As we embark on our third year of Latin America Focus, the ever-evolving landscape in the region brings fresh opportunities and challenges for local, regional and international businesses.

After an extremely positive post-Covid growth spurt in 2022, so far 2023 has been a bit more challenging for the region with GDP growth slowing and political uncertainty increasing. Nevertheless, we see plenty of bright spots on the horizon and opportunities for those who know where to find them.

In our third compendium of market insight from the Latin America team at White & Case, we look at what those opportunities are and where challenges might arise for investors.

On the opportunity front, we examine the mining & metals industry in detail. Interest in the region's lithium reserves has soared with the continued growing demand for the mineral for the battery manufacturing process. The "lithium triangle" has turned into a "lithium quad" with Brazil joining Chile, Argentina and Bolivia as a significant supplier of lithium. However, the countries' differing approaches to regulation of the industry means that those looking to source lithium in the region will have to understand the market in each country to determine where, when and how to make significant investments.

The lithium market could potentially be the beneficiary of another Latin American trend: Nearshoring. In a world of escalating geopolitical volatility, there is a shift away from broader globalization towards a more localized approach to manufacturing and trade. Several countries in Latin America have implemented investment and tax treaties, which, along with the ongoing geopolitical shift, make the establishment of industrial plants in the region easier and more enticing than ever before.

In this issue, we also take a look at environmental, social and governance (ESG) considerations; compared to their counterparts in North America or Europe, Latin American companies have arguably been slower to respond to the trend to disclose their approach to ESG. However, within the region this varies widely depending on the industry, as our recent survey of private issuers has shown.

As ever in our volatile world, the threat of market shocks and their impact on businesses and industries remains constant. Three major Latin American airlines and a variety of other businesses recently went through lengthy and difficult insolvency procedures following the Covid crisis. The good news is that most of these businesses are now back on track and performing very well, thanks in part to the creative and unprecedented use of Chapter 11 of the US Bankruptcy Code as well as local insolvency regimes to restructure the debt and the capital structures of the effected companies.

Another bright spot for investors in Latin America in recent years is that international arbitration in the region continues to develop in remarkable fashion, providing foreign investors with recourse to fair and impartial justice when investment disputes arise.

We at White & Case continue to believe that the Latin American market holds long-term promise for the savvy investor. We hope that you find this issue of Latin America Focus, which contains articles from our top experts on the subjects referenced above, interesting and useful as you embark on additional business in the region.

Sustainability disclosures gain momentum among Latin American issuers

Foreign direct investment soared 20-fold between 1980 and 2020, according to World Bank

Nearshoring is the buzzword of the moment, and one of the most popular destinations for US investors is Latin America

Nearshoring is the buzzword of the moment, and one of the most popular destinations for US investors is Latin America—with good reason.

The data suggest that this is not merely a trend derived from the recent political and health events, but rather a structural shift. There are signs that show that the investment that nearshoring has brought to Latin America so far is just the beginning, and that it will increase substantially in the future.

The once unquestioned wave of post-World War II globalization has faced profound scrutiny in recent years, driven by both political and practical concerns.

As the White & Case report "A world of clubs and fences: Changing regulation and the remaking of globalization" highlights, cross-border flows have increased markedly since the 1980s. According to World Bank, foreign direct investment soared 20-fold between 1980 and 2020, global trade rose from 35 percent of world GDP to 58 percent and average global real income grew by 120 percent. But new pressures have since arisen, ranging from unease about the social consequences of open borders, to the way governments are responding to national and international security threats.

One response is to reconsider the commitment to open economies, and this has been exacerbated by systemic shocks, including the COVID-19 pandemic and Russia’s invasion of Ukraine.

