Overall investment outlook for global aviation finance

Aviation sector executives expect to maintain or increase investment in 2022, despite continuing headwinds caused by COVID-19 and concerns about the global economy

The past two years has been a period of intense turbulence for the aviation sector, with a number of bankruptcies, bailouts and collapsing revenues brought about by the coronavirus pandemic. The impact on airline receipts has been challenging. Indeed, the gap between projected and actual receipts suggests that airlines have lost passenger revenues worth nearly US$1 trillion as a result of the pandemic.

Rebuilding balance sheets and restoring passenger confidence is going to take time. Uncertainties lie ahead, and (as the rapid spread of COVID-19 variants remind us) there is no room for complacency.

Yet as this survey shows, there are also tentative grounds for optimism.

First, airlines and lessors now have access to a wider range of funding opportunities than ever before. Innovative financing is the order of the day: In addition to traditional sources, such as banks, capital markets and export credit agencies, the aviation sector is increasingly tapping into funding from alternative capital providers, including private equity and hedge funds. High- net-worth individuals and family offices are now part of the mix as well, along with new capital market products, such as green bonds.

Second—and closely linked to the evolving financing environment—is the rising awareness of environmental, social and governance (ESG) considerations within aviation. Airlines and lessors—and the investors who back them—are making the first steps towards decarbonizing aviation with initiatives that span everything from the development of sustainable aviation fuel (SAF) to the first, albeit short-range, electric aircraft.

“Uncertainties lie ahead, and there is no room for complacency. Yet as this survey shows, there are also tentative grounds for optimism.”

This matters, because the future of aviation is as much a battle for hearts and minds as it is about technology. COVID-19 has turned many of us into teleworkers, while the rise of the "staycation" has reminded travelers of the good times they can have close to home. Winning back passengers—business travelers in particular—may not be easy. Against this background, travelers of all types are increasingly aware of the environmental impact of their journeys. Seen in this light, even small steps toward boosting the green credentials of airlines could make all the difference.

The aviation sector that emerges from the pandemic is likely to look very different from the one that went into it two years ago.

But it is also a sector that is likely to be more flexible, leaner, a little greener and—above all—better adapted to whatever the future has in store.

In the fourth quarter of 2021, White & Case, in partnership with Mergermarket, surveyed 100 senior-level executives at entities that have either financed or invested in the aviation industry in the past three years. The aim of the survey was to analyze sentiment regarding aviation finance. Organizations surveyed included airlines, operating lessors, banks, export credit agencies, private equity and other alternative capital providers. Job titles included CEO, CFO, director level and heads of investment.

Aviation sector executives expect to maintain or increase investment in 2022, despite continuing headwinds caused by COVID-19 and concerns about the global economy

Our survey shows that a majority of respondents expect funding to increase in 2022—and from a wide range of sources

Capital and liquidity remain a primary preoccupation for the aviation sector

Respondents see COVID-related disruptions, economic contraction and geopolitical instability as the top challenges for the aviation sector in the coming year. But growth is expected, notably in Asia-Pacific and Australasia

Flexibility in the ascendant aircraft leasing sector

Key takeaways from our survey and what they could mean for the aviation industry

Aviation sector executives expect to maintain or increase investment in 2022, despite continuing headwinds caused by COVID-19 and concerns about the global economy

The year 2021 was another turbulent one for aviation, as governments raced to combat new COVID-19 variants with travel bans and border closures. From the rise of the Delta variant in the first half of the year to the first appearance of Omicron at the end, 2021 was a year in which disruption lurked around every corner.

Despite this, passenger demand began to recover. Estimates published by IATA suggested that total revenues from global commercial airlines were likely to reach US$472 billion in 2021.1 While this is far below the US$838 billion revenue total achieved on the eve of the pandemic in 2019, it represents an increase of more than 26 percent compared with 2020. Scheduled passenger numbers also staged a recovery. The passenger total for 2021 is expected to reach 2.27 billion—a huge improvement on 2020 (1.8 billion), but still far short of 2019's 4.54 billion.

While passenger traffic has been hit hard by the pandemic, air cargo shines as a rare COVID-19 success story. The rapid reboot of economies and the race by businesses to obtain—along with bottlenecks in ocean shipping—helped to propel airfreight to new heights. The year ahead could be a record breaker with expected air cargo revenues of US$175 billion (compared with US$128.8 billion in 2020 and US$100.8 billion in 20192).

