Surging M&A surpasses expectations

All the stars aligned in 2021, creating a confident and exceptionally busy M&A market

Challenges loom—including the possibilities of tighter regulations, rising inflation and a stock market correction—but markets show little sign of slowing down

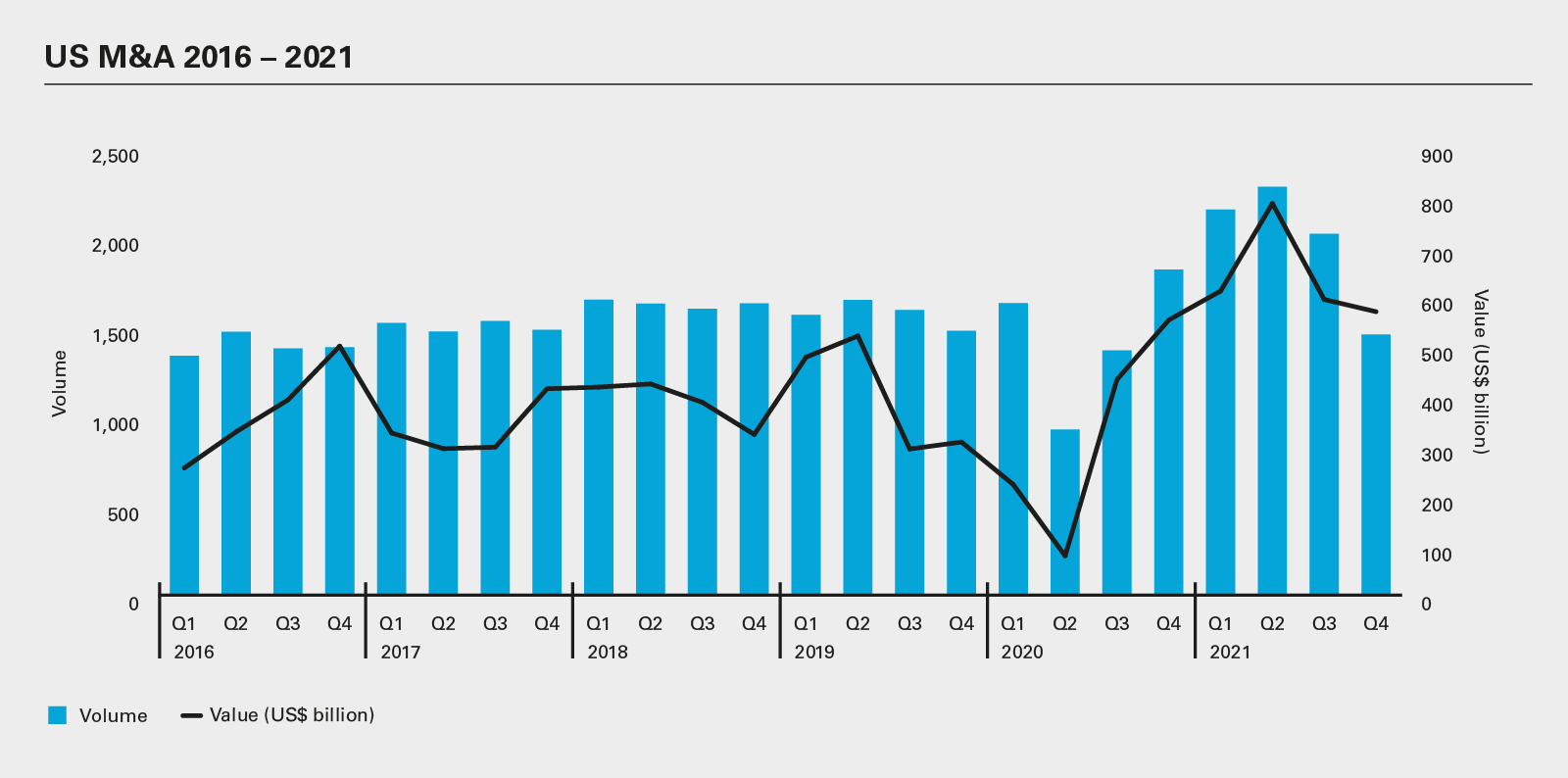

The value of US M&A blew past the US$2 trillion mark in 2021, ending the year more than 30 percent above the previous record set in 2015. US deal value reached US$2.6 trillion, twice the value of 2020, and volume set a new record at 7,896 transactions.

