Embracing change

The convergence of artificial intelligence (AI) and life sciences is no longer a distant promise. Companies operating in the sector are actively embracing the technology and are already achieving measurable results. In the following exclusive report from White & Case, in association with Mergermarket, this new reality is explored in depth. Drawing on a proprietary survey of senior executives spanning human pharma and biotech, healthcare provision, medical devices and animal health, the report provides a comprehensive overview of where the sector stands and where it may be heading.

Recent market data demonstrates the scale and urgency of this shift. AI in the pharma market alone is projected to reach US$25.7 billion by 2030, up from around US$4 billion today, according to market research firm Mordor Intelligence. AI-driven drug discovery is also expected to exceed US$20 billion by 2030, per research organization Grand View Research, as firms seek faster routes to novel compounds and more precise trial matching. These forecasts underscore that AI is much more than merely a back-office optimization tool; it is becoming integral to how life sciences companies design, test and deliver therapies, with growing expectations from regulators, investors and patients alike.

Our findings confirm this transition of AI from experimentation to practical application. Tools are being embedded in product design, trial optimization, diagnostics, drug target identification and commercial execution. Organizations are also adapting internally—reassessing governance structures, workforce capabilities and legal frameworks to ensure AI can scale sustainably and in compliance with complex legal frameworks. Board-level involvement is growing, and forward-looking investment strategies are being developed to match the pace of innovation.

This research explores the sector's priorities and pain points in detail. The report begins by mapping current use cases and business goals, showing how companies are deploying AI to address real operational needs—from shortening development cycles to improving diagnostic accuracy. It then turns to the structural challenges that remain, including the legal and regulatory complexities surrounding general AI deployment and use, data protection, intellectual property (IP) and cross-border compliance. These risks are shaping how organizations approach partnerships, procurement and policymaking.

