Borrowers and lenders are seeking new opportunities in the face of growing market volatility

Foreword

After cresting record levels of activity last year, US leveraged finance markets slowed in the first half of 2022 as lenders and borrowers adapted to a rapidly shifting geopolitical and macro-economic backdrop—deals continued to be done, but stakeholders reset expectations as debt costs rose and investors became increasingly risk-averse.

US leveraged loan markets are in a very different place than they were just six months ago.

Since the beginning of the year, lenders and borrowers have been forced to contend with soaring inflation, rising interest rates, supply chain constraints and an increasingly volatile geopolitical backdrop following events in Ukraine. The contrast with the frenetic levels of activity observed in 2021—characterized by abundant capital, low pricing and buoyant refinancing—is stark.

Macro-economic headwinds took their toll on activity levels. Leveraged loan issuance dropped by a fifth year-on-year in the first half of 2022. The impact was even more pronounced in the institutional loan issuance space, which was down by almost two-thirds on the same period in 2021, as increasingly risk-averse investors tapped the brakes. Some issuers that would have otherwise dipped their toes into leveraged loan markets opted to hold fire instead and await calmer waters.

In the face of these challenges, however, there have been positives. Cash-rich private equity firms continue to close deals and secure financing, cushioning the dip in year-on-year new money issuance. Loan issuance intended for buyouts, while suffering some decline, has also proven resilient. Collateralized loan obligations (CLOs)—the largest investors in leveraged loan assets—have also remained active, even as supply in the primary loan market dried up.

Even as markets take a moment to pause and recalibrate, the door remains open for issuers to secure financing on good terms from debt investors who are eager to put funds to work.

High yield, high costs

For high yield bonds, various headwinds, including rising inflation and interest rates, created a challenging market landscape for fixed rate instruments in the first half of the year. High yield bond issuance dropped to levels not seen since the start of the pandemic, falling by more than three-quarters year-on-year as cautious investors stepped back. According to Lipper funds data, in the first half of 2022, almost US$30 billion left the asset class.

Even in the face of volatile market conditions, stronger high yield issuers have kept a close eye on pockets of opportunities. More than a dozen others have joined the fray since, capitalizing on an improved landscape in June to bring new deals to market. These include Tenet Healthcare, which raised US$2 billion in senior secured notes, and Kinetik Holdings, which priced US$1 billion in senior unsecured notes. Both issuers raised the capital for refinancing.

As we enter the second half of the year, volatility is likely to continue weighing on the market, but investors and borrowers are already adjusting. Activity levels may not hit the buoyant highs of a year ago, but stronger credits should continue to secure investor support. There is no escaping the fact that costs have gone up for issuers accessing the more challenging markets, but patience, adaptability and nimble execution continue to be a successful formula when doing so.

Resilient US leveraged finance markets navigate volatile backdrop

Leveraged loan issuance reached US$612.5 billion in H1 2022, down on the US$755.5 billion recorded in the same period in 2021

High yield bond issuance also dropped, year-on-year, from US$267.6 billion to US$63.6 billion—though markets began to open again in June

Since January, the US Federal Reserve has raised interest rates four times, taking the benchmark federal-funds rate to a range between 2.25 and 2.5 percent

A volatile situation: Europe versus the United States

Leveraged loan issuance in the US dropped by 19 percent year-on-year in H1 2022

High yield bond activity in the US was down 76 percent year-on-year during the same period, hit by inflation and rising interest rates

Combined leveraged loan and high yield bond issuance in Western and Southern Europe was down more than 65 percent year-on-year, as events in Ukraine hit the markets

Pricing is moving in favor of lenders across the board

Taking stock at this point in the year may make for slightly sobering reading for some, but the cyclical nature of the market means that, even as activity slows in one area, it can (and usually does) pick up in another—but what does this mean for leveraged finance markets in the months ahead?

Lender appetite for US buyout opportunities remained resilient in the first half of 2022 despite a volatile macro-economic backdrop and a decline in activity across the wider leveraged finance market.