Confidence reigned among dealmakers as stock markets continued to rise; increasing numbers of SPACs sought merger targets; and private equity houses set new records, deploying some of the sector's historic levels of dry powder. All of which was underwritten by flexible and cheap debt financing.

Technology was a major driver of M&A, fueled by pandemic-related trends that continued to accelerate deployment of digital technologies across all sectors. The tech sector itself led the sector charts. Companies with product mixes boosted by the pandemic, including those in the pharma and healthcare sector, turned to M&A to complement and add to their existing business portfolios.

Despite a continuing positive outlook, dealmakers will need to keep potential risks in mind in 2022. Under the Biden administration, CFIUS went on a recruitment drive, and it will clearly continue to take a more aggressive stance across sectors, particularly when deals involve technology.

Indeed, regulatory scrutiny is tightening from a number of angles. The Securities and Exchange Commission under chair Gary Gensler is taking a tougher stance on enforcement and has its sights set on SPACs, cryptocurrencies and ESG. And the Federal Trade Commission has announced far-reaching antitrust policy changes that may require companies that reach settlements to observe a ten-year mandatory clearance period on new acquisitions and disposals—the new rules would even apply to buyers of affected assets.

This increasingly tough approach to regulating M&A has so far had little impact on dealmakers' appetites for transactions—although new rules may eventually render some deals less attractive.

In response to recent inflation, the Fed will increase interest rates, which could pose another challenge for dealmakers. But given that rates are so low by historical standards, increases are unlikely to have any direct significant effect on M&A for most of 2022.

One of the biggest questions is whether stock markets will continue to hold up. A correction seems inevitable at some point, but it's unclear what might trigger one in the foreseeable future. For example, markets seem to have shrugged off concerns related to the emergence of the Omicron variant of COVID-19—at least at the time of writing. And private equity still has a mountain of capital to deploy. Recent events, however, suggest that markets will be volatile.

As a result, although regulatory hurdles continue to multiply, we expect 2022 will be another strong year for US M&A, with robust activity through the first half and possibly well beyond.

All the stars aligned in 2021, creating a confident and exceptionally busy M&A market

Transaction values more than doubled year-on-year, as firms deployed ever-larger amounts of dry powder

Dynamics may be changing as the focus shifts to de-SPACs and regulatory scrutiny intensifies

In what was a stand-out year, M&A picked up the pace in almost every sector

Dealmaking may continue to rise, as price volatility abates and companies embrace energy transition

The pervasiveness of technology, particularly since the pandemic, continues to drive deals to all-time highs

Despite the absence of megadeals, M&A in the sector climbed from 2020 levels thanks in part to strong PE and SPAC activity

After dropping in 2020, real estate M&A ramped up significantly in 2021

The Federal Trade Commission is taking an increasingly stringent approach to antitrust investigations

Increased sector scope and concerns around a more aggressive approach to identifying non-notified transactions is leading to rising numbers of filings

Dealmakers should be braced for a more aggressive stance under Chair Gary Gensler

Borrower-friendly terms over the past few years have helped boost M&A totals—and a number of factors suggest the financing will not change dramatically in 2022

With data privacy laws tightening and cyberattacks on the rise, due diligence of technology networks and data processes should be a top priority for dealmakers

In the second half of 2021, Delaware courts issued several decisions affecting M&A dealmaking

Five factors that will shape dealmaking over the coming 12 months

All the stars aligned in 2021, creating a confident and exceptionally busy M&A market

Explore the data

M&A markets appeared to defy gravity through 2021. Globally, dealmakers were highly active, with values exceeding US$5 trillion for the first time ever. Total deal value rose by 81 percent on 2020 totals to US$5.75 trillion, with volumes rising 37 percent year-on-year to reach 26,060 deals.

And nowhere was busier than the US market. Surpassing all records, US dealmaking exceeded the US$2 trillion milestone for the first time, climbing to US$2.6 trillion—a massive 99 percent increase on 2020 total values. By volume, the US M&A market also smashed records, with 7,891 deals (versus the previous high of 6,497 transactions in 2018).

