Mining & metals 2022: ESG and energy transition – the sector's biggest opportunity

Against a backdrop of record commodity prices and the pressure for miners to boost their ESG credentials, the sector is seeking to position itself as a trusted partner in fighting climate change. Will 2022 cement the mining & metals industry’s role as a central plank of the energy transition?

14 min read

Subscribe

Stay current on your favorite topics

US$ 1,822.16

Gold price per ounce, January 26 2022

For the mining & metals industry, 2021 will be remembered for two very clear themes. First, the stunning recovery from the COVID-19 pandemic that sent commodity prices soaring to levels never seen before. Second, that ESG has anchored itself as a mainstream aspect of business and will remain top-of-mind in the boardroom.

While the industry proved itself remarkably resilient to the initial shock of the pandemic, 2021 highlighted that it was also well positioned to profit from the global recovery. As trillions of dollars of global stimulus fueled a rebound in both industrial and consumer demand, commodity prices surged. Copper, iron ore and lithium all hit records, alongside coal and natural gas. After years of streamlining businesses and being intensely disciplined in bringing on new supply, miners were able to deliver record profits and hand back bumper dividends to shareholders.

Despite the record prices, it also became clear that ESG—which has been growing in prominence in our last two surveys—is now central in terms of both attracting investors and holding a social license to operate. Companies that have focused their attention on their ESG performance are seeing the benefits.

So, what should we expect in 2022? To get an idea, White & Case has conducted its sixth annual survey of industry participants, with 63 senior decision-makers sharing their thoughts for the year ahead.

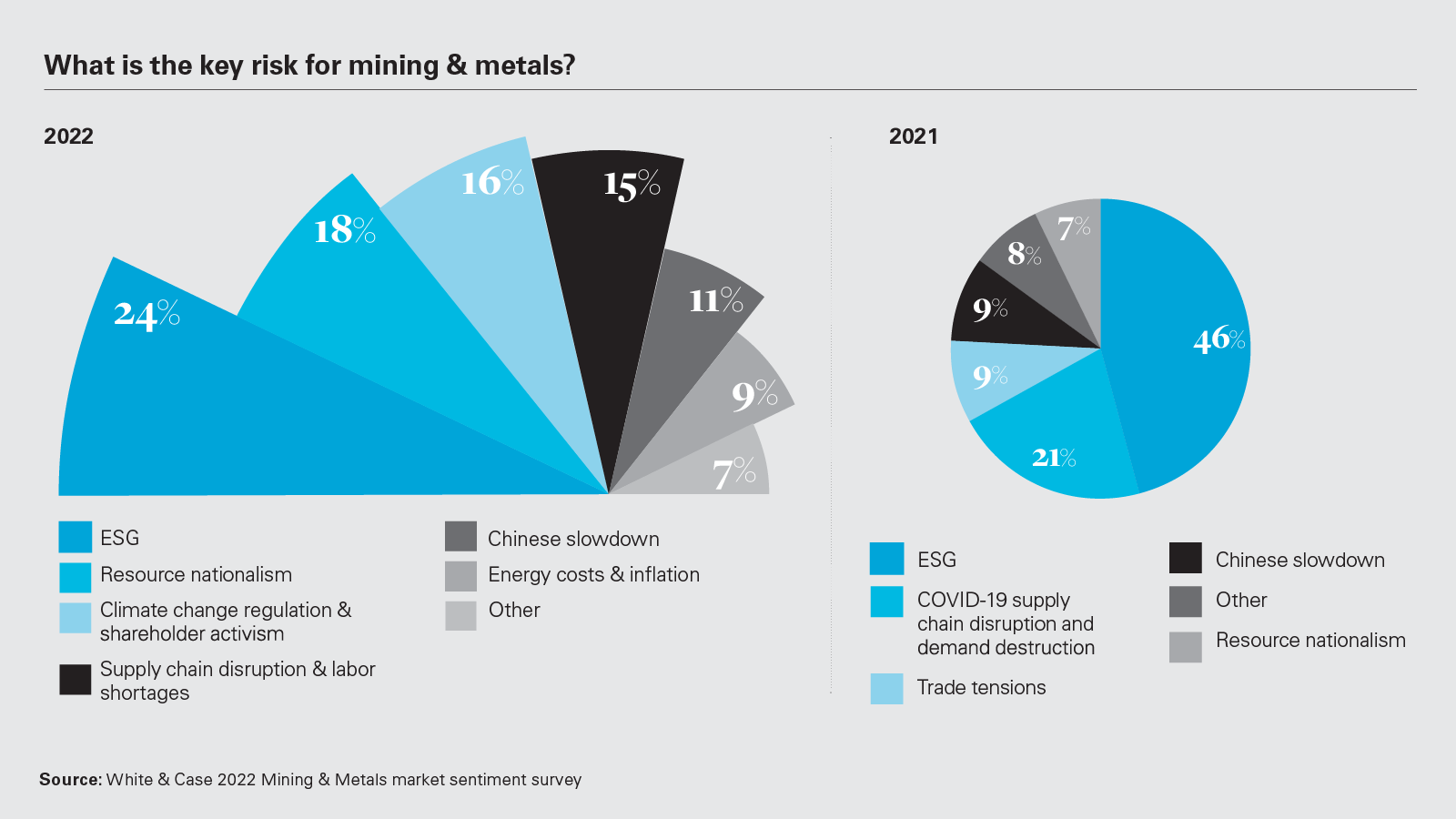

View full image: What is the key risk for mining & metals? (PDF)

View full image: What is the key risk for mining & metals? (PDF)

While the mining & metals industry proved itself remarkably resilient to the initial shock of the pandemic, 2021 highlighted that it was also well positioned to profit from the global recovery

ESG's prominence lays platform

The mining industry has found itself caught between two competing themes when it comes to ESG. On one side comes the continued pressure from mining fossil fuels and the recent disasters that have done considerable damage to the entire industry's reputation, such as the fatal dam collapse in Brazil and the destruction of ancient aboriginal heritage sites in Australia. More positively, however, is how the industry has become increasingly adept at making the argument that it is becoming a far cleaner—and more sustainable sector, and with this improved ESG performance—it can be a reliable and trusted partner to mine the materials that will enable the green transition. This shift opens up opportunities for the industry going forward, provided individual players can demonstrate their ESG credentials in all respects.

For the second year in a row, respondents to our survey state that ESG issues remain a considerable risk to the sector in 2022, with 24 percent viewing it as the biggest threat, rising to approximately 40 percent when climate-related activism and regulation is included. While not necessarily a surprise, an increasingly sophisticated conversation is happening and companies are recognizing that opportunity exists for those companies effectively managing this risk. Other risks are also elevated compared to 2021, with resource nationalism doubling to 16 percent, followed by supply chain disruption and a Chinese slowdown.