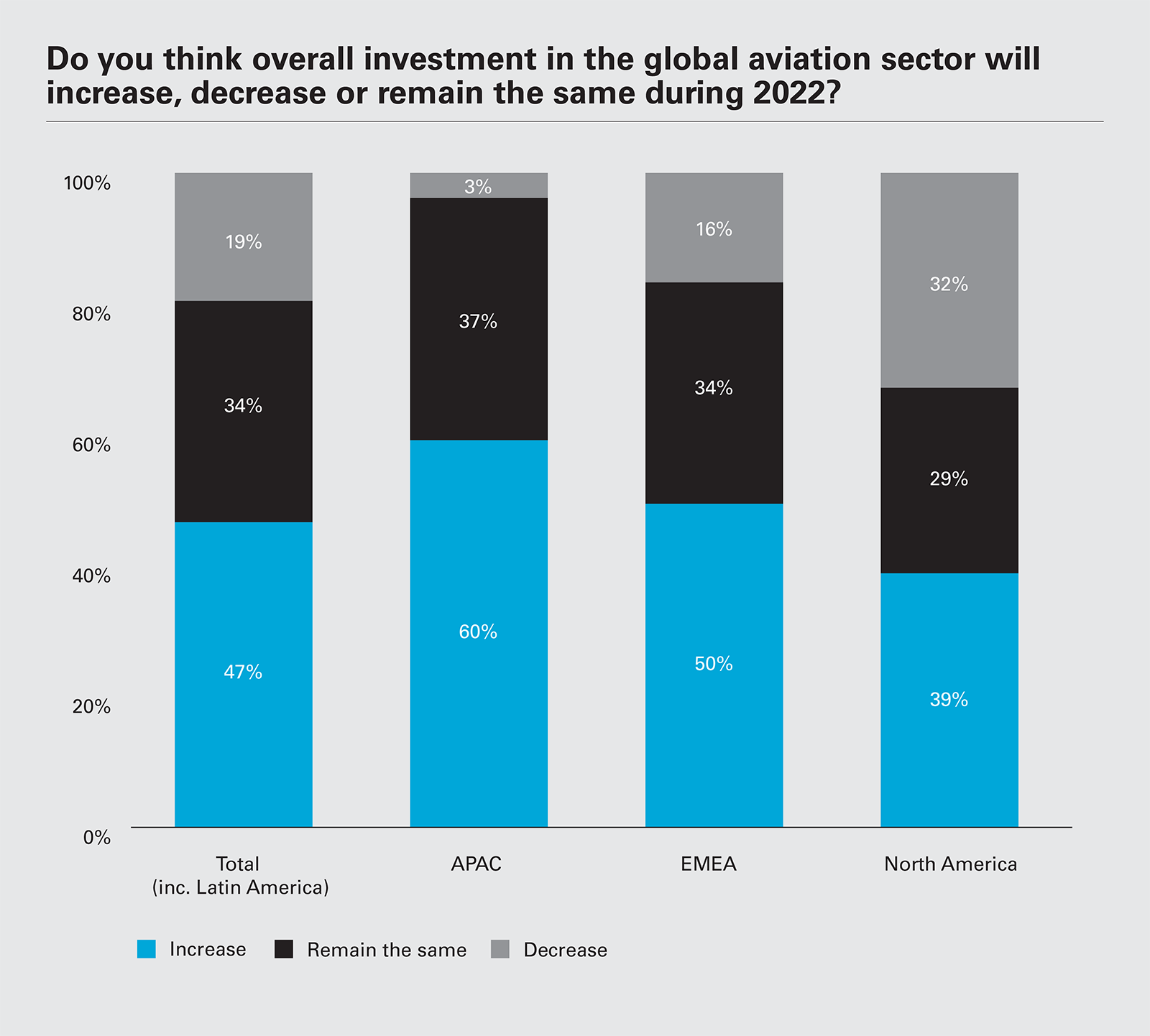

47%

of respondents expect investment

in the global aviation sector to increase in 2022

Our survey found that respondents are cautiously optimistic. Looking first at expectations for the global aviation sector as a whole, 81 percent expect that investment will be maintained or increased in 2022, with 47 percent suggesting an increase. Only 19 percent of respondents expect aviation investment to decrease.