US $2.6

trillion

The value of US M&A deals in 2021—a 99% increase compared to 2020

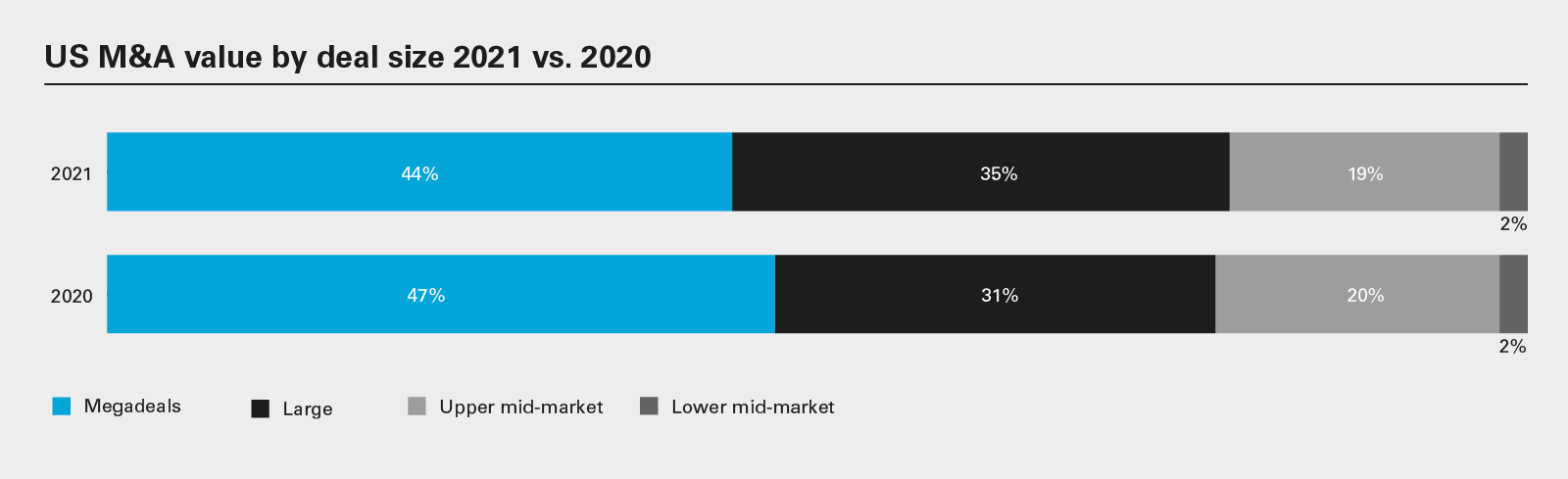

With stock markets trending higher through much of the year—the S&P 500 was up more than 26 percent for the year—public company financial firepower increased and dealmaker confidence ran high. Businesses seeking rapid growth and strategic shifts at a time of technological and societal change went on the hunt for large and potentially transformative deals to achieve these aims. Megadeals of US$5 billion or more accounted for nearly half of all US M&A.

