Latin American arbitration in transition

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

By Carlos Viana, Latin America Interest Group Leader and Editor of Latin America Focus

We are delighted to introduce the first edition of Latin America Focus, a publication produced by the Latin America Interest Group at White & Case. Our intent with this publication is to provide market insights from our practices and proprietary research that could be valuable to senior decision-makers who have an interest in the region.

COVID-19 hit Latin America's economies more heavily than it hit any other region around the world. The region's economies contracted by nearly 7 percent in 2020, compared to a global average of only 3 percent. Current projections indicate a healthy recovery through the end of 2021, perhaps by as much as 6.9 percent according to S&P Global,1 and thereafter steady growth of about 2.5 percent per annum.

As we look forward to 2022 – 2023, Latin America, in very significant part, will likely continue to face the ebbs and flows of populism, resource nationalism and weak institutions that seem to take turns at flooding some of the countries in the region from time to time. Yet, we also see Latin America propelled away from the COVID-19 swamp by the powerful global engines of economic, social and technological evolution that will push heavy foreign investment into the region: unprecedented global liquidity and the search for yields in emerging markets, the energy transition, the commitments to mitigate climate change by global natural resources and energy companies, and the technology-driven push to digitize and automate the increasingly global world economy. We saw these global drivers, and foreign investors' net-net belief that Latin America will resurge in the medium term, supporting our cross-border business in the region through a 2020 – 2021 period that we expected at the outset could be cataclysmic for foreign investment in view of the region's endemic challenges.

In this edition of Latin America Focus, partners in our Latin America Interest Group have written articles based on their personal experiences in the trenches and market research that go to the very heart of both the latest sequel in the Latin American saga of transitions, and the current global forces of growth, the interplay of which will likely shape what is to come in post-COVID-19 Latin America.

Times of transition are frequently associated with greater incidences of disputes, notably investor-state disputes, but also commercial disputes, especially in times of supply-chain disruption. In "Latin American arbitration in transition," our team outlines the past and present of commercial arbitration in Latin America, and its prospects for the future.

Latin America has experienced many sovereign debt defaults over the past century. The most recent installment of these usually long-brewing crises played out as COVID-19 partly disabled the region, involving Ecuador, Argentina, Belize and Suriname. Meanwhile, Venezuela continues mired in default for more than three years as of the time of publication. In the article "Sovereign debt restructurings in Latin America: A new chapter," our team explores some of the lessons learned and innovations employed in these recent sovereign debt restructuring exercises, providing insights into the implications for the future of sovereign and sub-sovereign international finance and, more broadly, cross-border restructurings, in the region.

With the COP26 conference being held in Glasgow in November 2021 and concerns about climate change at an all-time high, it is unsurprising that environmental, social and governance (ESG) trends are a recurring sub-theme through several of the articles in this inaugural edition of Latin America Focus. In "Sustainable finance in Latin America," our team focuses directly on green, social and sustainability-linked (GSS) bonds. This article also covers other kinds of sustainable finance, and international environmental agreements in this area to which Latin American countries are signatories.

Our world is being transformed by what the World Economic Forum calls the 4th Industrial Revolution, and Latin America is no exception. Over the next few years, the region is expected to experience faster growth in interconnection bandwidth capacity than any other region in the world. This is especially important for Latin America given the role that connectivity and digital capacity play in driving inclusive economic growth and prosperity. In "Bridging Latin America's digital divide," our team takes a detailed look at investments in digital infrastructure across the region. We focus especially on mobile networks (including 5G), data centers and sub-sea cables, exploring also how these investments are being (and might be) funded.

Latin American equity markets proved remarkably resilient to COVID-19, in terms both of growth in their major indexes and in new initial public offerings (IPOs), and other stock and rights issuances. Brazil, in particular, saw a large number of new publicly listed companies emerge in 2020 – 2021. "Equity capital markets in Latin America" provides a current overview of the state of equity capital markets in Latin America, emphasizing key growth opportunities.

Finally, the first half of 2020 saw a sharp contraction in M&A in Latin America, but deal flow has rebounded strongly in 2021. In "M&A in post-COVID-19 Latin America," our team explores some of the factors that international investors need to take into account when investing in the region's growing markets in view of the current environment. Data drawn from White & Case's global M&A Explorer tool is used to show current trends among various cross-sections of deals.

