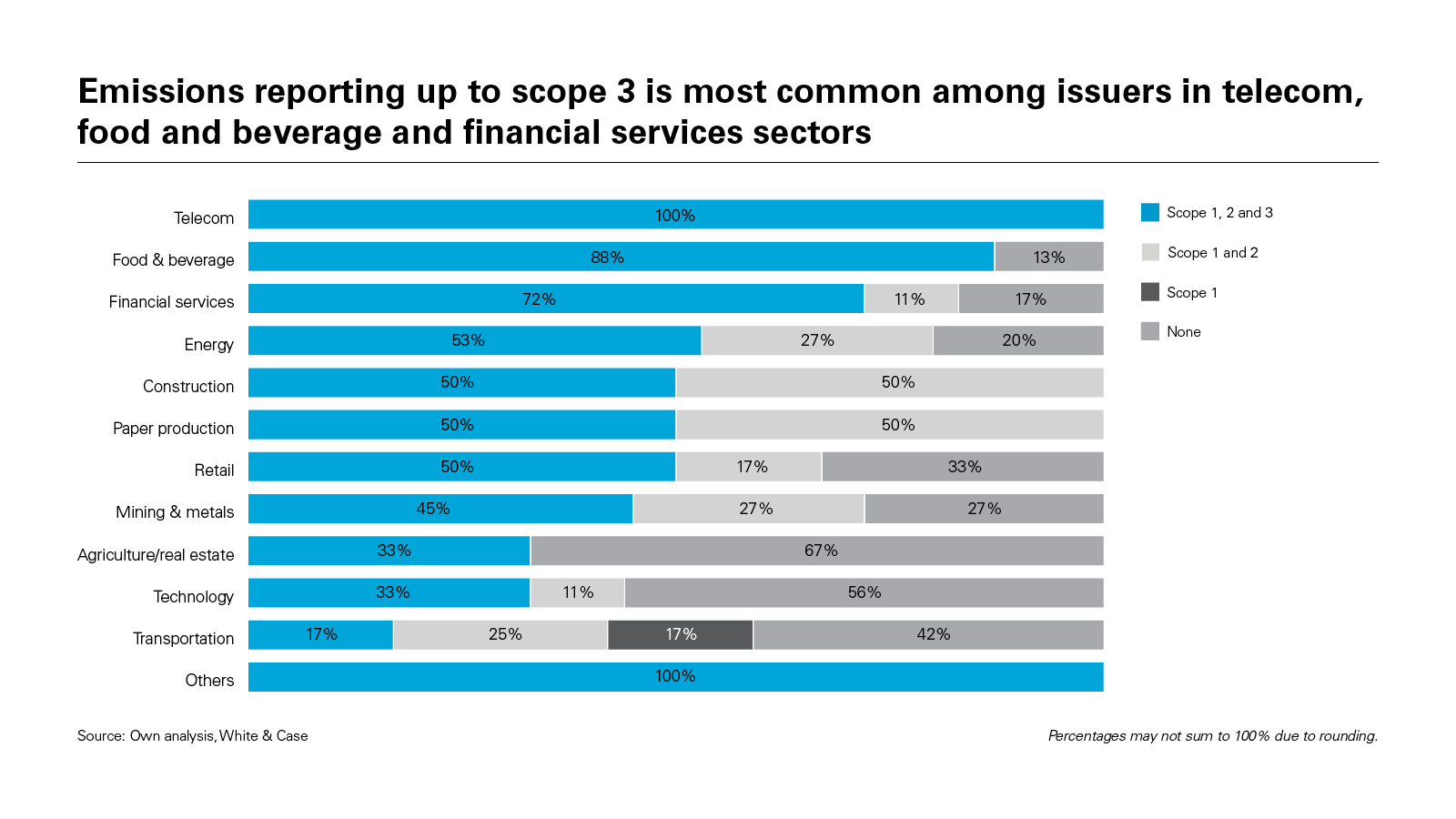

A significant majority of the surveyed companies report their emissions to some degree (74%), with the largest subset reporting their scope 1, 2 (direct) and scope 3 (indirect) emissions at least in part (54%). Just under a fifth (18%) of these issuers report only scope 1 and 2 emissions, whereas a negligible fraction of them (2%) limit their reporting to scope 1 emissions. The remainder (26%) opt for no emission disclosure.