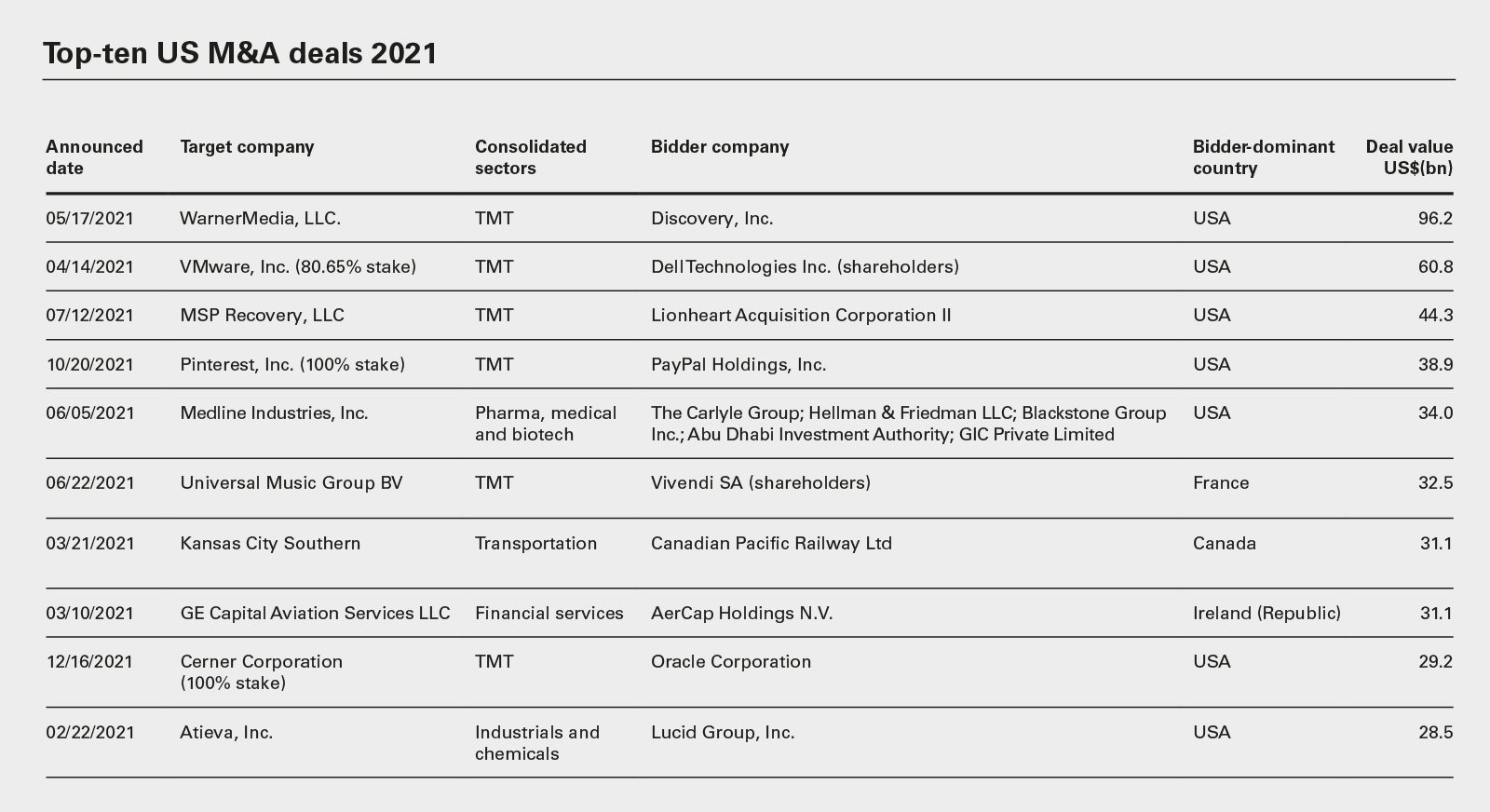

And it wasn't just the public markets pushing up M&A numbers. Private equity activity was highly active in 2021, with deal value reaching US$987.8 billion—more than double the previous year's total of US$474.5 billion. Volume over this period rose by 59 percent to 3,460 transactions. With strong fundraising totals in 2020—even despite a brief COVID-induced lull—and a continuation of that trend through 2021, dry powder extended its climb, reaching US$2.3 trillion in August 2021, according to S&P Global. Combined with the ready availability of low-cost debt financing, private equity firms had significant capital at their disposal to close deals. The fifth-largest deal of the year, valued at US$34 billion, was a private equity consortium that saw The Carlyle Group, Hellman & Friedman, Blackstone Group, Abu Dhabi Investment Authority and GIC acquire Medline.

