Latin American arbitration in transition

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

By Carlos Viana, Latin America Interest Group Leader and Editor of Latin America Focus

We are delighted to introduce the first edition of Latin America Focus, a publication produced by the Latin America Interest Group at White & Case. Our intent with this publication is to provide market insights from our practices and proprietary research that could be valuable to senior decision-makers who have an interest in the region.

COVID-19 hit Latin America's economies more heavily than it hit any other region around the world. The region's economies contracted by nearly 7 percent in 2020, compared to a global average of only 3 percent. Current projections indicate a healthy recovery through the end of 2021, perhaps by as much as 6.9 percent according to S&P Global,1 and thereafter steady growth of about 2.5 percent per annum.

As we look forward to 2022 – 2023, Latin America, in very significant part, will likely continue to face the ebbs and flows of populism, resource nationalism and weak institutions that seem to take turns at flooding some of the countries in the region from time to time. Yet, we also see Latin America propelled away from the COVID-19 swamp by the powerful global engines of economic, social and technological evolution that will push heavy foreign investment into the region: unprecedented global liquidity and the search for yields in emerging markets, the energy transition, the commitments to mitigate climate change by global natural resources and energy companies, and the technology-driven push to digitize and automate the increasingly global world economy. We saw these global drivers, and foreign investors' net-net belief that Latin America will resurge in the medium term, supporting our cross-border business in the region through a 2020 – 2021 period that we expected at the outset could be cataclysmic for foreign investment in view of the region's endemic challenges.

In this edition of Latin America Focus, partners in our Latin America Interest Group have written articles based on their personal experiences in the trenches and market research that go to the very heart of both the latest sequel in the Latin American saga of transitions, and the current global forces of growth, the interplay of which will likely shape what is to come in post-COVID-19 Latin America.

Times of transition are frequently associated with greater incidences of disputes, notably investor-state disputes, but also commercial disputes, especially in times of supply-chain disruption. In "Latin American arbitration in transition," our team outlines the past and present of commercial arbitration in Latin America, and its prospects for the future.

Latin America has experienced many sovereign debt defaults over the past century. The most recent installment of these usually long-brewing crises played out as COVID-19 partly disabled the region, involving Ecuador, Argentina, Belize and Suriname. Meanwhile, Venezuela continues mired in default for more than three years as of the time of publication. In the article "Sovereign debt restructurings in Latin America: A new chapter," our team explores some of the lessons learned and innovations employed in these recent sovereign debt restructuring exercises, providing insights into the implications for the future of sovereign and sub-sovereign international finance and, more broadly, cross-border restructurings, in the region.

With the COP26 conference being held in Glasgow in November 2021 and concerns about climate change at an all-time high, it is unsurprising that environmental, social and governance (ESG) trends are a recurring sub-theme through several of the articles in this inaugural edition of Latin America Focus. In "Sustainable finance in Latin America," our team focuses directly on green, social and sustainability-linked (GSS) bonds. This article also covers other kinds of sustainable finance, and international environmental agreements in this area to which Latin American countries are signatories.

Our world is being transformed by what the World Economic Forum calls the 4th Industrial Revolution, and Latin America is no exception. Over the next few years, the region is expected to experience faster growth in interconnection bandwidth capacity than any other region in the world. This is especially important for Latin America given the role that connectivity and digital capacity play in driving inclusive economic growth and prosperity. In "Bridging Latin America's digital divide," our team takes a detailed look at investments in digital infrastructure across the region. We focus especially on mobile networks (including 5G), data centers and sub-sea cables, exploring also how these investments are being (and might be) funded.

Latin American equity markets proved remarkably resilient to COVID-19, in terms both of growth in their major indexes and in new initial public offerings (IPOs), and other stock and rights issuances. Brazil, in particular, saw a large number of new publicly listed companies emerge in 2020 – 2021. "Equity capital markets in Latin America" provides a current overview of the state of equity capital markets in Latin America, emphasizing key growth opportunities.

