Although the record-breaking deal activity of 2021 spilled over into 2022, headwinds in the first quarter developed into a significant slowdown during the rest of 2022, with an expectation of continued slowness as we enter 2023

This time last year, the US M&A market continued to be busy with deals in the pipeline from 2021, both deals proceeding to signing, and signed deals in the process of moving to closing.

However, it was evident from early in 2022 that new M&A activity was going to be down significantly from 2021. Cracks were already beginning to show the year before, as the Federal Reserve's language took a more hawkish turn. Talk of inflation being "transitory" shifted. By March, the Fed had made its first interest rate hike in four years. By mid-year, the S&P 500 had entered a bear market.

Since first tightening its monetary policy, the central bank has raised the federal funds target rate by a full 425 basis points (bps). This is the fastest pace of change in modern history. By December 2022, the brakes were being pumped a little less, rounding off the year with a 50 bps increase.

Nevertheless, Fed chair Jerome Powell's language remained resolute at a December 14 press conference announcing the increase: "We have covered a lot of ground, and the full effects of our rapid tightening so far are yet to be felt. Even so, we have more work to do."

Officials forecast up to a total three-quarter point more in interest rate increases this year—the Fed's policy extending longer than many had anticipated. Some are still hopeful that a pivot is not far away. Bond markets have been calling the Fed’s bluff with two-year US Treasury yields peaking in November and dipping below the federal funds rate.

As inflation shows signs of rolling over and economic growth stalls, opinion is divided over what 2023 holds in store—a soft landing or a hard landing. Even if the Fed eventually walks back its recent comments with a course correction, that would suggest that it has overshot the mark.

What is clear is that the first half of 2023 will not carry with it the spillover momentum seen in early 2022, and some investors are bearish on how 2023 will fare. Nevertheless, another camp remains cautiously optimistic. Taken as a whole, 2022 put in a solid performance as compared to historic performance. The real story, however, is that deal activity trended down with each successive quarter as valuations fell, corporate equity issuances became less attractive and debt financing was increasingly costly and less accessible.

As the articles in this report demonstrate, we do not see an early return to a busy M&A market. Opportunistic strategic M&A will dominate until questions regarding a recession are answered and confidence in the stock market returns.

US M&A in review: Momentum can only take you so far

M&A started strong in 2022 with robust deal activity and megadeals dominating the landscape that was largely the result of unprecedented spillover from 2021. But then, things took a turn and deals stalled in the second half of the year, as shifting macro-economic conditions began to take hold.

The US private equity (PE) market in 2022 aligned overall with the broader M&A trend—activity eased off considerably, year-on-year, but remained above historic levels—and like the M&A market at large, it tailed off as the year progressed, but what does this mean for the year ahead?

With some rare exceptions—namely in the oil & gas and energy sectors—deal activity was down in 2022 as a sense of fatigue set in following a prolonged period of high deal activity and as inflation and rising interest rate concerns took center stage.

PMB performs as pharma groups repurpose their portfolios

After a year of historic profits in 2021 following the mass roll-out of COVID-19 vaccines and related treatments, big pharma companies armed with cash for deals have been shifting their attention.

A flurry of activity early in 2022 sees real estate outperform

Real estate has historically shown resilience during challenging economic periods and is considered a reliable hedge against inflation—but not all assets are created equal, and dealmakers were highly selective in the transactions they pursued in 2022.