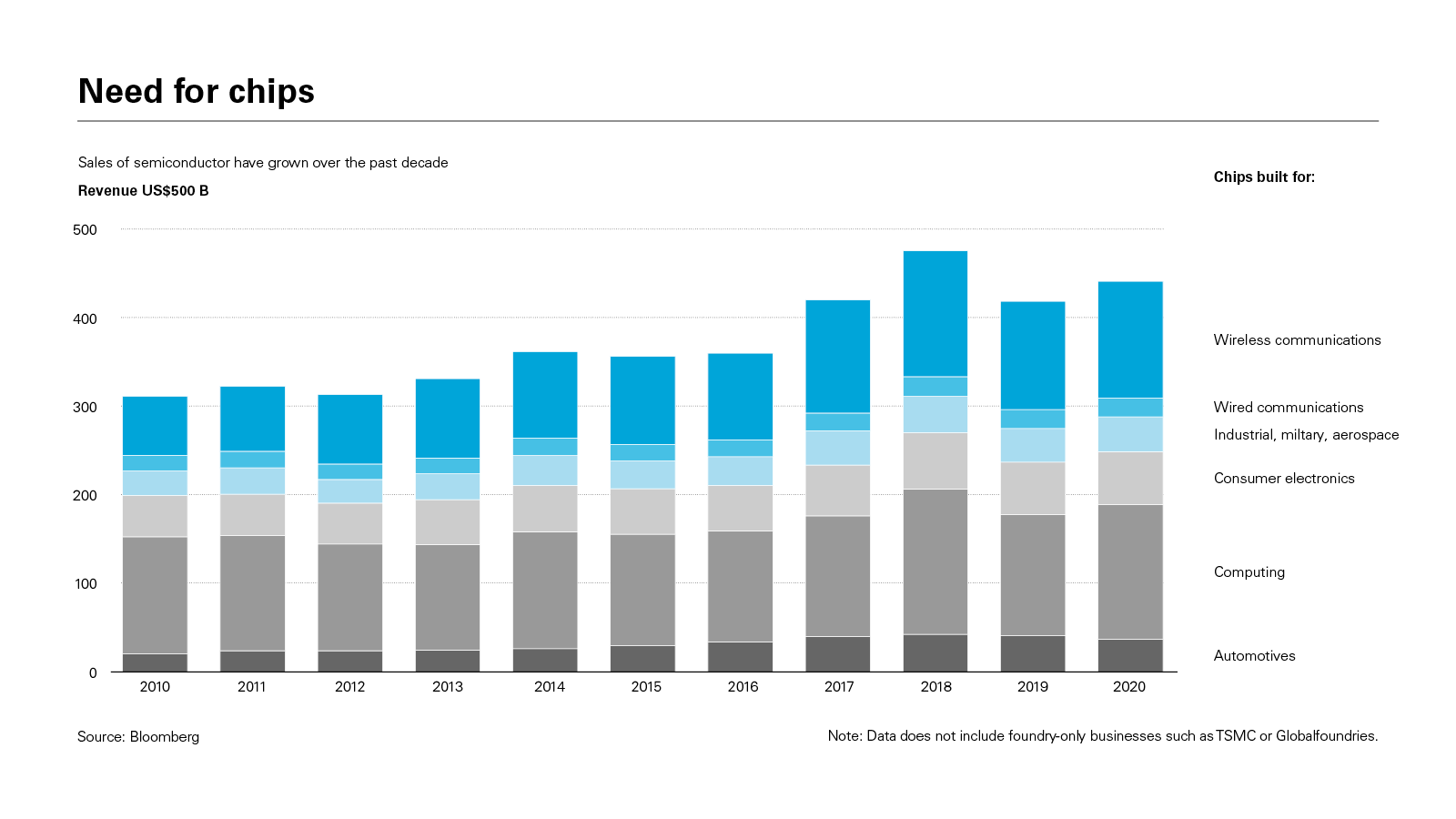

Global production and trade were disrupted due to the pandemic and the restrictions in the flow of people and goods, coupled with changing demands, resulted in shortages throughout the world. A good example was the shortage of electronic chips, caused by a bottleneck of production resulting from the increase in demand for smartphones and computers amid the pandemic.