Finally, the first half of 2020 saw a sharp contraction in M&A in Latin America, but deal flow has rebounded strongly in 2021. In "M&A in post-COVID-19 Latin America," our team explores some of the factors that international investors need to take into account when investing in the region's growing markets in view of the current environment. Data drawn from White & Case's global M&A Explorer tool is used to show current trends among various cross-sections of deals.

We do hope that you enjoy reading these insights, and find them valuable. Please do not hesitate to let me know if there are any topics that you would like us to cover in future editions.

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

Sovereign debt restructuring solutions developed in Latin America during 2020 and 2021 create a new paradigm for sovereign debt restructurings in the region and globally

GSS bonds and other forms of sustainable finance have become a mainstream feature of Latin American debt capital markets

COVID-19 has created strong incentives for investment in digital infrastructure in Latin America, especially in 5G, private networks, data centers and fiberoptic cables

Strong pandemic-era performance and a look around the corner

Established trends driving M&A globally are also reflected in Latin American deal flow

Sovereign debt restructuring solutions developed in Latin America during 2020 and 2021 create a new paradigm for sovereign debt restructurings in the region and globally

Stay current on your favorite topics

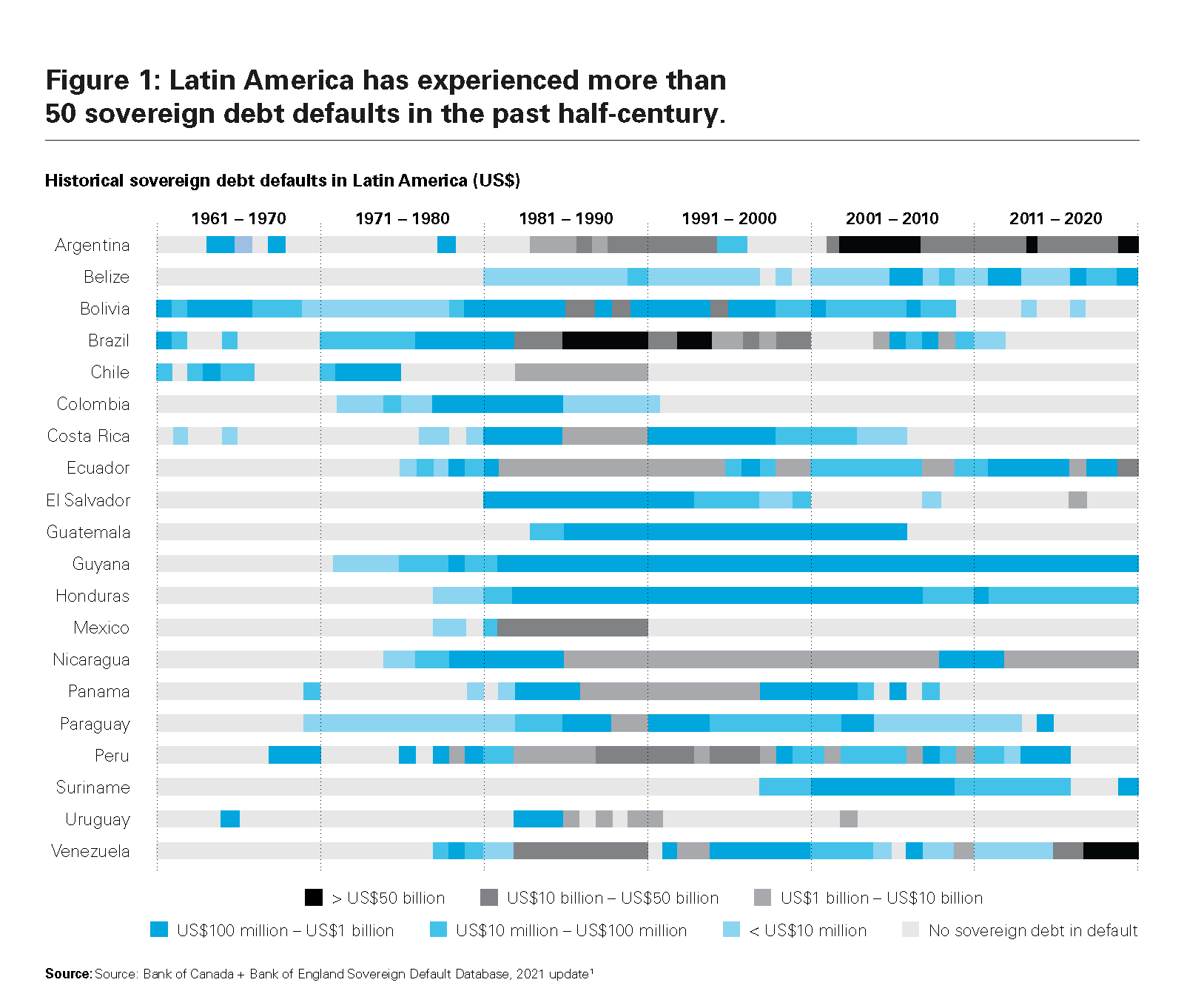

Over the past 50 years, the Latin American and Caribbean region has experienced at least 50 sovereign debt crises and sovereign debt restructurings.

Over the past 50 years, the Latin American and Caribbean region has experienced at least 50 sovereign debt crises and sovereign debt restructurings (see figure 1).1 Domestic macroeconomic mismanagement, currency crises and commodity price shocks are just some of the drivers that have led countries into distress, rendering governments unable to repay their foreign creditors according to the original terms of the underlying debt contracts. In response, sovereign borrowers have engaged in multiple and complex sovereign debt restructuring transactions—with varying degrees of success.

During 2020 and 2021, the region faced yet another shock as a result of the COVID-19 pandemic, which for some countries created new liquidity constraints, while for others exacerbated existing macroeconomic imbalances and fiscal pressures. As a result, several Latin American and Caribbean countries and Argentine provinces sought to comprehensively restructure their external debt: Among others, Argentina