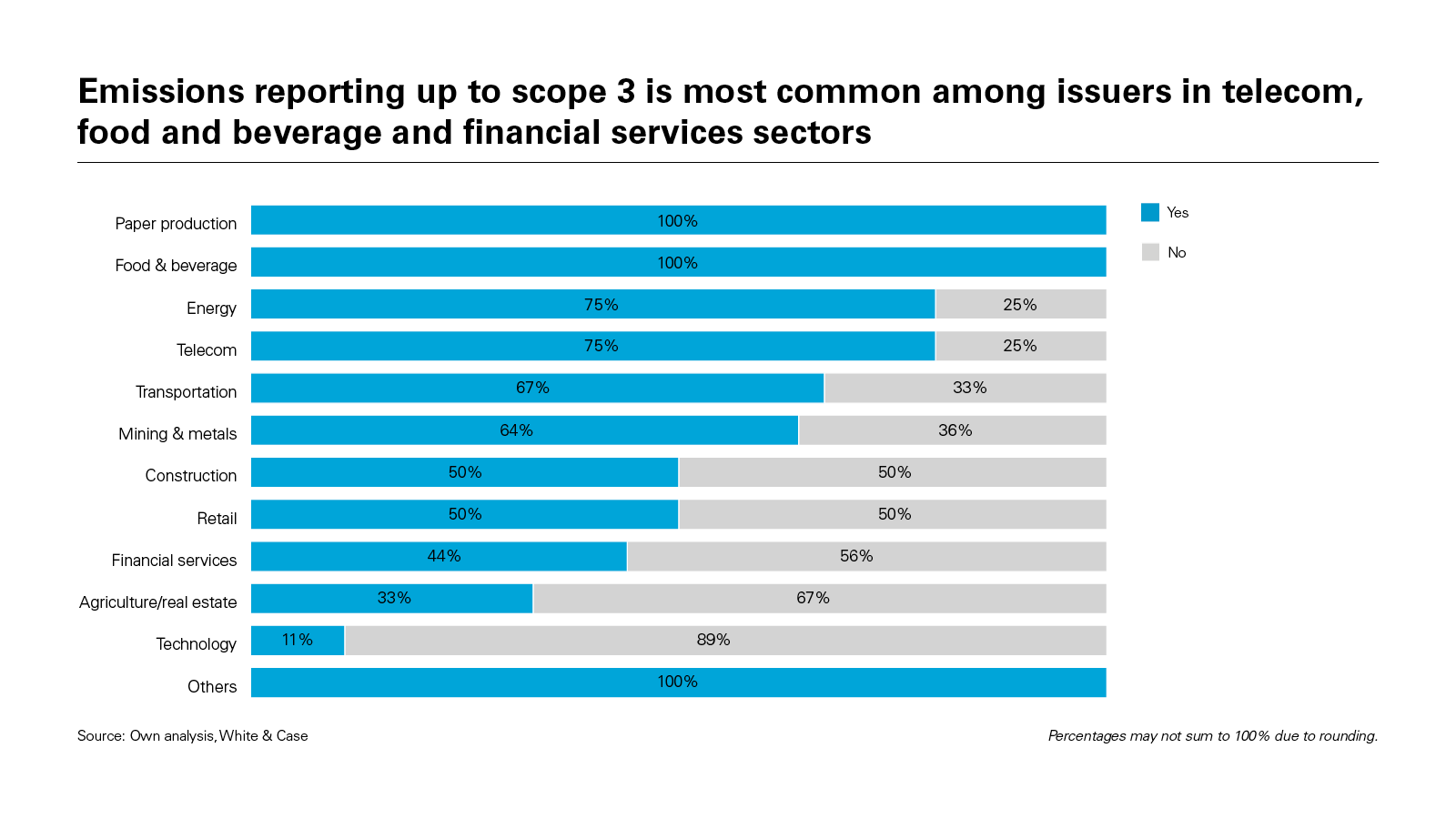

Emissions reporting up to scope 3 is most common among issuers in telecom (100%), food and beverage (87.5%) and financial services (72%). Otherwise, emissions reporting up to scope 2 is the highest in construction (100%), financial services (83%), energy (80%) and mining & metals (73%). The industries with the least emissions reporting are retail, transportation, technology and agriculture/real estate, with only 66%, 58%, 44% and 33%, respectively, reporting any type of emission.

