Strong foundations: Asian infrastructure is open for business

Despite the pandemic, optimism for Asia-Pacific infrastructure projects is increasing with investors looking at a plurality of regions and sectors

While some projects have been delayed, the sector has proven itself remarkably resilient. As has occurred with previous crises, there is now a growing expectation that infrastructure financing volumes will increase above and beyond historical values as the effects of the pandemic subside. And private investment is vital, considering the region’s infrastructure needs— demanding US$1.7 trillion annually in financing, according to the Asian Development Bank (ADB).

With this in mind, White & Case, in association with Inframation, set out to investigate the prospects for infrastructure investment across the APAC region. This new survey builds on our 2019 report Cutting Through the Noise.

The research reveals that, Black Swan events aside, investors remain extremely bullish over the long-term fundamentals of the Asia-Pacific infrastructure sector, with four clear trends emerging:

New frontiers

Investors see APAC as a land of opportunity. More than half of respondents cited ‘wealth of opportunity’ as the greatest benefit to investing in the region.

Growth plans

Despite concerns regarding aspects such as construction and delivery risk and political scrutiny, the outlook from respondents is overwhelmingly positive—78 per cent of firms intend to grow their teams in the region in 2021.

Social surges

Mirroring the findings from our previous report, roads are once again seen as the key infrastructure sector destination. The most eye-catching trend is the significantly increased focus on social infrastructure, with 58 per cent of firms intending to invest.

Responsibility reigns

An increasing need for sustainable infrastructure management caused 60 per cent of respondents to cite environmental, social and governance (ESG) considerations as ‘very important’ when looking at their investment in the region.

Despite the pandemic, optimism for Asia-Pacific infrastructure projects is increasing with investors looking at a plurality of regions and sectors

Digitalisation and ESG are transforming the face of infrastructure. Here we explore how investors are reacting to the opportunities and challenges these forces present

The future is bright for the asset class in the region. Here we explore investor' vision for the future

The future is bright for the asset class in the region. Here we explore investor' vision for the future

World in Transition

Our views on changing dynamics in energy, ESG, finance, globalization and US policy.