restructured approximately US$65 billion of external debt owed to private creditors, Ecuador restructured US$17.4 billion of external private debt, more than ten Argentine provinces collectively restructured in excess of US$10 billion of external private debt, including the Province of Buenos Aires (PBA), which restructured US$7.1 billion of its external private debt, while Suriname is in the process of restructuring US$675 million of external private debt (and a total of US$1.4 billion of external debt).

In the absence of a sovereign bankruptcy regime, the resolution of debt crises is ultimately a matter of ad hoc negotiation between a sovereign and its creditors. In this article, we provide an overview of the resolution of sovereign debt crises in Latin America in the COVID-19 era. In particular, we discuss (1) the evolution of debt and creditor compositions and the corresponding restructuring challenges, (2) the role of the International Monetary Fund (IMF) in the restructuring process and in the provision of financing, and (3) the adopted restructuring mechanisms that have provided substantial debt relief to several sovereign and sub-sovereign debtors.

By drawing comparisons to pre-COVID-19 debt crisis resolutions in the region, we conclude that the solutions found during 2020 and 2021 create a new paradigm for sovereign debt restructurings in the region and globally, where good-faith negotiations between sovereign debtors and organized creditor groups, together with targeted use of contractual mechanisms to reduce holdout risks, can lead to orderly restructuring transactions that provide debtors substantial debt relief, preserve value for investors, and minimize the risk of chronic and acrimonious litigation.

Bondholder committees have proven successful in reaching consensual restructuring deals with the debtor that provide needed debt relief while preserving bondholder value.

The landscape of sovereign borrowing has evolved considerably over the past 40 years. Before the 1970s, many Latin American countries borrowed proportionately more from multilateral lenders, including the IMF, the World Bank and the Inter-American Development Bank, and "official" lenders, including the US and other developed economies. The source of credit fundamentally shifted in the 1970s, however, when, as a result of oil price shocks, Organization of Petroleum Producing Countries (OPEC) countries experienced sudden massive trade surpluses and deposited oil earnings and receipts in commercial banks. The banks, in turn, extended relatively cheap credit to Latin American countries to finance their fiscal and current account deficits, amounting in many cases to more than two-thirds of external financing.