We do hope that you enjoy reading these insights, and find them valuable. Please do not hesitate to let me know if there are any topics that you would like us to cover in future editions.

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

Sovereign debt restructuring solutions developed in Latin America during 2020 and 2021 create a new paradigm for sovereign debt restructurings in the region and globally

GSS bonds and other forms of sustainable finance have become a mainstream feature of Latin American debt capital markets

COVID-19 has created strong incentives for investment in digital infrastructure in Latin America, especially in 5G, private networks, data centers and fiberoptic cables

Strong pandemic-era performance and a look around the corner

Established trends driving M&A globally are also reflected in Latin American deal flow

Strong pandemic-era performance and a look around the corner

Stay current on your favorite topics

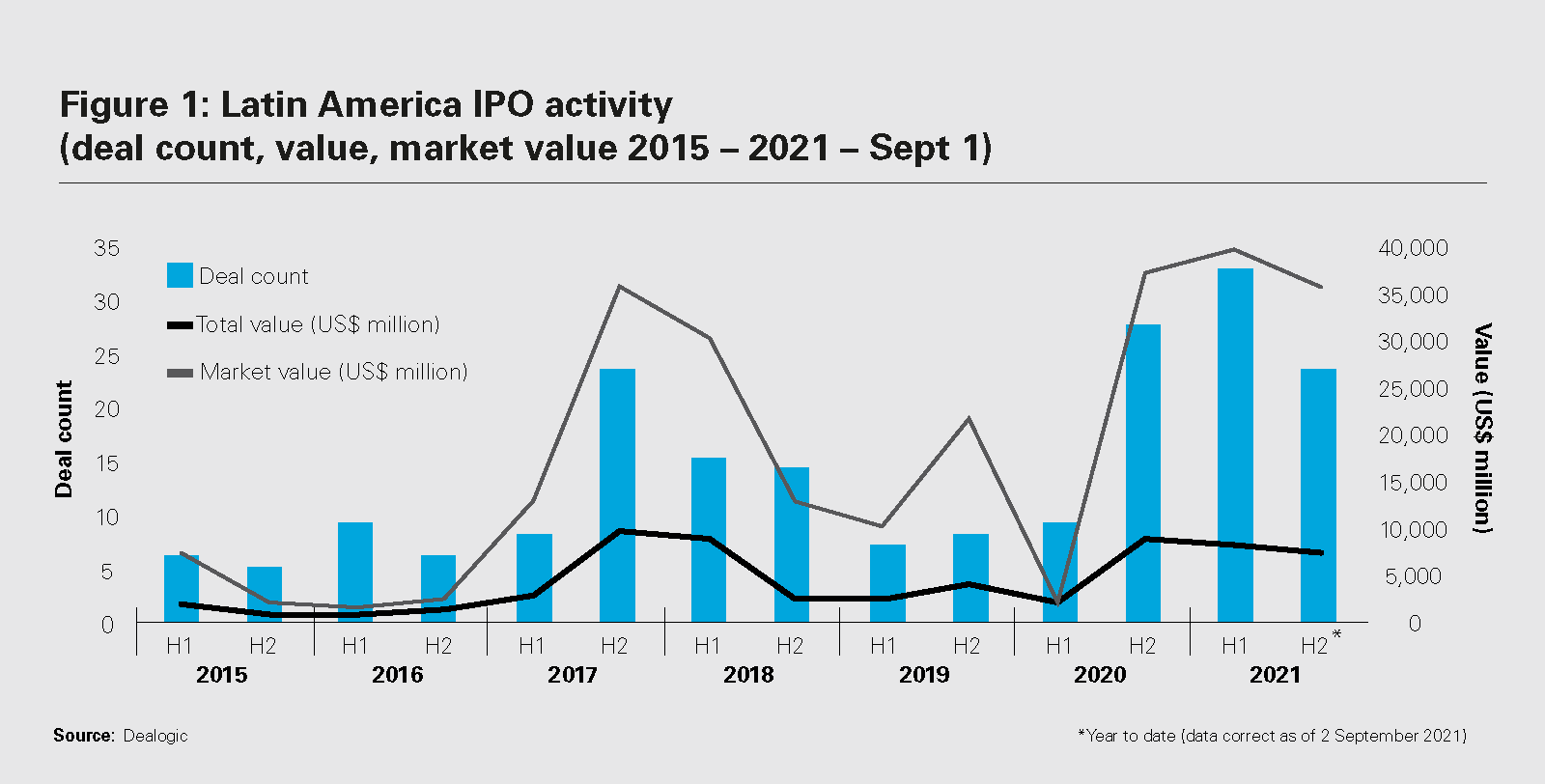

IPO activity in Latin America has hit record levels in 2021, with the region’s largest economy taking the lion’s share of the bounty.

