Surging M&A surpasses expectations

All the stars aligned in 2021, creating a confident and exceptionally busy M&A market

Challenges loom—including the possibilities of tighter regulations, rising inflation and a stock market correction—but markets show little sign of slowing down

The value of US M&A blew past the US$2 trillion mark in 2021, ending the year more than 30 percent above the previous record set in 2015. US deal value reached US$2.6 trillion, twice the value of 2020, and volume set a new record at 7,896 transactions.

Confidence reigned among dealmakers as stock markets continued to rise; increasing numbers of SPACs sought merger targets; and private equity houses set new records, deploying some of the sector's historic levels of dry powder. All of which was underwritten by flexible and cheap debt financing.

Technology was a major driver of M&A, fueled by pandemic-related trends that continued to accelerate deployment of digital technologies across all sectors. The tech sector itself led the sector charts. Companies with product mixes boosted by the pandemic, including those in the pharma and healthcare sector, turned to M&A to complement and add to their existing business portfolios.

Despite a continuing positive outlook, dealmakers will need to keep potential risks in mind in 2022. Under the Biden administration, CFIUS went on a recruitment drive, and it will clearly continue to take a more aggressive stance across sectors, particularly when deals involve technology.

Indeed, regulatory scrutiny is tightening from a number of angles. The Securities and Exchange Commission under chair Gary Gensler is taking a tougher stance on enforcement and has its sights set on SPACs, cryptocurrencies and ESG. And the Federal Trade Commission has announced far-reaching antitrust policy changes that may require companies that reach settlements to observe a ten-year mandatory clearance period on new acquisitions and disposals—the new rules would even apply to buyers of affected assets.

This increasingly tough approach to regulating M&A has so far had little impact on dealmakers' appetites for transactions—although new rules may eventually render some deals less attractive.

In response to recent inflation, the Fed will increase interest rates, which could pose another challenge for dealmakers. But given that rates are so low by historical standards, increases are unlikely to have any direct significant effect on M&A for most of 2022.

One of the biggest questions is whether stock markets will continue to hold up. A correction seems inevitable at some point, but it's unclear what might trigger one in the foreseeable future. For example, markets seem to have shrugged off concerns related to the emergence of the Omicron variant of COVID-19—at least at the time of writing. And private equity still has a mountain of capital to deploy. Recent events, however, suggest that markets will be volatile.

As a result, although regulatory hurdles continue to multiply, we expect 2022 will be another strong year for US M&A, with robust activity through the first half and possibly well beyond.

All the stars aligned in 2021, creating a confident and exceptionally busy M&A market

Transaction values more than doubled year-on-year, as firms deployed ever-larger amounts of dry powder

Dynamics may be changing as the focus shifts to de-SPACs and regulatory scrutiny intensifies

In what was a stand-out year, M&A picked up the pace in almost every sector

Dealmaking may continue to rise, as price volatility abates and companies embrace energy transition

The pervasiveness of technology, particularly since the pandemic, continues to drive deals to all-time highs

Despite the absence of megadeals, M&A in the sector climbed from 2020 levels thanks in part to strong PE and SPAC activity

After dropping in 2020, real estate M&A ramped up significantly in 2021

The Federal Trade Commission is taking an increasingly stringent approach to antitrust investigations

Increased sector scope and concerns around a more aggressive approach to identifying non-notified transactions is leading to rising numbers of filings

Dealmakers should be braced for a more aggressive stance under Chair Gary Gensler

Borrower-friendly terms over the past few years have helped boost M&A totals—and a number of factors suggest the financing will not change dramatically in 2022

With data privacy laws tightening and cyberattacks on the rise, due diligence of technology networks and data processes should be a top priority for dealmakers

In the second half of 2021, Delaware courts issued several decisions affecting M&A dealmaking

Five factors that will shape dealmaking over the coming 12 months

The Federal Trade Commission is taking an increasingly stringent approach to antitrust investigations