US M&A in review: Momentum can only take you so far

M&A started strong in 2022 with robust deal activity and megadeals dominating the landscape that was largely the result of unprecedented spillover from 2021. But then, things took a turn and deals stalled in the second half of the year, as shifting macro-economic conditions began to take hold

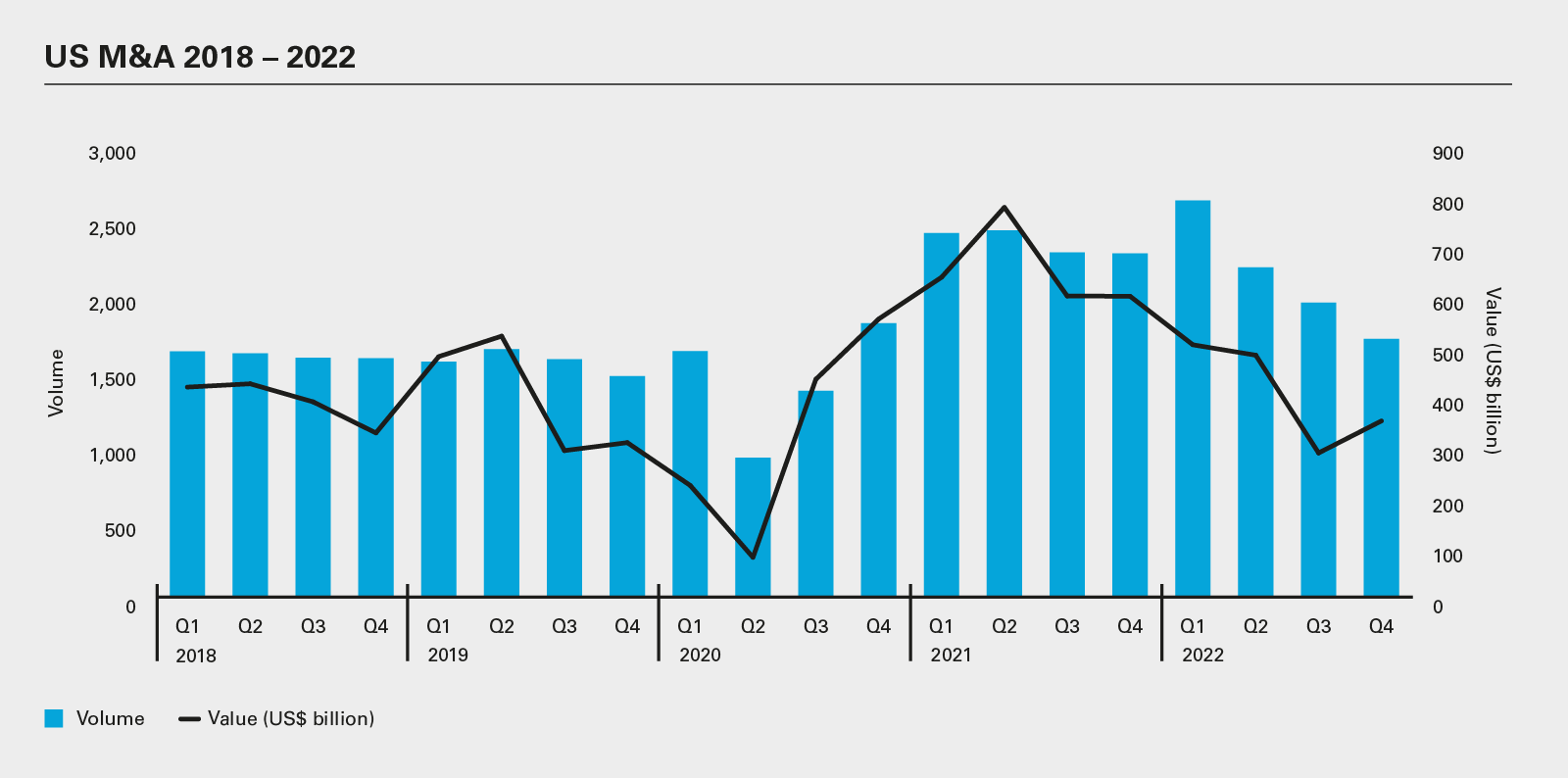

On the surface and compared to historical performance, it was another solid year. According to Mergermarket, a total of 8,468 M&A deals were announced in the US in 2022, worth in aggregate US$1.6 trillion. Although this was a year-on-year decline, in terms of volume and value, of 10 percent and 38 percent respectively, it was still exceptionally strong. Put into perspective, the deal tally is higher than in any year except for 2021.

