Borrowers and lenders are seeking new opportunities in the face of growing market volatility

Foreword

After cresting record levels of activity last year, US leveraged finance markets slowed in the first half of 2022 as lenders and borrowers adapted to a rapidly shifting geopolitical and macro-economic backdrop—deals continued to be done, but stakeholders reset expectations as debt costs rose and investors became increasingly risk-averse.

US leveraged loan markets are in a very different place than they were just six months ago.

Since the beginning of the year, lenders and borrowers have been forced to contend with soaring inflation, rising interest rates, supply chain constraints and an increasingly volatile geopolitical backdrop following events in Ukraine. The contrast with the frenetic levels of activity observed in 2021—characterized by abundant capital, low pricing and buoyant refinancing—is stark.

Macro-economic headwinds took their toll on activity levels. Leveraged loan issuance dropped by a fifth year-on-year in the first half of 2022. The impact was even more pronounced in the institutional loan issuance space, which was down by almost two-thirds on the same period in 2021, as increasingly risk-averse investors tapped the brakes. Some issuers that would have otherwise dipped their toes into leveraged loan markets opted to hold fire instead and await calmer waters.

In the face of these challenges, however, there have been positives. Cash-rich private equity firms continue to close deals and secure financing, cushioning the dip in year-on-year new money issuance. Loan issuance intended for buyouts, while suffering some decline, has also proven resilient. Collateralized loan obligations (CLOs)—the largest investors in leveraged loan assets—have also remained active, even as supply in the primary loan market dried up.

Even as markets take a moment to pause and recalibrate, the door remains open for issuers to secure financing on good terms from debt investors who are eager to put funds to work.

High yield, high costs

For high yield bonds, various headwinds, including rising inflation and interest rates, created a challenging market landscape for fixed rate instruments in the first half of the year. High yield bond issuance dropped to levels not seen since the start of the pandemic, falling by more than three-quarters year-on-year as cautious investors stepped back. According to Lipper funds data, in the first half of 2022, almost US$30 billion left the asset class.

Even in the face of volatile market conditions, stronger high yield issuers have kept a close eye on pockets of opportunities. More than a dozen others have joined the fray since, capitalizing on an improved landscape in June to bring new deals to market. These include Tenet Healthcare, which raised US$2 billion in senior secured notes, and Kinetik Holdings, which priced US$1 billion in senior unsecured notes. Both issuers raised the capital for refinancing.

As we enter the second half of the year, volatility is likely to continue weighing on the market, but investors and borrowers are already adjusting. Activity levels may not hit the buoyant highs of a year ago, but stronger credits should continue to secure investor support. There is no escaping the fact that costs have gone up for issuers accessing the more challenging markets, but patience, adaptability and nimble execution continue to be a successful formula when doing so.