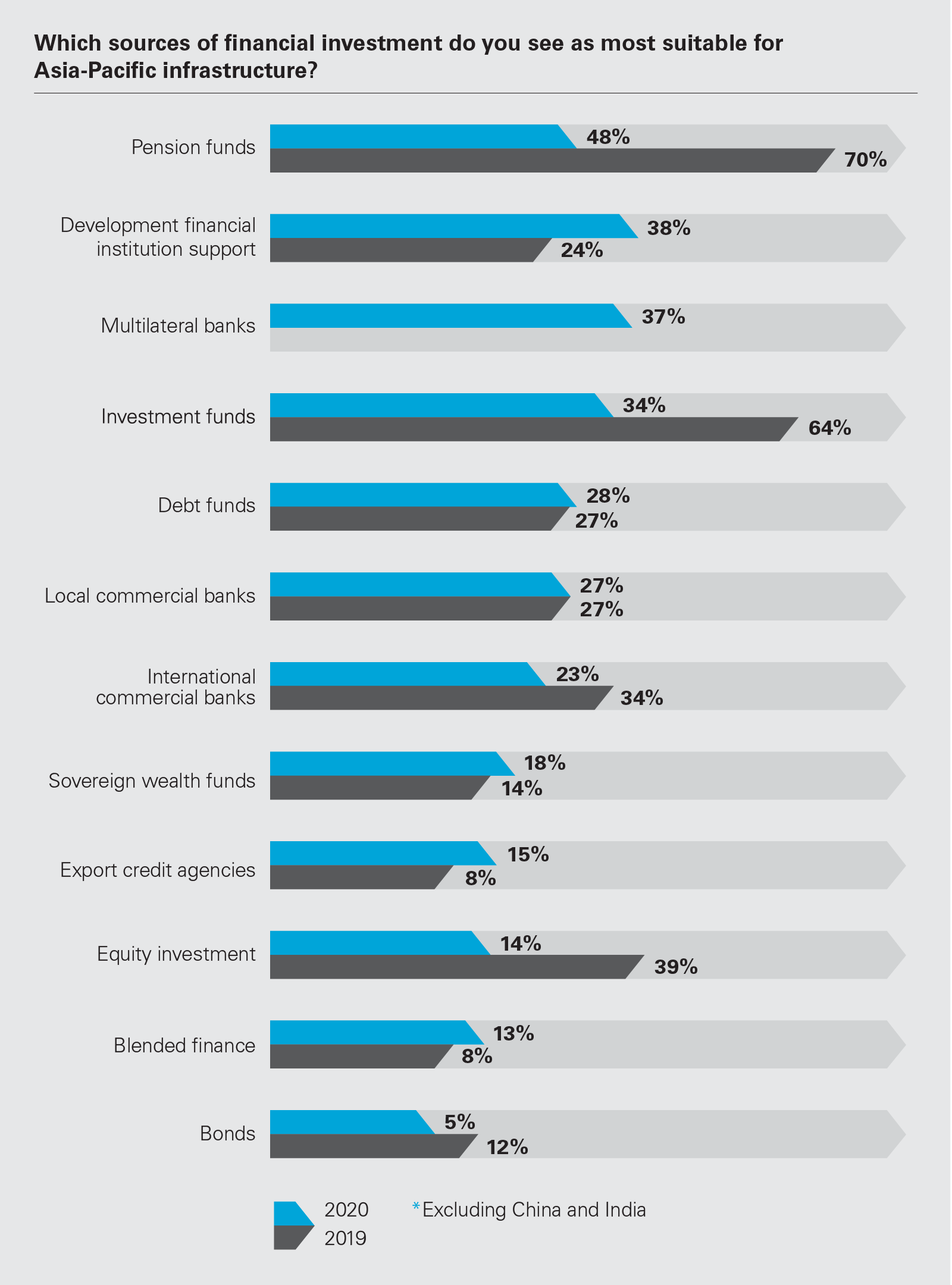

38%

said that development financial institution support would be the most suitable source of finance in this sector, up from 24% in 2019

The pandemic has dealt a heavy blow to government budgets and containing the virus, and supporting households and businesses have taken priority over financing infrastructure projects.

As a result, governments around the region are focused on turning infrastructure projects into an asset class that can attract an increasingly diverse range of institutional investors.

For their part, investors remain extremely bullish over the long-term fundamentals of the Asia-Pacific infrastructure sector. Meanwhile, our survey has shown they are prioritising technology transformation and ESG considerations into their decision-making. Looking ahead, investors are focusing on new financing routes, enhanced partnership models, changing risk mitigation strategies and a brighter future.

The severe disruption caused by the pandemic has created uncertainty in the valuation of many infrastructure assets. In an M&A context, this has made it difficult to assess future earnings when negotiating a sale of infrastructure assets. As a result, many respondents believe that some sources of finance will be restricted.

"Funding sources will change as traditional banking and financing units become more conservative during the resulting recession," said the director of investment at one Canadian investment bank. "Alternative funding sources are more likely to be popular, even with the higher risk."

While private capital tends to avoid riskier greenfield construction projects because of frequent delays and escalating costs, more mature brownfield sites are attracting a variety of financing sources.

Whereas two years ago, 70 per cent of respondents believed that pension funds would be the main source of investment in infrastructure in Asia, only 48 per cent agree with that statement in this year's survey. Instead, 38 per cent of respondents said that development financial institution support would be the most suitable source of finance in this sector, which is up on the 24 per cent who mentioned it two years ago.

Private equity funds are also expected to be more active in the region in 2021, with many having kept their dry powder in 2020. For example, New York-based firm KKR closed its first fund focused on infrastructure investment across Asia-Pacific in January. The US$3.9 billion fund, which is a record size for the region, will invest in sectors such as waste, renewables, power and utilities, telecommunications and transport infrastructure.