The debt and creditor composition again changed drastically during the Brady bond restructuring era in the late 1980s. Increased debt levels following the borrowing splurge of the 1970s and early 1980s made many countries in the region highly vulnerable to refinancing and interest rate risk. Rising interest rates in the US soon led borrowers such as Mexico, Brazil, Venezuela and Argentina to conclude that their debt burdens had become unsustainable. After a "lost decade" of economic stagnation, and superficial and inadequate debt re-profiling efforts, Latin American countries embraced the Brady initiative, persuading their commercial bank lenders to exchange their non-performing loans into tradable instruments that were issued with a principal haircut but were backed by US treasury notes as collateral. This allowed banks to free up capital by substituting non-performing assets on their balance sheets with collateralized, performing obligations of the same debtor. The large-scale Brady bond restructurings of the 1980s and 1990s led to the widespread replacement of syndicated loans by tradable bonds as the primary source of sovereign borrowing and financing in Latin America. From that point onward, the domestic and international bond markets became the principal source of finance for Latin American sovereign issuers.

As the source of credit shifted, the composition of sovereign creditors changed as well. Bank lenders, often with decades of on-the-ground experience and a profound understanding of local political and economic trends, were replaced by anonymous and dispersed holders of interests in global bonds lodged in the international clearing systems.

From the sovereign's perspective, a dispersed and heterogenous private creditor base makes a potential debt restructuring operation particularly complicated: Not only is it hard to locate and negotiate with creditors, but a sovereign also has to negotiate with creditors that have different business models and economic preferences, and therefore, respond to different incentives. Specialist distressed debt investors behave differently than "real money" institutional investors, retail investors behave differently than local banks, and so on. In the absence of a sovereign debt restructuring regime, or sufficiently robust contractual mechanisms embedded in the terms of the debt instruments, this landscape creates opportunities for holdout behavior that can debilitate a restructuring process, as illustrated by the Argentine restructuring saga between 2001 and 2014 discussed further below.

Lack of creditor coordination can create risks from the creditor perspective as well: A dispersed and uncoordinated creditor base may tempt a sovereign to launch a unilateral, non-negotiated transaction or play creditors against one another in an effort to extract outsized value from the creditor claims. Take, for example, Ecuador's debt buyback in 2008: Ecuador publicly defaulted on two series of bonds, depressing their prices, and then proceeded to buy them back in a Dutch auction using financial intermediaries. Lack of creditor coordination arguably contributed to the success of this effort, as creditors were not able to set forth a unified response to the default.

The establishment of representative creditor (particularly bondholder) committees provides an answer to the creditor coordination problem. Creditor committees facilitate information flow between the debtor and the creditors, reduce information asymmetry and facilitate constructive dialogue between the parties. Indeed, a key characteristic of the Latin America debt restructurings in the COVID-19 era has been the presence of well-organized creditor committees.

In each of the COVID-19-era restructuring cases, the composition of the creditor committee has been critical. In every case, committees have been composed of either large institutional investors who had purchased debt in the primary market, or hedge funds that had been long-term active investors in the secondary market. Such committees have been widely perceived to represent the interests of the broad class of bondholders, giving credibility to the negotiating process and facilitating relatively quick resolutions.

In the case of Argentina, Ecuador, Suriname and several Argentine provinces in 2020/2021, bondholder committees have proven successful in reaching consensual restructuring deals with the debtor that provide needed debt relief while preserving bondholder value. In the case of Ecuador and Suriname, creditor committees first negotiated temporary deferral of payment obligations to provide breathing space until a longer-term debt restructuring solution could be found. Ultimately, Ecuador reached a comprehensive restructuring agreement with its bondholder committee in September 2020, while Suriname remains in debt restructuring talks with its bondholder committee.

Equally notable, creditor committees have been effective in rejecting lowball and unilateral "take-it-or-leave-it" offers designed to extract maximum debt relief from external creditors, as in the case of Argentina in 2020 and the Province of Buenos Aires in 2020 – 2021. Argentina launched an exchange offer in early 2020 with subsequent unilateral amendments that were all quickly and publicly rejected by Argentina's largest bondholder groups. Such public rejection continued until successive counteroffers led to a mutually acceptable deal. At that stage, the public endorsement of the deal by the largest bondholder groups led to overwhelming support for the deal.

In addition to private commercial debt, either in the form of bank loans or bonded debt, and to traditional official and multilateral loans, the external liabilities of many Latin American countries today include exposures to repurchase obligations, supplier credits, secured debts, guaranteed debt of state-owned enterprises and, on many occasions, court judgments or arbitral awards. If such other categories of debts are denominated in foreign currency or governed by foreign law, then they often need to be taken into account when assessing the sustainability of the sovereign's debt stock. Having a highly heterogenous debt stock creates additional challenges for sovereign debtors in a restructuring scenario, as creditors holding different categories of claims often have differing expectations as to the relative seniority or priority that should be accorded such claims. Nowhere is this complexity more evident than in the ongoing case of Venezuela's debt restructuring, where the perimeter of an external debt restructuring, if and when that becomes politically feasible, may include debt of the sovereign, debt of the state-owned oil company PDVSA, various promissory notes, arbitral awards and other liabilities.

The IMF has played a central role in sovereign debt restructurings in Latin America and globally. Often seen as the lender of last resort, member countries approach the IMF when faced with significant balance-of-payment problems. Under the IMF's Articles of Association, the IMF may only provide its general resources to assist in the resolution of balance-of-payment problems if there are "adequate safeguards" for the IMF resources. This requires that the IMF concludes the debt of the sovereign is sustainable and that it be satisfied with the policy adjustments being undertaken by the debtor country to overcome the problems that led it to seek financial aid (such required policy adjustments are known as conditionality). If, following a debt sustainability analysis, the IMF determines that a country's debt is not sustainable, it is precluded from lending (including emergency financing) unless the member country takes steps to restore sustainability, which often requires seeking debt relief from its creditors. IMF lending has a tumultuous history in Latin America as a result of strict conditionality and austerity programs that were seen as impediments to growth and development, prohibited popular social spending programs, and thus became politically toxic.

Since the outset of the COVID-19 pandemic, the IMF has become more flexible in extending concessional financing: Notably, the IMF doubled the access to its emergency facilities—the Rapid Credit Facility and the Rapid Financing Instrument (RFI)—to accommodate increased demand for emergency financing. Borrowing from these facilities does not require the adoption of a full-fledged program or strict conditionality, unlike when the IMF extends balance-of-payment support (although it does require an assessment of debt sustainability as discussed above). By the end of 2020, more than 60 percent of the IMF emergency financing went to Latin America and the Caribbean, the regions hit hardest by the crisis. Bolivia, Costa Rica, Dominican Republic, El Salvador, Grenada and Ecuador are some of the countries that received RFI financing.

By contrast, few countries in Latin America qualified for the IMF's Flexible Credit Line (FCL). The FCL provides flexibility to draw on the credit line at any time during the period of the arrangement (one or two years). This large, upfront access to IMF resources with no conditionality has only been granted to countries with very strong macroeconomic records, such as Colombia, Chile and Peru.

While sovereigns in Latin America have historically been reluctant to request financial support from the IMF as part of a fully fledged program, such programs are not only welcomed by creditors, but sometimes required as a pre-condition to a debt restructuring. The reasoning is simple: The conditionality of an IMF program ensures a certain degree of macroeconomic and fiscal discipline, and the adoption of a credible policy framework for the country's return to debt sustainability.

This was clearly the case in Ecuador's 2020 restructuring, where bondholders conditioned the consummation of the restructuring transaction and the provision of debt relief on the adoption of an IMF program by a certain date. Argentine bondholders did not require a similar condition in connection with the consummation of that country's 2020 debt restructuring, in part because the IMF was a recent and large creditor, which presented additional complications. However the subsequent (and unanticipated) fall in Argentine bond prices, which many market participants attributed to the absence of an IMF-supported adjustment program and policy framework, may be seen as a cautionary tale by investors in future regional restructurings.

60%

By the end of 2020, more than 60 percent of the IMF emergency financing went to Latin America and the Caribbean, the regions hit hardest by the COVID-19 crisis

In the absence of an internationally recognized bankruptcy regime for sovereigns, a distressed sovereign debtor can only restructure its debts through negotiation with its creditors—requiring good faith and realism on both sides. With the prevalence of bonded debt across Latin America following the Brady bond restructurings of the 1980s and 1990s, the risk of strategic holdout behavior from anonymous bondholders increased substantially. No longer were sovereigns able to work out the terms of their debt restructuring within the relatively predictable and reliable framework of the "London Club" of major commercial bank creditors, where they could have a high degree of confidence that the negotiated terms would be widely accepted within the international financial community. Instead, sovereign debtors faced the risk of disruption posed by individual bondholders seeking to capitalize on the sacrifices made by other creditors. The source of this problem lies in the terms of sovereign bond contracts themselves, specifically in the requirement (virtually universal prior to 2003) that changes to bond payment terms must attract unanimous creditor support. In other words, there was no contractual mechanism for a supermajority of bond investors who favored a debt restructuring proposal to bind a minority of holdout investors to the terms of the restructuring.

In the absence of an alternative, sovereigns conducted debt restructurings by way of voluntary exchange offers, inviting creditors to exchange their existing bonds for new bonds with reduced payment terms that included lower principal, lower coupons, an extension of maturities, or all three. A use of specific incentives and disincentives would accompany each offer to maximize participation and minimize holdout risk.

Ecuador in 2000, for example, was the first sovereign to use an "exit consent" technique to restructure its debt. While New York law-governed bonds required unanimity to amend payment terms, they only required a simple majority to amend various non-payment terms of each bond series. Ecuador, therefore, invited bondholders to exchange their bonds and, in the process, amend various terms of their existing bonds to make them less attractive to holdout creditors. The proposed modified terms removed the cross-default clause, the negative pledge clause and the requirement to list the bonds on the Luxembourg Stock Exchange.

In 2003, Uruguay also utilized an exit consent technique to restructure its New York law-governed bonds, albeit narrower than Ecuador's. There the proposed modification—which narrowed the sovereign immunity waiver—was intended to limit the ability of holdouts to attach payments made by the sovereign to service the new bonds offered on the exchange. The exit consent was supplemented by an explicit threat that Uruguay would prefer the servicing of exchanged debt over non-exchanged debt.

While the use of exit consents and other restructuring mechanisms worked well in these early cases of Ecuador and Uruguay, leading to bondholder participation in excess of 90 percent, the shortcomings of these techniques in remedying the collective action problem were revealed in Argentina's 2001 – 2014 restructuring saga. At that time, Argentina's outstanding bonds did not include collective action clauses that would allow payment terms to be amended with supermajority support, and because creditors had allegedly amassed more than 50 percent in some individual series, a comprehensive exit consent strategy was not an option. Argentina's strategy relied on the use of "value recovery instruments" (in particular GDP-linked warrants that would provide creditors who participated in the restructuring additional value to compensate for their losses if Argentina's GDP exceeded certain targets)—and the explicit threat of non-payment of non-exchanged debt. The threat of non-payment was carried through via the introduction of the Lock Law in 2005, which made it illegal, as a matter of Argentine law, for the sovereign to service defaulted debt or settle with holdout creditors. Notwithstanding those elements, Argentina's exchange offer was only accepted by approximately 75 percent of its creditors. Holdout creditors sought to enforce their claims in court and arbitral tribunals for years, some for nearly a decade, before Argentina was forced to settle them. During this time, Argentina was shut off from the international capital markets. International arbitration under investment treaties in particular was used to facilitate the initial settlement agreement with the government of President Mauricio Macri that proved to be the beginning of the end of the Argentine debt saga, although the use of arbitration in the sovereign debt restructuring context is highly dependent on particular facts and treaties, and has been marked by significant debate.