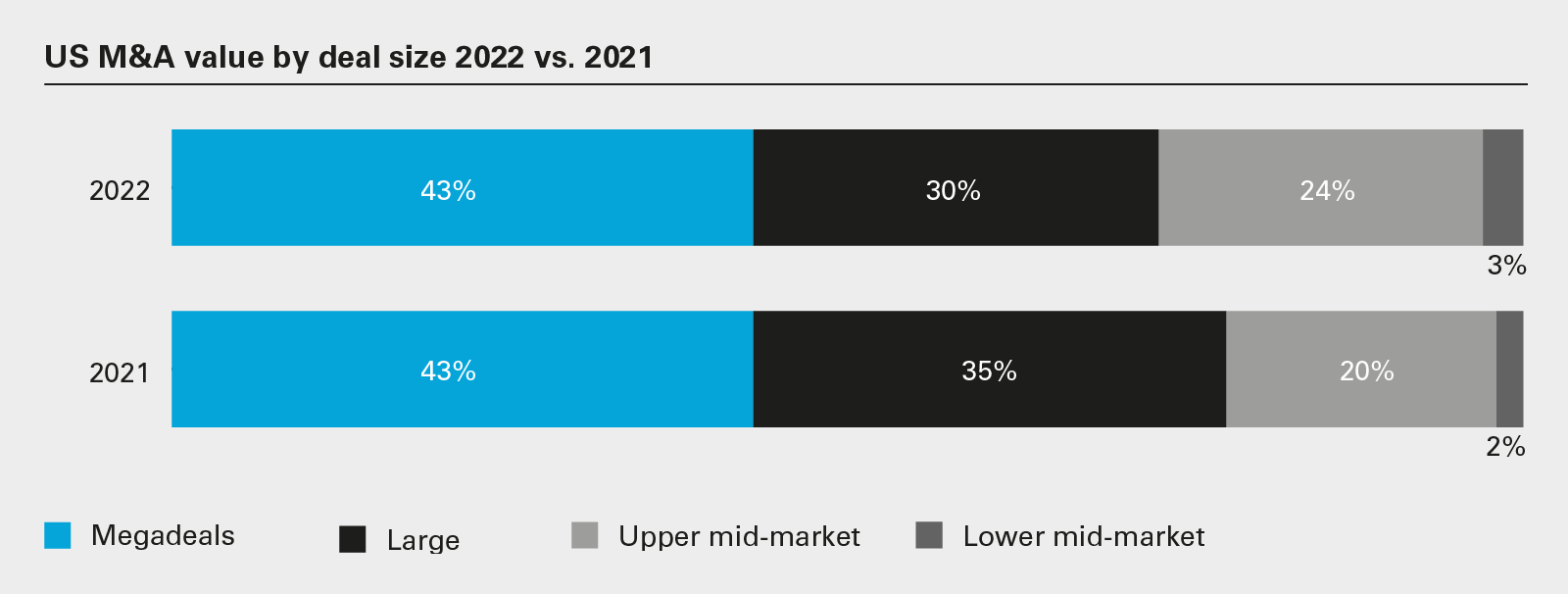

Megadeals worth upward of US$5 billion were also a major feature, thanks to some monumental technology transactions. Mergermarket data shows large-cap deals accounted for more than 40 percent of total deal value, matching 2021. Based on these stats alone, 2022 looked like a strong year for M&A.

Looks can be deceiving, however, and 2022 was a year of two halves. Several large tech deals boosted deal values through the first half of the year. Microsoft's US$75.1 billion merger bid for video game developer Activision Blizzard, Broadcom's US$71.6 billion offer for VMWare and Elon Musk's US$44 billion Twitter takeover—the year's top-three largest deals—were all announced between January and May. These helped ensure that technology remained the dominant sector by value, with deals worth in aggregate US$612.6 billion, and retained the top spot measured by volume at 2,589 deals.

