Overall investment outlook for global aviation finance

Aviation sector executives expect to maintain or increase investment in 2022, despite continuing headwinds caused by COVID-19 and concerns about the global economy

The past two years has been a period of intense turbulence for the aviation sector, with a number of bankruptcies, bailouts and collapsing revenues brought about by the coronavirus pandemic. The impact on airline receipts has been challenging. Indeed, the gap between projected and actual receipts suggests that airlines have lost passenger revenues worth nearly US$1 trillion as a result of the pandemic.

Rebuilding balance sheets and restoring passenger confidence is going to take time. Uncertainties lie ahead, and (as the rapid spread of COVID-19 variants remind us) there is no room for complacency.

Yet as this survey shows, there are also tentative grounds for optimism.

First, airlines and lessors now have access to a wider range of funding opportunities than ever before. Innovative financing is the order of the day: In addition to traditional sources, such as banks, capital markets and export credit agencies, the aviation sector is increasingly tapping into funding from alternative capital providers, including private equity and hedge funds. High- net-worth individuals and family offices are now part of the mix as well, along with new capital market products, such as green bonds.

Second—and closely linked to the evolving financing environment—is the rising awareness of environmental, social and governance (ESG) considerations within aviation. Airlines and lessors—and the investors who back them—are making the first steps towards decarbonizing aviation with initiatives that span everything from the development of sustainable aviation fuel (SAF) to the first, albeit short-range, electric aircraft.

“Uncertainties lie ahead, and there is no room for complacency. Yet as this survey shows, there are also tentative grounds for optimism.”

This matters, because the future of aviation is as much a battle for hearts and minds as it is about technology. COVID-19 has turned many of us into teleworkers, while the rise of the "staycation" has reminded travelers of the good times they can have close to home. Winning back passengers—business travelers in particular—may not be easy. Against this background, travelers of all types are increasingly aware of the environmental impact of their journeys. Seen in this light, even small steps toward boosting the green credentials of airlines could make all the difference.

The aviation sector that emerges from the pandemic is likely to look very different from the one that went into it two years ago.

But it is also a sector that is likely to be more flexible, leaner, a little greener and—above all—better adapted to whatever the future has in store.

In the fourth quarter of 2021, White & Case, in partnership with Mergermarket, surveyed 100 senior-level executives at entities that have either financed or invested in the aviation industry in the past three years. The aim of the survey was to analyze sentiment regarding aviation finance. Organizations surveyed included airlines, operating lessors, banks, export credit agencies, private equity and other alternative capital providers. Job titles included CEO, CFO, director level and heads of investment.

Aviation sector executives expect to maintain or increase investment in 2022, despite continuing headwinds caused by COVID-19 and concerns about the global economy

Our survey shows that a majority of respondents expect funding to increase in 2022—and from a wide range of sources

Capital and liquidity remain a primary preoccupation for the aviation sector

Respondents see COVID-related disruptions, economic contraction and geopolitical instability as the top challenges for the aviation sector in the coming year. But growth is expected, notably in Asia-Pacific and Australasia