During the first eight months of 2021, Latin America recorded its strongest initial public offering (IPO) activity of the past six years. In total, 55 IPOs took place up to the end of August. That compared to 36 new issues for the whole of 2020. All this in a year that saw the region's economy contract by 6.9 percent due to the COVID-19 pandemic1—the sharpest contraction in the world.2

Moreover, first-half deal volume (32 in H1) also accelerated compared to the second half of last year, when 27 companies came to market for the first time. Value and volume have already outstripped every year since 2015, and, with more companies unveiling plans to come to market, records may continue to be smashed (see figure 1).

This stands in sharp contrast to the general trend over the past decade, which saw domestic Latin American markets struggling to attract new companies to go public, with capital from US and European markets shifting toward emerging markets in Asia-Pacific.3 This meant that Latin American markets remained concentrated around a relatively low number of listed companies largely dominated by company groups. The recent uptick in Latin American IPO activity injects new life into the global IPO scene.

In value terms, the region also posted strong figures: The 55 IPOs to the end of August raised US$15.17 billion, an increase of 41 percent compared to the whole of 2020, when US$10.8 billion was raised.

The broad range of sectors that saw significant IPO activity is also noteworthy. Since January 2021 in Brazil, there has been a steady stream of IPOs in more traditional industries such as oil & gas, financial services and transport and retail. However, we have also seen activity in sectors such as healthcare with the IPO of Hospital Care Caledonia; mining with Companhia Brasileira de Alumínio coming to market; technology as TC Traders Club S.A. floated on the São Paulo exchange in July; and in telecoms with Unifique Telecomunicações S.A. coming to market in the same month.

The Brazilian market dominated Latin American dealmaking during the first half of 2021, with the country accounting for all but five of the IPOs that came to market. The strength of the country's new issue market reflects the broader bounce-back of the Brazilian economy in 2021. The International Monetary Fund (IMF) expects economic growth of 3.7 percent in Brazil this year, followed by 2.6 percent growth in 2022; that compares to an estimated decline of 4.1 percent over the whole of 2021.

Market analysts also point to the strength of Brazilian equities during the first half of the year, with the Bovespa stock market index rising 8.4 percent over the six months to June 30. That has seen both domestic and international investors take increasing interest in the country.

Mexico's IPO market has been slow over the past few years. There have been a number of factors behind this including the implementation of several regulatory policies that limit private investment in the energy sector, and the slowdown from the COVID-19 pandemic. This has resulted in Mexican companies struggling to find adequate incentives to make offerings. However, the deals that are being done demonstrate that investors (particularly institutional investors, such as AFORES, the Mexican pension funds) have the appetite to invest in the equities market.

In 2020, BlackRock Inc. launched its iShares ESG MSCI Mexico ETF (ESGMEX), on the Mexican Stock Exchange (Bolsa Mexicana de Valores), which is the first ETF that tracks a Mexican market-based sustainable index (the ESG Mexico ESG Select Focus Index). Within the first few months of its launch, this ETF reached US$500 million in assets under management, primarily through investments by AFORES.4

In May 2021, Sempra Energy, the California-based company with energy infrastructure investments in North America (including Mexico, through its subsidiary IEnova) conducted an exchange offer on the Mexican Stock Exchange for shares of IEnova. As a result of this US$1.8 billion deal, Sempra Energy now has its common stock listed on the Mexican Stock Exchange, trading as one of the few foreign issuers there.

In addition, the past few years have seen Mexico becoming a hub for fintech companies, in a country where much of the population has no formal access to banking and financial services. This trend has been supported by the 2018 enactment of the Mexican Fintech Law, the first statute of its kind in the region. It is likely that the technology sector, and fintech in particular, will drive IPO activity in Mexico in the years ahead.