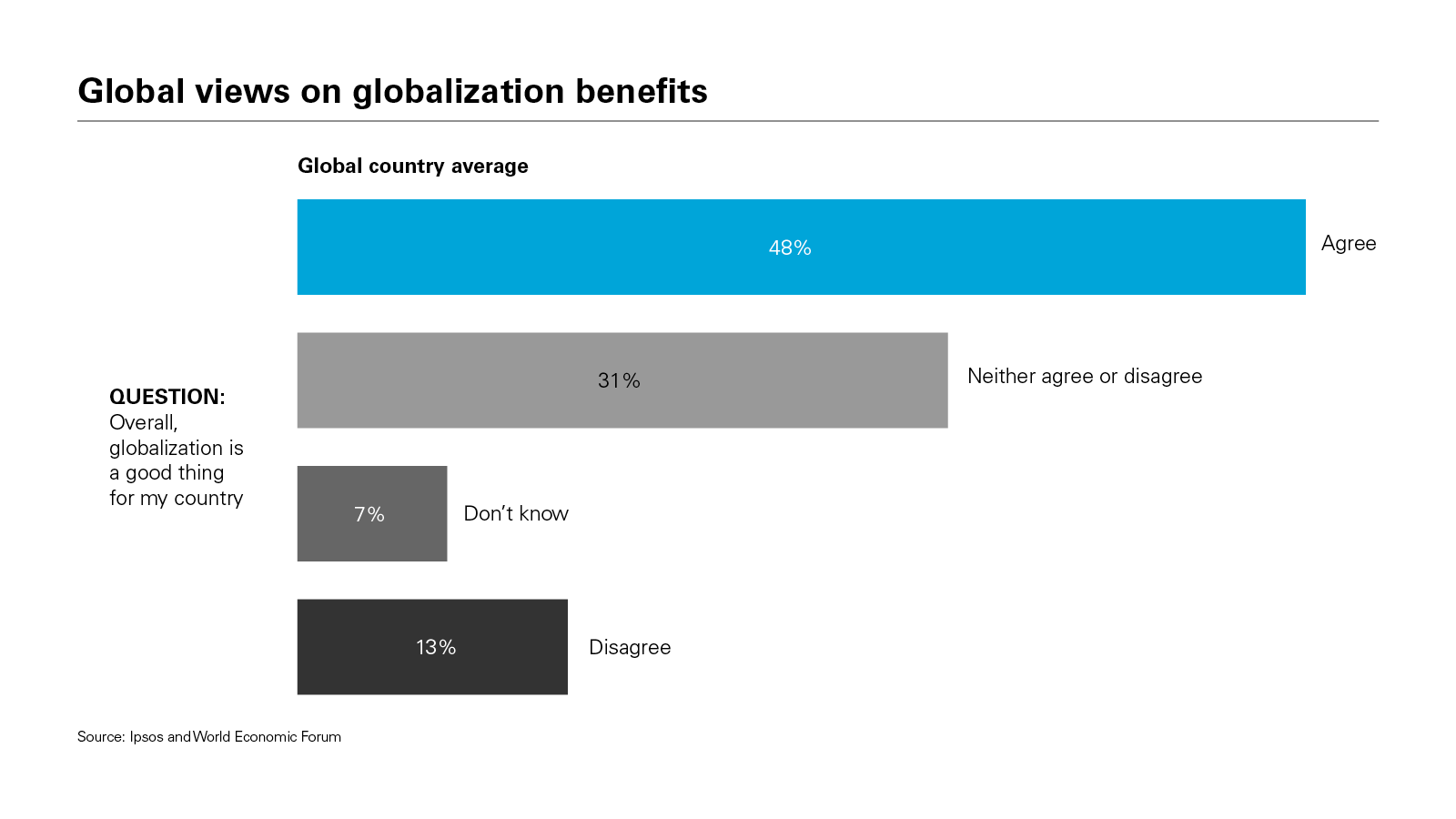

A 2021 survey by Ipsos and the World Economic Forum showed the positive sentiment toward globalization decreased substantially from pre-pandemic levels. It currently ranges from 72 percent in Malaysia to 27 percent in France.