Flexibility in the ascendant aircraft leasing sector

Key takeaways from our survey and what they could mean for the aviation industry

Flexibility in the ascendant aircraft leasing sector

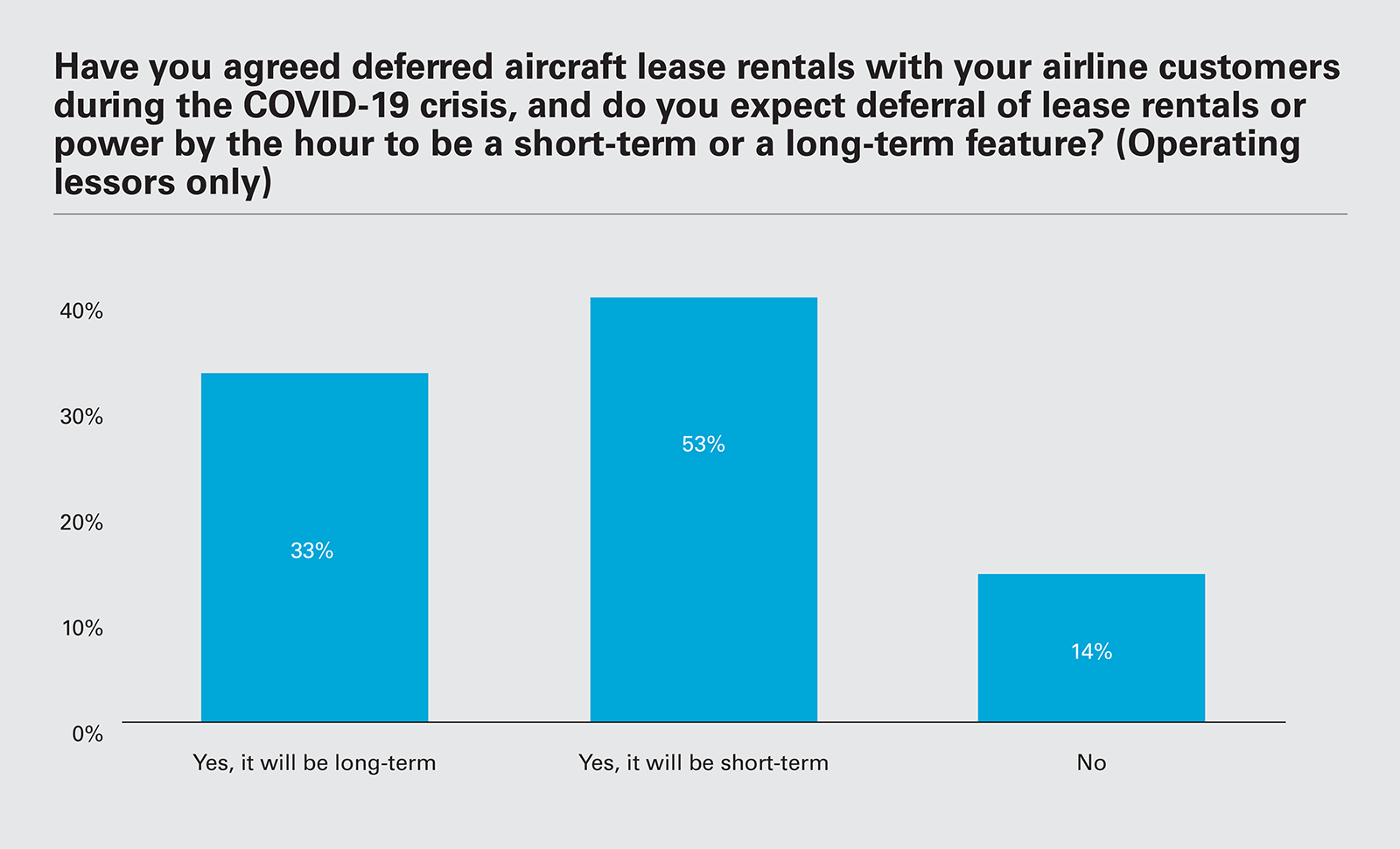

86%

of leasing companies agreed deferred aircraft lease rentals with customers during the COVID-19 crisis