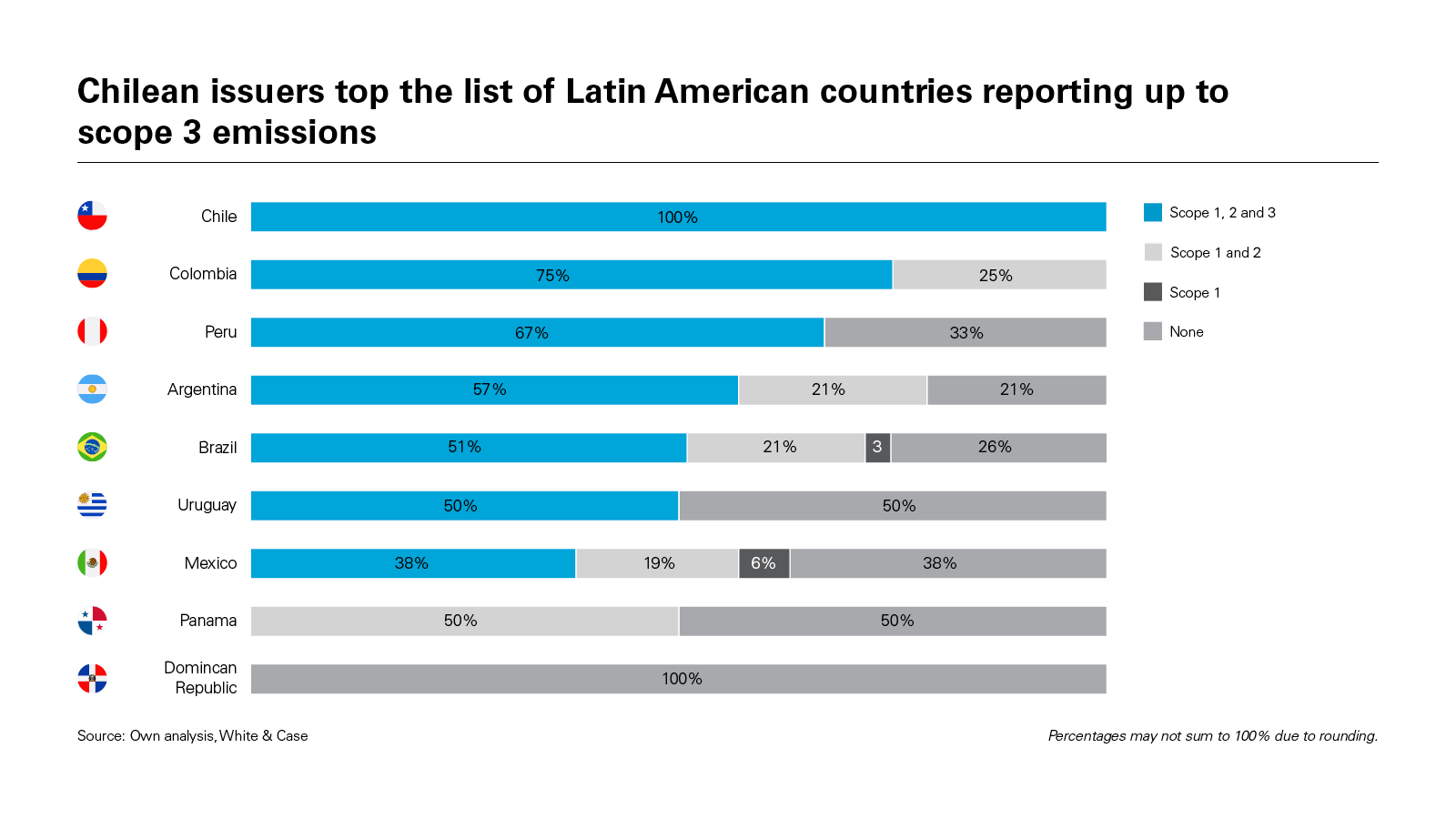

Chilean issuers top the list among those reporting up to scope 3 (100%), followed by Colombians (75%) and Peruvians (66%). However, among issuers reporting up to scope 2, issuers in Colombia and Peru are eclipsed by Argentina (78%), and Peruvian issuers are eclipsed by Brazilians (72%).

Among Latin America’s large countries, Mexico is generally on the lower end among issuers reporting up to scope 2 (56% of its issuers) or reporting any emissions at all (63% of its issuers). The countries with the lowest record of emissions reporting are Uruguay and Panama (each with only 50% of issuers) reporting any emissions at all. The Dominican Republic is in last place, with its sole issuer not reporting any emissions. In all cases, it should be noted that the reach of scope 3 emissions varies among issuers, who limit the activities associated with their business for which they report emissions in different ways.

Of surveyed companies have followed either GRI, SABS--or both--reporting standards

