Although the record-breaking deal activity of 2021 spilled over into 2022, headwinds in the first quarter developed into a significant slowdown during the rest of 2022, with an expectation of continued slowness as we enter 2023

This time last year, the US M&A market continued to be busy with deals in the pipeline from 2021, both deals proceeding to signing, and signed deals in the process of moving to closing.

However, it was evident from early in 2022 that new M&A activity was going to be down significantly from 2021. Cracks were already beginning to show the year before, as the Federal Reserve's language took a more hawkish turn. Talk of inflation being "transitory" shifted. By March, the Fed had made its first interest rate hike in four years. By mid-year, the S&P 500 had entered a bear market.

Since first tightening its monetary policy, the central bank has raised the federal funds target rate by a full 425 basis points (bps). This is the fastest pace of change in modern history. By December 2022, the brakes were being pumped a little less, rounding off the year with a 50 bps increase.

Nevertheless, Fed chair Jerome Powell's language remained resolute at a December 14 press conference announcing the increase: "We have covered a lot of ground, and the full effects of our rapid tightening so far are yet to be felt. Even so, we have more work to do."

Officials forecast up to a total three-quarter point more in interest rate increases this year—the Fed's policy extending longer than many had anticipated. Some are still hopeful that a pivot is not far away. Bond markets have been calling the Fed’s bluff with two-year US Treasury yields peaking in November and dipping below the federal funds rate.

As inflation shows signs of rolling over and economic growth stalls, opinion is divided over what 2023 holds in store—a soft landing or a hard landing. Even if the Fed eventually walks back its recent comments with a course correction, that would suggest that it has overshot the mark.

What is clear is that the first half of 2023 will not carry with it the spillover momentum seen in early 2022, and some investors are bearish on how 2023 will fare. Nevertheless, another camp remains cautiously optimistic. Taken as a whole, 2022 put in a solid performance as compared to historic performance. The real story, however, is that deal activity trended down with each successive quarter as valuations fell, corporate equity issuances became less attractive and debt financing was increasingly costly and less accessible.

As the articles in this report demonstrate, we do not see an early return to a busy M&A market. Opportunistic strategic M&A will dominate until questions regarding a recession are answered and confidence in the stock market returns.

US M&A in review: Momentum can only take you so far

M&A started strong in 2022 with robust deal activity and megadeals dominating the landscape that was largely the result of unprecedented spillover from 2021. But then, things took a turn and deals stalled in the second half of the year, as shifting macro-economic conditions began to take hold.

The US private equity (PE) market in 2022 aligned overall with the broader M&A trend—activity eased off considerably, year-on-year, but remained above historic levels—and like the M&A market at large, it tailed off as the year progressed, but what does this mean for the year ahead?

With some rare exceptions—namely in the oil & gas and energy sectors—deal activity was down in 2022 as a sense of fatigue set in following a prolonged period of high deal activity and as inflation and rising interest rate concerns took center stage.

PMB performs as pharma groups repurpose their portfolios

After a year of historic profits in 2021 following the mass roll-out of COVID-19 vaccines and related treatments, big pharma companies armed with cash for deals have been shifting their attention.

A flurry of activity early in 2022 sees real estate outperform

Real estate has historically shown resilience during challenging economic periods and is considered a reliable hedge against inflation—but not all assets are created equal, and dealmakers were highly selective in the transactions they pursued in 2022.

Private Equity in focus: Value slips as volume persists

The US private equity (PE) market in 2022 aligned overall with the broader M&A trend—activity eased off considerably, year-on-year, but remained above historic levels—and like the M&A market at large, it tailed off as the year progressed, but what does this mean for the year ahead?

In 2022, there was an 18 percent drop in the number of US PE deals, year-on-year, to 3,293 transactions. Total value fell 33 percent in the same period to US$696.7 billion. While these drops are large, 2021 was the highest volume and value on Mergermarket record.