The value of US M&A deals in 2022— a 38% decrease compared to 2021

35%

The fall in US M&A deal value in H2 2022 compared to H1 2022

Second-half slowdown

A very different picture emerged in the second half of the year once the spillover from 2021 receded and the momentum was lost. Deal announcements were fewer and farther between as the reality of surging inflation and the Fed's tightening path came into sharp relief and the S&P 500 entered bear market territory. Fears of a future recession began to enter the conversation.

There were 3,659 deals in the second half of this year, worth US$636 billion. This compares with first-half totals of 4,809 transactions worth US$981.6 billion (representing respective declines of 24 percent and 35 percent). Drilling down further, M&A levels continued to fall throughout the year, each quarter showing a successive decline in deal volume and value.

SPAC activity followed a similar path, with 16 listings on US exchanges in the second half of 2022 worth US$1.3 billion, versus the 70 listings worth US$12.1 billion in the first half of the year.

It can take time for private market valuations to catch up with the declining public market equity valuations. The resulting mismatch in value perspectives between buyers and sellers negatively impacts deal activity.

This year's Fed policy switch has had two main impacts on capital markets that are clearly dragging on confidence and deal activity. The broad fall in share prices—and therefore corporate valuations—has made it far less attractive to targets and dilutive to stockholders to issue equity to fund deals. This is especially true in the technology sector. By mid-December 2022, the tech-heavy Nasdaq 100 was down 32 percent on the start of the year (compared with a decline of less than 20 percent for the S&P 500).

It can take time for private market valuations to catch up with the declining public market equity valuations. The resulting mismatch in value perspectives between buyers and sellers negatively impacts deal activity. Some potential sellers may feel compelled to wait for more positive macro news, and instead are focusing their attention on operational support and protecting value until the dust settles.

In principle, this could be an unmissable buy opportunity for PE. Middle-market operators have found themselves at a distinct advantage, buttressed by a supportive private credit ecosystem. This lifeline is not available for the largest PE deals, and the material weakening of public debt markets in the second half of the year is hamstringing the upper end of the PE buyout market in particular. Rising interest rates also have made loans prohibitively expensive, where they are even available at all. According to Debtwire Par, primary issuance across institutional loan and high yield bond markets in the US was down 68 and 78 percent year-on-year respectively.

Outside of fundamental market forces, there are policy and enforcement developments that are proving to be both carrots and sticks. The recently passed Inflation Reduction Act has created compelling tax incentives for investment into the renewable energy sector, unlocking some US$400 billion in federal funding. Investors are actively strategizing to capitalize on this opportunity, and this will play out for years to come.

At the same time, antitrust actions are being enforced with a fervor and level of coordination not previously seen. In December 2022, the Department of Justice and the Office of the Inspector General of the Department of Health and Human Services announced a new partnership to protect healthcare markets, while the Federal Trade Commission has thrown some of last year's largest deal announcements into doubt.

These mixed signals are complicated by the uncertainty of the macro outlook. Inflation is showing signs of improvement but remains well above the Fed's 2 percent target. Jobs reports also continue to beat expectations. To date, however, the Fed is not diverting from its plan to slow the labor market and tackle inflation just yet.

As we look ahead to a new year, there are two camps. Some expect more pain ahead—certainly, debt financing will remain costly until further notice—but a full-blown recession looks increasingly unlikely. Optimists, meanwhile, are not ruling out the Fed achieving its fabled soft landing. One thing is clear, the first half of 2023 will look more like the second half of 2022 than the upbeat opening half of last year.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: US M&A 2018 – 2022