Notwithstanding the recent track record, it makes sense to observe the geopolitical drivers in the region, which will accelerate or hamper IPO activity in coming years. Recent research of roughly 9,500 IPOs that occurred across 33 countries between 1995 and 2017 showed that IPO under-pricing is significantly more prevalent just before general elections.5 This under-pricing effect tends to be less pronounced in developed democracies that are characterized by effective corporate governance.6 It has also been shown that IPOs tend to be fewer in number during election years.7

General elections are scheduled to take place in Brazil and Costa Rica in 2022, as well as a presidential election in Colombia that year. General elections are also due to take place in November 2021 in Nicaragua and Chile, with a legislative election scheduled in Argentina during the same month, and a general election in Honduras in December. Venezuela is also scheduled to hold municipal elections in the coming months.

Political uncertainty can have a general depressing effect on IPOs for other reasons, too. If uncertainty causes the country's currency to weaken, that can lead to divestment—in turn making it more difficult to achieve successful IPOs. Similarly, if uncertainty causes interest rates to rise, stock markets will be negatively impacted and IPOs more challenging. In addition, if central banks curb liquidity, economic growth will be depressed.

The fact that Brazil's central bank felt it necessary to hike interest rates three times between February and June illustrates growing nervousness about Brazilian inflation, which reached 8 percent in May, and further interventions may occur.

More broadly, the uncertainties of the pandemic inevitably mean that further lockdown restrictions cannot be ruled out across Latin America. The World Health Organization (WHO) has warned that case numbers are once again surging in the region. However, dealmakers have rapidly evolved to overcome the logistical challenges posed by the pandemic, becoming adept at running IPO processes and roadshows virtually, without face-to-face engagement.