Resilient US leveraged finance markets navigate volatile backdrop

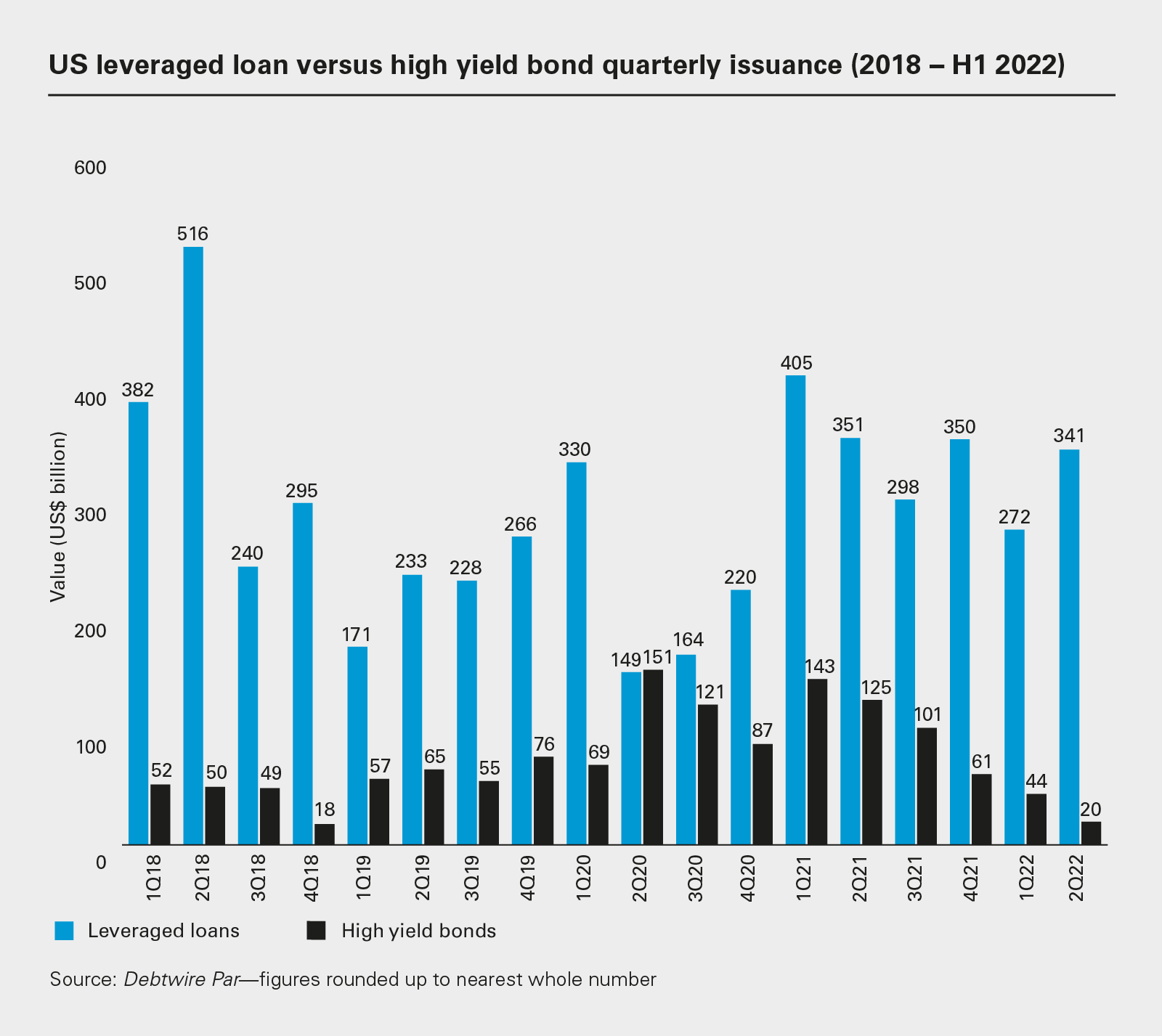

Leveraged loan issuance reached US$612.5 billion in H1 2022, down on the US$755.5 billion recorded in the same period in 2021

High yield bond issuance also dropped, year-on-year, from US$267.6 billion to US$63.6 billion—though markets began to open again in June

Since January, the US Federal Reserve has raised interest rates four times, taking the benchmark federal-funds rate to a range between 2.25 and 2.5 percent

A volatile situation: Europe versus the United States

Leveraged loan issuance in the US dropped by 19 percent year-on-year in H1 2022

High yield bond activity in the US was down 76 percent year-on-year during the same period, hit by inflation and rising interest rates

Combined leveraged loan and high yield bond issuance in Western and Southern Europe was down more than 65 percent year-on-year, as events in Ukraine hit the markets

Pricing is moving in favor of lenders across the board

Taking stock at this point in the year may make for slightly sobering reading for some, but the cyclical nature of the market means that, even as activity slows in one area, it can (and usually does) pick up in another—but what does this mean for leveraged finance markets in the months ahead?