Emissions targets

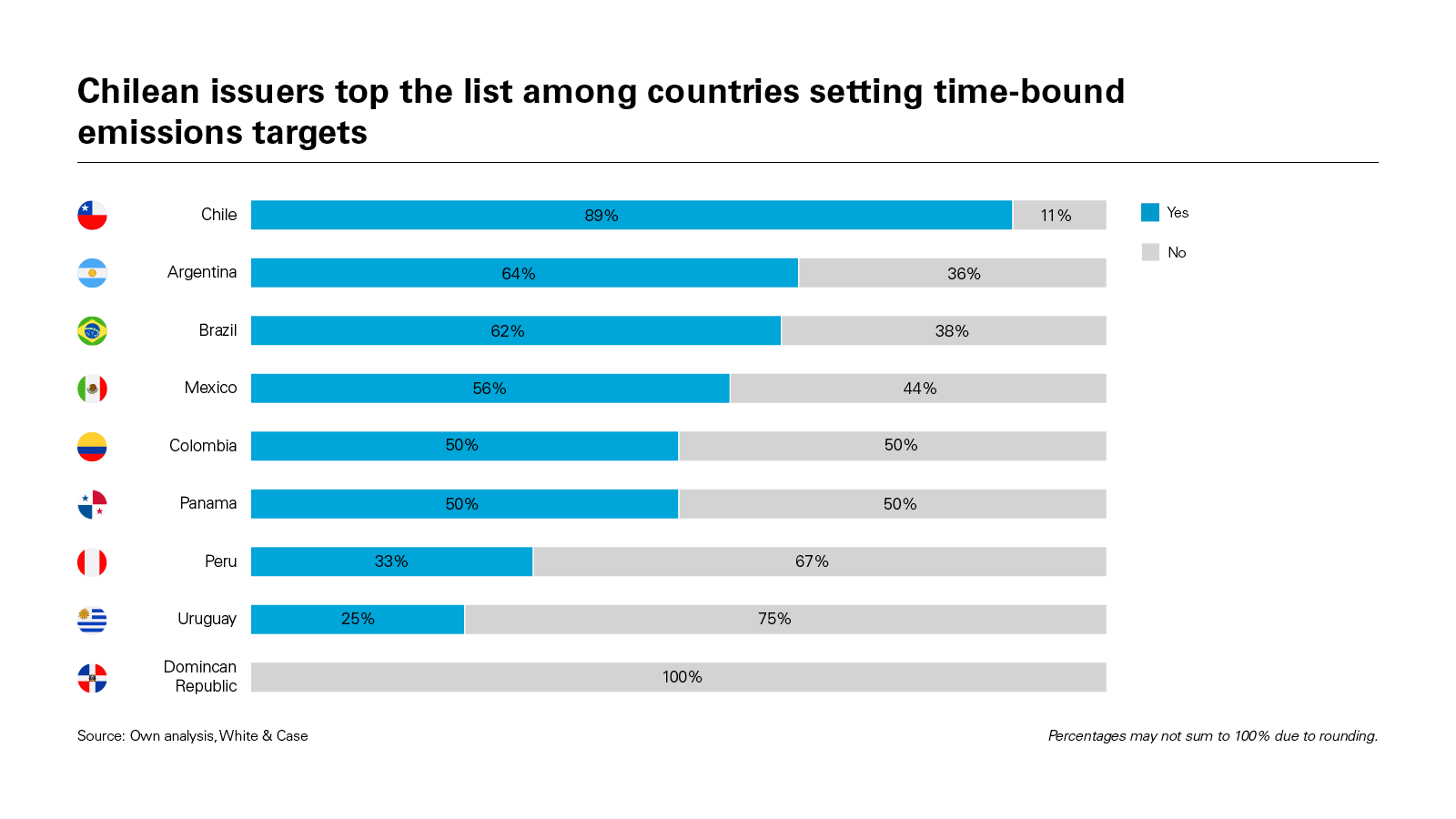

A relatively narrow majority (60%) of the surveyed companies sets some type of time-bound emissions target. The types of targets vary greatly, ranging from modest reductions in emissions with longer lead times, to carbon neutrality or net-zero emissions within various aspects of the business with time objectives anywhere from under ten years to more than 25 years. The industries with the greatest proportion of issuers setting time-bound targets are paper production (100%), followed by food and beverage (88%), and then energy and telecom (each 80%).

The industries with the lowest portion of surveyed Latin American issuers setting such targets are financial services (44%), agriculture/real estate (33%) and technology (11%).

In line with their high standards of emissions reporting, Chilean issuers top the list among those setting time-bound emissions targets (89%), followed, with a noticeable difference, by Argentine issuers (64%) and Brazilian issuers (62%).

Despite having higher standards of emission reporting, Colombian and Peruvian issuers tend not to set time-bound emissions targets, with 50% and 33%, respectively, establishing such goals. Consistent with their lower standards of emissions reporting, issuers from Panama, Uruguay and the Dominican Republic also have lower rates of setting of emissions targets, with 50%, 25% and no issuers, respectively, setting such targets. Mexican issuers set time- bound emissions targets proportional to their rate of emissions reporting up to scope 2 (56%).