Asia-Pacific stands out as the region where sentiment is most positive, with 60 percent expecting global aviation sector investment to rise in the year ahead—the highest of any region. From the perspective of APAC, this positive sentiment may not be surprising: The region's growing middle class and favorable demographics support growth in the aviation sector. A managing director of a leading APAC-based bank says: "Investments will increase in 2022, because there are fresh prospects for growth in the aviation sector. The investments will derive optimum returns, because development is taking place in many locations. This will stabilize the sector and help growth."

Respondents in the more mature markets of EMEA and North America are more cautious, with 50 percent and 39 percent, respectively, anticipating increased investment in the year ahead—somewhat lower than APAC. That said, a number of respondents in these regions have an eye on emerging opportunities—notably investments in decarbonization.

"The project pipeline looks promising," says the head of investment and capital markets at a North America–based lessor. "There are many green funds emerging that will support these projects." The managing director of an EMEA-based bank that invests US$1 to US$5 billion per year in aviation adds: "The emphasis on ESG will prompt younger-generation investor audiences to invest."

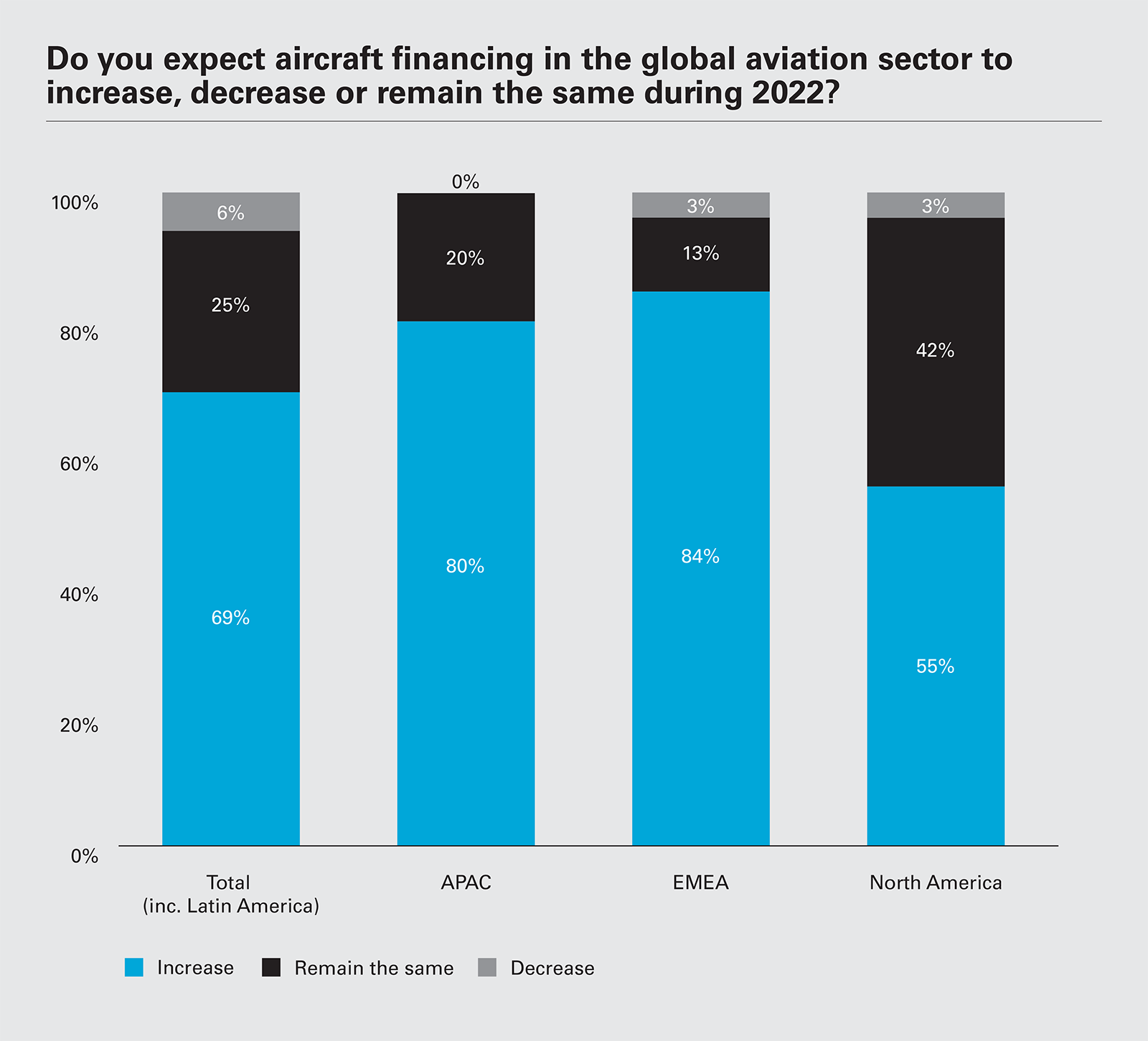

Turning to aircraft financing, respondents are upbeat about the year ahead. Globally, 69 percent expect aircraft financing in the global aviation sector to increase in 2022.

69 percent expect aircraft financing in the global aviation sector to increase in 2022.

Looking more closely at specific regions, EMEA-based respondents have the most positive outlook, with 84 percent pointing to a rise in financing, followed by APAC with 80 percent. Notably, no respondents in APAC expect aircraft financing to decrease in the year ahead. North America–based respondents are less optimistic, with only 55 percent expecting aircraft financing globally to rise in 2022.