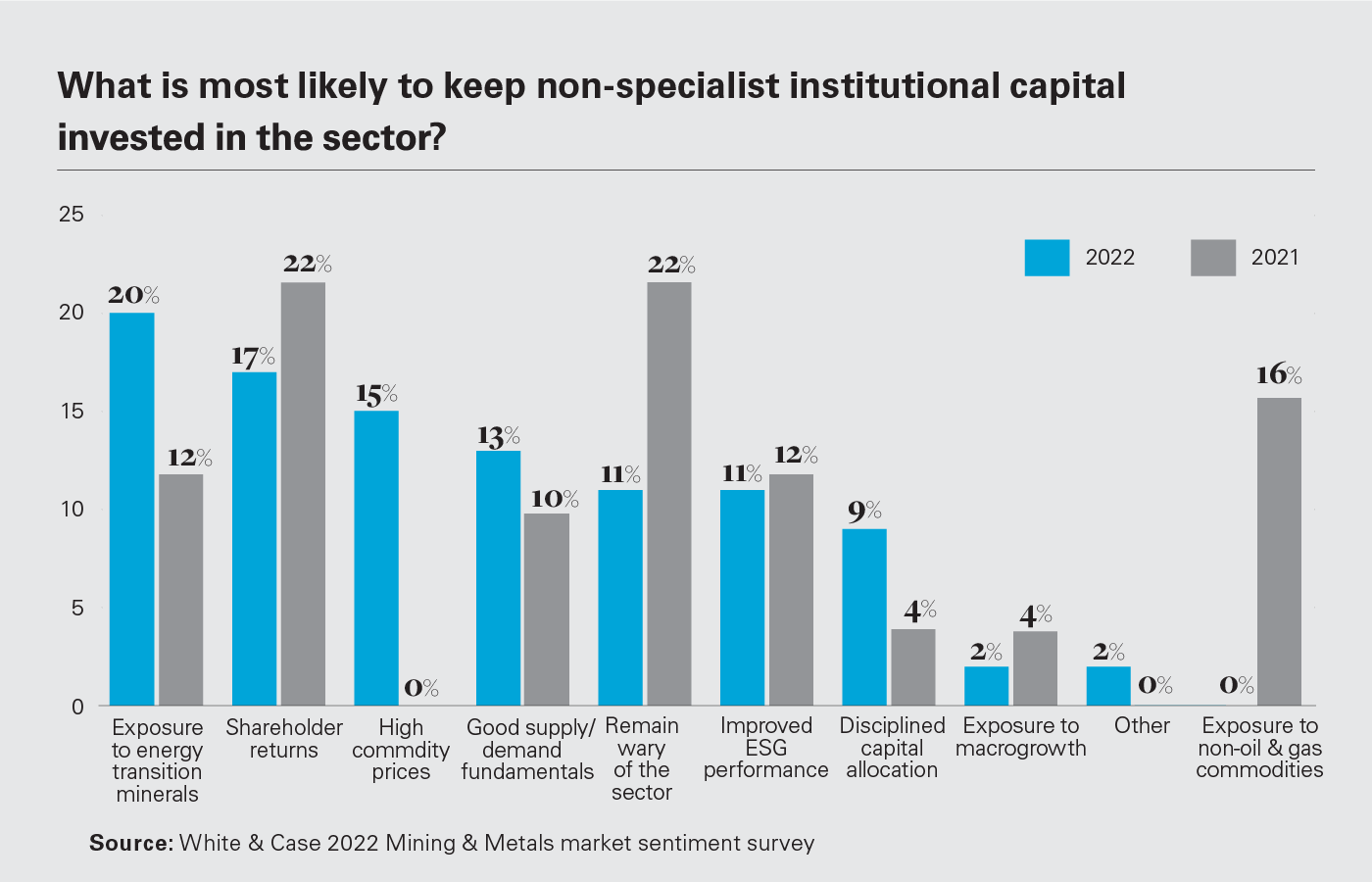

View full image: What is most likely to keep non-specialist institutional capital invested in the sector? (PDF)

View full image: What is most likely to keep non-specialist institutional capital invested in the sector? (PDF)

Showcasing green credentials

The opportunity for the sector is clear. End-users, especially those pushing energy transition agendas, such as the electric vehicle makers, want to be able to tell consumers that the materials they use come with impeccable ESG credentials. That's created the opportunity for the mining sector to position itself as a trusted partner in fighting climate change. In 2021, we saw BHP sign a nickel supply agreement with Tesla, with the two companies saying they would work together to make the supply chain cleaner. Tesla's chief executive, Elon Musk, has repeatedly called for a sustainable supply of the materials, with battery demand expected to grow 500 percent over the next decade, according to BHP.

This trend has been repeated across the metals industry. Rio Tinto is working to produce carbon-free aluminum, partnering with consumers such as Apple, while Glencore has also struck a cobalt supply deal with Tesla.

Lenders are also considerably more willing to finance projects that meet these criteria. In particular, we are seeing government agencies stepping in to help ensure the supply of minerals critical to the energy transition.