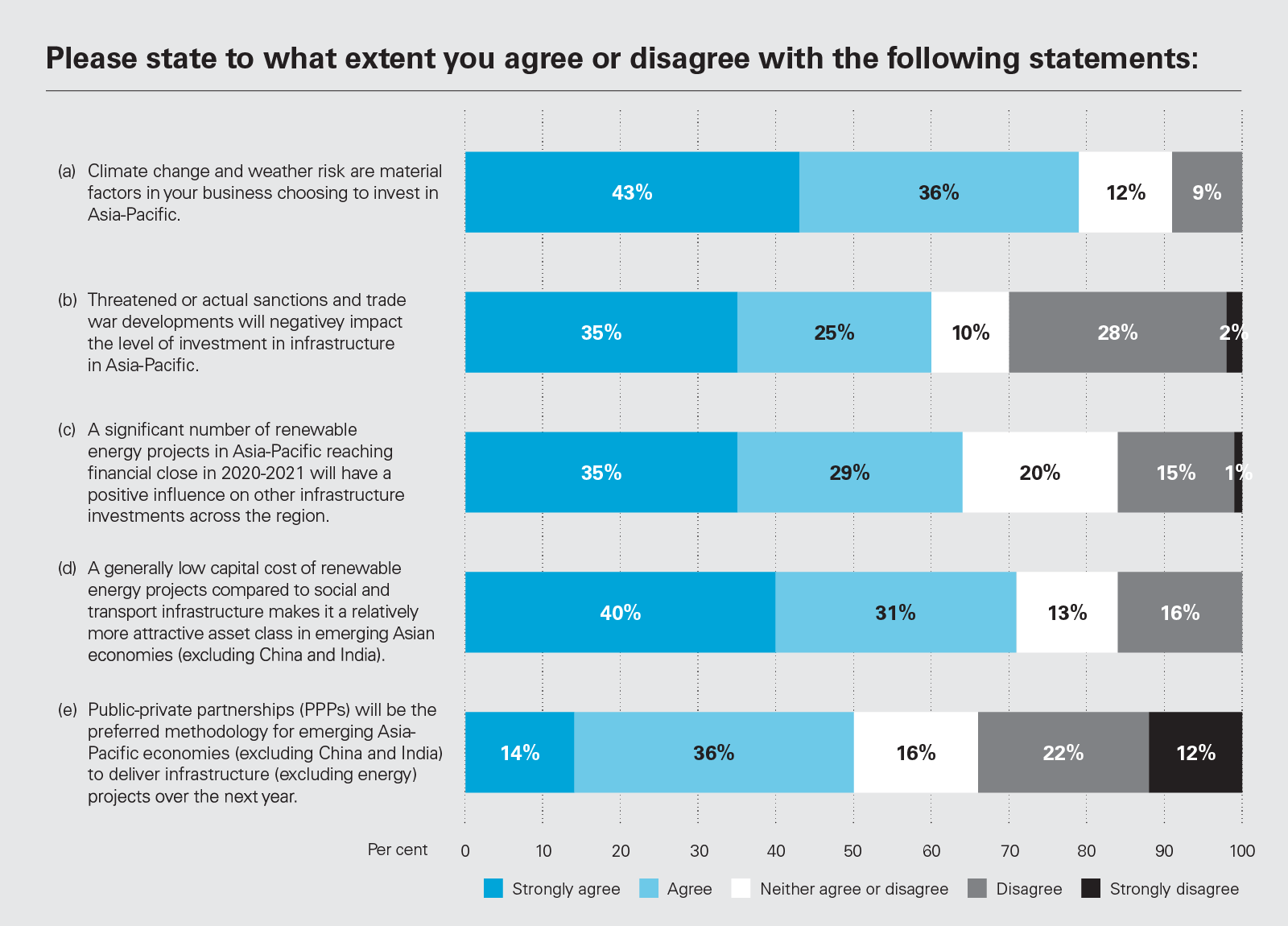

43%

agree strongly that climate change and weather risk are material factors in a business choosing to invest in Asia-Pacific