Future increases in aircraft financing will be determined, primarily, by the extent to which passenger numbers recover. But both survey data and comments by respondents suggest that there are two new factors in play as well.

The first of these is the need to boost the efficiency and environmental performance of aircraft fleets against a background of rising ESG imperatives. This point was made by a number of respondents, including airlines, lessors, banks and alternative capital providers. "I expect aircraft financing to increase because equipment upgrades are required," says the partner of an APAC-based PE firm. "Older aircraft will have to be replaced because they have a high level of fuel consumption." This point is echoed by the CEO of an EMEA-based lessor who expects spending on aircraft development to rise: "Post pandemic, the emphasis on low-carbon aircraft will increase further."

The second factor is the rise of new sources of financing. Banks—traditionally a mainstay of aviation financing—have reduced their exposure to the sector since the onset of the pandemic. The vacuum they have left behind is being filled with everything from green bonds to private equity. Indeed, the past two years has seen an upsurge in private equity and hedge fund activity. Armed with ample dry powder, buyout firms have been on the hunt for opportunities, from debtor-in-possession loan financings, to setting up aircraft leasing companies. "Many private equity firms have started collective funds for aircraft financing," says the managing director of an EMEA-based bank. "Sustainable development goals in particular have been an important part of their decision to support the low-carbon transition in the aircraft industry."