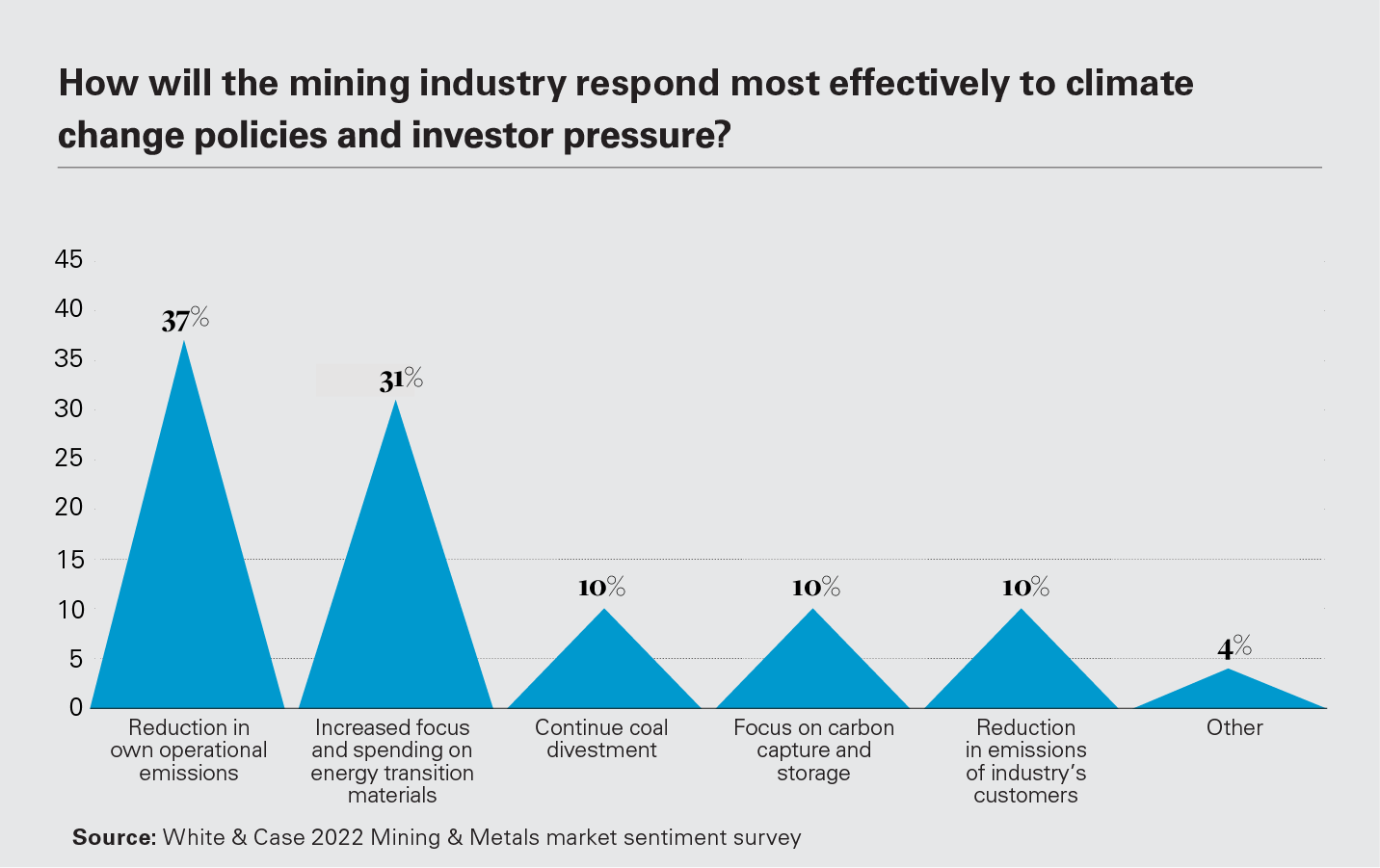

View full image: How will the mining industry respond most effectively to climate change policies and investor pressure? (PDF)

View full image: How will the mining industry respond most effectively to climate change policies and investor pressure? (PDF)

Moving on from the pandemic

Despite many challenges still facing the sector, from inflationary pressure, resource nationalism and continued trade disruptions, it's clear that boards are focusing on the opportunity presented by the global energy transition. This view is reinforced by our survey, which shows that responding to the challenges of climate change and the energy transition should be the number-one priority for the industry this year, at more than double last year's 12 percent tally. Yet another takeaway is the relatively even spread of responses, with supply chains, growth and productivity all relatively prominent. After the challenges wrought by the pandemic, perhaps the industry is finally able to return to more traditional issues this year.

Moving on is certainly what the majors have been doing, and it has been rewarded. Ever since the commodity crisis of 2015 and 2016, when some of the biggest names in the industry came close to collapse, the mining sector struggled to regain its position with generalist investors. Yet in 2021, the industry showed it has two compelling offerings to investors: unprecedented cash returns and the ability to position itself as a supplier of materials needed to combat climate change.

In light of looming tightness in supply in various key energy transition minerals, it will be interesting to see if investment for growth draws greater prominence as a priority over the course of 2022—something to watch for our 2023 survey results.

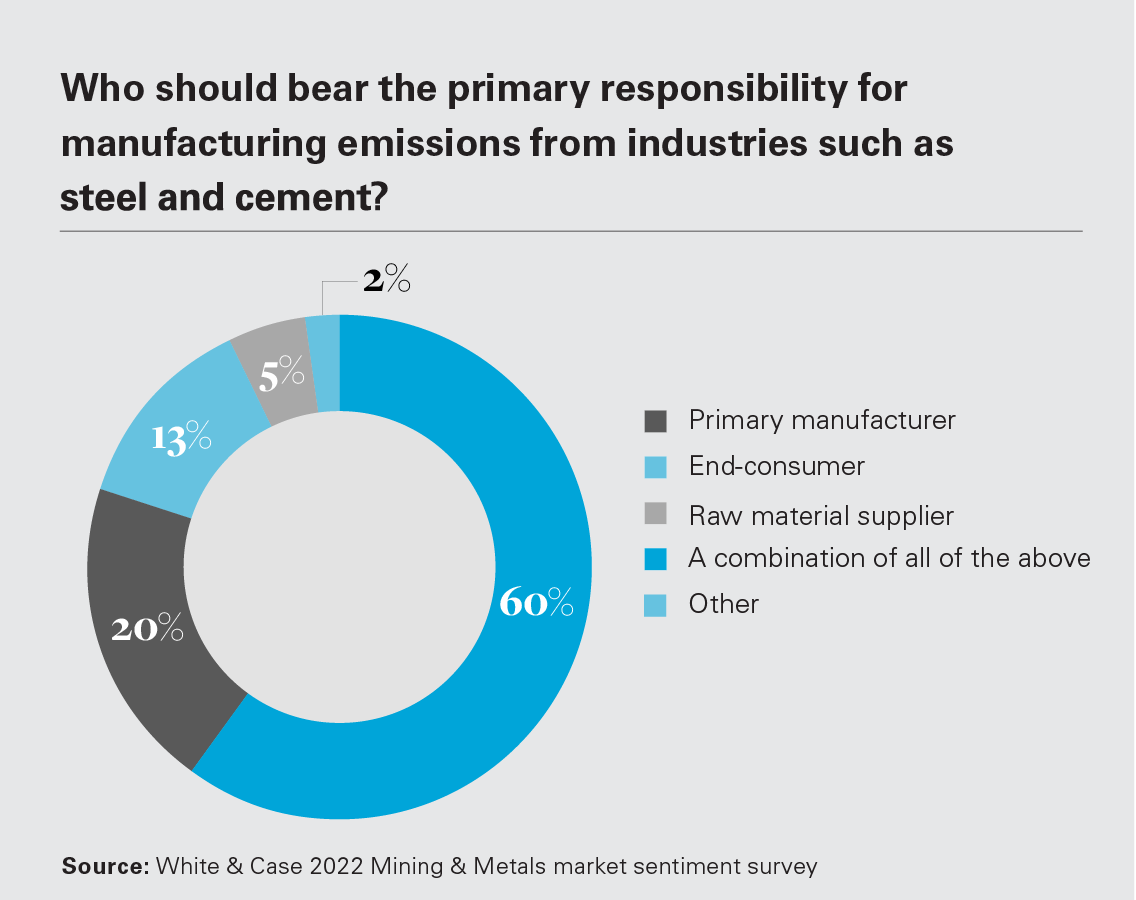

View full image: Who should bear the primary responsibility for manufacturing emissions from industries? (PDF)

View full image: Who should bear the primary responsibility for manufacturing emissions from industries? (PDF)

588,000 tonnes

Total global production of lithium, measured as lithium carbonate equivalent, is forecast at 588,000 tonnes for 2022Source: Credit Suisse

Energy transition materials even more in focus

This status is reflected in our survey, with 20 percent saying that exposure to such commodities is the best way to draw in new investors, almost double last year's response. The second and third most popular answers were shareholder returns and high commodity prices, illustrating that these themes are working in tandem.