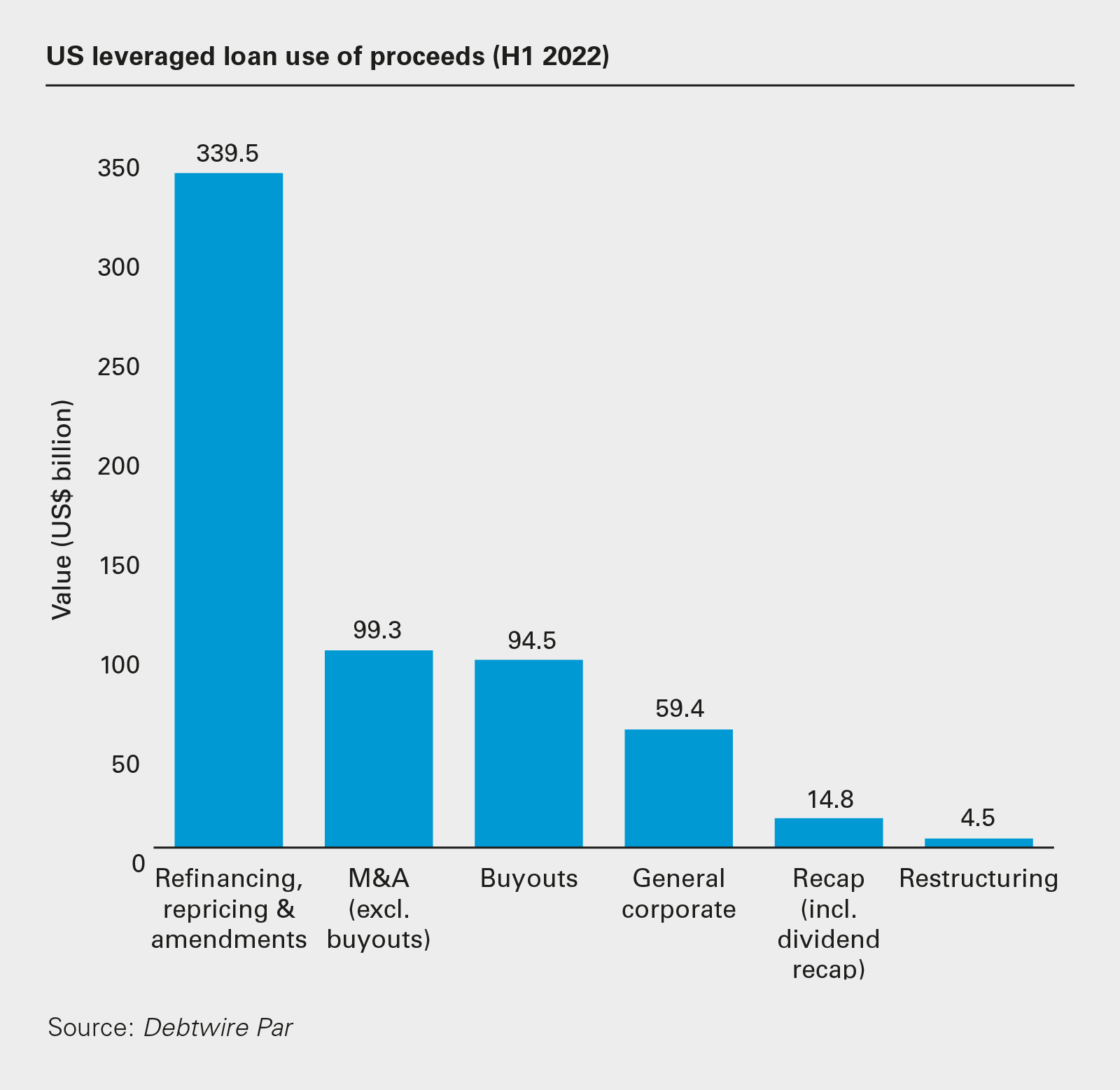

Loan issuance for buyouts came in at US$94.5 billion in H1 2022, up from the US$79 billion secured in what was already considered a red-hot market in H1 2021.

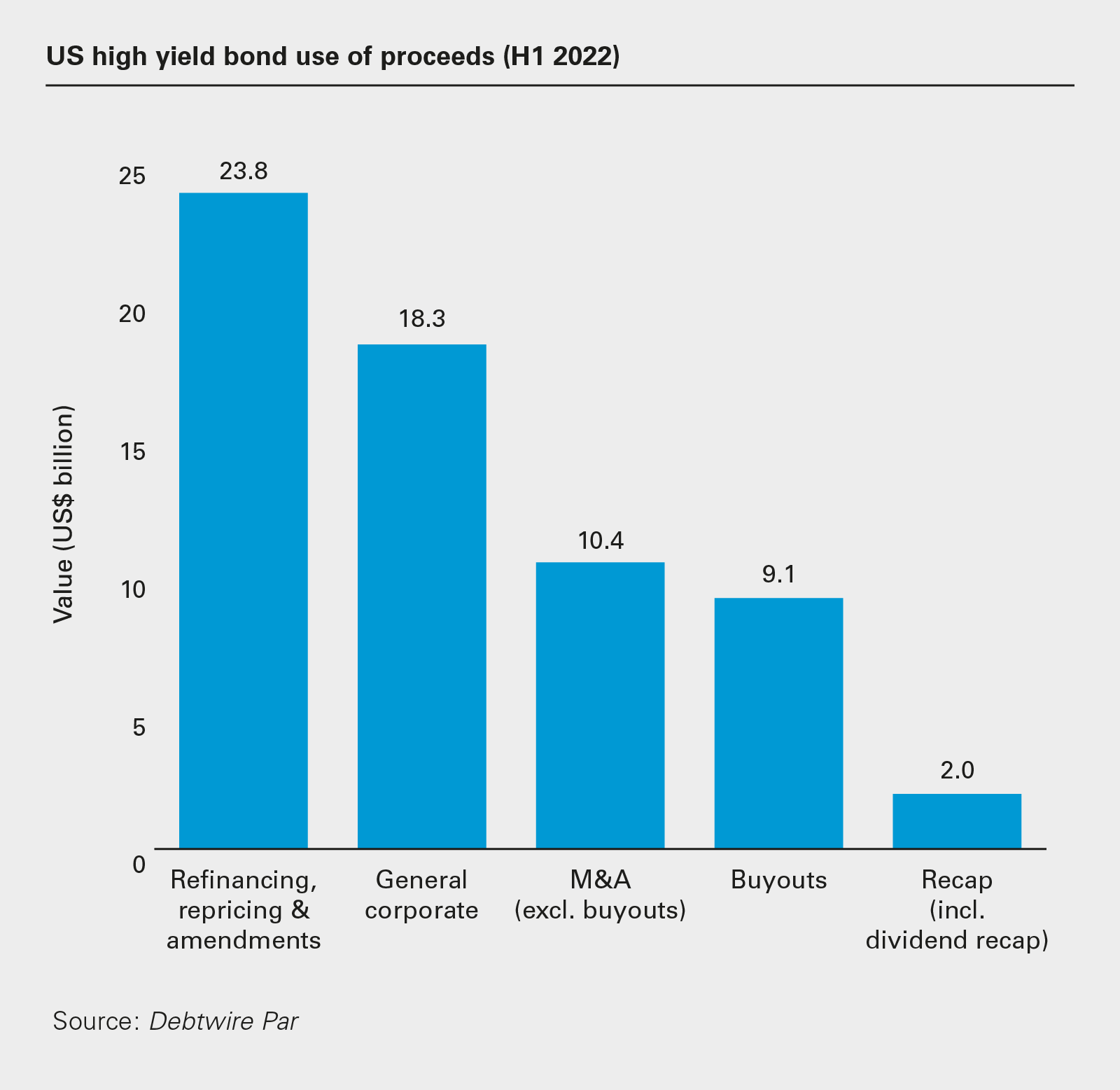

The high yield bond space did not fare quite as well, as inflation and climbing interest rates pushed many investors to find safer alternatives. After a very strong first quarter, in which there was US$7.4 billion in high yield bond buyout issuance—up more than 80 percent, year-on-year—the second quarter saw just US$1.7 billion in additional issuance for these purposes.

Despite a tougher market, buyout deals of significant scale were completed in the first half of 2022. In February, 3G Capital priced a US$5.36 billion-equivalent loan package to fund its buyout of window coverings manufacturer Hunter Douglas.

That same month, government contractor Amentum progressed with a US$2.26 billion term loan facility to finance its purchase of fellow contractor PAE from Platinum Equity and the Gores Group.

Market looks for direction

20%

Loan issuance for buyouts reached US$94.5 billion in H1 2022, up 20 percent year-on-year

Loan and bond issuance linked to buyouts, however, has not been immune to market uncertainty sparked by events in Ukraine and rising inflation and interest rates. While buyout issuance figures recorded in the first half of 2022 look good, they benefited from a pipeline of deals launched in 2021 that closed in the first three months of 2022.

As geopolitical and macro-economic risk intensified, however, getting buyout debt packages over the line has become more challenging. Underwriting banks and institutional investors, as a whole, have taken a somewhat more conservative stance on funding highly leveraged, sub-investment-grade buyout credits.

Leveraged loan and high yield investors, meanwhile, are asking for higher pricing and wider original issue discounts (OIDs) to gain the necessary comfort against a shifting risk backdrop.

According to Debtwire Par, both average OIDs and loan margins have widened materially since the start of the year, and this pricing pressure can be seen in several deals that have closed in the first half of the year. For example, Syniverse Technologies completed a US$1.025 billion term loan B (TLB) to refinance debt in connection with the company's minority stake acquisition by Twilio. The TLB, due in 2027, priced at SOFR + 700 bps, up from initial guidance of SOFR + 500–525 bps.

Lightstone Generation completed an amend and extend of its US$1.463 billion TLB, pricing the TLB at SOFR + 575 bps—up 200 bps on the existing loans, which priced at LIBOR + 375 bps in 2018.

According to Bain & Co., private equity dry powder still sits at record levels, compelling buyout firms to maintain deployment. This has sustained buyout deal volumes even as wider M&A markets have cooled and may well drive additional buyout issuance in H2 2022 if financing sources come to the table.

While M&A deal value in the US, excluding buyouts, slid by more than 20 percent in H1 2022, year-on-year, buyouts worth US$235 billion were announced during the same period, according to Mergermarket—still far above pre-pandemic levels going back to 2007.

Even though leveraged finance markets have cooled, investors remain on the lookout for high-quality credits backed by familiar sponsors. Deals can still be financed, but the quality bar is higher, and financing is likely to be pricier.

The most significant shift in buyout deal financing since the start of the year, however, has been the growing prominence of direct lenders on deals of increasing scale.

Direct lending's roots lie in smaller, mid-market deals and packages characterized by higher pricing and tighter covenant packages. For jumbo deals, sponsors historically would almost always default to cheaper, more liquid leveraged loan and high yield bond markets, which also offered looser covenants.

In the past couple of years, however, the direct lending option has become increasingly compelling for financial sponsors in a volatile market, and this trend has accelerated in 2022.

Unlike leveraged finance markets, where banks underwrite loans and then sell down tranches to investors, direct lenders underwrite and hold credits. For sponsors, this removes syndication risk and delay, with direct lenders providing greater certainty of execution and terms.

Sponsors have also noted that the gap in pricing between the two products has narrowed. Direct lenders may ask for a higher price up front but, once OID and price flex in syndication are factored in, the gap in pricing is often minimal, with many sponsors finding that any direct lending premium is worth paying to remove syndication risk.

Direct lenders have also grown their assets under management in the past decade. With Preqin putting private debt dry powder above US$1 trillion (up from US$400 billion in 2008), these lenders have more firepower at their disposal and are capable of digesting much bigger credits.

It has become increasingly common for financial sponsors to run dual-track processes looking at both leveraged loan and bond options alongside what direct lenders can offer.

In some cases, buyout firms are bypassing syndicated loan and high yield bond markets altogether. In 2021, Thoma Bravo financed 16 of its 19 buyouts with direct lenders, according to Reuters. It secured a US$2.6 billion debt financing deal in March from a club of direct lenders, including Owl Rock Capital, Apollo Global Management, Golub Capital and Blackstone Credit, to fund its US$10.7 billion buyout of Bay Area software company Anaplan.

Direct lenders have also become more comfortable with providing financing on looser, more flexible terms tailored to borrower requirements for bigger deals. Sponsors pursuing buy-and-build strategies, for example, can turn to direct lenders for delayed draw term loans that allow borrowers to draw down cash over a long hold period to fund add-on acquisitions.

Despite a volatile and uncertain market, financial sponsors are finding that they still have several options available when it comes to funding deals.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: US leveraged loan use of proceeds (H1 2022) (PDF)

View full image: US leveraged loan use of proceeds (H1 2022) (PDF)

View full image "US high yield bond use of proceeds (H1 2022)" PDF

View full image "US high yield bond use of proceeds (H1 2022)" PDF