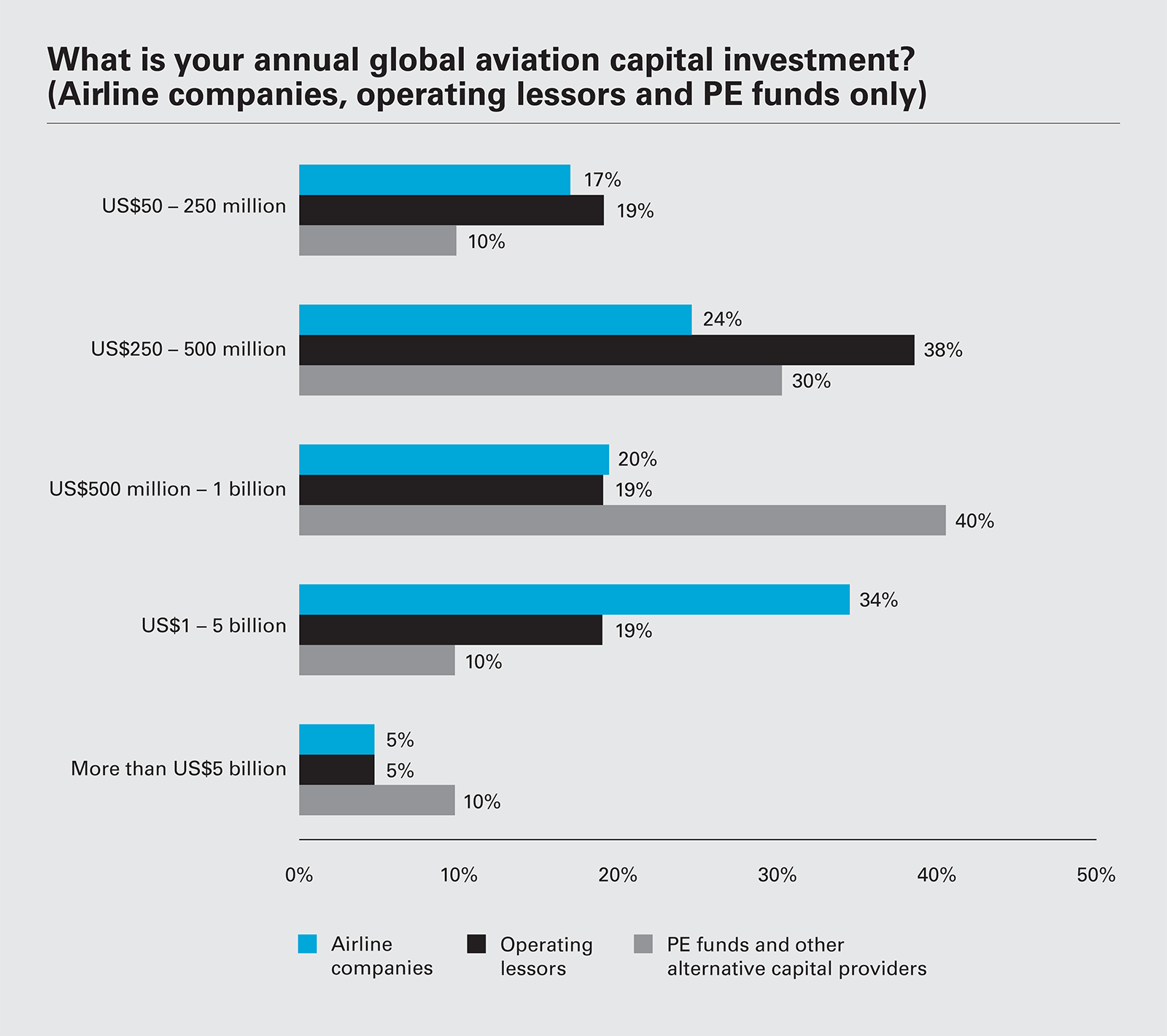

The ability to tap into wider and deeper pools of capital bodes well for the aviation sector. But our survey data shows that the distribution of investments by airlines, lessors and PE funds has shifted since the peak of the cycle, with a trend towards higher volumes of lower-value investments, reflecting changing risk appetites.

An interesting feature of this shift is that private equity and other alternative capital providers are now competing right across the value spectrum—10 percent currently invest in the US$50 to US$250 million bracket at one end, while another 10 percent are investing in the US$5 billion-plus bracket at the other. This is a broader spread than has been seen in the past. At the same time, the proportion of operating lessors making high-value investments has declined, with just under a quarter (24 percent) currently investing US$1 billion or more. In a similar vein, fewer airline companies currently invest more than US$5 billion, down from previous years.