Environmental sustainability reporting standard

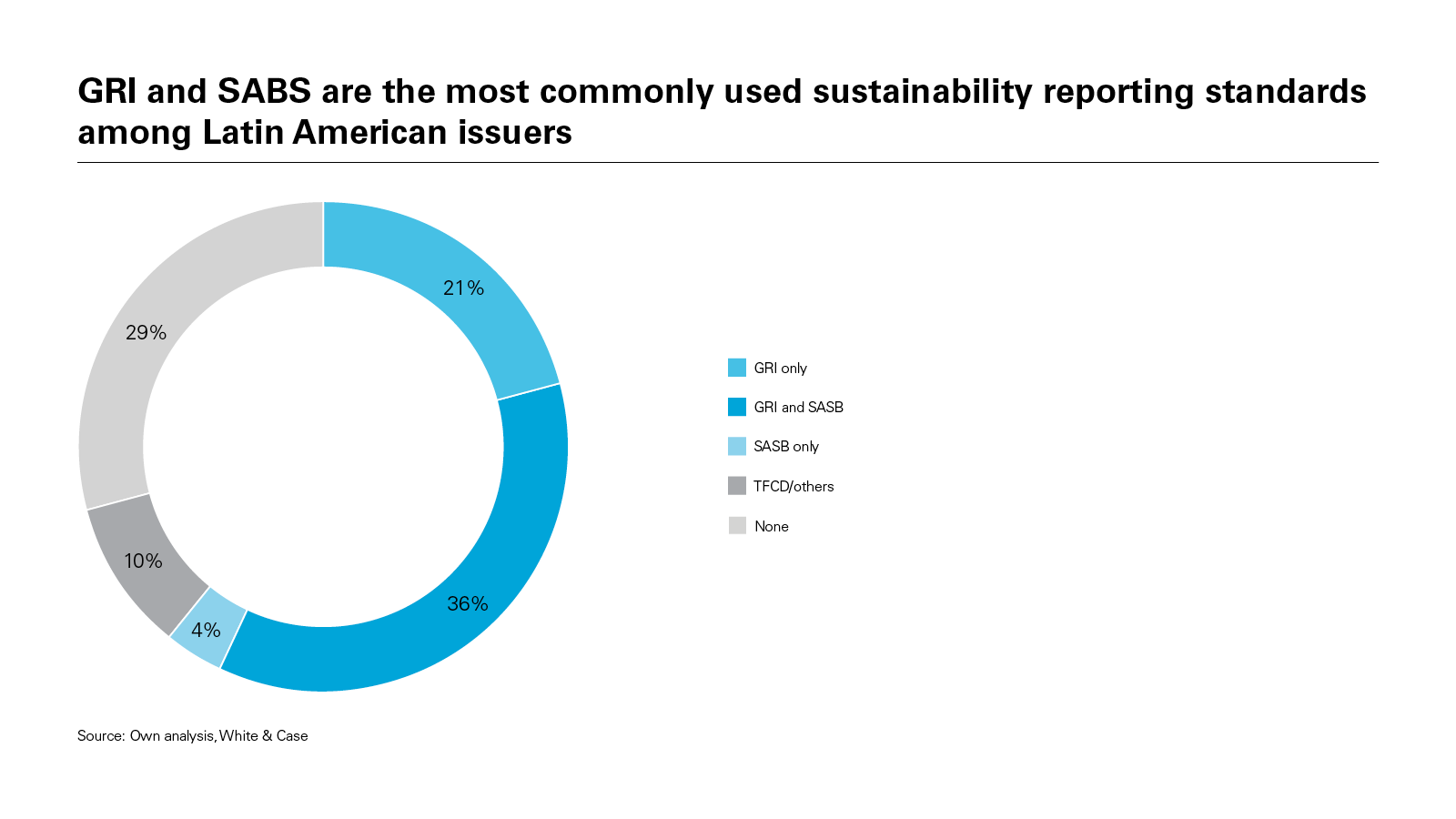

Among Latin American issuers providing sustainability reporting, the most commonly used sustainability reporting standards are the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB). The standards created by the Task Force on Climate Disclosure (TFCD) are used by a small minority of issuers. The remainder of surveyed Latin American companies, to the extent they use any standard at all, report under a wide umbrella of frameworks, including the International Integrated Reporting Council, the Stakeholder Capital Metrics of the World Economic Forum, the Brazilian GHG Protocol Program, the United Nations Global Compact and Ipieca. Several of the surveyed issuers reported fewer than one standard.