View full image: US M&A 2018 – 2022

View full image: Top-ten US M&A deals in 2022

View full image: Top-ten US M&A deals in 2022

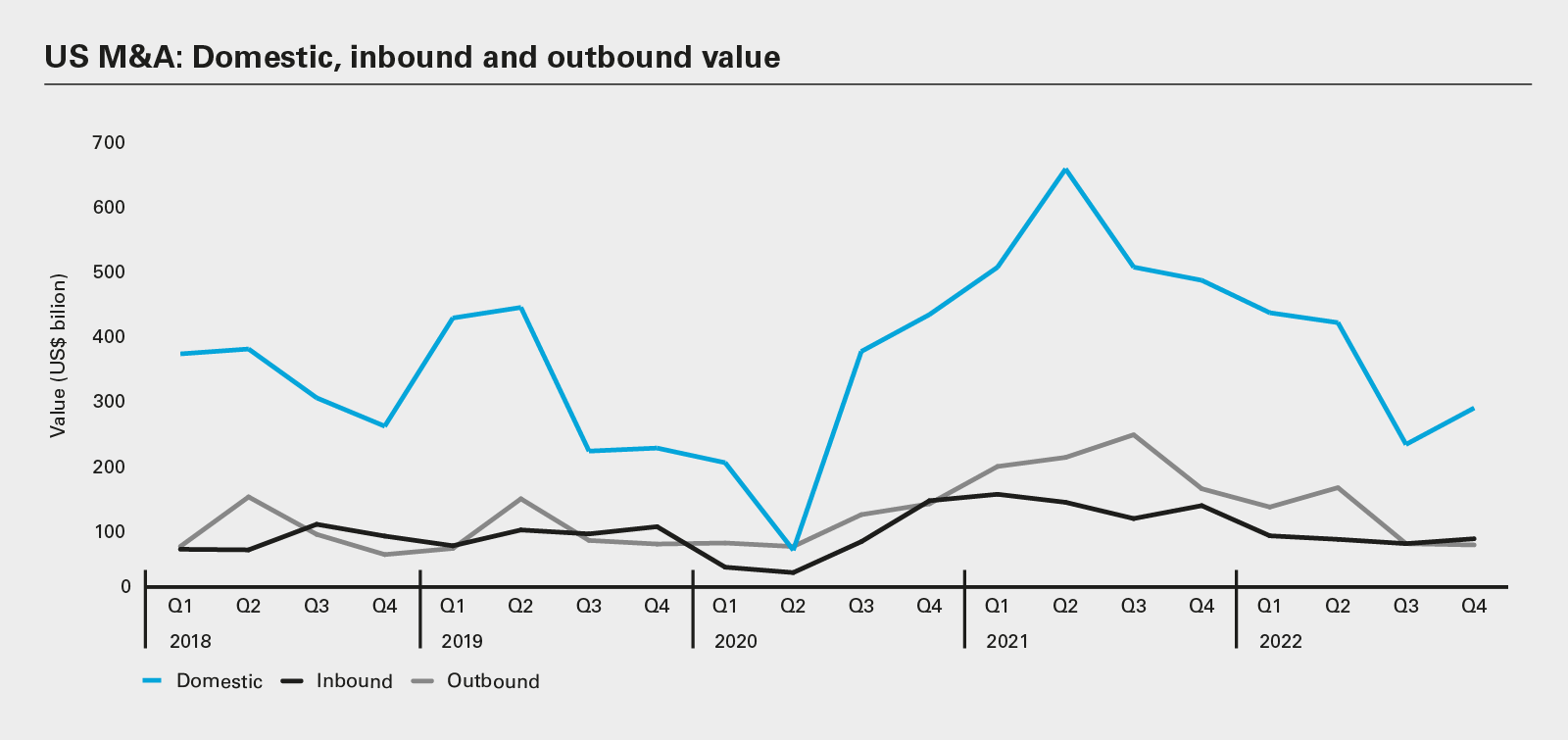

View full image: US M&A: Domestic, inbound and outbound value

View full image: US M&A: Domestic, inbound and outbound value

View full image: US M&A value by deal size 2022 vs. 2021

View full image: US M&A value by deal size 2022 vs. 2021