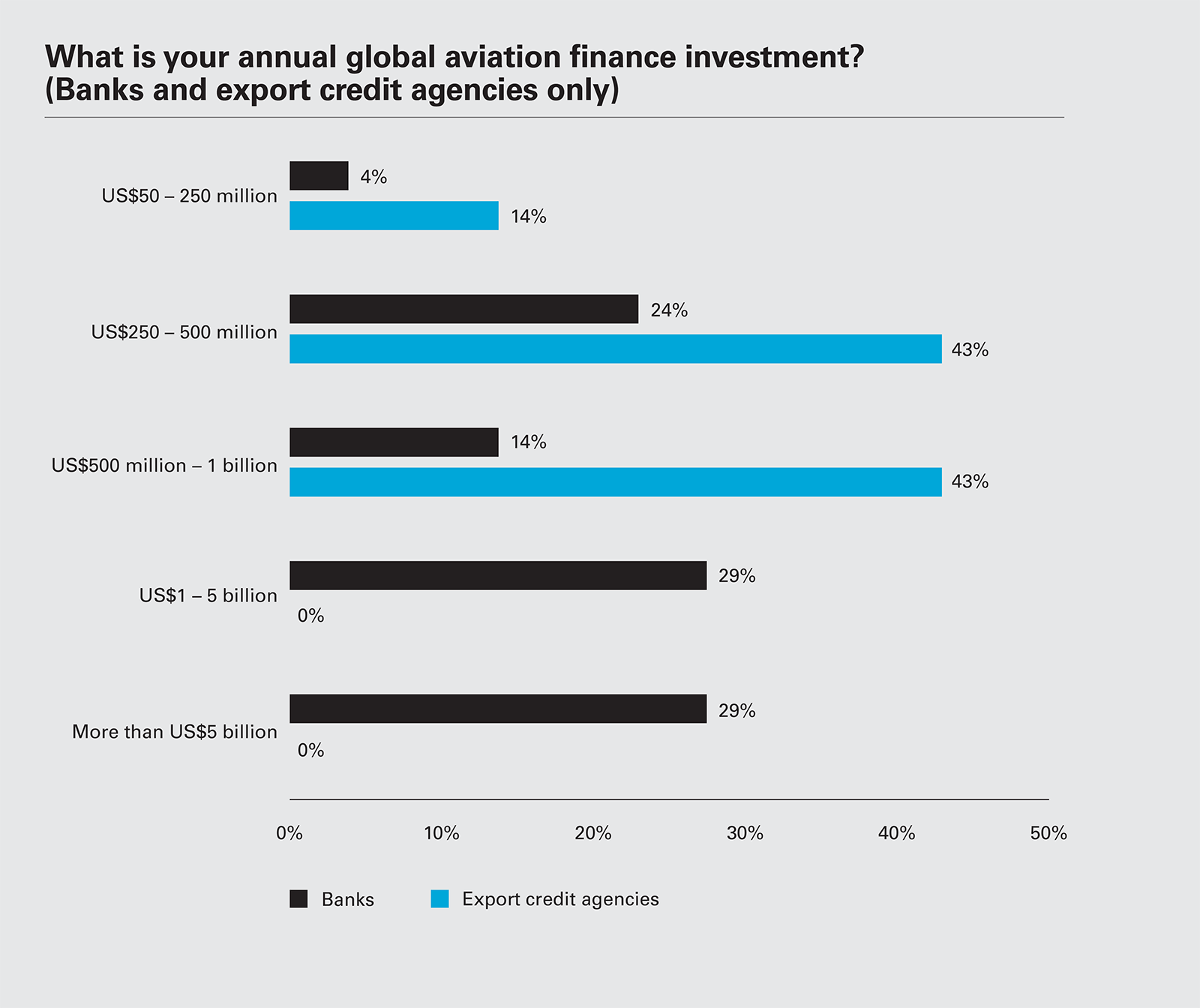

Bank and export credit agency (ECA) financing has also changed, with respondents reporting less activity at the higher end of the value spectrum. For example, our survey shows that ECAs have stepped back from making the highest-value allocations, with no respondents providing finance in either the US$1 to US$5 billion or US$5 billion-plus categories. Bank lending has tended to be more consistent, and the proportion of respondents who report lending in the highest bracket (more than US$5 billion) is only marginally less than the pre-pandemic level.

1 IATA Industry Statistics Fact Sheet: https://www.iata.org/en/iata-repository/pressroom/fact-sheets/industry-statistics/

2 IATA Cargo Market Analysis: https://www.iata.org/en/iata-repository/publications/economic-reports/air-freight-monthly-analysis---october-2021/

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: Do you think overall investment in the global aviation sector will increase, decrease or remain the same? (PDF)

View full image: Do you think overall investment in the global aviation sector will increase, decrease or remain the same? (PDF)

View full image: Do you expect aircraft financing in the global aviation sector to increase, decrease or remain the same? (PDF)

View full image: Do you expect aircraft financing in the global aviation sector to increase, decrease or remain the same? (PDF)

View full image: What is your annual global aviation capital investment? (PDF)

View full image: What is your annual global aviation capital investment? (PDF)

View full image: What is your annual global aviation finance investment? (PDF)

View full image: What is your annual global aviation finance investment? (PDF)