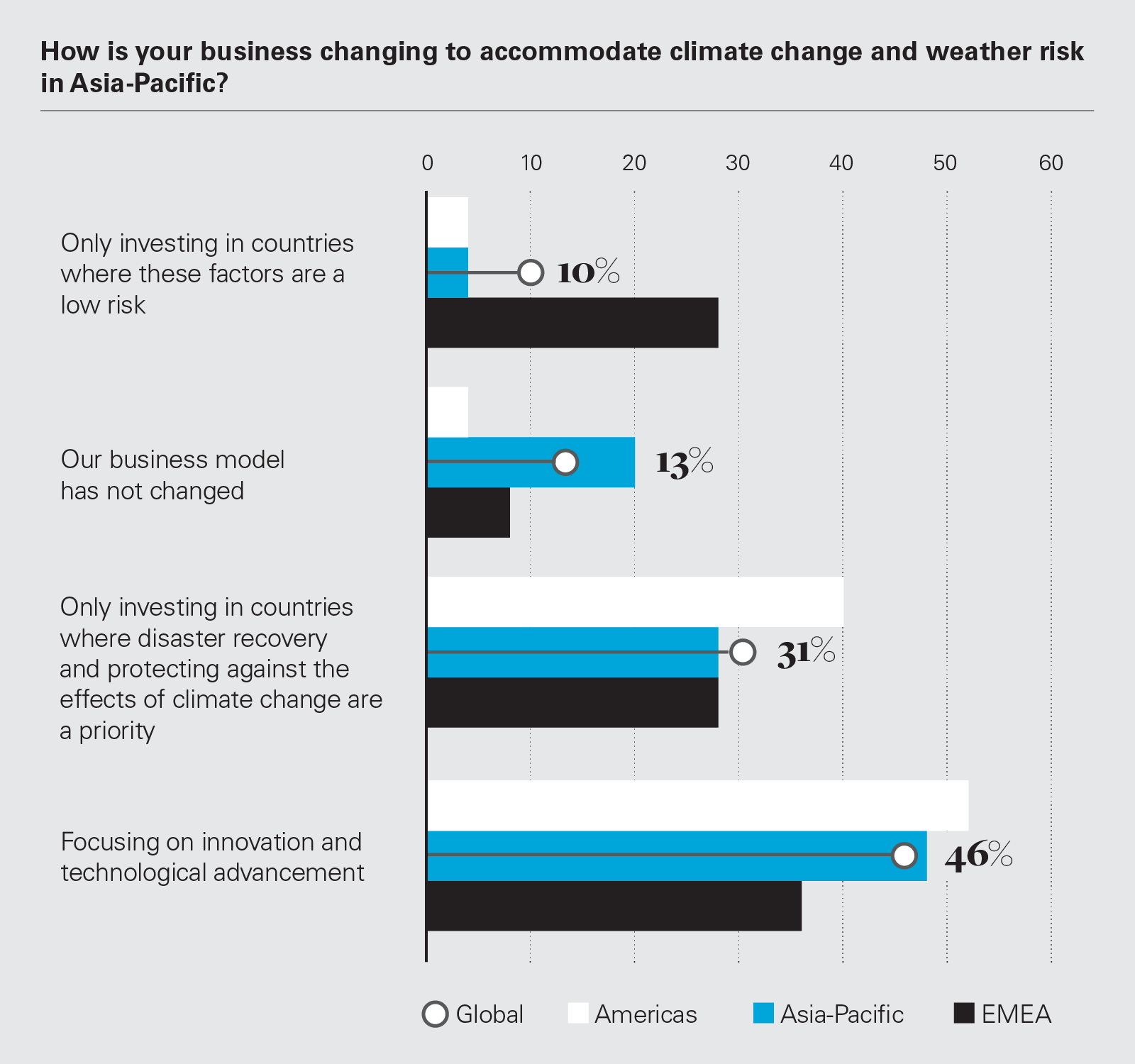

46%

of Asia-Pacific investors will focus on innovation and technological advancement to accommodate climate change and weather risk in Asia-Pacific