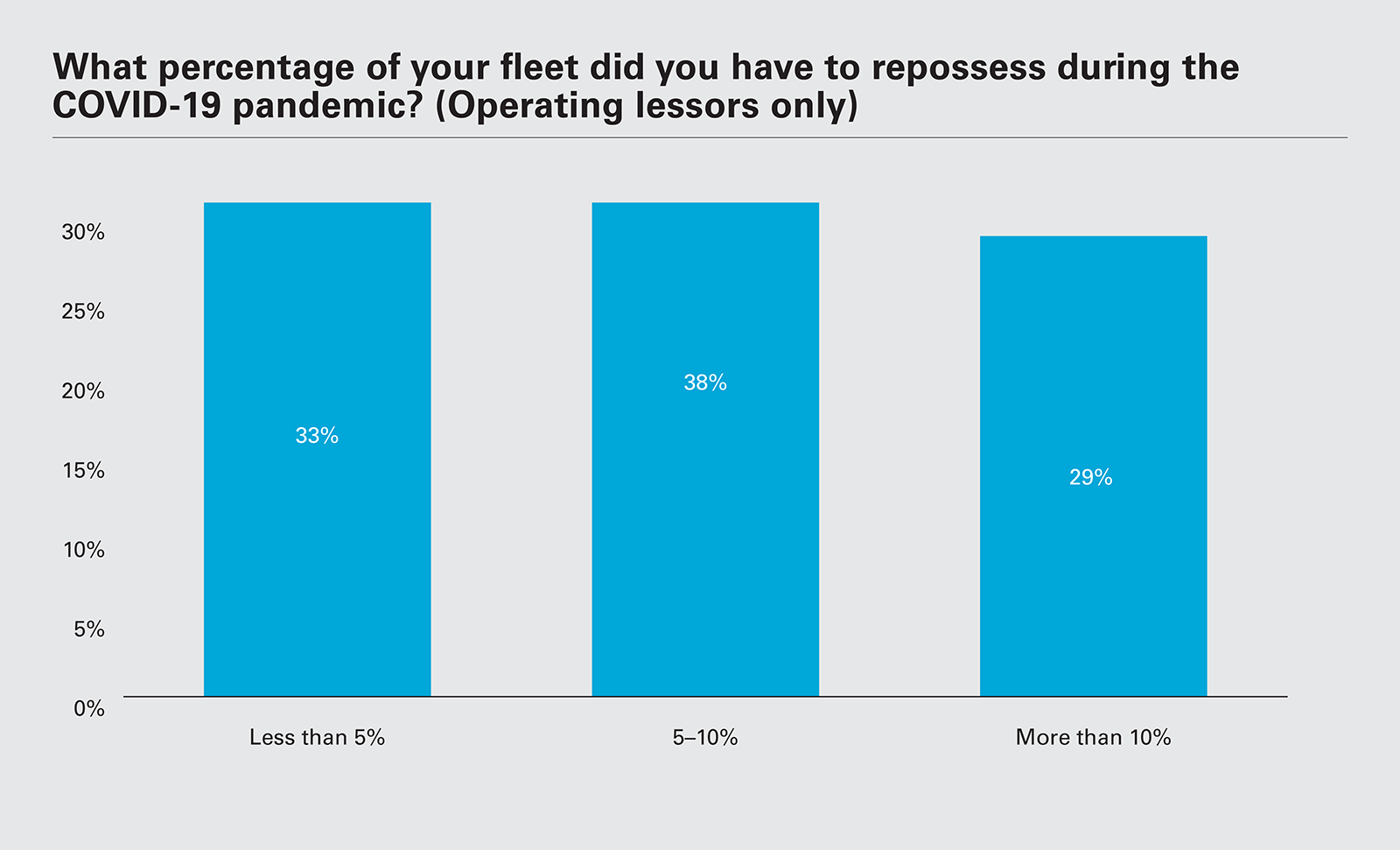

67 percent of lessors have repossessed 5 percent or more of their fleets during the COVID-19 pandemic.

Aircraft leasing companies are the backbone of modern commercial aviation. Lessors now account for an estimated 60 percent of new passenger jet deliveries, up from approximately 45 percent on the eve of the pandemic and just 10 percent in the mid-1980s.

Thanks in part to their ability to access cheaper financing than airlines, the ascendency of aircraft leasing companies has accelerated during the COVID-19 crisis. Nonetheless, the sector has experienced consolidations during the pandemic, including the US$31.1 billion acquisition by Ireland-based AerCap of General Electric's aircraft leasing arm, GECAS.

Lessors have demonstrated flexibility throughout the pandemic: 86 percent agreed deferred aircraft lease rentals with their airline customers during the COVID-19 crisis, with a little over half of respondents expecting these deferrals of lease rentals or power by the hour (PBH) to be a short-term measure.

Repossession is a last resort. Reduced demand during the pandemic (particularly for wide-body aircraft) has encouraged lessors to work with troubled airlines rather than taking aircraft back. A third of lessors in our survey say they repossessed less than 5 percent (or none) of their fleet during the COVID-19 pandemic. But 29 percent say they had to take back more than a tenth of their fleet.

