As we enter 2021, COVID-19 continues to weigh on every decision, from our health to our work and our long-term plans and yet, despite these concerns, European leveraged finance markets have weathered the storm and remain positive about the year ahead

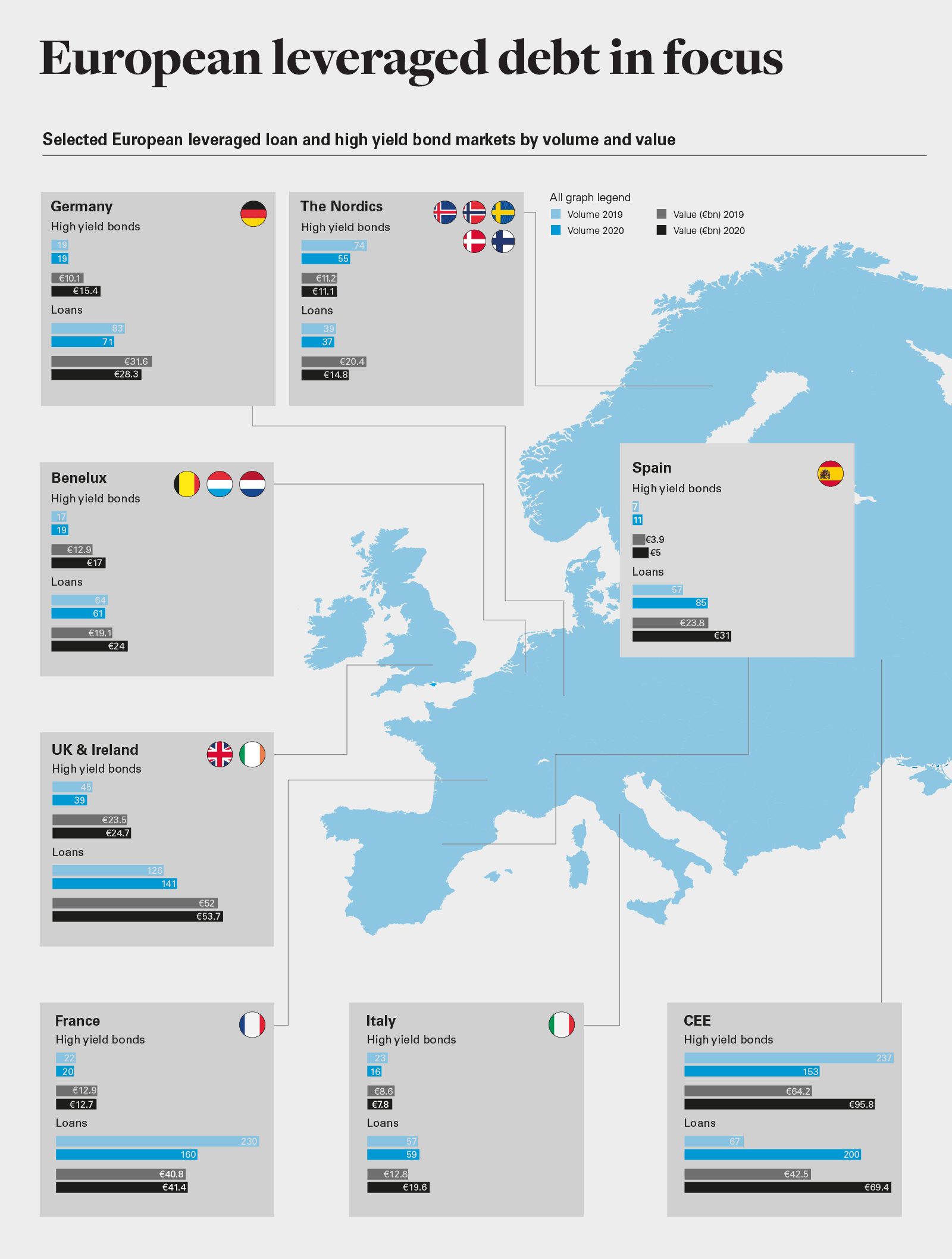

In March 2020, as lockdown restrictions took hold, the European leveraged finance markets ground more or less to a halt. Many feared the worst, as leveraged loan issuance dropped significantly that month and high yield bonds saw virtually no activity at all. Borrowers and lenders alike held their breath, shoring up their finances and waiting to see what might come next. And then, just as quickly, investor sentiment began to improve. By the end of Q2 2020, leveraged loan activity had returned almost to pre-pandemic levels.

And while it slowed somewhat in the latter half of the year, as new waves of COVID-19 swept across the UK and Europe, the final tally was up 11% on the year before—a remarkable achievement, confirming the market’s long-term resilience.

The story in high yield bond markets was equally impressive, ending the year up 10% on 2019 figures, with every indication that it will retain a larger share of the market in the months ahead.

What does all of this mean for 2021?

First and foremost, the influence of COVID-19 will continue to be felt, even as vaccines are rolled out across Europe. Sectors hammered by the first wave—including entertainment and leisure, hospitality, retail, oil & gas and aviation—will struggle to secure financing, having already done what they can to survive. Within those sectors, those that require financing and are able to secure deals are likely to have to pay for the privilege, with leveraged debt either becoming more costly for those whose credit has taken a hit or only being made available on tighter terms.

Second, and in contrast, lenders will turn their attention to high-quality credits or sectors that have found new avenues for growth during COVID-19, such as technology and healthcare.

Third, loan supply will continue to open up—but primarily for those that meet the right criteria. For those well-positioned companies, this flight to quality will continue to offer favourable terms and pricing, and the light-touch covenant packages that were the norm pre-pandemic should remain in place.

At the same time, an anticipated recovery in mergers and acquisitions and leveraged buyout activity will provide an additional lift in the early months of 2021.

And finally, the issues that were front of mind pre-pandemic will continue to influence borrowing and lending decisions, especially environmental, social and governance (ESG) factors—investors will take a positive view of any credits that incorporate ESG criteria in a meaningful way. This will no doubt drive this trend in the months ahead as recovery takes hold and global debt markets return to growth.

View full image: European leveraged debt in focus (PDF)

View full image: European leveraged debt in focus (PDF)