In terms of supplying energy transition materials, the sector can be split into two categories: those with pure exposure—such as lithium miners—and the larger diversified companies that produce both forward-looking materials and more traditional commodities, such as iron ore.

The diversified miners accelerated their transition in 2021. BHP announced it was exiting oil & gas and continued to move away from thermal coal, while Anglo American exited thermal coal altogether. Vale also announced its exit from the coal market as part of its commitment to become carbon-neutral by 2050 and reduce one-third of its emissions by 2030. In its place, the biggest miners have been pushing aggressively into future-facing materials. Rio Tinto sanctioned a US$2.4 billion lithium project in Serbia (which now faces significant local challenges—linking into our respondents' growing concerns about resource nationalism in the sector) in addition to announcing the purchase of the Rincon brine project in Argentina. BHP sanctioned a giant new potash project, and has been actively looking to buy new copper and nickel assets, most recently investing in Tanzania's Kabanga nickel project early in 2022.

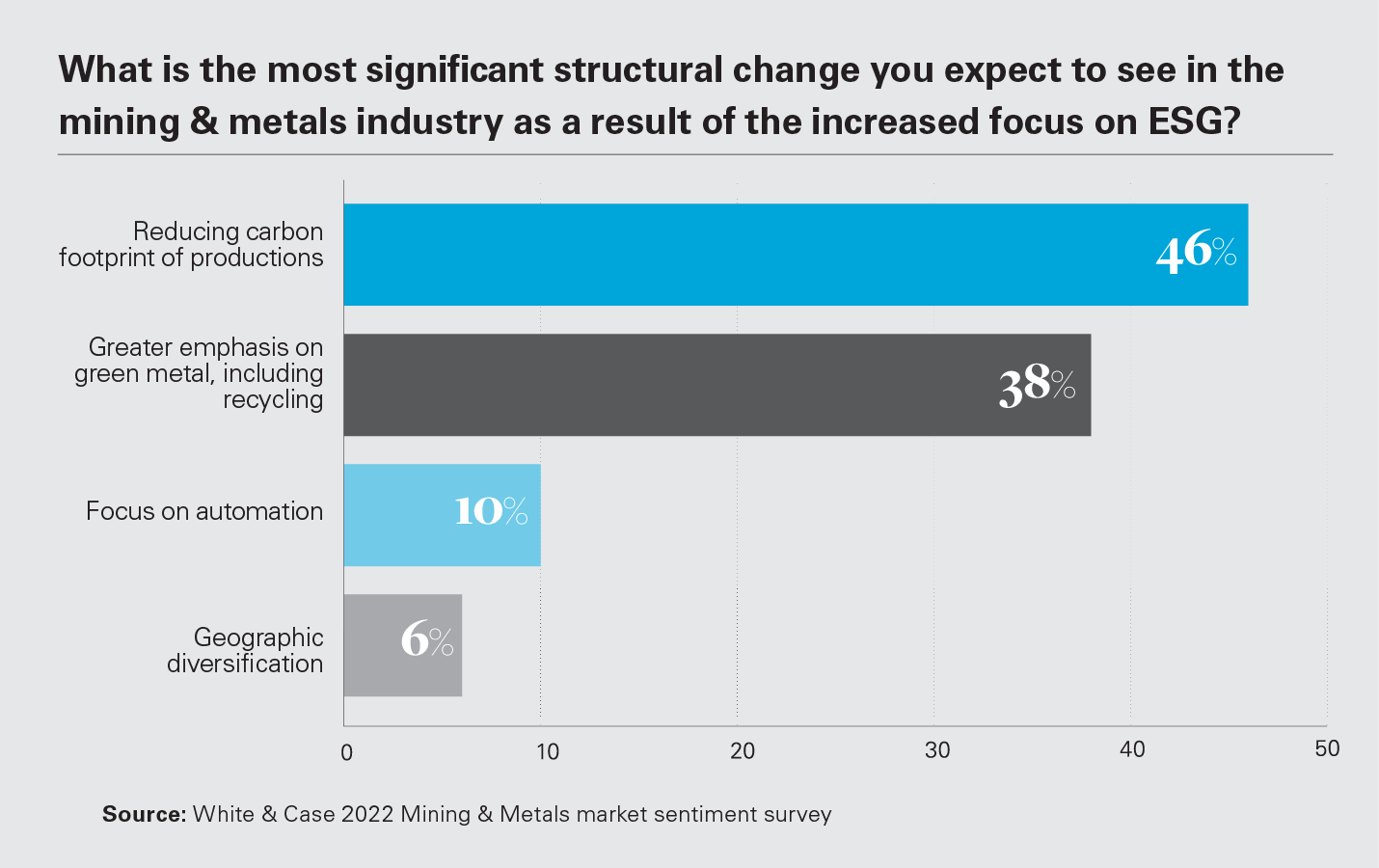

View full image: What is the most significant structural change you expect to see in the mining & metals industry? (PDF)

View full image: What is the most significant structural change you expect to see in the mining & metals industry? (PDF)

Committing to the global clean-up

While the mining industry is able to tell a compelling story explaining its role in the materials it produces, the impact of its operations remains a hurdle. Scope 1 and Scope 2 emissions—when pollution is created by the miners' operations, and Scope 3—the pollution created when the materials they mine are used by their customers—remain significant obstacles for many investors.

Last year saw nearly every major miner commit to becoming carbon-neutral at their own operations over the next two to three decades, and perhaps more importantly, details on how they intend to get there. Most striking was Rio Tinto's pledge to spend US$7.5 billion to halve its own emissions by the end of this decade. The scale of the investment to future-proof its business rather than drive immediate shareholder returns shows just how seriously the industry is taking it, but also the scale of the costs involved.