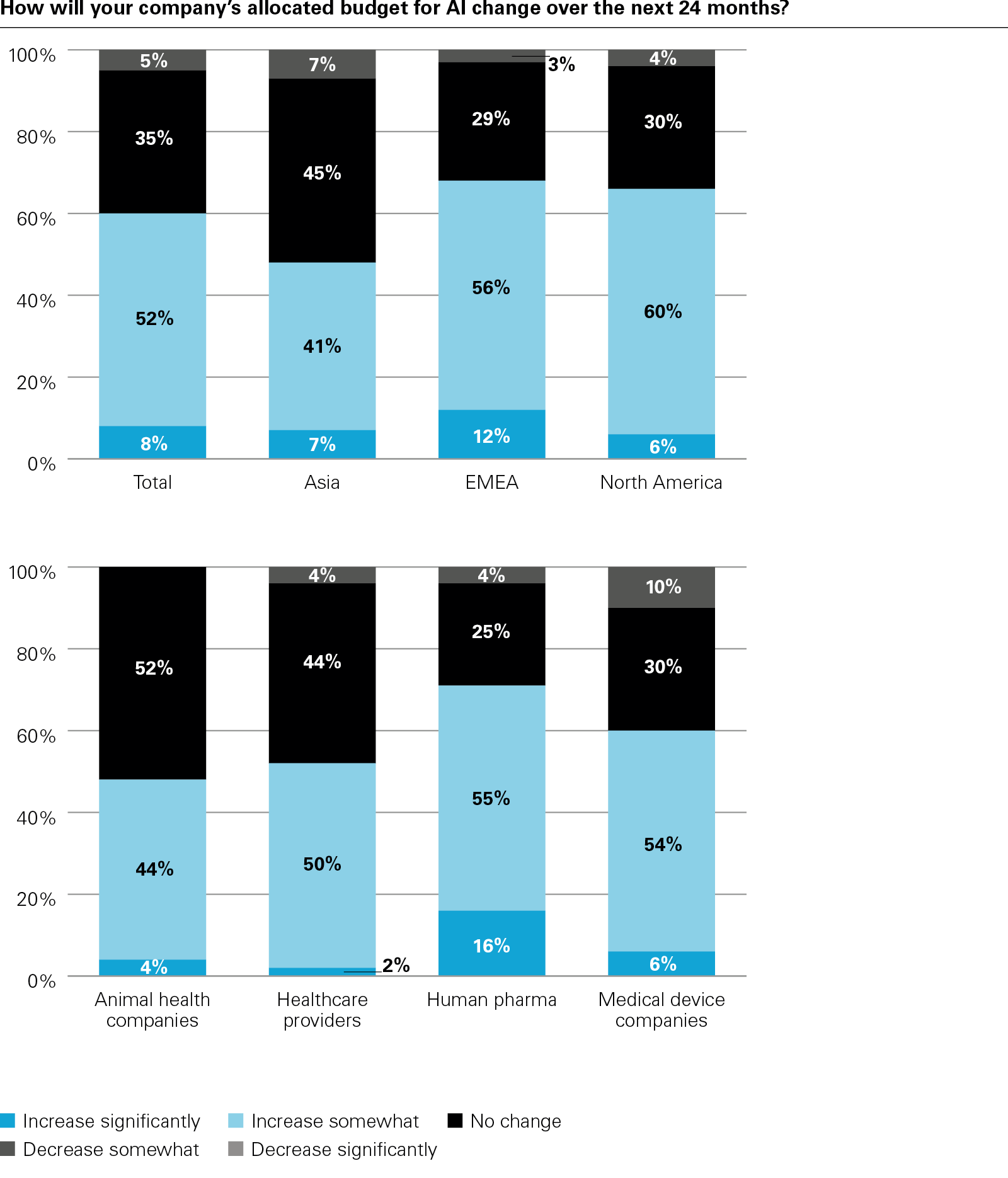

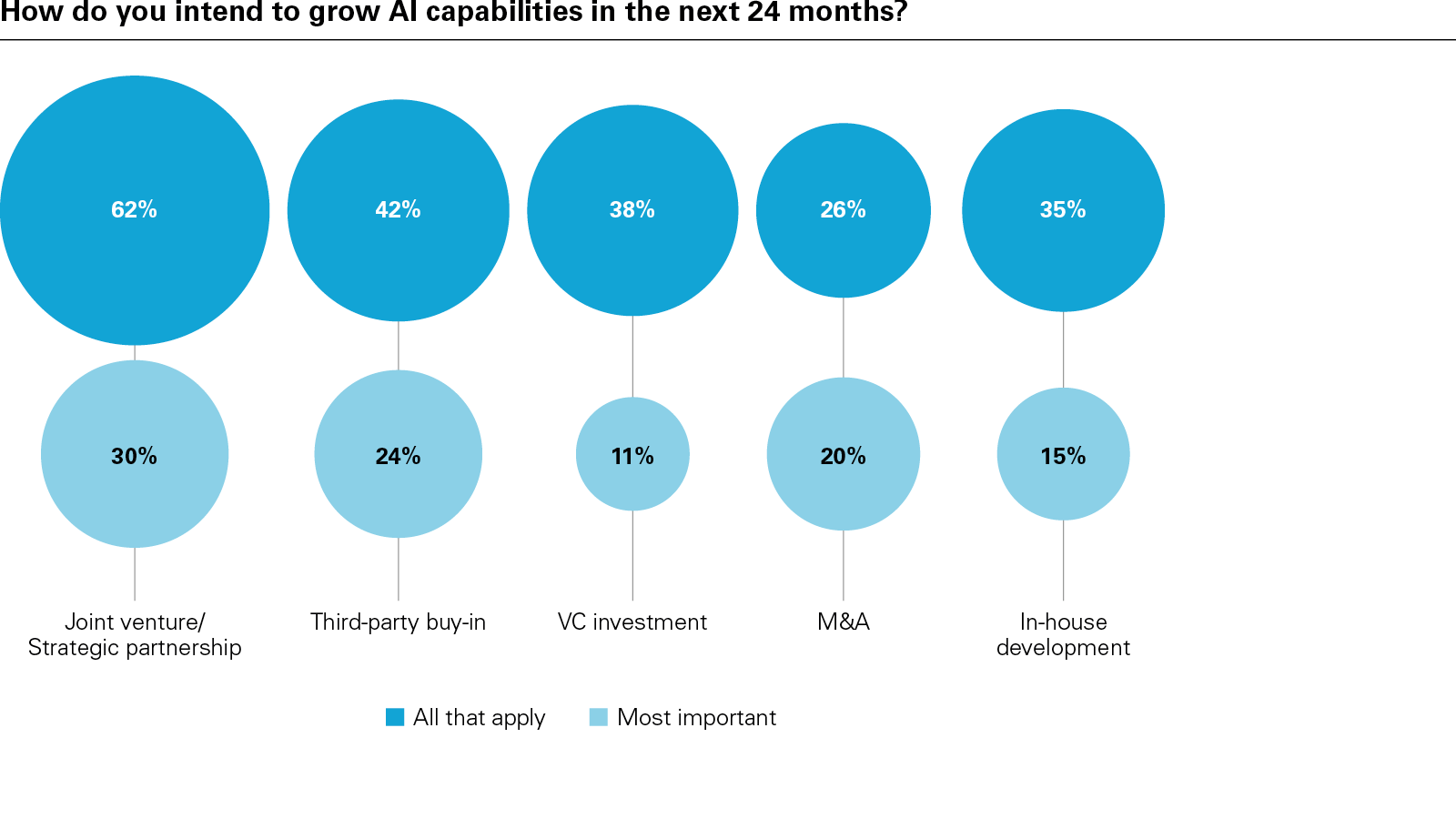

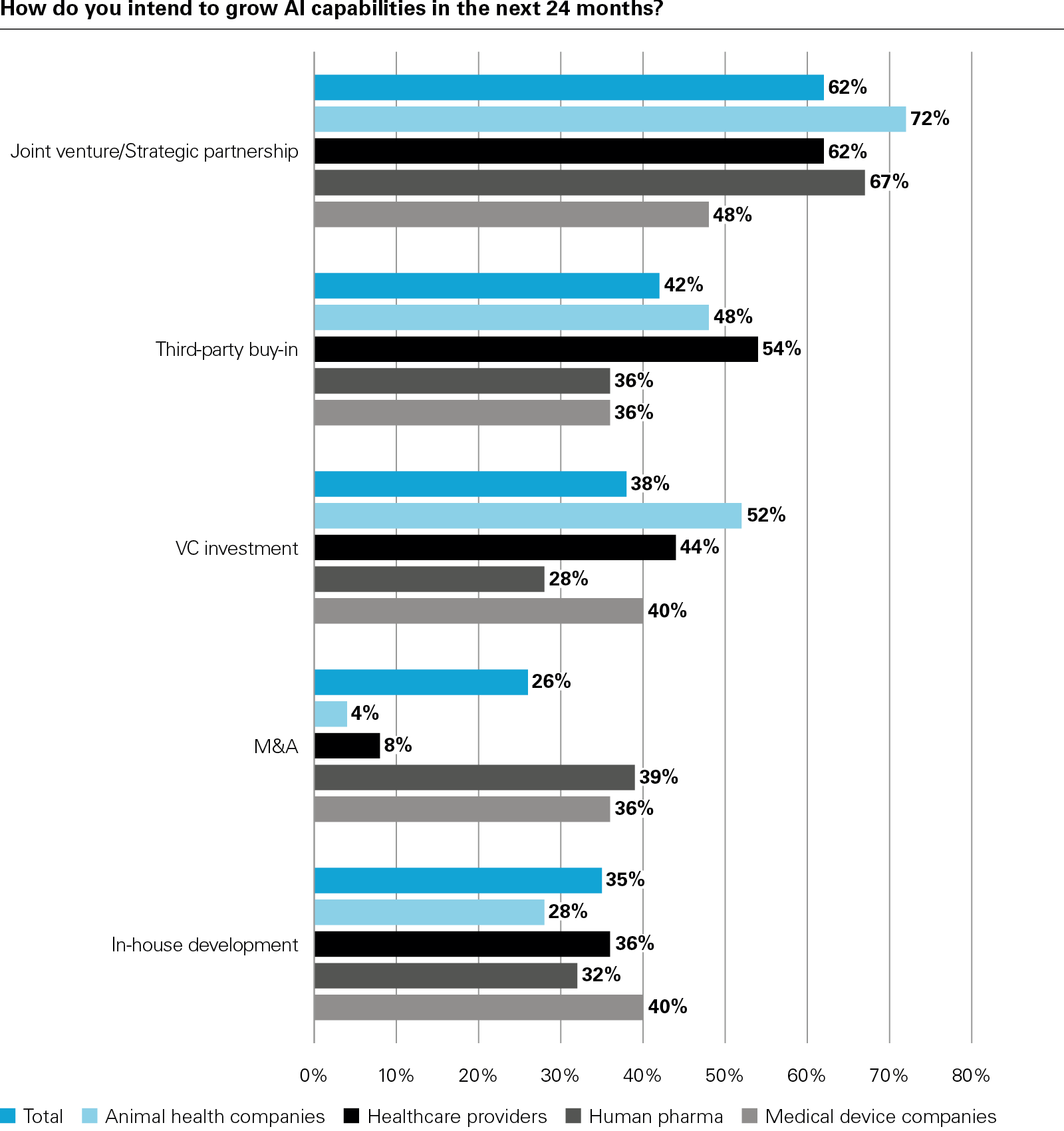

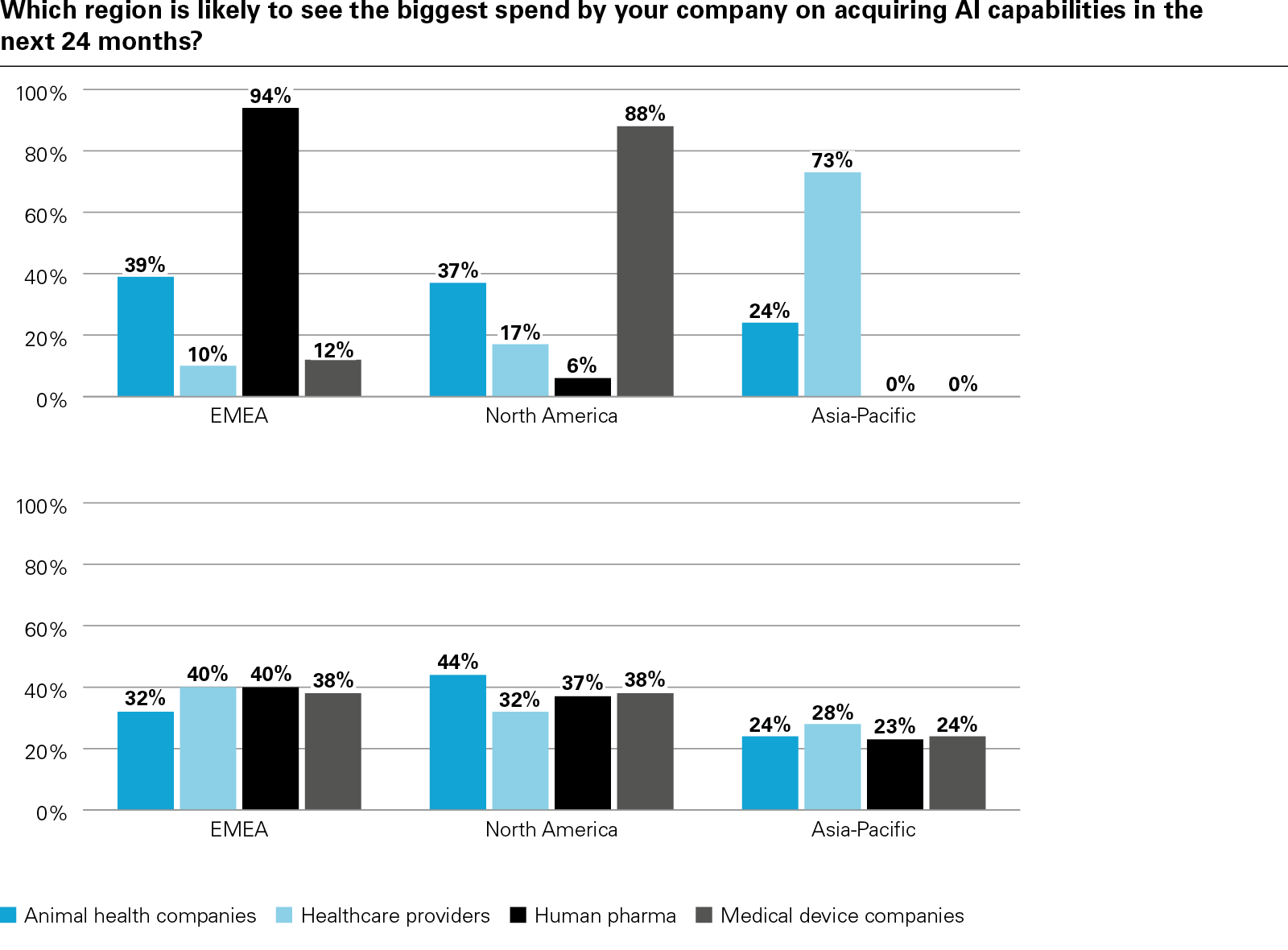

Investment is a central theme. Budgets are shifting from discretionary pilots to embedded line items, with many companies pursuing joint ventures, acquisitions or internal buildouts to accelerate capability development. Local sourcing is often favored, but appetite for cross-border expansion remains in markets with advanced regulatory pathways or concentrated AI talent.

In conclusion, the report examines how success is being defined and why it matters. Metrics such as diagnostic accuracy, cost reduction, and patient access are becoming essential to both internal planning and external validation. Encouragingly, the vast majority of respondents believe AI will improve patient outcomes, while investors increasingly view AI maturity as a signal of innovation-readiness and long-term value creation.

With AI moving rapidly up the agenda in boardrooms and regulatory agencies, understanding how to scale responsibly and legally is critical. This report offers a grounded view of what effective AI adoption in life sciences looks like today—and where the next key opportunities and risks lie.

Methodology

In 2025, White & Case, in partnership with Mergermarket, surveyed 200 senior executives of life sciences organizations. The organizations surveyed included human pharma and biotech companies (75), healthcare providers (50), medical device companies (50) and animal health companies (25). Respondents from each company type were split equally between EMEA (66), Asia-Pacific (67) and North America (67).

Contacts

Partner

|

Brussels

Partner

|

Boston

Partner

|

New York

Counsel

|

Berlin

Counsel

|

Washington, DC

View full image

View full image

View full image

View full image

View full image

View full image

View full image

View full image