Leveraged loan issuance reached US$612.5 billion in H1 2022, down on the US$755.5 billion recorded in the same period in 2021

02

High yield bond issuance also dropped, year-on-year, from US$267.6 billion to US$63.6 billion—though markets began to open again in June

03

Since January, the US Federal Reserve has raised interest rates four times, taking the benchmark federal-funds rate to a range between 2.25 and 2.5 percent

Issuance across US leveraged loan and high yield bond markets cooled in the first half of 2022, but the market has proven resilient in the face of rising interest rates, inflationary pressures and geopolitical headwinds.

After a frenetic period of activity in 2021, when issuance pushed up against all-time highs, spurred on by a post-pandemic bounce and bountiful liquidity, the market was already preparing to take a breath. The challenging macro-economic backdrop has given lenders and borrowers further reason to shift gears and adjust to the changing landscape.

As a result, issuance across US leveraged loan and high yield bond markets eased, with leveraged loan issuance dropping from US$755.5 billion in H1 2021 to US$612.5 billion in H1 2022 and high yield bond issuance dropping from US$267.6 billion to US$63.6 billion in the same period.

The decline in leveraged loan issuance in H1 2022 year-on-year

Volatility upends status quo

In response to this volatility, cautious investors have pulled back from leveraged loans and high yield bonds in favor of safe haven assets like US Treasuries, which are providing higher yields as interest rates rise.

In the leveraged loan market, these factors contributed to some transactions being put on hold, including the proposed loans for Callaway Golf and Goodnight Midstream, while Covis Pharma sweetened its loan issuance with an issue price of 90 to help push a prolonged syndication process over the line.

US high yield bond markets issuance meanwhile, ground to a halt, particularly in the second quarter of the year. This prompted several issuers—including nutrition company BellRing Distribution and Tesla—to pull bond offerings from the market.

According to Bloomberg, approximately 80 companies worldwide (with nearly half of them in the US) paused about US$25 billion worth of capital -raising plans between the last week of February and the last week of March.

Stubbornly high inflation and rising interest rates contributed to this abundance of caution.

In March 2022, the US Federal Reserve approved its first interest rate increase in more than three years, raising rates by a quarter percentage point. At the beginning of May, the Fed proceeded with a 0.5 percentage point increase to its benchmark interest rate and outlined a program to reduce its bond holdings by US$95 billion a month. By June, as inflation reached a 40-year high, interest rates were increased by another 0.75 percentage points—the third increase of the year and the largest hike since 1994. This was followed by another 0.75 percentage point hike in July. More hikes are expected this year, with liquidity also expected to tighten as the US Central Bank reduces its US$9 trillion balance sheet.

There are positive signs, however, that high yield investors are adjusting to the shifting interest rate backdrop. In the first ten days of June, issuers secured US$5 billion in high yield funding (versus just US$4 billion for all of May). The pipeline of high yield deals at the time was healthy too, including a US$750 million note intended to back Brookfield’s buyout of CDK. According to Debtwire Par, issuance reached US$8.6 billion by the end of June—still down on monthly averages, but more than double the issuance seen in May.

According to Debtwire Par, the average prices for US high yield bonds trading in the secondary market have gone from a high of 3 percent above par in January down to 85.58 percent of par in June.

Issuers recalibrate expectations and strategies

These profound changes in the market have prompted many issuers in the US to reassess their capital requirements as well as their financing strategies.

Higher pricing has seen several borrowers kick planned issuance down the road into the second half of 2022 or even 2023. With transaction volumes down, pricing has proven choppy, with little visibility on where the market will settle as pricing moves from week to week.

This unpredictability around pricing, combined with increasing flex and wider uncertainty, has seen more issuers turn to direct lending options, even for sizeable credits that would historically have defaulted to syndicated loan and high yield bond markets. (See "From rising costs to ESG ratchets: Five trends that will drive leveraged finance in 2022" for more.)