Our survey suggests this is the right approach, with 37 percent of respondents stating that cutting their own emissions is the most effective way for miners to respond to climate change. Significantly, placing increased focus and spending on energy transition materials came in a strong second with 31 percent, up from just 6 percent a year earlier, further demonstrating the importance of—and opportunity presented by—investing in more future-facing commodities.

US$ 9,955

Copper price per tonne, London Metal Exchange, January 26 2022

Recycling becomes more viable

Going hand-in-hand with this drive to reduce emissions is an accelerating push toward recycling, both from already-processed metals and tailings dumps on mine sites. Some 38 percent of our respondents see increased recycling as a key structural shift that the industry can undertake to burnish its ESG credentials. Although early-stage, this has begun to play out with miners and downstream players seeking to build on the opportunity.

Glencore has been steadily increasing its recycling capacity, especially for electronic waste, while BHP and Freeport have invested in Jetti Resources, a US startup that says it can process millions of tons of copper from existing waste dumps. There have also been advances in green steel technologies, fueled by innovative investments from miners and steel producers. We expect these trends to accelerate further in the coming years as technologies improve, especially if commodity prices continue to rise.

Expect consolidation within battery minerals

Since the big gold deals of a couple of years ago, major M&A has come to a halt in the mining space. But in its place has been a steady repositioning of portfolios. Anglo American, South 32, Vale and BHP are among companies that have reduced fossil fuels from their portfolios, predominantly by way of spinoffs or trade sales. To replace those assets, the miners are increasingly looking to take stakes in junior miners sitting on forward-facing commodities such as copper, nickel and lithium.

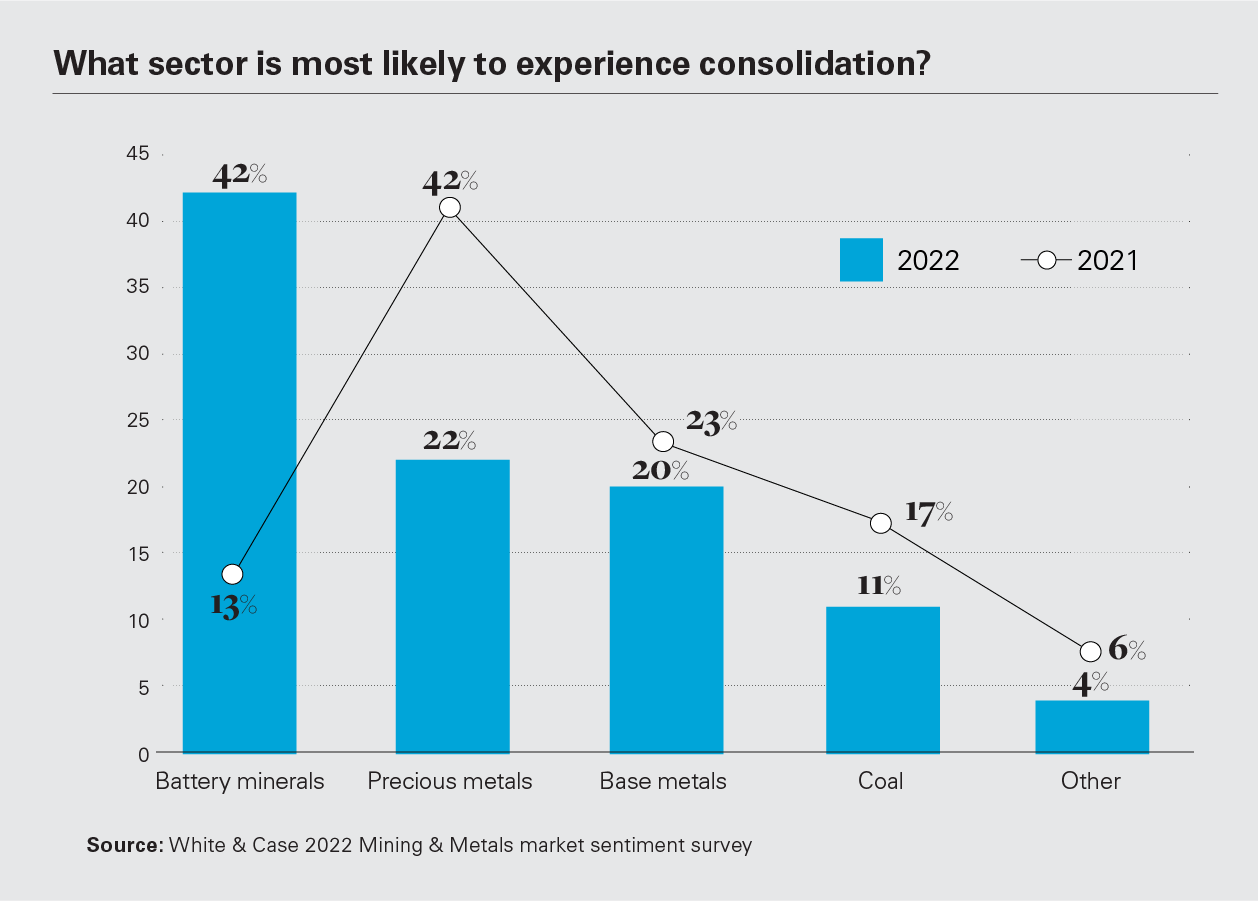

There was a small window at the start of the pandemic, when equity values plummeted, but now with many of the miners trading near record highs, transformational M&A looks to be an unlikely prospect. According to our survey, that means opportunistic deals remain the most likely, especially as portfolios continue to shift toward more ESG-friendly commodities. Some 42 percent of respondents expect consolidation in the battery minerals space this year, up from only 13 percent a year ago.

View full image: What sector is most likely to experience consolidation? (PDF)

View full image: What sector is most likely to experience consolidation? (PDF)

Latin America emerges as a key resource nationalism hotspot

Resource nationalism has long been a concern for the mining industry. When prices rise, such as last year, so do government and societal demands. Yet a notable change in 2021 was the increase in ESG-related nationalism, with an expectation for miners to maintain a social license to operate. This resulted in rising tensions with local communities around the world.

Last year, Latin America came to the fore on this issue, especially after the election of left-wing governments in Peru and Chile, two of the world's most important copper-producing nations. In our survey, 39 percent said they expect Latin America to be the region most affected this year, up from 14 percent last year, and putting it on a par with Africa.

This shift is likely to be driven by both more left-wing governments, but also increasing tension with host communities. The giant Antamina copper and zinc mine was forced to shutter last year as protestors blocked roads, saying the mine had not lived up to its commitments to the local population. Silver miner Hochschild also saw its shares collapse, when the new Peruvian government threatened to block mine extensions after protests from local communities. Further north in Colombia, authorities shelved AngloGold Ashanti's request for an environmental license, with locals opposing the Quebradona project.