Global Reporting Initiative (GRI) and Sustainability Accounting Standards Board (SABS) are the most commonly used sustainability reporting standards among Latin American issuers

Engagement with local and indigenous communities

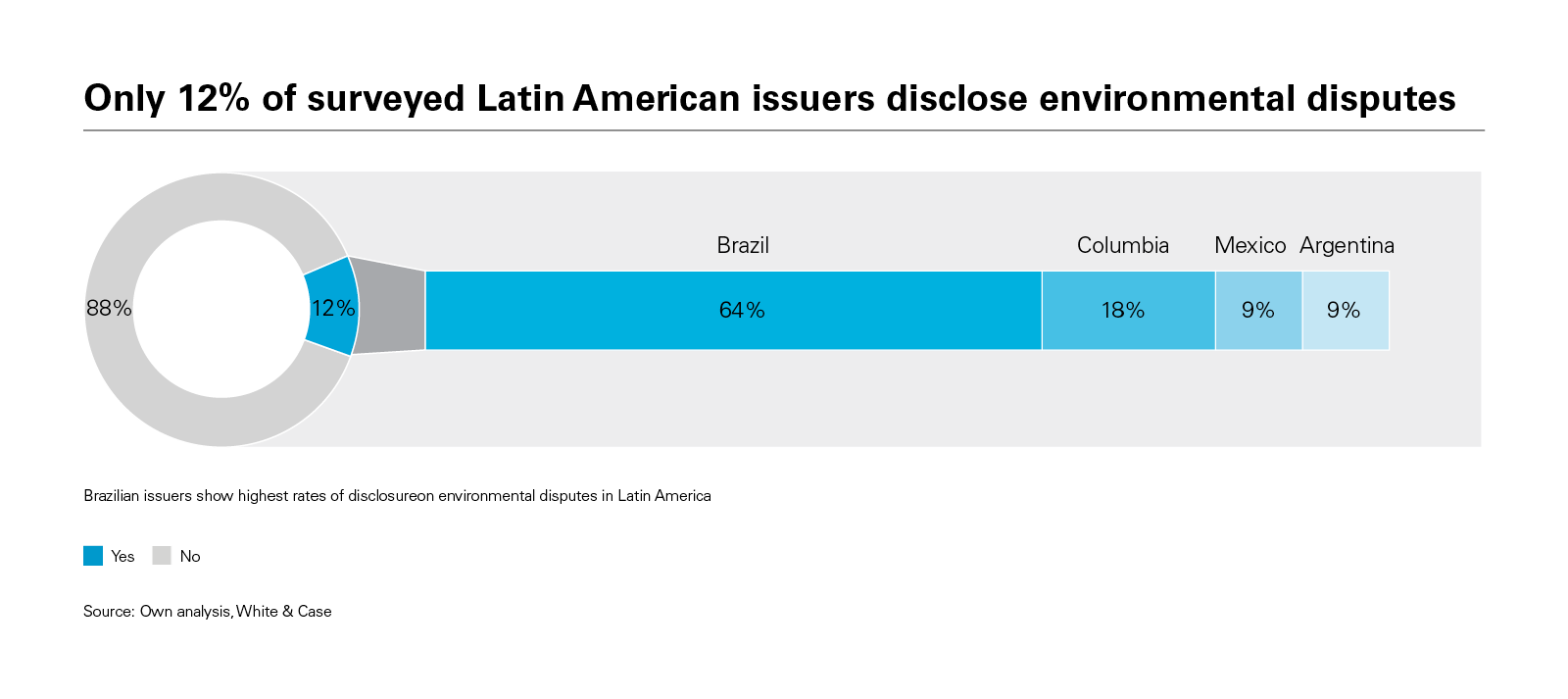

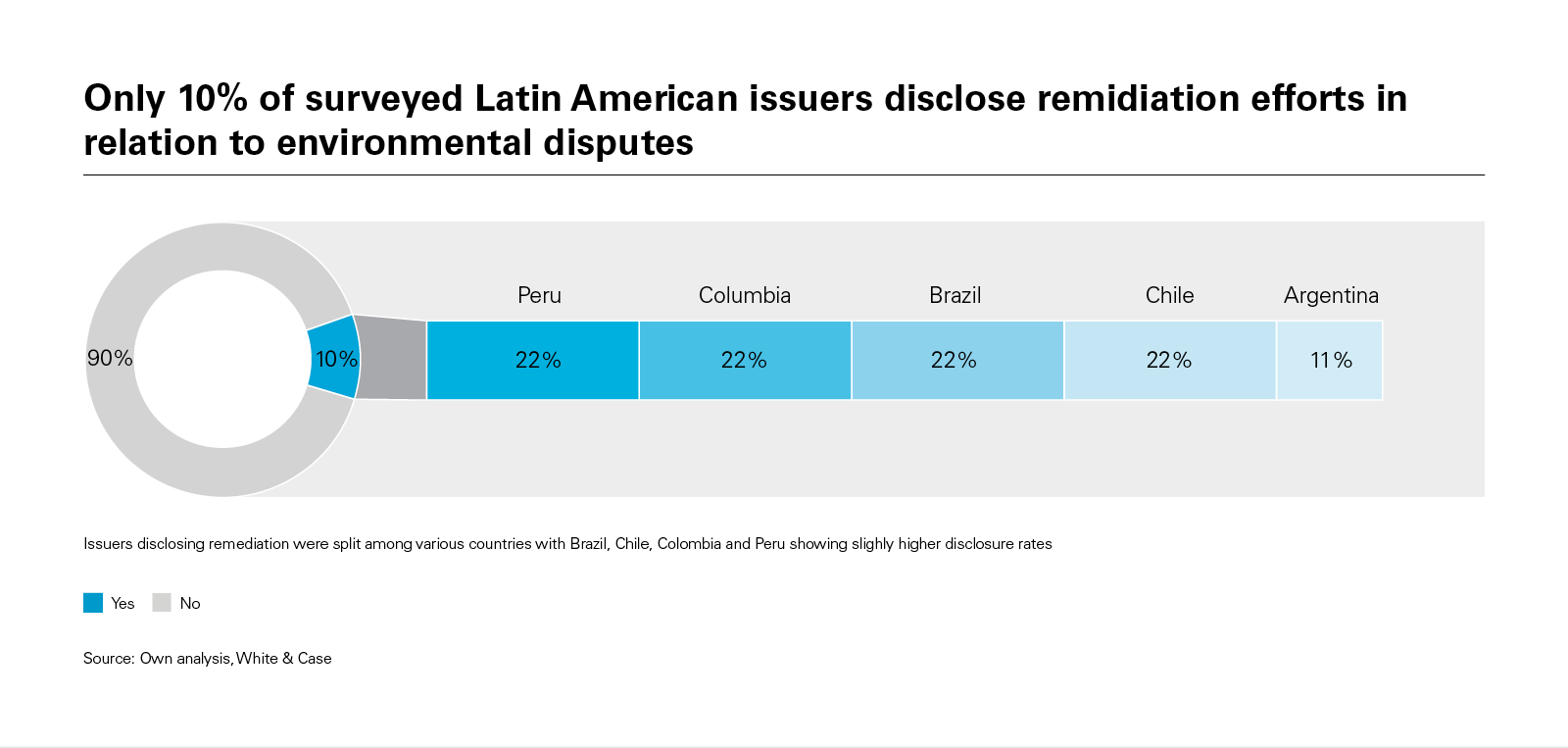

Despite the prominence of environmental disputes with indigenous communities among Latin American companies, few seemed to consider this a material subject for investors. A very small minority (12%) of companies had any type of disclosure on environmental disputes, with even fewer (10%) disclosing remediation efforts in regard to environmental disputes.

Within this small group of companies, most of those disclosing a dispute were Brazilian (64%), whereas the companies disclosing remediation were split among various countries, with 22% in each of Brazil, Chile, Colombia and Peru, and the remaining 11% in Argentina.