As the dry powder available to direct lenders has grown, they have been able to team up and fund increasingly larger transactions. While direct loans are typically more expensive than traditional loans, direct lenders have been able to win more deals in 2022 as they underwrite and hold debt themselves.

This puts direct lenders in a position to remove syndication risk and uncertainty for borrowers, placing them in a strong position to take market share from traditional leveraged loans and bonds.

The growing prominence of direct lenders has been especially strong on the financings of buyout deals. Private equity firm Thoma Bravo, for example, secured a US$2.6 billion financing package from direct lenders for its US$10.7 billion buyout of software company Anaplan, bypassing leveraged finance markets entirely, according to Pitchbook.

Another notable change in the market has been easing refinancing and repricing activity, which was expected after the high volume of opportunistic activity observed in the first half of 2021.

In the first half of the year, investors have favored secondary markets, where the drop in prices for existing credits has offered attractive valuations, over refinancings.

According to Debtwire Par, the average prices for US high yield bonds trading in the secondary market have gone from a high of 3 percent above par in January down to 85.58 percent of par in June. This represents the biggest shift in pricing since the most uncertain period of the pandemic in May 2020.

In loan markets, meanwhile, weighted average bids in the secondary market shifted from 97.72 percent of par in January to 91.48 percent of par by the end of June.

For loan and bond issuers, the fallout of lower pricing in secondary markets has meant higher pricing for new primary issuance.

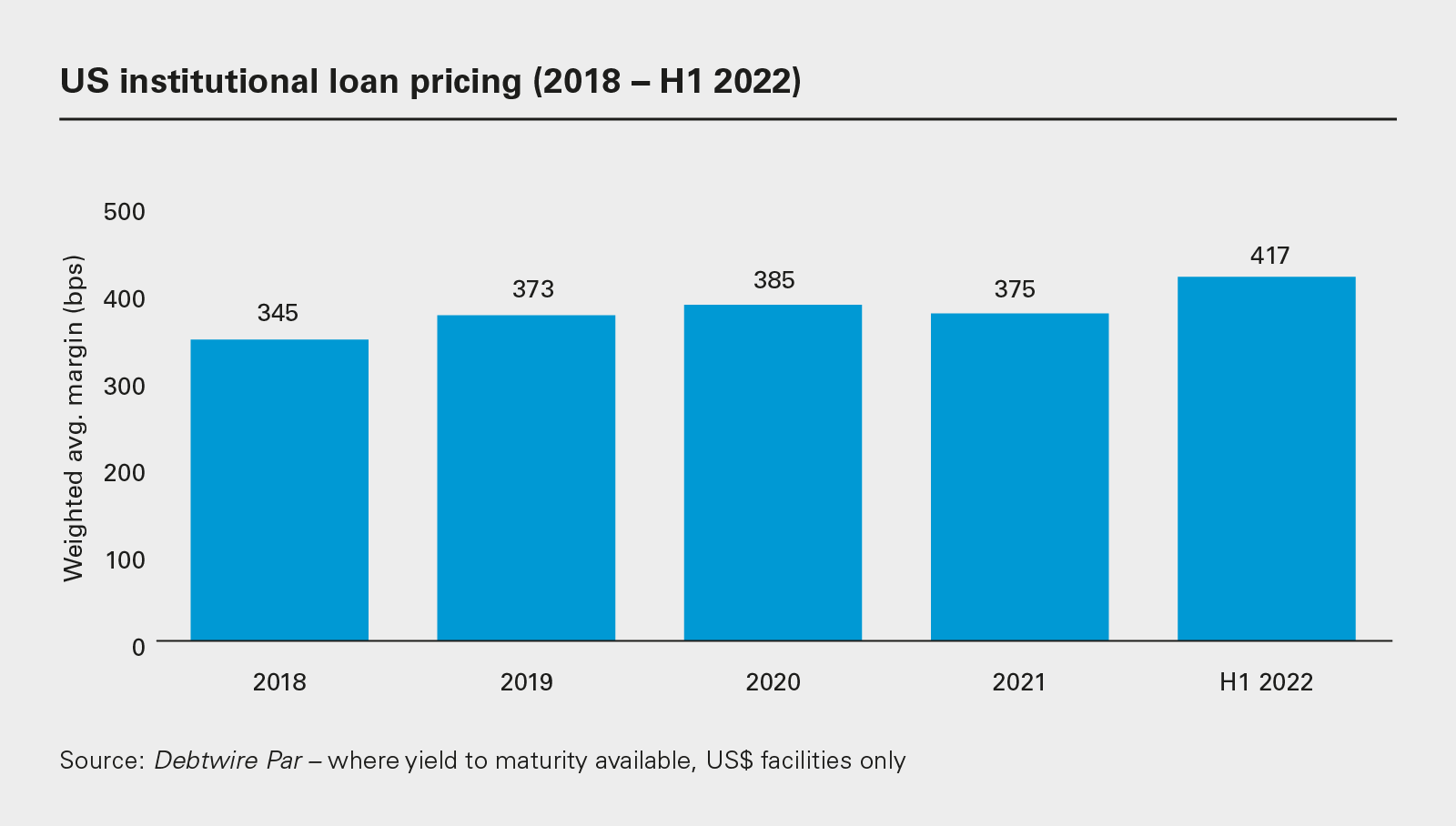

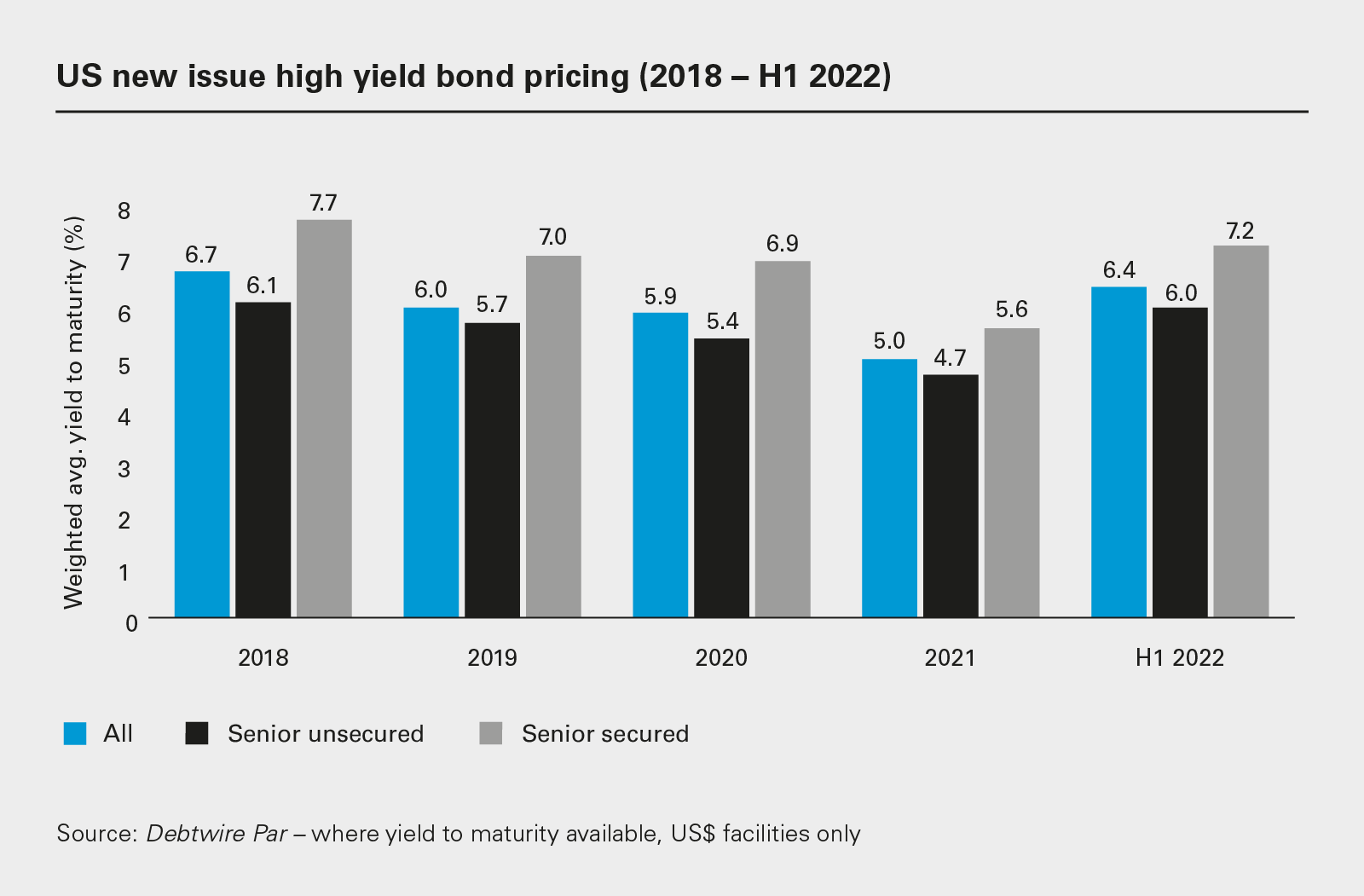

According to Debtwire Par, average margins on US institutional loans widened from 3.73 percent in Q4 2021 to 4.31 percent in Q2 2022. In the high yield market, the weighted average yields to maturity on senior secured and senior unsecured high yield bonds widened from 5.85 percent and 4.79 percent in Q4 2021, respectively, to 8.46 percent and 7.89 percent by the end of Q2 2022.

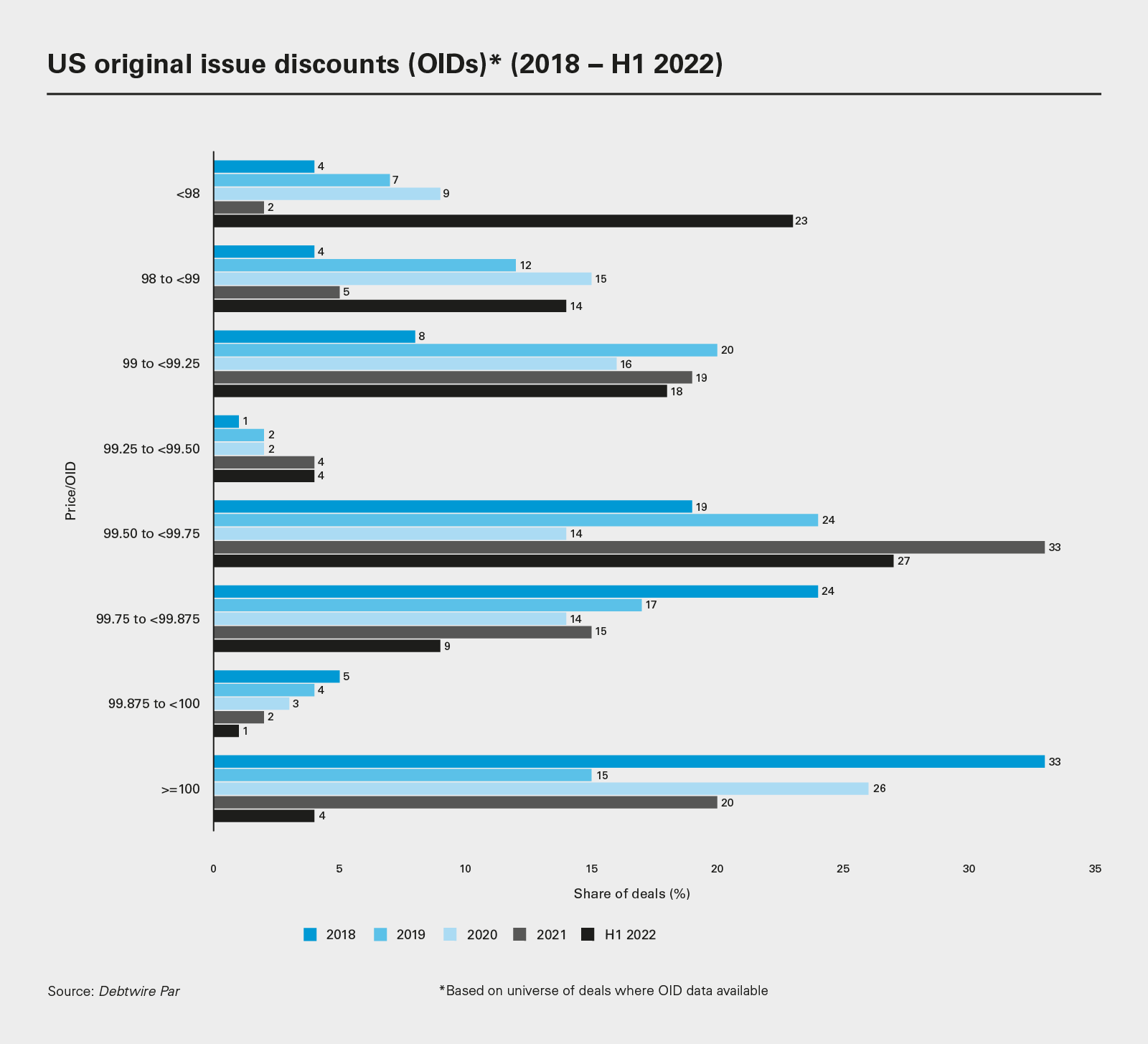

In the loan space, more deals are also flexing in favor of lenders as borrowers face greater scrutiny in a tougher market. Pricing flex allows the arrangers of loans to adjust pricing in line with investor demand. Depending on market conditions, pricing can rise, requiring borrowers to pay higher interest rates on loans, or fall, reducing borrowing costs.

Figures from Debtwire Par show that, in Q1 2022, there were roughly the same number of price flex increases and market-driven pricing decreases on execution.

This represents a significant rebalancing of the market from the 94 downward adjustments and 22 upward flexes recorded during the same period a year earlier. In June, Debtwire Par recorded two upward flexes and one downward adjustment.

Issuers are starting to accept that debt has become more expensive. Used car retailer Carvana, for example, was able to price a US$3.27 billion bond to finance its acquisition of ADESA’s physical auction business but had to offer investors a coupon of 10.25 percent to land the package. This compares to a bond the same company issued in August of last year at 4.8 percent.

With half of the year still to go, the outlook for the US leveraged finance market remains uncertain, as lenders and borrowers continue to adapt to a challenging market backdrop and expected ongoing volatility.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: US leveraged loan versus high yield bond quarterly issuance (2018 − H1 2022) (PDF)

View full image: US leveraged loan versus high yield bond quarterly issuance (2018 − H1 2022) (PDF)

View full image: US institutional loan pricing (2018 − H1 2022) (PDF)

View full image: US institutional loan pricing (2018 − H1 2022) (PDF)

View full image: US new issue high yield bond pricing (2018 − H1 2022)

View full image: US new issue high yield bond pricing (2018 − H1 2022)

View full image: US original issue discounts (OIDs)* (2018 − H1 2022) (PDF)

View full image: US original issue discounts (OIDs)* (2018 − H1 2022) (PDF)

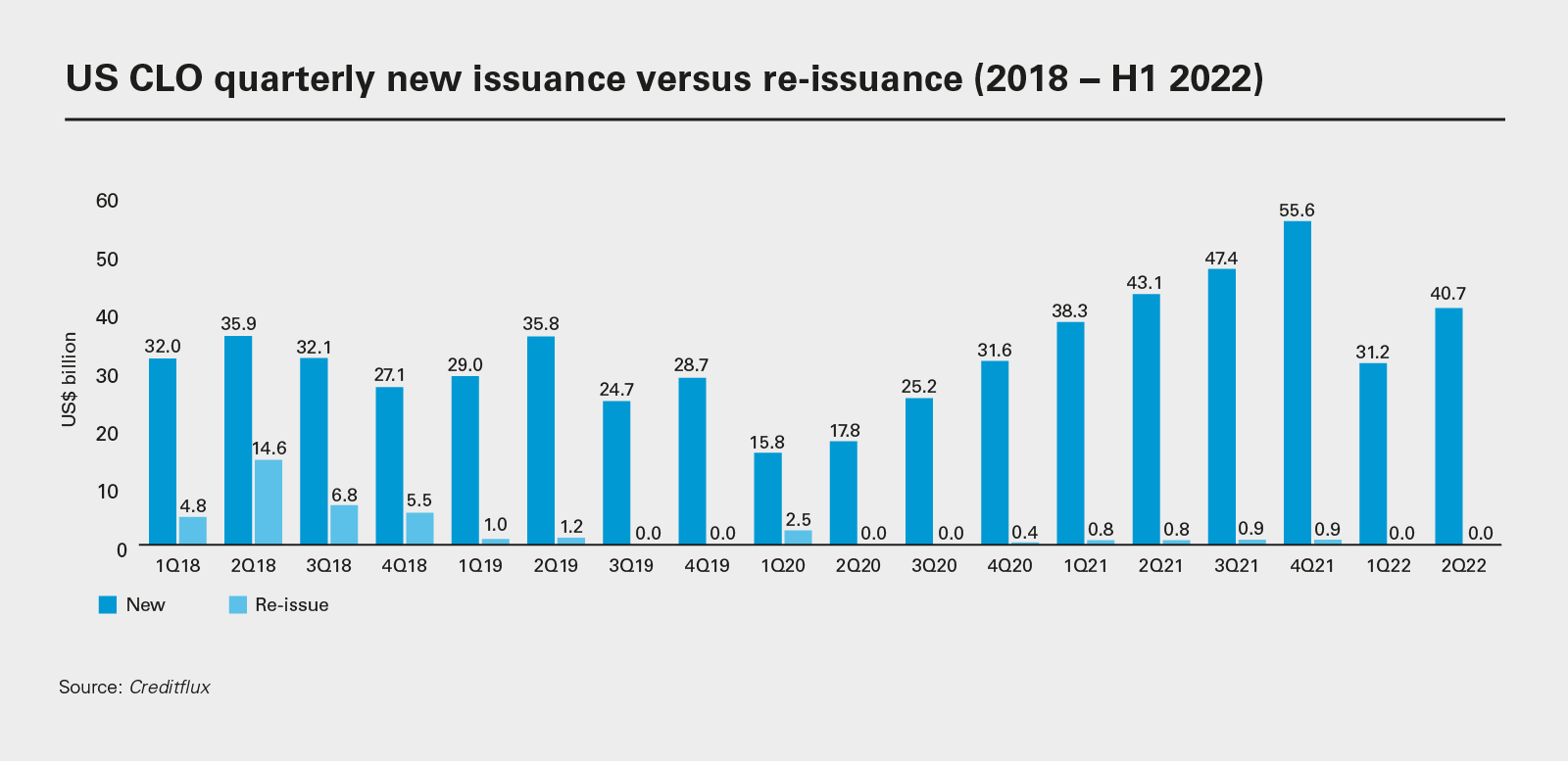

View full image: US CLO quarterly new issuance versus re-issuance (2018 − H1 2022) (PDF)

View full image: US CLO quarterly new issuance versus re-issuance (2018 − H1 2022) (PDF)