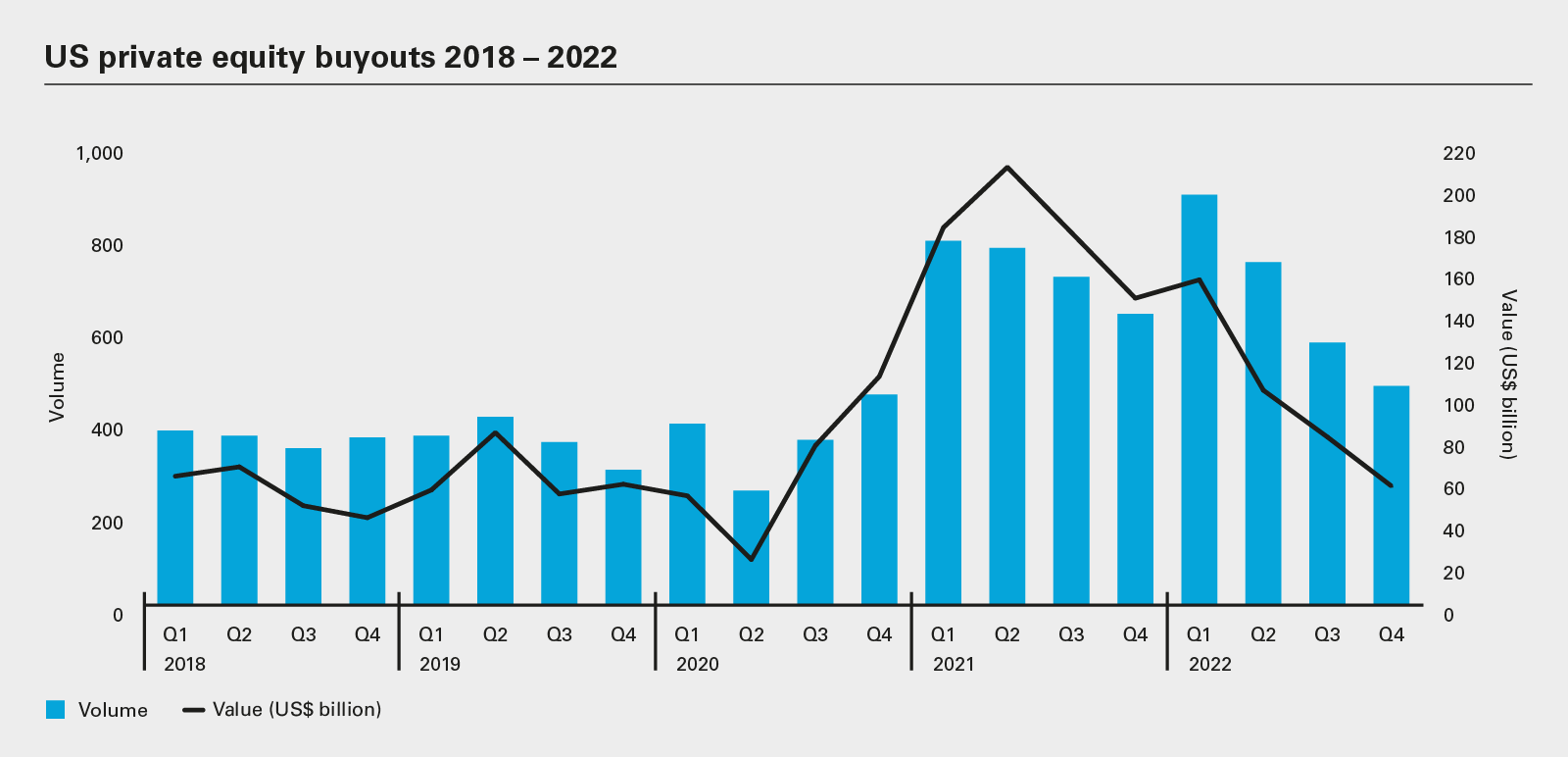

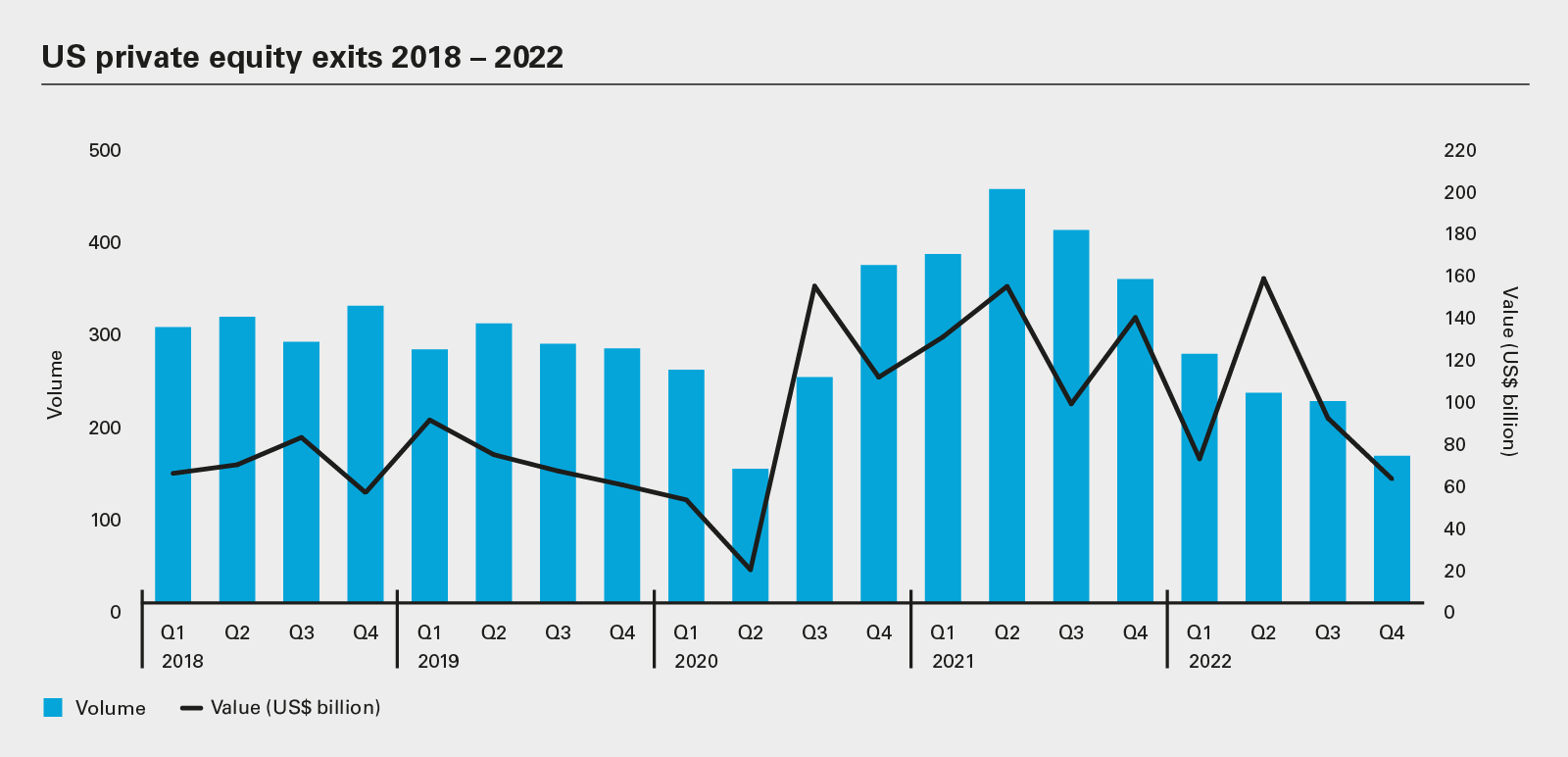

As expected, the volume of buyouts held up more firmly than exits as conditions transitioned from the unprecedentedly supportive seller's market of 2021 to something closer to a buyer's market—albeit with some important caveats.

This transition is evident in the freefall in exit volume, which had already been in steady decline as far back as Q2 2021. Divestitures were down by as much as 45 percent year-on-year to 873 transactions in 2022. Value fell by 27 percent in the same period to US$363.1 billion, even though the top-three largest PE transactions in the US were all exits, according to Mergermarket. The US$71.6 billion merger of VMWare and Broadcom saw Silver Lake Partners cash out. Cerberus Capital Management took Albertsons public in 2020 and is now realizing its holding through Kroger's US$24.8 billion takeover of its competitor, Albertsons. And, when Adobe Systems made its US$20 billion Figma play, a collection of VC funds including Index Ventures, Greylock, Kleiner Perkins, Sequoia Capital, Andreesen Horowitz and Durable Capital Partners cracked open the champagne.

The volume of buyouts held up more firmly than exits as conditions transitioned from the unprecedentedly supportive seller’s market of 2021 to something closer to a buyer’s market.

On the buy-side, a total of 2,676 buyouts were made in 2022—an 8 percent drop in volume, but far and away the highest total on record for any year aside from the outlier 2021. The next-closest year was 2020, which saw 1,455 deals, compared to 2,905 in 2021.

It is in value terms where real weakness has been showing and there is good reason for this. The US$394.3 billion in new deals is down 45 percent year-on-year. By Q4 2022, buyout value had ebbed to its lowest level since the pandemic nadir in Q2 2020.

One main reason relates to access to debt financing (in particular the syndicated debt market), which became painfully restrictive in the second half of 2022, to the extent that some of the industry's very largest deals were simply impossible to execute on economically feasible terms. However, at lower value deals, private credit funds were willing to lend to fill the funding gap, though notably at lower overall commitment levels and materially higher yield profiles. This