The recent announcement by Serbia that it has revoked Rio Tinto's exploration licenses for the proposed Lithium mine in Serbia, shows that permitting/country risk abounds even in Europe, which is simultaneously trying to position itself as the leading economic bloc in the energy transition.

View full image: What impact are trade tensions likely to have? (PDF)

View full image: What impact are trade tensions likely to have? (PDF)

The opportunity is right here, right now, but the mining & metals sector needs to get this right to cement its position as a central plank of the entire energy transition

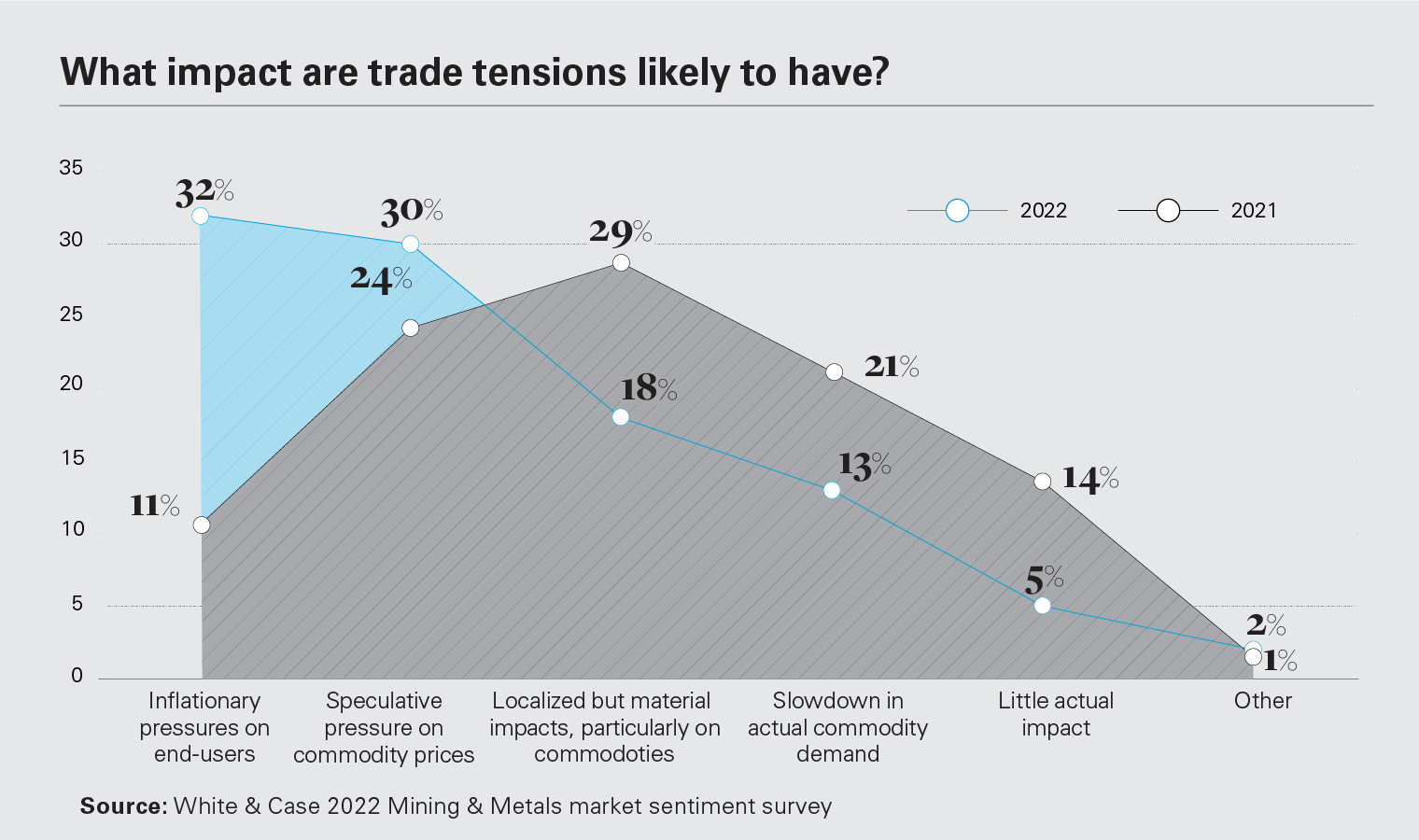

Inflation emerges as a key concern

Heightened levels of friction between the US and China have resulted in trade tensions, which are an ever-present item on the survey. Although less vocal and more traditional in terms of their diplomatic delivery since the change in government in the US, potential tensions remain between the two superpowers in 2022. Other nations, such as Australia, are also enjoying less cordial relations with Beijing. One fascinating takeaway from our survey is that 32 percent of respondents expect a problematic byproduct of trade tensions this year is likely to be inflationary pressures on end-users, compared with just 11 percent in 2021.

Examples of such inflation can be seen through the responses to anticipated underperformers in 2022. Our survey flagged coal and iron ore as the commodities most likely to lag this year, despite, or perhaps because, both hit record prices in 2021. Iron ore rallied strongly in the first half, supporting record earnings and dividends for the period, as China ramped back up its steel industry, while coal was a big winner from the energy crunch in the latter part of the year. Both, however, were also squeezed higher by the ongoing tensions between the Australian government and Beijing.