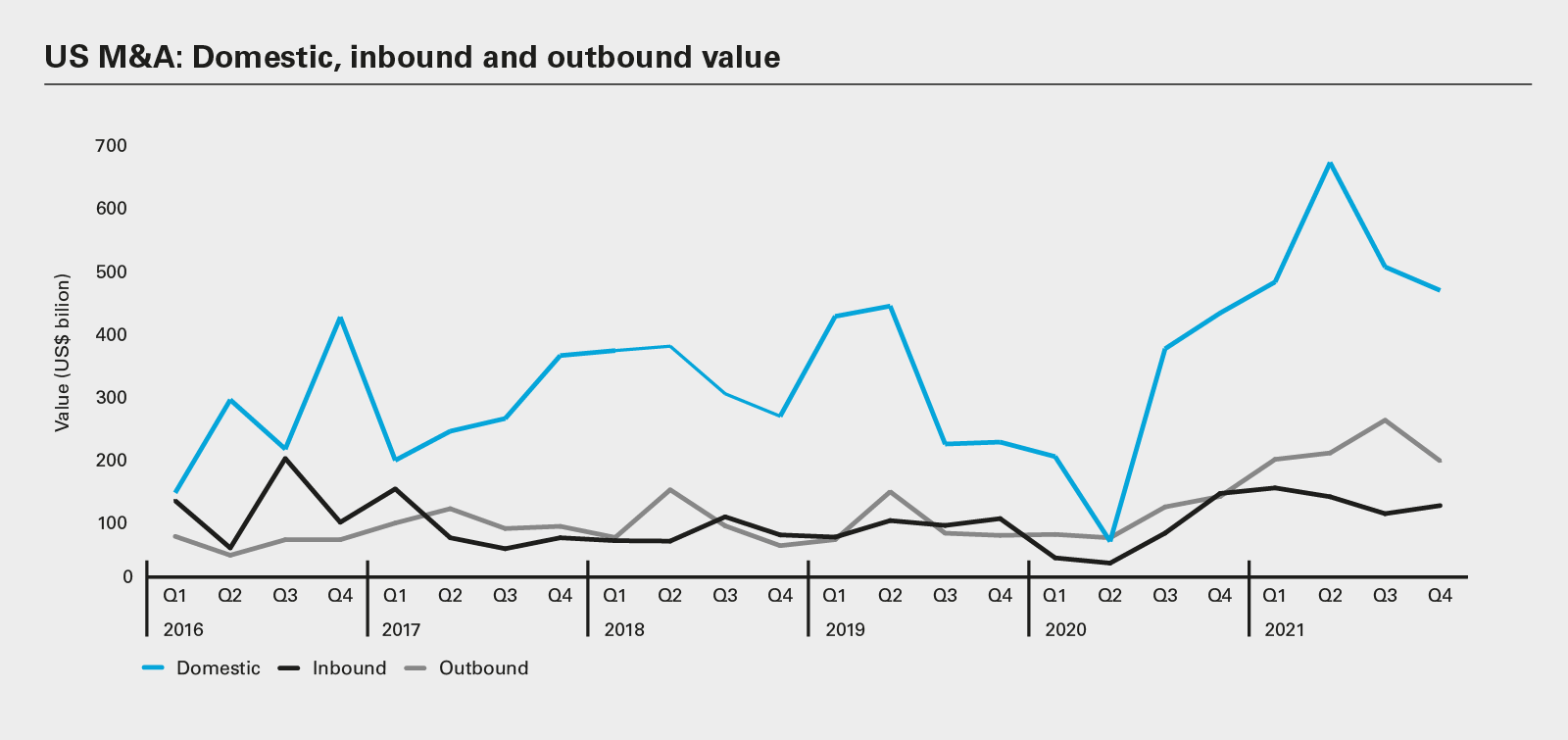

Domestic transactions were particularly buoyant and accounted for much of the spectacular rise in activity. Totaling US$2.1 trillion, US-to-US transactions rose by 102 percent in 2021 versus the previous year.

The surge in domestic activity is partly the result of supply chain issues and the increased regulatory scrutiny of cross-border transactions. Since COVID-19 disrupted the production and flow of goods around the world, companies have begun to bring supply sources closer to home, boosting M&A in the process.

Rising concerns about the national security implications of deals involving data and other sensitive assets have also placed some roadblocks in the way of overseas investments. With the US taking a stronger stance on deals involving certain jurisdictions, getting some deals over the line has been challenging. At the same time, other countries in Europe and Asia-Pacific are also looking much more closely at overseas investments, potentially stemming the flow of cross-border deals overall.

However, even with a more cautious approach to cross-border deals, 2021 saw both inbound and outbound M&A increase. The value of US transactions involving overseas buyers rose by 90 percent over 2020 figures to US$483 billion, and those involving US buyers of foreign assets increased to US$817.8 billion—a 121 percent increase on the previous year.

In a bid to finance certain spending on social, infrastructure and other initiatives, President Joe Biden has been trying to reform the US tax code, including initial proposals that would raise the corporate income tax rate and change capital gains and individual tax rates.

The proposed tax reforms were subject to significant changes throughout 2021. Proposals have included increasing the corporate tax rate to 28 percent from its current level of 21 percent and increasing the highest marginal capital gains tax rate to 25 percent. In addition, a proposal was put forth to charge corporations with average financial statement income in excess of US$1 billion with an alternative minimum tax of 15 percent.

Some of the proposals may have impacted the timing of M&A activity, as dealmakers attempted to get deals over the line before the end of the year to lock in their tax liability at the current rates, particularly since the proposals include the possibility of retroactive application of new tax rates. Some dealmakers have taken out tax insurance to cover this risk.