An alternative to our current globalization model is the integration of production lines, value chains and sourcing from countries close to large consumption markets. There is also a trend known as "friend-shoring" characterized as increasing trade among countries with similar political values.

Is this real?

So far, the nearshoring trend has seemingly resulted in higher foreign direct investment in the Latin American region. For example, Mexico reported a 12 percent increase in FDI for 2022, and the highest investment figure of the past seven years.

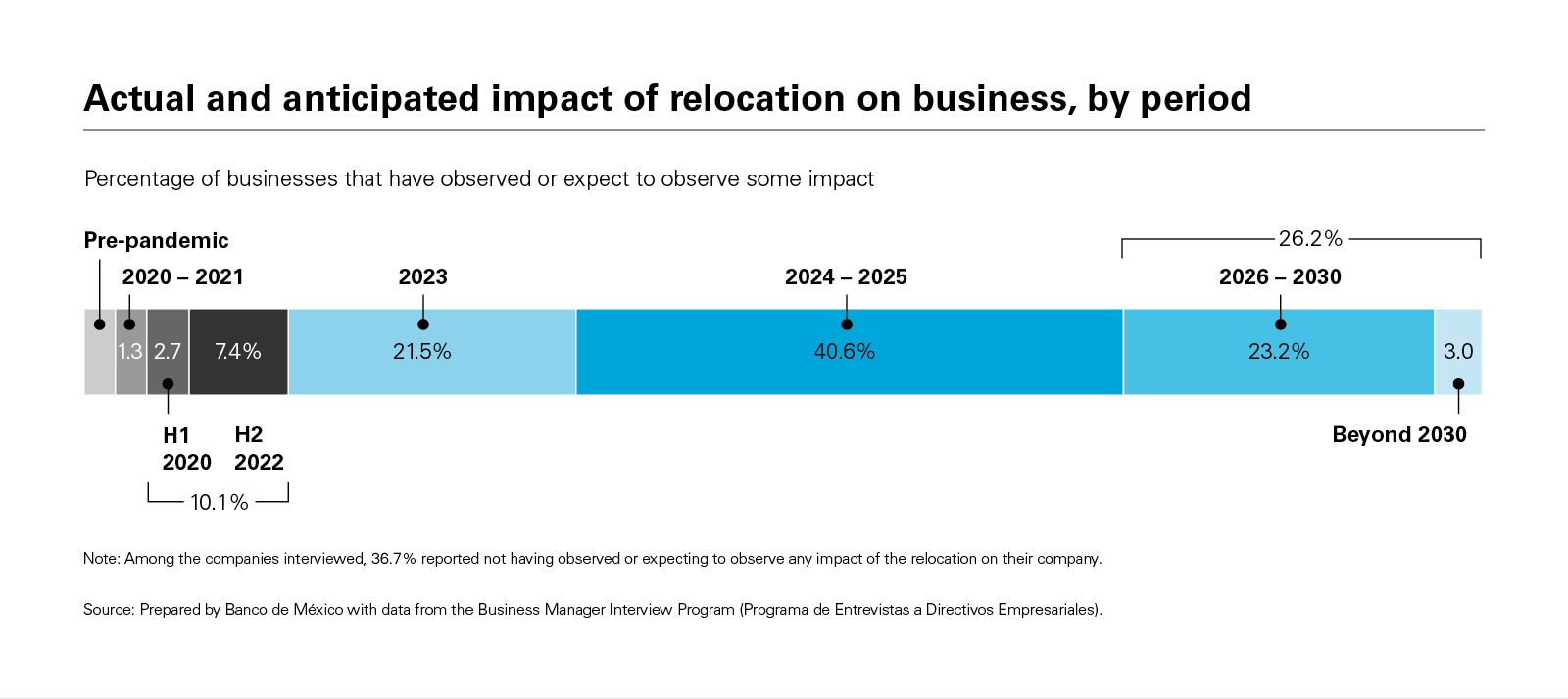

This has resulted in higher demand for industrial space in the region. The Mexican Central Bank reports that the view among large corporations is that the greater impact of nearshoring is yet to be seen. Most industrial companies expect the increase in demand to be reflected between 2024 and 2025, and a large number of survey participants expected the benefits to be observed after 2026.

This seems to make sense: The relocation of industrial production lines takes time. Infrastructure needs to be developed and plants need to be built, permits acquired, workers retained, companies incorporated and so on, before commencing production.

The US has free trade agreements with 12 countries in Latin America

Relocating smartly: Investment protections

Proximity to a large consumptions market, such as the US and the North American region as a whole, is not enough for Latin American countries to take advantage of the relocation opportunities that may arise in the future. Rule of law, investment protections and tax matters are very relevant to any relocation decisions.

The US has free trade agreements with 12 countries in the region: Chile, Colombia, Costa Rica, Dominican

Republic, El Salvador, Guatemala, Honduras, Mexico, Nicaragua, Panama and Peru, as well as Canada. It also has trade and investment framework agreements or trade and investment council agreements with Argentina, Brazil, the Caribbean Community, Ecuador, Uruguay and Paraguay.

The European Union currently has five free trade agreements with 11 Latin American countries, and an economic partnership agreement with 14 Caribbean states, known as CARIFORUM.

Trade agreements in general provide investment protection and certainty for investors as they relocate into the region. Another important aspect of the investor protections is concerning intellectual property. The host countries should be able to provide the necessary assurances to foreign investors that their valuable IP will be protected while it is being used in each country.

These agreements go well beyond World Trade Organization investment provisions, and may include access directly or through separate instruments, to investor-state arbitration, which is probably a last resort mechanism to recover damages caused by state entities against foreign investments in their territories. Mexico, for example, has 14 free trade agreements with 52 countries and 30 bilateral investment treaties.

A clear understanding on tax implications of the relocation is also very relevant. The tax treaty network in Latin America plays a key role in preventing double taxation. For instance, Mexico has 61 tax treaties, covering most of the largest economies in the world.

Transfer pricing rules are essential to offer certainty in the proper allocation of profits. The Latin American region, and particularly Mexico, has significant experience of dealing with rules in full alignment with Organization for Economic Cooperation and Development transfer pricing guidelines that were adopted since the 1990s, as well as all its amendments and improvements made from time to time. In Mexico, the legal framework provides the opportunity for taxpayers to file for unilateral advance pricing agreements or bilateral with other jurisdictions, for instance, with the US or any other jurisdiction with a double tax treaty with Mexico.

The maquila regime in Mexico has resulted in the development of a large manufacturing base, especially close to the border with the US, with foreign trade programs that allow exporters to import free of tax and duties of goods for subsequent export.

Some countries in Latin America have begun setting up incentives for plants and investors that relocate in certain regions. Mexico launched a tax incentive program to attract investment for the zone of Itsmo de Tehuantepec, including corporate income tax exemptions for the first three years of operations, followed by the reduction of 50 percent, and up to 90 percent of income tax payments, in a second phase of three years, plus additional benefits regarding indirect taxes.

These incentives, coupled with the expanding suite of treaties, make Latin America an attractive proposition for companies wishing to nearshore operations in the region. The global political situation looks likely to remain uncertain for some years yet, and a more localized approach to business could well be the more prudent approach in the future.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Need for chips (PDF)

View full image: Need for chips (PDF)

View full image: Global views on globalization benefits (PDF)

View full image: Global views on globalization benefits (PDF)

View full image: Actual and anticipated impact of relocation on business, by period (PDF)

View full image: Actual and anticipated impact of relocation on business, by period (PDF)