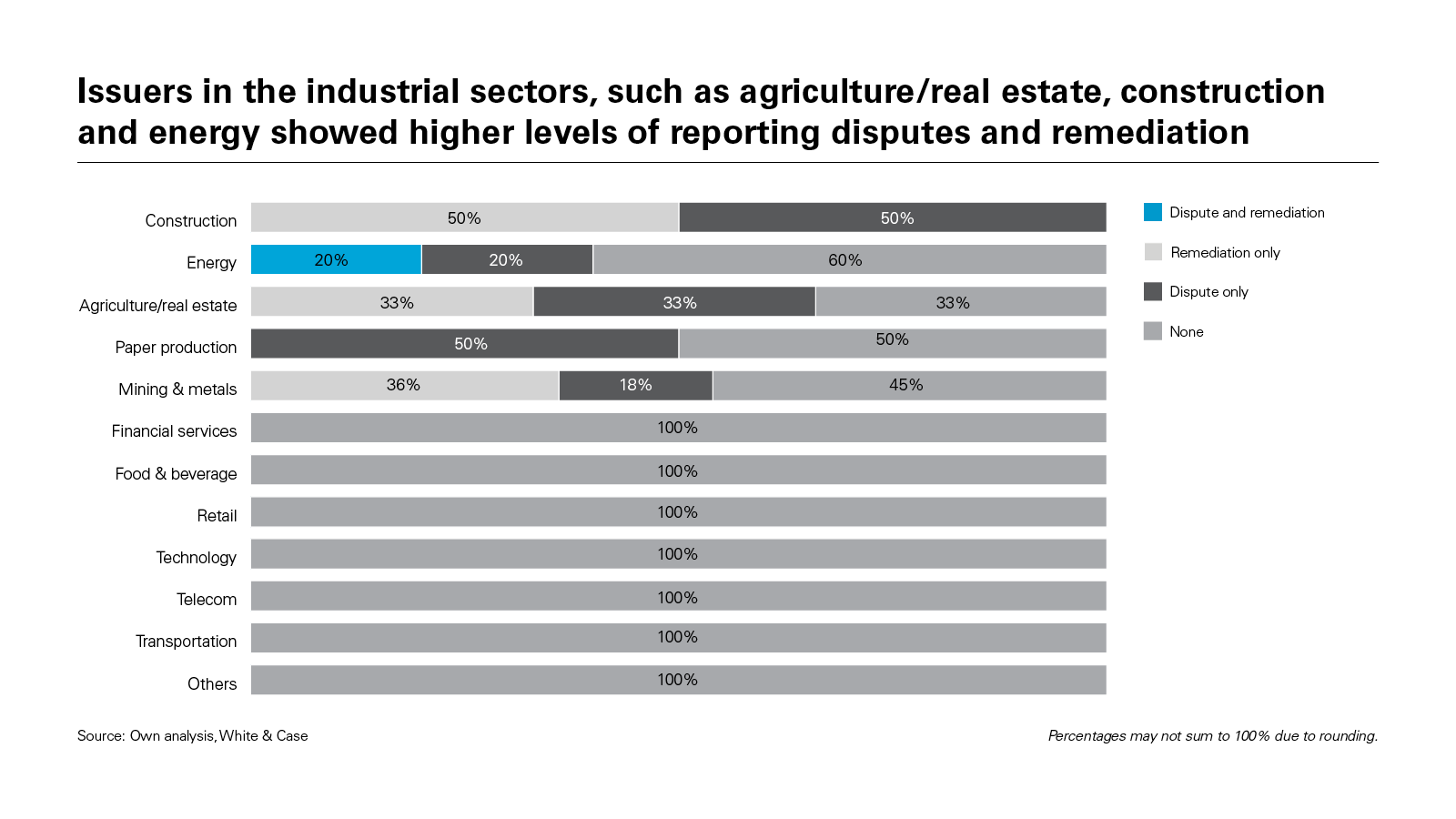

Disclosures were higher in more industrial sectors, such as construction (50% of issuers reporting a dispute and/ or remediation), energy (40% of issuers reporting a dispute and 33% reporting remediation), agriculture (30% of issuers reporting a dispute and/or remediation), paper production (50% of issuers reporting a dispute but none reporting remediation), and mining & metals (18% of issuers reporting a dispute and 36% of issuers reporting remediation).

The survey underscores a compelling opportunity for Latin American issuers to enhance the depth and thoroughness of their reporting. Companies that are more consistent and transparent in their sustainability disclosures are poised to stand out as more appealing investment options in the evolving landscape of sustainable finance. As ESG factors continue to hold a prominent place on the agenda of investors worldwide, embracing a more comprehensive approach to sustainability reporting not only aligns with responsible business practices but also positions these companies for greater investor trust and engagement in the future.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Sustainability reports are the overwhelming norm among issuers in Latin America Source (PDF)

View full image: Sustainability reports are the overwhelming norm among issuers in Latin America Source (PDF)

View full image: Issuers in agriculture/real estate, construction, paper and telecom industries lead in sustainability rep (PDF)

View full image: Issuers in agriculture/real estate, construction, paper and telecom industries lead in sustainability rep (PDF)

View full image: Issuers in agriculture/real estate, construction and energy sectors (PDF)

View full image: Issuers in agriculture/real estate, construction and energy sectors (PDF)

View full image: Emissions reporting up to scope 3 is most common among issuers in telecom, food and beverage (PDF)

View full image: Emissions reporting up to scope 3 is most common among issuers in telecom, food and beverage (PDF)

View full image: Chilean issuers top the list of Latin American countries reporting up to scope 3 emissions (PDF)

View full image: Chilean issuers top the list of Latin American countries reporting up to scope 3 emissions (PDF)

View full image: Emissions reporting up to scope 3 is most common among issuers in telecom, food and beverage (PDF)

View full image: Emissions reporting up to scope 3 is most common among issuers in telecom, food and beverage (PDF)

View full image: Chilean issuers top the list among countries setting time-bound emissions targets (PDF)

View full image: Chilean issuers top the list among countries setting time-bound emissions targets (PDF)

View full image: GRI and SABS are the most commonly used sustainability reporting standards among Latin American issuers (PDF)

View full image: GRI and SABS are the most commonly used sustainability reporting standards among Latin American issuers (PDF)

View full image: Only 12% of surveyed Latin American issuers disclose environmental disputes (PDF)

View full image: Only 12% of surveyed Latin American issuers disclose environmental disputes (PDF)

View full image: Only 10% of surveyed Latin American issuers disclose remidiation efforts (PDF)

View full image: Only 10% of surveyed Latin American issuers disclose remidiation efforts (PDF)

View full image: Issuers in the industrial sectors, such as agriculture/real estate, construction and energy (PDF)

View full image: Issuers in the industrial sectors, such as agriculture/real estate, construction and energy (PDF)