resulted in larger deals still being able to be executed with private credit funds clubbing up to provide the larger debt packages. For example, in May, Blackstone led a group of direct lending funds including Ares, Blue Owl and Oak Hill to provide a US$4.5 billion unitranche loan for Hellman & Friedman's acquisition of Information Resource.

Adapting to change

More recently, as macro-economic uncertainties continue to persist, even these larger unitranches have become more difficult to pull together. Private debt funds have continued downsizing their quanta to reduce their concentration risk in the face of a weakening economic outlook and the prospect of rising default rates.

For this reason, the bifurcation between relatively strong volume and depressed value is likely to persist in the near term as sponsors focus on deals that are still possible in the constricted environment. This may include smaller platform deals or minority investments that do not involve a change of ownership control and, therefore, existing debt instruments are portable.

Add-ons have also been an increasingly popular strategy in the more recent past, since current portfolio companies will already have debt agreements and borrowing relationships, making it easier to access capital for the right acquisitions, even if it comes with the potential for existing debt to reprice at closer to today's market rate.

In keeping with the Fed's "higher for longer" mantra, sponsors should expect debt financing to come at a higher cost for the foreseeable future, even if access to leveraged loans shows signs of improving in 2023. At the same time, pedigree sponsors with a long history will have experience with a higher interest rate environment and will consider lower returns to be only temporary. Such firms will lean on lending relationships they have formed over the years, and those lenders will likely continue to support them as both sets of dealmakers rely on deal activity to advance. If PE has proven one thing time and time again, it's that it is a highly adaptable industry.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: US private equity buyouts 2018 – 2022

View full image: US private equity buyouts 2018 – 2022

View full image: US private equity exits 2018 – 2022

View full image: US private equity exits 2018 – 2022