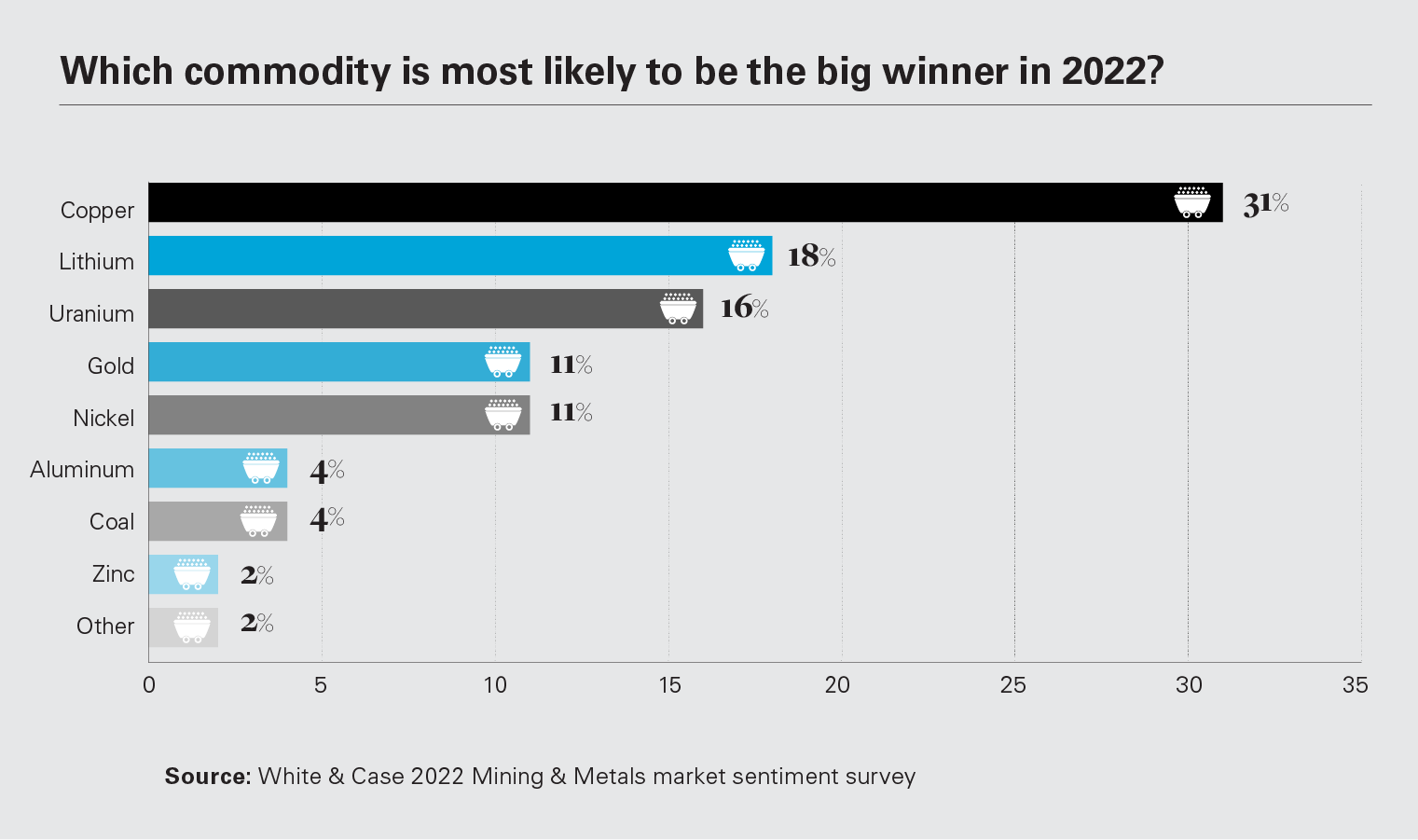

View full image: Which commodity is most likely to be the big winner in 2022? (PDF)

View full image: Which commodity is most likely to be the big winner in 2022? (PDF)

US$ 20,000

Estimated price for lithium carbonate per tonne at point of loading in June 2022Source: Allkem

Copper the top pick again

For the third straight year, our survey has picked copper to be the best-performing metal in 2022, with 31 percent saying it's set for another year of outperformance. The metal, an economic bellwether and a key material for the energy transition, hit record prices last year, breaking above US$10 thousand per ton. Minor production losses, from both COVID-19 disruptions and water issues in Chile, combined with strong industrial demand. Our respondents' enthusiasm for the metal is matched by the wider mining industry. The biggest miners remain universally bullish on its prospects, with demand expected to surge this decade and new supplies looking increasingly scarce.

The second pick is lithium, the crucial ingredient for electric vehicle batteries. The global push to electrify transport, and the need to secure long-term supply agreements, has seen consumption soar, leading to a more than tripling of prices in 2021, to a record high. While the mining industry is pushing hard to expand capacity, it hasn't been able to keep up with demand so far, and market tightness is likely to persist in the near-term. Uranium comes in third, perhaps because nuclear is beginning to displace traditional resources due to reactors generating virtually emission-free power.