Prompted by the difficulties in restructuring Argentina's debt, the international community decided that the collective-action problem would be best remedied by re-drafting New York law-governed debt contracts to allow a bondholder supermajority to bind a minority to the terms of a debt restructuring. Collective action clauses (CACs) did just that and were included widely in New York law-governed bonds following Mexico's debt issuance in 2003. Following the approach that had been accepted in English law-governed bonds for many years, Mexico-style CACs permitted a qualified bondholder supermajority, usually 75 percent per bond series (the "series-by-series" CAC), that approved modifications to the payment terms of the bonds to bind a dissenting minority into the modifications. That design, however, was not immune from the risk of creditors amassing over a quarter of a series in order to pursue a holdout strategy.

The design of CACs evolved over time in response to the evolving strategies and increased financial resources of potential holdout creditors. The CACs drafted and endorsed by the International Capital Markets Association (ICMA) in 2014 represent the latest and most widely accepted iteration of the clauses. ICMA CACs provide three options for modifying the payment and other key terms of sovereign bonds: (1) a single-series option, which requires a 75 percent supermajority of each relevant series; (2) a "two-limb" option, which requires a 66 2/3 percent supermajority across all series of bonds voting in a designated pool and a 50 percent majority of each bond series within the pool; and (3) a "single-limb" option, which requires a 75 percent supermajority across all series of bonds voting in a designated pool as long as all holders are offered the same instrument or a choice from the same menu of instruments.

The COVID-19-era Latin America restructurings provided the first occasion for the new ICMA CACs to be tested in practice, though on several occasions the debt to be restructured included debt issued pre-2014 that did not include the enhanced CACs or included CACs with different, usually higher, voting thresholds.

Notwithstanding such heterogeneity, the CACs operated to facilitate consensual restructuring outcomes for Argentina, Ecuador and a number of Argentine provinces in 2020/2021. While each debtor tailored its restructuring proposal to its particular characteristics, the availability of CACs, coupled with the endorsement of large creditors and well-organized creditor committees, ultimately catalyzed a holistic restructuring for these debtors.

Ecuador was the first sovereign to consummate a restructuring transaction in September 2020. In July 2020, after constructive consultation with its largest creditor group, Ecuador launched a consent solicitation and exchange offer inviting holders of ten series of bonds to consent to the amendment of those bonds and exchange them for new bonds in three series maturing in 2030, 2035 and 2040. Holders who chose to participate in the exchange offer and receive the package of new bonds also consented to modify the payment terms of the outstanding existing bonds (held by holdout creditors) to replicate the terms of the least attractive, longer-dated new bond. Concurrently, Ecuador solicited the consent of holders to delete a contractual provision (dubbed the "No Less Favorable Treatment" clause) restricting Ecuador's ability to leave non-consenting holders financially impaired vis-à-vis consenting holders. After prevailing in a New York lawsuit brought by an investor seeking to enjoin the restructuring, Ecuador reached the requisite CAC thresholds in all series and achieved a 98 percent creditor participation in the process.

While Argentina was pursuing its restructuring concurrently with Ecuador, it initially took a more confrontational approach toward its creditors, launching a unilateral exchange offer where it attempted to take advantage of certain deficiencies in the drafting of the ICMA CACs to consummate a restructuring that was not supported by a bondholder supermajority. Following months of failed negotiations and a series of rejected offers, Argentina agreed to the terms of a debt restructuring with its largest creditor groups. The terms of the restructuring would provide Argentina with US$39 billion of debt relief over the following nine years, via a combination of maturity extensions and coupon reductions, and would also enhance the legal terms of the bonds to rectify the observed deficiencies in the ICMA CACs.2

In August 2020, Argentina proposed these terms to its bondholders via a structure combining the use of the two-limb CACs with the use of exit consents, in a combined exchange offer and consent solicitation. Under this structure, holders who agreed to participate in the exchange offer and tender their bonds for a new bond chosen from a menu of options would also be deemed to consent pursuant to the two-limb CACs to substitute any outstanding existing bonds (which would thereafter be held only by holdout creditors) for new bonds with the least favorable maturity structure.