When it comes to delivering projects, half of all respondents agreed that public-private partnerships (PPPs) will be the preferred method for emerging Asian economies to deliver infrastructure projects over the coming year. While this is less than the 71 per cent who favoured such partnerships in 2019, PPPs are being increasingly used in Asia although the level is still low compared with other regions.

However, the sectoral and regional spread can be extremely uneven. According to the Asian Development Bank, more than 80 per cent of PPPs that reached financial close in Asia over the past two decades were in the transport sector, and the story is equally unbalanced across countries. More than 70 per cent are in East Asia and South Asia, and 90 per cent of that share is in India and China. However, PPPs are gaining ground in Southeast Asia, particularly in the larger economies of Indonesia, Malaysia, the Philippines, Thailand and Vietnam. Part of the problem is the varying definitions and interpretations of PPPs across the Asia-Pacific region.

The increased use of PPPs as a procurement method by countries is driven by expectations that such partnerships deliver better quality and more

affordable infrastructure services. However, weak governance in many developing Asian countries is not helping to attract private sector investment in infrastructure PPPs. Feedback from survey respondents suggests that Asian countries should focus more on regulatory and institutional reforms needed to make infrastructure more attractive to private investors and generate a pipeline of bankable projects for PPPs. These reforms could include enacting PPP laws, streamlining procurement and bidding processes, introducing dispute resolution mechanisms and establishing independent PPP government units.

When asked about risks to future projects, 79 per cent of investors agree that climate change and weather risk is a material factor when choosing to invest. In order to mitigate such risk, 46 per cent said they would focus more on innovation and technological advancement. This represents a significant shift in mindset from 2019, when only 13 per cent said the same.

Meanwhile, 60 per cent of respondents agreed (35 per cent strongly) that threatened or actual sanctions and trade war developments will negatively impact their level of investment in infrastructure in Asia-Pacific.

"When investing in Asia- Pacific, some regions are more vulnerable to global geopolitical events and policy decisions taken by developed countries," said the CFO of one Malaysian sponsor. "Increased planning for sustainable development and encouraging a transparent dialogue between parties is essential."

While more than half of respondents cited 'wealth of opportunity' as the greatest benefit to investing in Asia-Pacific infrastructure, as a result of the pandemic some investors may only pursue acquisition opportunities this year in sectors or jurisdictions which are familiar to them. "We have been active in healthcare and highway management projects in Malaysia, and we are ready to invest more in the markets where we have knowledge and experience," confirmed the CFO of one Malaysian sponsor.

Overall, the prospects for infrastructure investment in the region are extremely positive. While COVID-19 has had a significant impact on the development and financing of infrastructure across the region, some of that change is benefitting project lenders and investors. The pandemic is accelerating investment in low-carbon and climate resilient infrastructure, and projects that enhance digital connectivity and public health. And as our survey shows, these two areas—ESG and digitalisation—are set to dominate the infrastructure market for the foreseeable future.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

Which sources of financial investment do you see as most suitable for Asia-Pacific infrastructure? (PDF)

Which sources of financial investment do you see as most suitable for Asia-Pacific infrastructure? (PDF)

Please state to what extent you agree or disagree with the following statements (PDF)

Please state to what extent you agree or disagree with the following statements (PDF)

How is your business changing to accommodate climate change and weather risk in Asia-Pacific? (PDF)

How is your business changing to accommodate climate change and weather risk in Asia-Pacific? (PDF)