Stay current on global M&A activity

Explore the data

Create custom charts using the latest data on global M&A

View data on merger control notifications in more than 55 jurisdiction

WAMS: White & Case Antitrust Merger StatPak

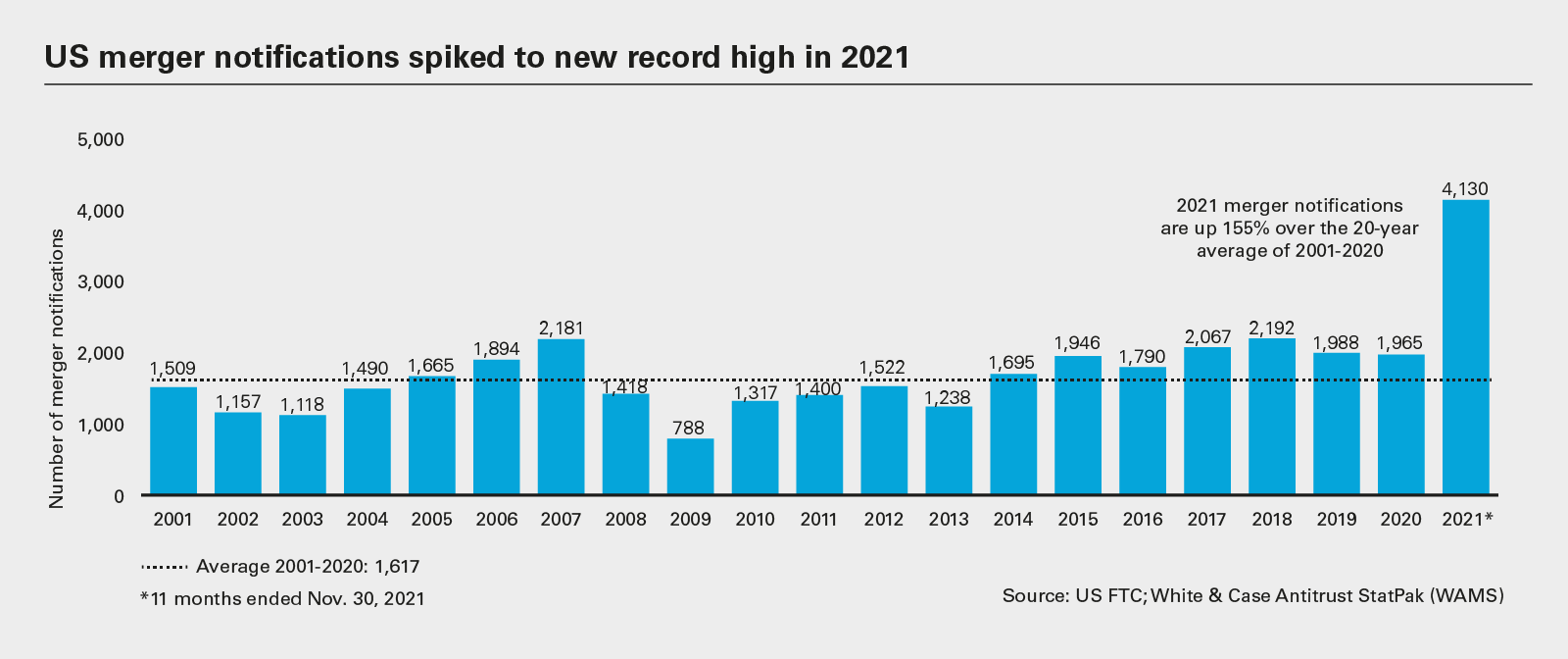

The Federal Trade Commission (FTC) was busy in its first year under the Biden administration. Over the past year, the FTC announced several important policy and process changes that may have significant implications for US M&A, and dealmakers should be prepared for far more scrutiny around antitrust issues—and longer review periods as well.

The first shift began in February 2021 when the FTC announced a temporary suspension of the early termination process under the HSR (Hart-Scott-Rodino Antitrust Act) waiting period. While early termination was never guaranteed on any particular deal, that process allowed deals without competitive concerns to be cleared within approximately ten to 15 days. Now, all deals are subject to the initial 30-day waiting period. There is little evidence that this temporary suspension will be removed any time soon, and the practical result is that dealmakers are making their HSR filings at an earlier stage—sometimes based on letters of intent or term sheets—to kick-start the waiting period.

Faced with a significant rise in filings (see chart), the FTC also announced that it may send "warning letters" to companies when the FTC is unable to complete investigations within the 30-day HSR period, or even at the end of an investigation following substantial compliance with a second request.

These co-called "pre-consummation warning letters" advise merging parties that, while they can legally proceed with the transaction, they do so "at their own risk" because the FTC's investigation is ongoing. The FTC also announced that these warning letters could be sent on the basis of not just competition or consumer welfare concerns, but rather on an extended scope of issues, including where it perceives that a merger may harm workers or "honest business."

It is unclear at this stage how much risk these warning letters actually pose to closed transactions, but we are watching closely to see how substantive they prove to be and the extent to which the FTC or DOJ challenge completed mergers.

These letters have so far had little effect on deal closings, although it is possible that more cautious buyers may reconsider their involvement in a deal if it triggers a warning letter with a plausible risk of a meaningful investigation (and subject to agreement covenants).

The FTC has also reinvigorated a policy requiring companies that have entered into a consent agreement to obtain the FTC's prior approval before pursuing a future transaction in a directly or indirectly affected market. This reverses a policy change made in 1995 and could have far-reaching implications for a company's future acquisitions. Yet the biggest impact is likely to be on divestitures because, not only would the FTC need to approve the deal, but the buyer of the business would also become subject to the 10-year prior notice and approval period. This could narrow the universe of buyers for a business, since a divestiture buyer must be willing to commit to a prior approval process for unknown, future transactions.

While a PE buyer often presents no directly competitive issues in any particular transaction, in January 2022, PE was highlighted in a joint agency public inquiry. As part of the FTC and DOJ's planned revamping of their Merger Guidelines, the internal standards by which they review the competitive effects of transactions, the agencies are polling the public to see if stronger enforcement measures against PE firms should be taken.

Underlying this inquiry, the FTC Chair has expressed a focus on "rollup plays" by PE buyers, i.e., when a firm acquires several small players to combine them later, but the initial investments are not HSR reportable, thus potentially flying under the government's radar.

The FTC is not the only agency signalling an aggressive enforcement stance. On January 24, 2022, the DOJ Assistant Attorney General remarked that in most situations, the agency should seek an injunction to block the transaction, rather than negotiating a remedy with the parties to fix the issue. The Assistant AG also criticized the use of "partial divestitures" (i.e., buying less than what the agency considers a full-functioning business unit) as effective at maintaining competition.

Overall, the agencies' more aggressive stance on antitrust means that dealmakers will need to factor in longer timelines and the potential for agency involvement or investigations post-transaction. As recently as January 24, 2022, the FTC Chair asked Congress to consider an increase in funding, an increase in HSR filing fees, and additional time beyond the 30-day window to review deals. Further, the agency's policy changes have not so far had a major impact—if any—on M&A activity, though they may change the structure and scope of some deals. One potential future development, as a result of the 10-year prior notice and approval period, may be that parties consider a "fix-it first" option with assets carved out of a business before a transaction is filed, to limit the FTC's oversight of the transaction in its entirety. It also remains to be seen whether parties in front of the DOJ will have less success in negotiating remedies, and instead should prepare for an increased possibility of litigation.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

US merger notifications spiked to new record high in 2021 (PDF)

US merger notifications spiked to new record high in 2021 (PDF)