Similarly to the Argentine sovereign, the province of Buenos Aires launched a unilateral offer in 2020 that was repeatedly extended for over a year due to lack of participation. Following months of lack of engagement and progress in the negotiations, members of the organized creditor committee filed a lawsuit in New York courts to recover defaulted principal and interest amounts. Ultimately, PBA reached a deal with its largest creditor and committee member in July 2021 and subsequently launched an amended offer. The amended offer provided that while participating holders were entitled to receive new "A" or "B" bonds, non-participating holders would receive new "C" bonds that have materially worse terms compared to A and B bonds, if the CAC thresholds were met under each series. Because certain of PBA's bonds issued under its "old" 2006 indenture contained higher CAC thresholds than bonds issued under its more recent 2015 indenture (which contained ICMA CACs), PBA incorporated additional exit consents in the restructuring proposal for those series to disincentivize holdout behavior. Although PBA launched the offer after negotiating and agreeing to the terms with its largest bondholder, it had not obtained the support of the entire committee. In the absence of such support, the offer and the associated mechanics were not well received by many in the investor community, who deemed that PBA had launched a coercive offer designed to force bondholders into a deal. Notwithstanding such opposition, PBA's restructuring ultimately obtained the support of 93 percent of its existing bondholders.

The novelty in the combined use of CACs and exit consents in COVID-19-era restructurings in Latin America is that, in contrast to the use of exit consents by Ecuador and Uruguay in the early 2000s, creditors who tender or "exit" their existing instruments also consent to modifications of payment terms (as opposed to legal terms) of bonds held by holdout creditors. This threat of imposing on non-consenting creditors less favorable financial treatment is a stronger incentive to participate than had been the case with the prior generation of exit consents, where bondholders were left with impaired legal terms, but were still entitled to their original claim for principal and interest. Furthermore, in all the COVID-19-era restructurings in Latin America, accrued interest on debt instruments being restructured was only paid to consenting, or participating, bondholders—further heightening the financial penalty for a failed holdout strategy.

This use of CACs and exit consents was only effective after the debtor in each case had built prior consensus and obtained the support of its main bondholder groups (or in the case of PBA, its largest creditor). In the presence of well-organized creditor groups with significant holdings across the yield curve, it has proven impossible for a sovereign to successfully use CACs with exit consents to force a hostile, unilateral offer upon the market. The COVID-era experience in sovereign debt restructuring has, thus, proven that well-organized creditor groups can effectively resist sovereign debtors' opportunistic and coercive use of these powerful restructuring techniques. Accordingly, good-faith negotiation between debtors and their creditor committees remains the lynchpin to successful sovereign and sub-sovereign restructurings.

The experience of Latin American sovereigns and sub-sovereigns in COVID-19-era debt restructurings bodes well for the future of sovereign restructurings. After the unruly debt restructuring episodes of the past, the evolution of the contractual architecture, the increased appetite for strong creditor coordination early in the restructuring process, and the willingness of debtors and creditors alike to engage in good-faith negotiations have proven to be catalysts for (relatively) orderly and consensual restructuring outcomes.

As the restructuring techniques employed in Latin American situations effectively addressed holdout and collective action problems (although not without controversy), we can expect to see these same techniques employed in future sovereign restructuring cases in Latin America and beyond.

1 D. Beers, Z. Quiviger and J. F. Walsh (2021), BoC–BoE Sovereign Default Database: What's New in 2021? Bank of England.

2 For a detailed discussion of the restructuring mechanisms of the 2020 Argentine restructuring, the controversial use of CACs and the negotiated legal enhancements to the terms of the bonds, see Ian Clark and Dimitrios Lyratzakis, Towards a More Robust Sovereign Debt Restructuring Architecture: Innovations from Ecuador and Argentina, Capital Markets Law Journal, Volume 16, Issue 1, January 2021, pp. 31–44.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: Figure 1: Latin America has experienced more than 50 sovereign debt defaults in the past half-century (PDF)

View full image: Figure 1: Latin America has experienced more than 50 sovereign debt defaults in the past half-century (PDF)

View full image: Total debt in default by country in 2020 (US$) (PDF)

View full image: Total debt in default by country in 2020 (US$) (PDF)