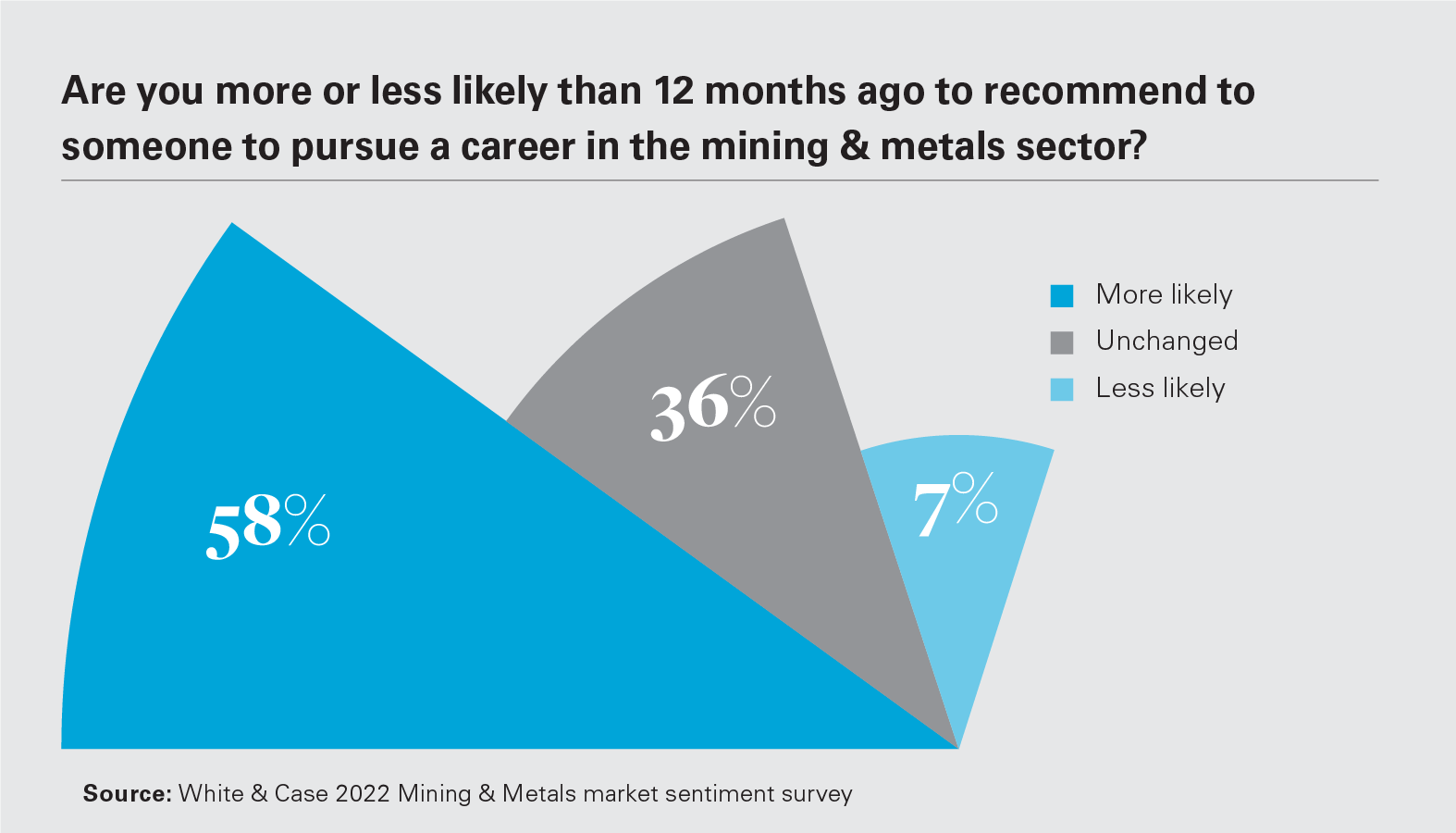

View full image: Are you more or less likely than 12 months ago to recommend to someone to pursue a career (PDF)

View full image: Are you more or less likely than 12 months ago to recommend to someone to pursue a career (PDF)

The sector is a pariah no more?

Overall, therefore, our survey paints a picture of opportunity for those companies engaged in—and willing to transition to—those products that will be a core focus for the energy transition, in addition to those making efforts to develop more green versions of traditional commodities. Perhaps a positive byproduct of this comes in the form of the chance to be part of building the future economy, with some 58 percent of respondents more likely to recommend working in the industry compared to a year ago.

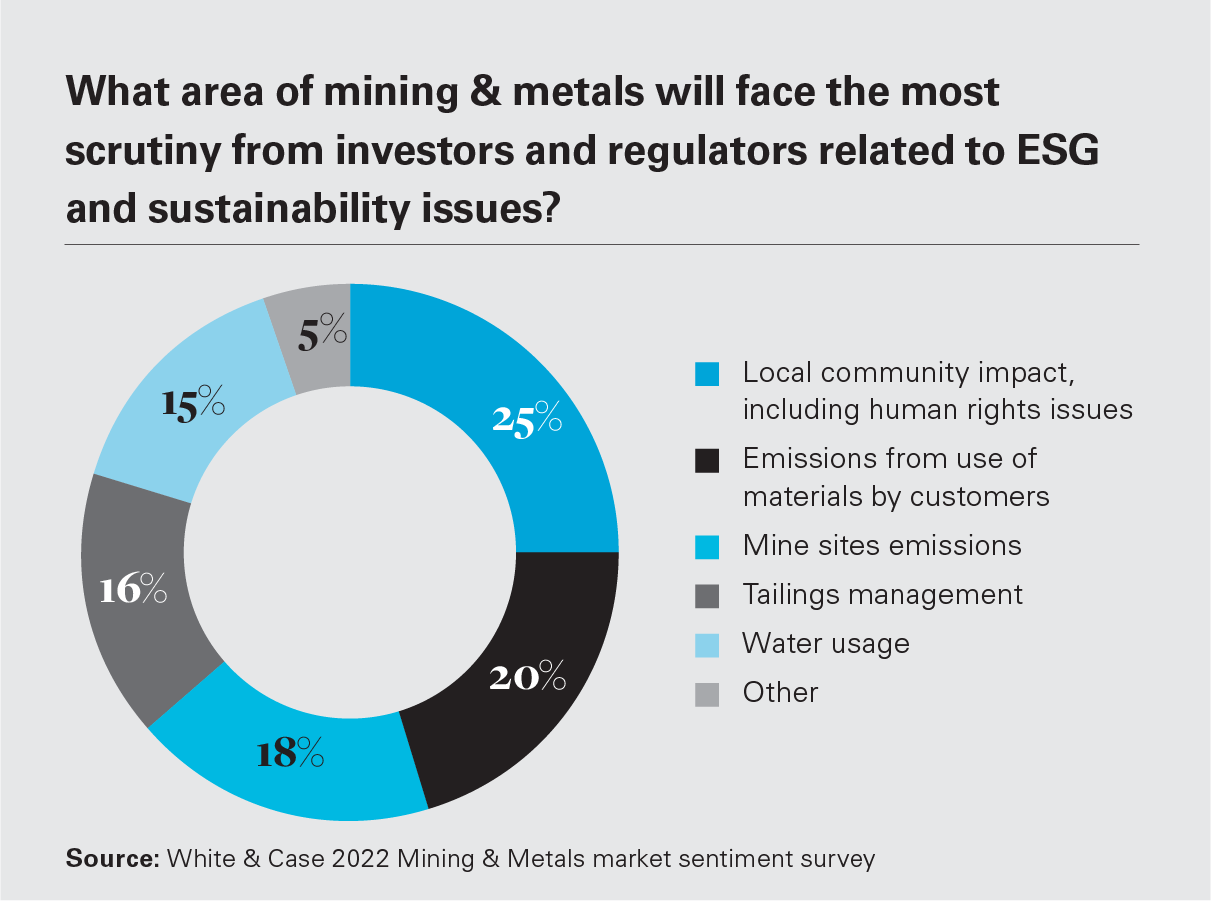

While the industry is making great strides in terms of shedding its prior image, it's clear that investors and regulators will hold it to the highest of standards. The evenly spread answers to the question about which area of ESG will face the most scrutiny demonstrates that miners need to make the correct decision in every element of the ongoing battle to reduce their carbon footprint. If this is achieved, it is possible to envision an energy transition that is aligned with the ESG objectives that are now so fundamental to the operations of a modern mining company.

The stakes are high. A failure to proactively address ESG issues in an energy supply chain can result in future problems that are more difficult to overcome than if addressed at the outset; the development of hydrocarbons as an energy source is a case example. So, the opportunity for the sector is right here, right now, but it needs to get this right. The Global Battery Alliance (GBA) could offer a blueprint for best practice, bringing more than 70 organizations together to ensure the entire battery value chain is both socially and environmentally responsible. From projects that seek to address child labor issues at the source of mineral extraction through to battery recycling—and creating a "battery passport" that verifies ESG standards are met, the GBA's approach seeks to future-proof projects from the outset. Such a framework is ensuring that the EV revolution is occurring in a manner that aligns with the ESG principles that corporates are now expected to meet. If the broader industry can grasp the opportunity on offer, it can cement its position as a central plank of the entire energy transition.

View full image: What area of mining & metals will face the most scrutiny from investors and regulators related to ESG? (PDF)

View full image: What area of mining & metals will face the most scrutiny from investors and regulators related to ESG? (PDF)

View the full results of our survey (PDF)

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP