Overall investment outlook for global aviation finance

Aviation sector executives expect to maintain or increase investment in 2022, despite continuing headwinds caused by COVID-19 and concerns about the global economy

The past two years has been a period of intense turbulence for the aviation sector, with a number of bankruptcies, bailouts and collapsing revenues brought about by the coronavirus pandemic. The impact on airline receipts has been challenging. Indeed, the gap between projected and actual receipts suggests that airlines have lost passenger revenues worth nearly US$1 trillion as a result of the pandemic.

Rebuilding balance sheets and restoring passenger confidence is going to take time. Uncertainties lie ahead, and (as the rapid spread of COVID-19 variants remind us) there is no room for complacency.

Yet as this survey shows, there are also tentative grounds for optimism.

First, airlines and lessors now have access to a wider range of funding opportunities than ever before. Innovative financing is the order of the day: In addition to traditional sources, such as banks, capital markets and export credit agencies, the aviation sector is increasingly tapping into funding from alternative capital providers, including private equity and hedge funds. High- net-worth individuals and family offices are now part of the mix as well, along with new capital market products, such as green bonds.

Second—and closely linked to the evolving financing environment—is the rising awareness of environmental, social and governance (ESG) considerations within aviation. Airlines and lessors—and the investors who back them—are making the first steps towards decarbonizing aviation with initiatives that span everything from the development of sustainable aviation fuel (SAF) to the first, albeit short-range, electric aircraft.

“Uncertainties lie ahead, and there is no room for complacency. Yet as this survey shows, there are also tentative grounds for optimism.”

This matters, because the future of aviation is as much a battle for hearts and minds as it is about technology. COVID-19 has turned many of us into teleworkers, while the rise of the "staycation" has reminded travelers of the good times they can have close to home. Winning back passengers—business travelers in particular—may not be easy. Against this background, travelers of all types are increasingly aware of the environmental impact of their journeys. Seen in this light, even small steps toward boosting the green credentials of airlines could make all the difference.

The aviation sector that emerges from the pandemic is likely to look very different from the one that went into it two years ago.

But it is also a sector that is likely to be more flexible, leaner, a little greener and—above all—better adapted to whatever the future has in store.

In the fourth quarter of 2021, White & Case, in partnership with Mergermarket, surveyed 100 senior-level executives at entities that have either financed or invested in the aviation industry in the past three years. The aim of the survey was to analyze sentiment regarding aviation finance. Organizations surveyed included airlines, operating lessors, banks, export credit agencies, private equity and other alternative capital providers. Job titles included CEO, CFO, director level and heads of investment.

Aviation sector executives expect to maintain or increase investment in 2022, despite continuing headwinds caused by COVID-19 and concerns about the global economy

Our survey shows that a majority of respondents expect funding to increase in 2022—and from a wide range of sources

Capital and liquidity remain a primary preoccupation for the aviation sector

Respondents see COVID-related disruptions, economic contraction and geopolitical instability as the top challenges for the aviation sector in the coming year. But growth is expected, notably in Asia-Pacific and Australasia

Flexibility in the ascendant aircraft leasing sector

Key takeaways from our survey and what they could mean for the aviation industry

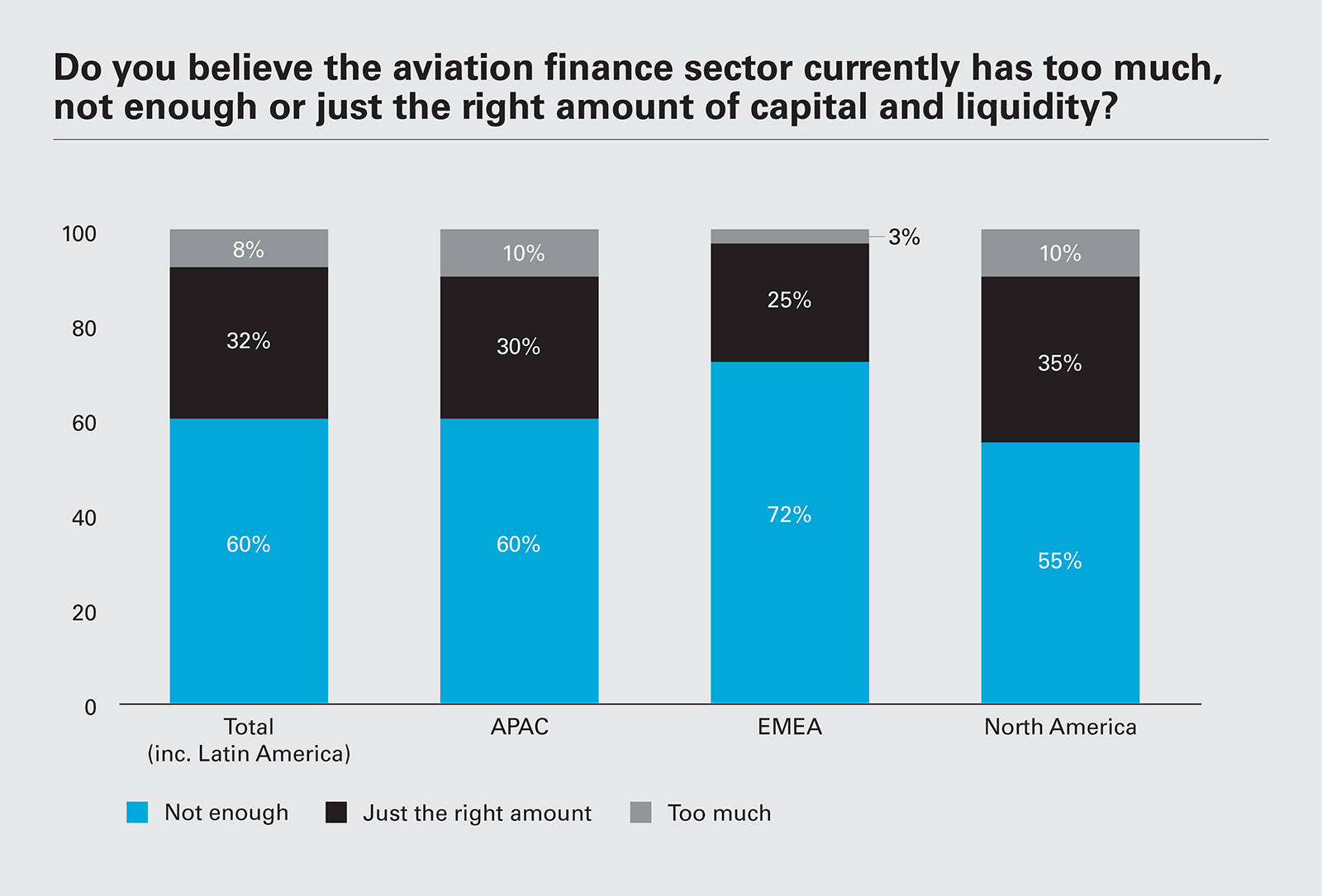

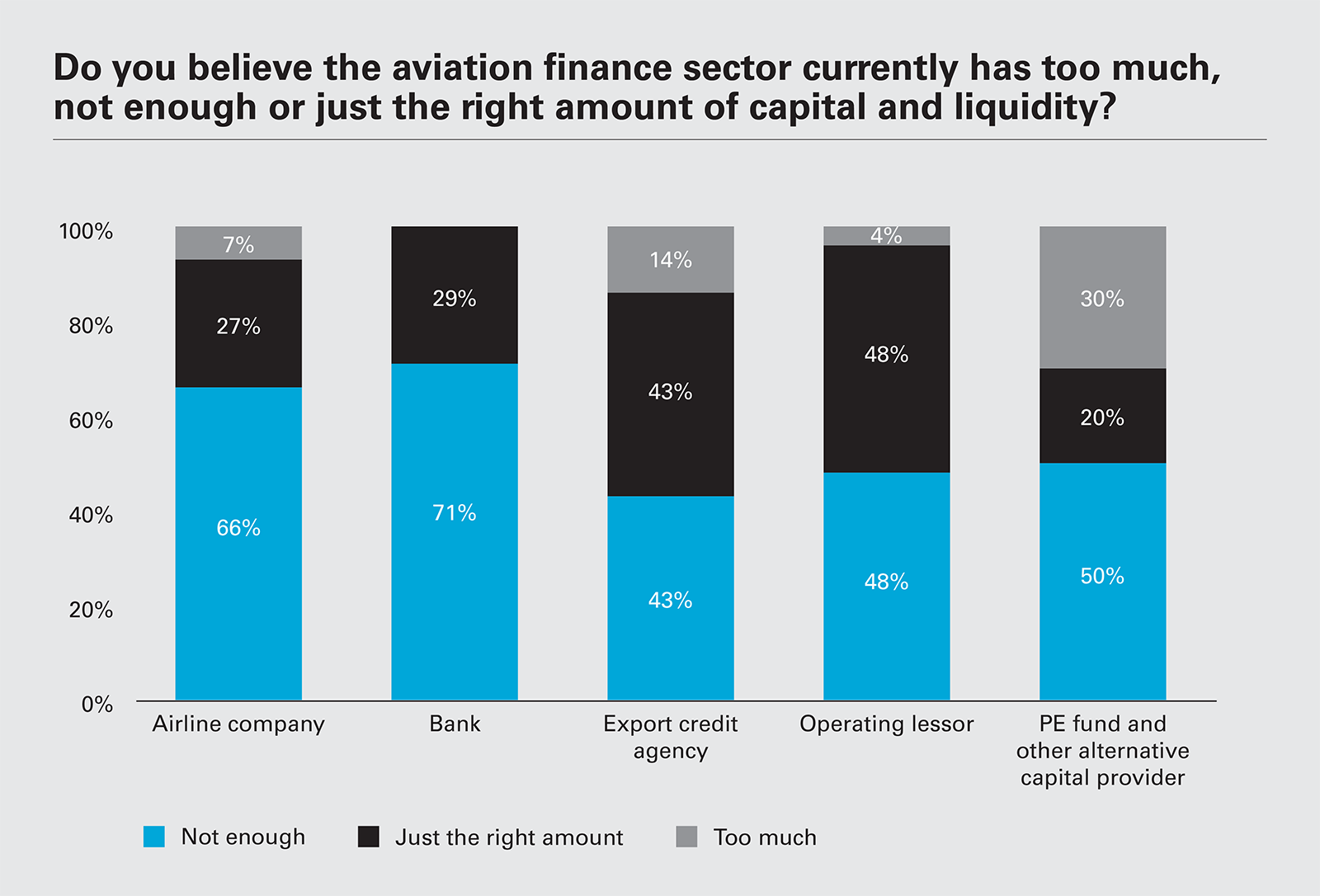

Capital and liquidity remain a primary preoccupation for the aviation sector

Looking at the current picture, 60 percent of respondents globally say that the aviation finance sector does not have enough capital and liquidity. Meanwhile, 32 percent believe that the sector has just the right amount of capital and liquidity. Only 8 percent believe there is too much capital.

Focusing on regions, EMEA-based respondents are most likely to believe that there is not enough capital and liquidity (72 percent), followed by those in APAC (60 percent). North America–based respondents are the least likely to say there is not enough capital and liquidity (55 percent)—they are also the most likely group to report that there is just the right amount (35 percent).

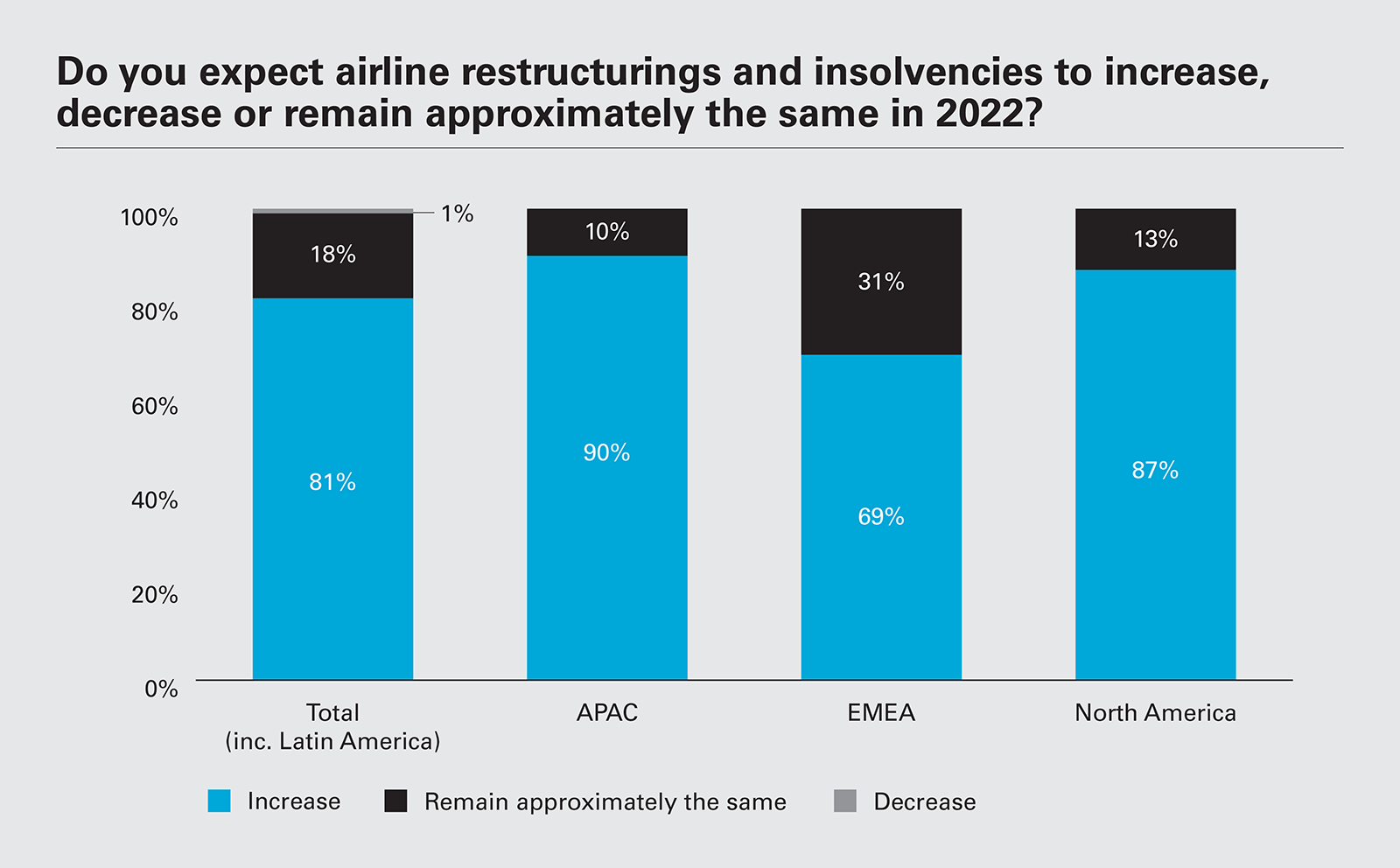

Our survey shows that a majority of respondents expect restructurings and insolvencies to increase in 2022.

Few respondents report that there is too much capital and liquidity. Historically, excess liquidity has created problems for the aviation sector, as it did toward the end of the cycle immediately pre-pandemic—a period that saw a flood of new Chinese leasing capital chasing a finite number of assets, pushing up the price of aircraft.

Private equity funds and other alternative capital providers are the respondent group most likely to say that there is too much capital and liquidity (with 30 percent saying this, compared to 7 percent of airline companies and no banks surveyed in agreement with this). With more than US$1 trillion of dry powder looking for deals, this point of view may not be surprising.

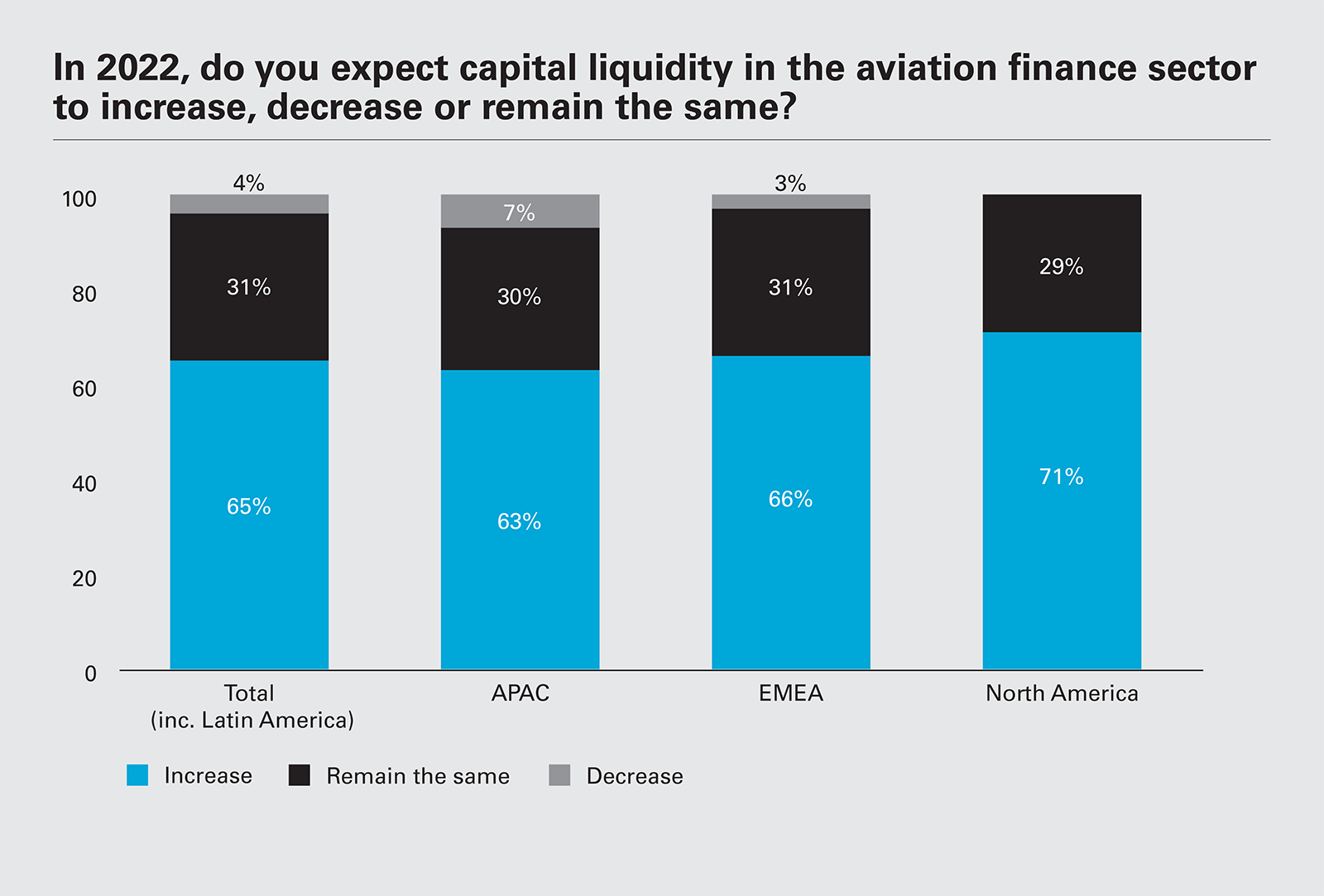

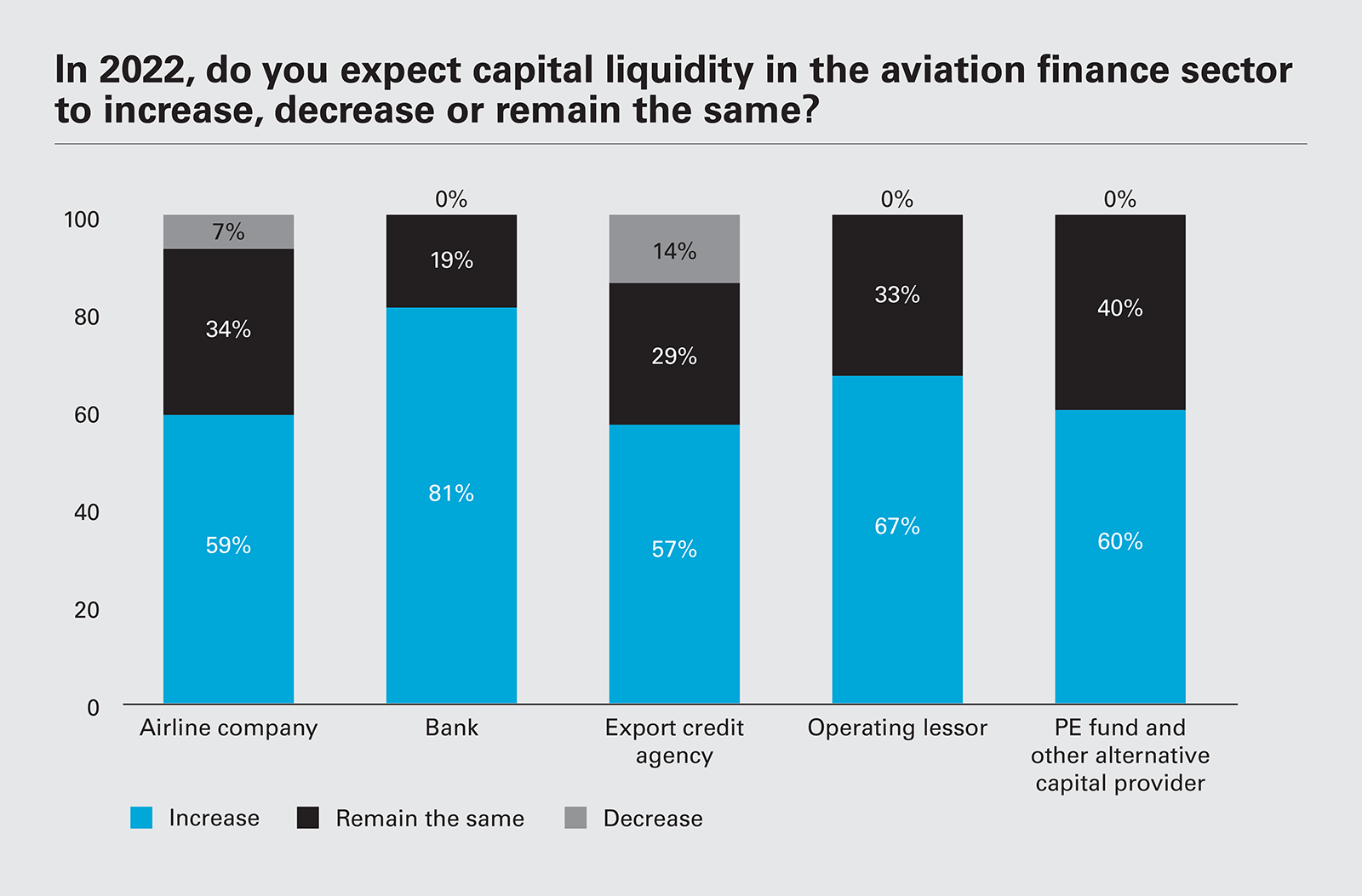

Looking ahead, majorities of respondents across all regions think that capital and liquidity in the aviation sector will rise in 2022, suggesting that the level of financing is set to improve.

Globally, nearly two-thirds (65 percent) expect capital liquidity to increase, while only 4 percent think it will fall. North America–based respondents are more likely to predict an increase (71 percent), with those in APAC less likely (63 percent). Looking at respondent types, banks are the group most likely to point to increased capital liquidity in 2022, while export credit agencies are the least likely.

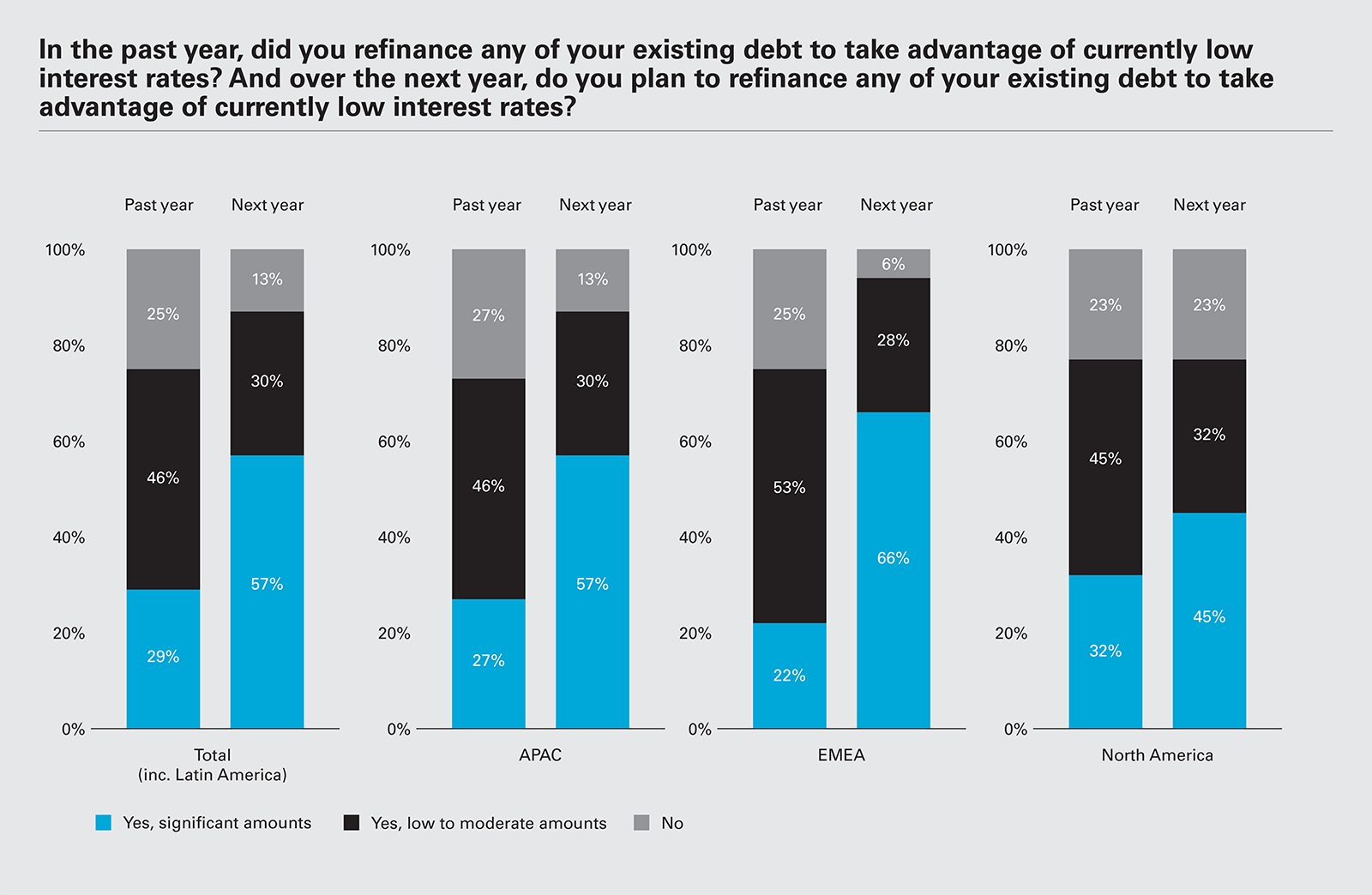

Turning to the question of refinancing, our survey suggests that on the whole, respondents were slower to take advantage of the record-low interest rates of the past year than might have been expected. Overall, only 29 percent say that they refinanced a significant amount of debt. This apparent lack of urgency may not be surprising, given the prevailing low rates and the reluctance of governments (so far) to tighten monetary policy.

Looking ahead, our survey indicates refinancing is likely to gain momentum in 2022, with 57 percent of all respondents expecting to refinance significant amounts of their existing debt and only 13 percent saying they have no plans to do so. EMEA respondents are the most interested in this course of action (66 percent expect to refinance in the year ahead), and those in North America are the least interested (45 percent).

The rising appetite for refinancing is likely linked to a number of factors. These include the need to refinance term debt as it falls due and the opportunity for refinancing driven by higher levels of M&A—a point underlined by the fact that a large majority of respondents expect to see significant airline and leasing company consolidation in 2022. Overshadowing all of this is the fact that interest rate hikes are on the horizon—although even with an increase, they could still remain near historic lows.

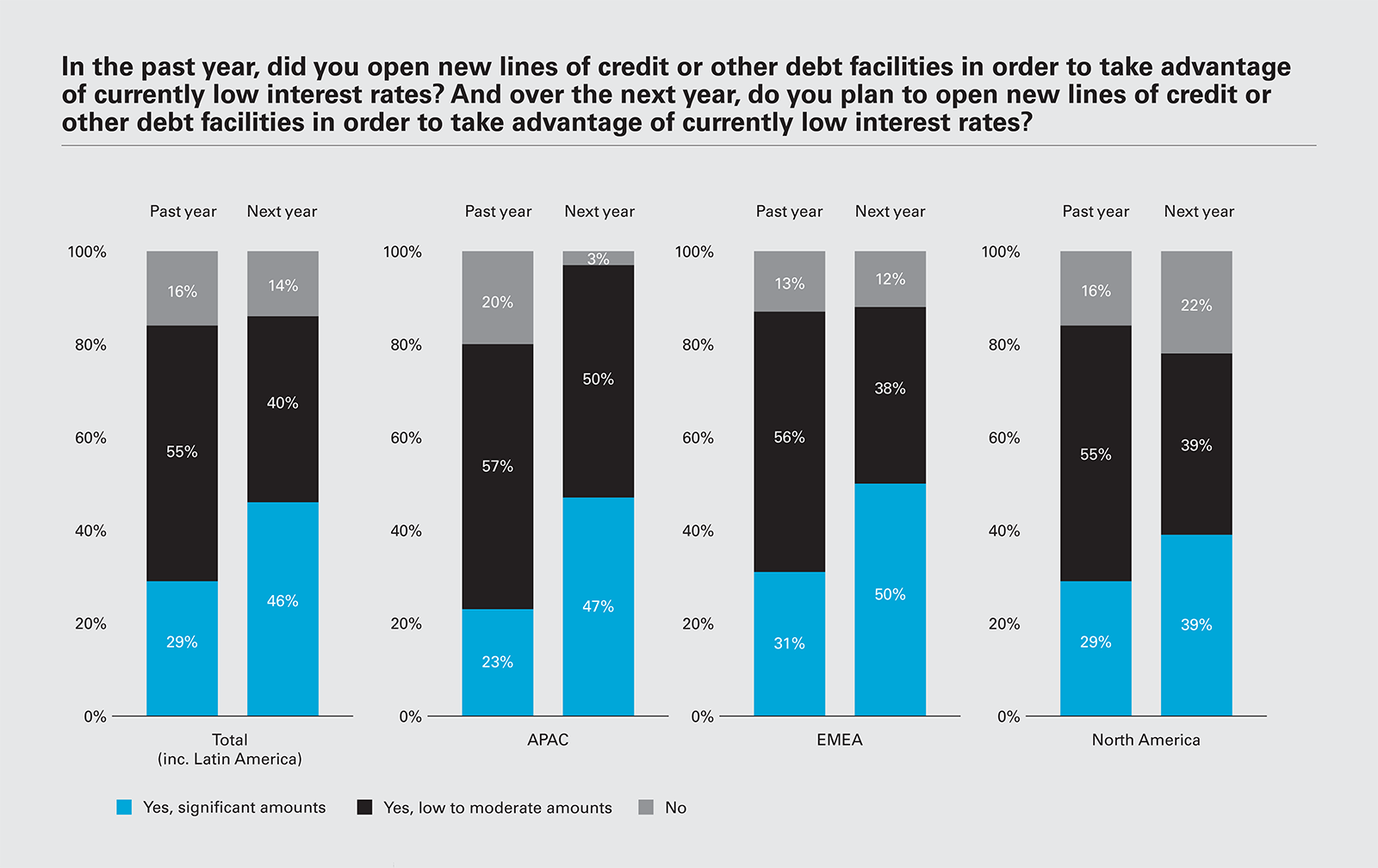

Aside from sharpening the appetite for refinancing, low interest rates also look likely to stimulate demand for new lines of credit and other debt facilities in the year ahead. While 29 percent of respondents globally say they took on "significant amounts" of new debt in the past year, 46 percent are looking to do so over the next 12 months. EMEA respondents are most likely to open new lines of credit or take advantage of debt facilities (50 percent), while those based in North America are the least likely (39 percent).

Aviation sector players are clearly confident about their continuing ability to refinance their debt and tap into new sources of funding. At the same time, there is also widespread recognition that the shakeout in aviation is still far from over. Many airlines have already been through painful restructurings, with notable chapter 11 filings in the US by Aeroméxico, Avianca and LATAM—the three most important carriers in hard-hit Latin America.

So what might 2022 have in store?

Our survey shows that a majority of respondents expect restructurings and insolvencies to increase in 2022. This opinion is prevalent in APAC, with 90 percent of respondents expecting such an increase. In large part, this reflects the fact that airlines in Asia-Pacific (along with those in Latin America) generally have not benefited from the same level of government support as airlines in Europe and North America. "The COVID-19 pandemic has affected our repayments, and the debt has mounted ever since," says the head of finance at an APAC-based airline. "We are in the process of restructuring, and this will mitigate the risk of any further loss due to the pandemic."

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: Do you believe the aviation finance sector currently has too much, not enough or just the right amount of capital and liquidity? (PDF)

View full image: Do you believe the aviation finance sector currently has too much, not enough or just the right amount of capital and liquidity? (PDF)

View full image: Do you believe the aviation finance sector currently has too much, not enough or just the right amount of capital and liquidity? (PDF)

View full image: Do you believe the aviation finance sector currently has too much, not enough or just the right amount of capital and liquidity? (PDF)

View full image: In 2022, do you expect capital liquidity in the aviation finance sector to increase, decrease or remain the same? (PDF)

View full image: In 2022, do you expect capital liquidity in the aviation finance sector to increase, decrease or remain the same? (PDF)

View full image: In 2022, do you expect capital liquidity in the aviation finance sector to increase, decrease or remain the same? (PDF)

View full image: In 2022, do you expect capital liquidity in the aviation finance sector to increase, decrease or remain the same? (PDF)

View full image: In the past year, did you refinance any of your existing debt to take advantage of currently low interest rates? And over the next year, do you plan to refinance any of your existing debt to take advantage of currently low interest rates? (PDF)

View full image: In the past year, did you refinance any of your existing debt to take advantage of currently low interest rates? And over the next year, do you plan to refinance any of your existing debt to take advantage of currently low interest rates? (PDF)

View full image: In the past year, did you open new lines of credit or other debt facilities in order to take advantage of of currently low interest rates? And over the next year, do you plan to open new lines of credit or other debt facilities in order to take advantage of currently low interest rates? (PDF)

View full image: In the past year, did you open new lines of credit or other debt facilities in order to take advantage of of currently low interest rates? And over the next year, do you plan to open new lines of credit or other debt facilities in order to take advantage of currently low interest rates? (PDF)

View full image: Do you expect airline restructurings and insolvencies to increase, decrease or remain approximately the same in 2022? (PDF)

View full image: Do you expect airline restructurings and insolvencies to increase, decrease or remain approximately the same in 2022? (PDF)