There had also been some discussion of whether the reforms would cover the preferential tax treatment for carried interest payments, which would primarily affect private equity sponsors. The current rules, enacted as part of the Tax Cuts and Jobs Act of 2017, generally require that investments be held for at least three years for the related carried interest to qualify for favorable tax rates. At one point, there was a proposal to increase the holding period to five years, although this proposal was removed from the latest version of the bill.

Structural changes

Tax reforms would be most likely to affect deal structuring, share buybacks and cross-border investments. The decrease in the corporate tax rate as part of the tax cuts under the Trump administration made corporate holding structures more attractive. Conversely, increasing the corporate tax rate could cause a shift to pass-through investments and holding structures.

The latest version of the bill also included proposals to levy a 1 percent tax on the value of share buybacks to encourage company investment rather than distributing excess cash to shareholders. Should this be included in future versions of the bill, it could reduce the level of buybacks seen in the aftermath of the 2017 tax cuts.

And finally, a key aim of the proposed reforms is to increase taxes on profits earned by US companies overseas. If enacted, these may well have an impact on decisions as to where to locate certain assets, acquisition holding structures, and the amount and timing of repatriations of cash to the US, among other things.

The M&A market is exceptionally buoyant, with activity driven by the combination of high levels of private equity cash, strong stock markets, significant numbers of SPACs looking for deals and a healthy debt market. Tax changes—whatever shape they may take—are unlikely to dampen dealmaking appetite to any great degree, although they may have a marginal effect on deal timings and on structures employed in M&A transactions.

Technology was by far the most active sector by value, chalking up US$790 billion worth of transactions, an increase of 133 percent on an already busy 2020, while volumes also rose, by 69 percent, to 2,194 deals.

The surge in US tech M&A is partly due to the strong technology base in the US. Technology assets are hotter than ever, as businesses rapidly digitalize their operations and deploy technologies such as machine learning and artificial intelligence, particularly since the pandemic.

Appetite for media and entertainment assets also surged due to the pandemic. Indeed, the biggest deal of the year hailed from the sector: the US$96.2 billion WarnerMedia and Discovery tie-up. This megadeal helped media M&A surge by 744 percent to US$182.9 billion compared to the previous year. Volume in the sector ticked up by 35 percent over the same period.

As we move into 2022, the signs are that many of the factors underpinning strong M&A markets are set to endure. The emergence of the highly transmissible Omicron variant of COVID-19 may cause some stock market volatility in the short term, while rising inflation and the prospect of interest rate rises are also potential risks. However, should these risks materialize, their effects will take some time to filter through to M&A activity. Absent a major shock, we anticipate continued robust M&A activity, at least through the first half of 2022.

The pandemic forced dealmakers to run M&A processes differently. How much of this will stick? And how will this affect M&A infrastructure?

The pandemic has shown just how resilient dealmaking infrastructure really is. While there was clearly a lull in M&A activity in the first half of 2020, as businesses got their staff working remotely and stabilized finances where necessary, deal numbers and values have been on a roll since.

New COVID-19 variants could trigger restrictions once more, but even without this, the M&A process seems to have changed forever. Indeed, some of the work practices put in place when people were ordered to stay home turned out to be far more efficient versus the status quo. Management and bidder meetings no longer have to be face-to-face every time. At least part of the roadshow can be done online via video meetings, and staff working on deals can collaborate with colleagues and clients remotely.

It seems likely that at least some remote working will continue to feature in the market, including among the advisory and investment banking community. This may mean less office space is needed, which would reduce overheads. It may also mean advisors can hire globally, at least for some jobs, attracting talent without necessarily requiring relocations. And deal teams may often be able to close deals from home, cutting down the number of late nights in the office. There are plenty of positives to the new working environment.

Meeting people in the flesh, however, is still important, given that M&A is built on trust and relationships. But as the past two years have demonstrated, in-person interaction is not always essential. It turns out that dealmaking infrastructure is more flexible than anyone imagined just a few years ago.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: US M&A 2016 – 2021 (PDF)

View full image: US M&A 2016 – 2021 (PDF)

View full image: US M&A: Domestic, inbound and outbound value (PDF)

View full image: US M&A: Domestic, inbound and outbound value (PDF)

View full image: US M&A value by deal size 2021 vs. 2020 (PDF)

View full image: US M&A value by deal size 2021 vs. 2020 (PDF)

View full image: Top-ten US M&A deals 2021 (PDF)

View full image: Top-ten US M&A deals 2021 (PDF)