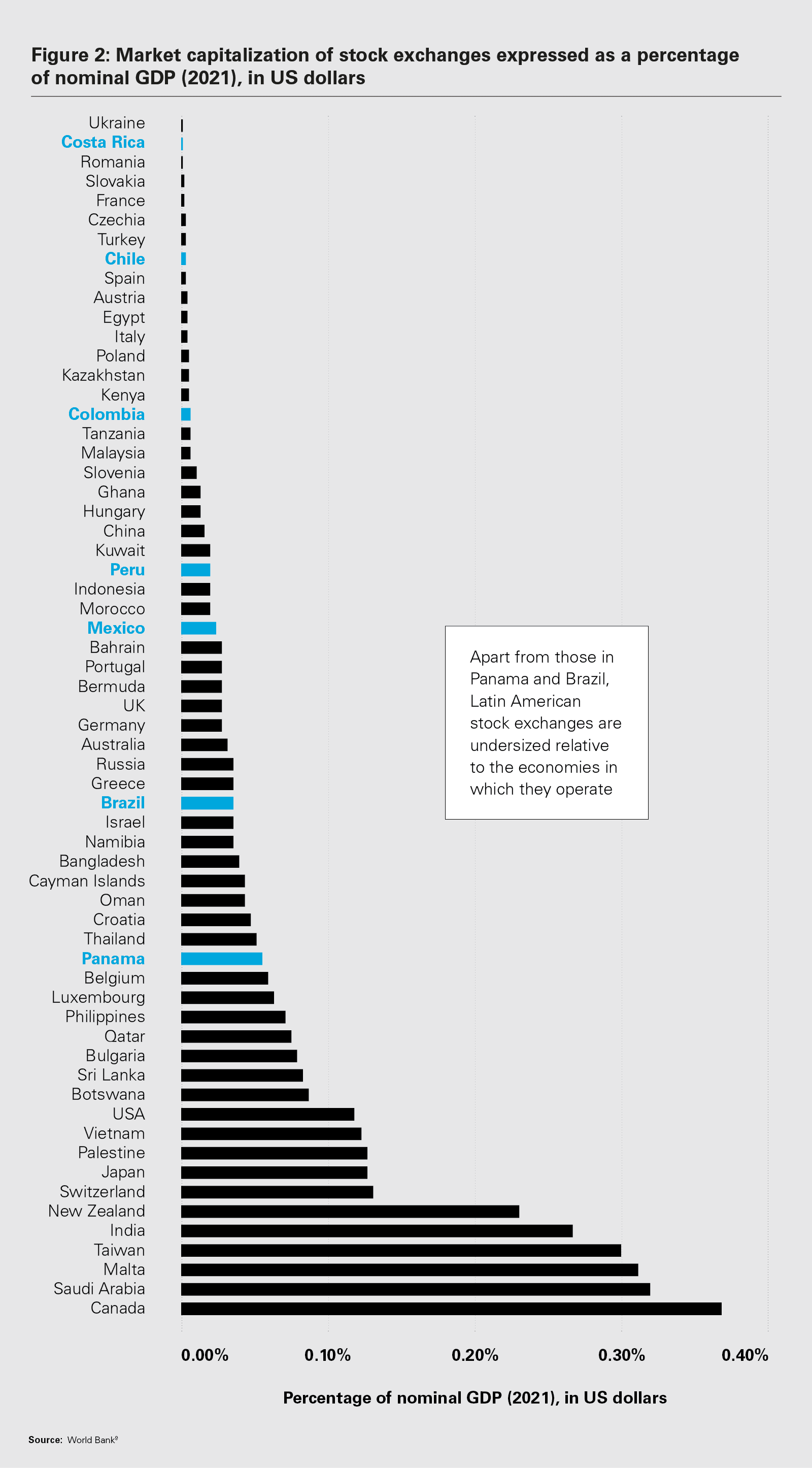

In general, though, the short-term factors in Latin America appear to make cautious optimism the most appropriate sentiment regarding the prospect for the flow of IPOs through the remainder of 2021 and into 2022. Equity capital markets (ECM) in Latin America are relatively small when compared to developed economies, indicating significant scope for growth as the region's economies mature. Figure 2 shows this clearly, comparing stock market capitalization to gross domestic product (GDP) in a range of countries worldwide.

Latin America's IPO bonanza over the past year or so is in line with the global equity capital markets generally. More than 6,100 equity capital markets offerings were brought to market globally during 2020, a 33 percent increase compared to a year ago and an all-time record. ECM activity totaled US$1.1 trillion during 2020, a 56 percent increase compared to a year ago and the strongest annual period for global ECM activity since records began in 1980.8

Despite institutional, geopolitical and other challenges to overcome, the outlook for ECM activity in Latin America—including further IPOs—appears bright.

1 World Bank (2021), World Economic Outlook: Latin America and the Caribbean.

2 International Monetary Fund (IMF) (2021), Short-Term Shot and Long-Term Healing for Latin America and the Caribbean, available at: https://blogs.imf.org/2021/04/15/short-term-shot-and-long-term-healing-for-latin-america-and-the-caribbean/.

3 Organisation for Economic Co-operation and Development (OECD) (2019), Equity Market Development in Latin America: Enhancing Access to Corporate Finance.

4 https://www.fundssociety.com/es/noticias/etf/cinco-afores-invierten-en-el-etf-esg-con-exposicion-a-mexico-de-blackrock

5 G. Marcato and C. Zheng (2021). Political Uncertainty and Cross-Country IPO Underpricing. Paper presented at the 2021 annual meeting of the European Financial Management Association, Leeds, England, June 30 – July 3, 2021.

6 H. N. Duong, A. Goyal, V. Kallinterakis and M. Veeraraghavan (2021), Democracy and the Pricing of Initial Public Offerings Around the World. Journal of Financial Economics, available at: https://doi.org/10.1016/j.jfineco.2021.07.010.

7 G. Çolak, A. Durnev and Y. Qian (2017), Political Uncertainty and IPO Activity: Evidence from U.S. Gubernatorial Elections. Cambridge University Press. Published online on December 4, 2017, available at: https://www.cambridge.org/core/journals/journal-of-financial-and-quantitative-analysis/article/political-uncertainty-and-ipo-activity-evidence-from-us-gubernatorial-elections/8F2EE62C6038B166F009987127269210

8 Refinitiv (2021), Global Equity Capital Markets Review 2020.

9 World Bank website, accessed on 19 September 19, 2021, available at: https://data.worldbank.org/indicator/CM.MKT.LCAP.GD.ZS?.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: Latin America IPO activity (deal count, value, market value 2015 – 2021 – Sept 1) (PDF)

View full image: Latin America IPO activity (deal count, value, market value 2015 – 2021 – Sept 1) (PDF)

View full image: Figure 2: Market capitalization of stock exchanges expressed as a percentage of nominal GDP (2021), in US dollars (PDF)

View full image: Figure 2: Market capitalization of stock exchanges expressed as a percentage of nominal GDP (2021), in US dollars (PDF)