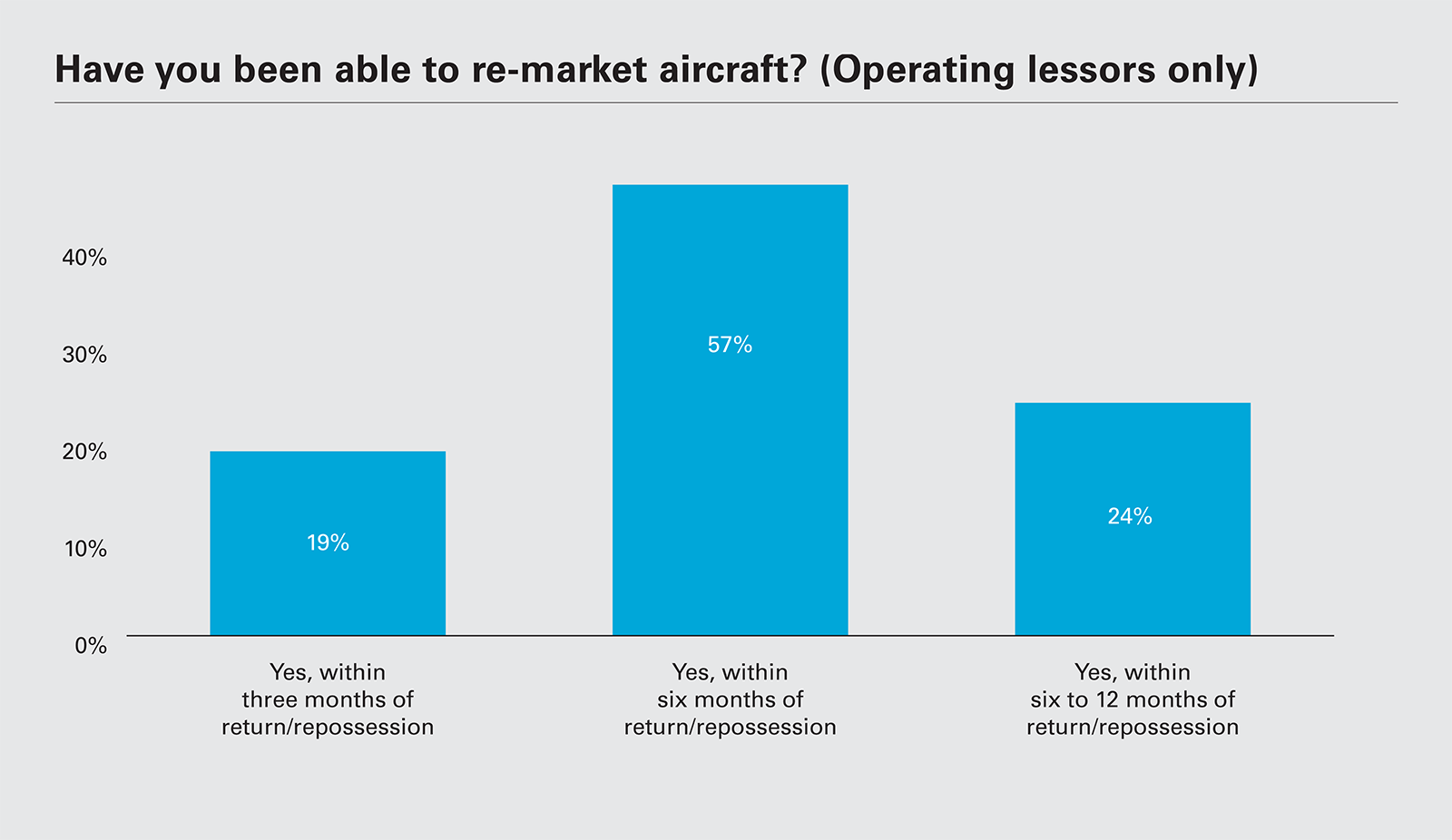

Despite suppressed demand during the pandemic, lessors have been able to re-market aircraft. This requires patience and deep pockets: For most lessors in this study (57 percent), it took three to six months to re-market aircraft, while nearly a quarter (24 percent) say it took six to12 months. Only one in five found a new taker within three months of return or repossession.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: Have you agreed deferred aircraft lease rentals with your airline customers during the COVID-19 crisis, and do you expect deferral of lease rentals or power by the hour to be a short-term or a long-term feature? (PDF)

View full image: Have you agreed deferred aircraft lease rentals with your airline customers during the COVID-19 crisis, and do you expect deferral of lease rentals or power by the hour to be a short-term or a long-term feature? (PDF)

View full image: What percentage of your fleet did you have to repossess during the COVID-19 pandemic? (PDF)

View full image: What percentage of your fleet did you have to repossess during the COVID-19 pandemic? (PDF)

View full image: Have you been able to re-market aircraft? (PDF)

View full image: Have you been able to re-market aircraft? (PDF)