Canada

The Canadian government announced a strict framework to evaluate foreign investments in the critical minerals sector by state-owned enterprises and state-linked private investors, especially if from “non-likeminded” countries.

Now in its seventh year of annual publication, White & Case's Foreign Direct Investment Reviews provides a comprehensive look into rapidly evolving foreign direct investment (FDI) laws and regulations in approximately 40 national jurisdictions and two regions. This 2023 edition includes more than 15 new jurisdictions in addition to those covered in previous editions and summarizes high-level principles in the European Union and Middle East. Our expansion in coverage reflects the rapid global proliferation of FDI regimes and our market leading position in the field.

FDI regimes are wide-reaching in scope, from national security to public health and safety, law and order, technological superiority, and continuity and integrity of critical supply chains. They are divergent with respect to jurisdictional triggers across countries, and are almost always a black-box process.

The following are some general observations, in large part based on the 2022 CFIUS and EU annual reports:

Investors conducting cross-border business need to understand FDI restrictions as they are today—and how these laws are evolving over time—to avoid disruption to realizing synergies, achieving technological development and integration, and ultimately securing liquidity.

We would like to extend a special thank-you to all of our external authors, who have provided some insightful commentary on the FDI regimes in a number of important jurisdictions. The names of these individual contributors and their law firms are provided throughout this publication.

We would also like to extend a special thank-you to James Hsiao of our Hong Kong office and Tim Sensenig of our Washington, DC office for their tireless efforts and dedication to the publication of this edition.

The Canadian government announced a strict framework to evaluate foreign investments in the critical minerals sector by state-owned enterprises and state-linked private investors, especially if from “non-likeminded” countries.

Foreign direct investments, whether undertaken directly or indirectly, are generally allowed without restrictions or without the need to obtain prior authorization from an administrative agency.

Most deals are approved, but expanded jurisdiction, mandatory filings applying in certain cases, enhanced focus on national security considerations, and a substantially increased pursuit of non-notified transactions have changed the landscape.

Driven by the European Commission's guidance, Member States keep expanding their investment screening regimes. A similar trend is observed in Europe at large.

In Austria, the Austrian Federal Investment Control Act (Investitionskontrollgesetz or the ICA) introduced a new, fully fledged regime for the screening of Foreign Direct Investments (FDI) and came into effect on July 25, 2020. With its wide scope of application and extensive interpretation by the competent authority, the number of screened investments has soared.

The new Foreign Investments Screening Act took effect in May 2021, and completed its first full year in operation in 2022.

The scope of the Danish FDI regime is comprehensive and requires a careful assessment of investments and agreements involving Danish companies.

In France, FDI screening authorities have issued new guidelines to improve the transparency of the FDI process.

The Federal Ministry for Economic Affairs and Energy continues to tighten FDI control, but the investment climate remains liberal in principle.

The need for FDI screening remains in focus for deals with Hungarian dimensions.

Ireland anticipates adopting and implementing an FDI screening regime by Q1 2023.

Italian "Golden Power Law:" Ten years old and continuously expanding its reach.

The Russian Federation's invasion of Ukraine has precipitated the inclusion of provisions blocking Russian and Belarussian nationals from direct investment in a number of sectors.

All investments concerning national security are under the scope of review.

Luxembourg has introduced a bill of law to regulate foreign direct investments. The law is currently being discussed before the Luxembourg Parliament.

Malta's recently introduced FDI regime captures a substantial number of transactions that must be notified to the authorities and, in some cases, will be subject to screening.

The Middle East continues opening to foreign investment, subject to licensing approvals and ownership thresholds for certain business sectors or in certain geographical zones.

The Netherlands prepares for its first effective year of new FDI regulation.

Changes in the geopolitical situation have resulted in increased awareness of security threats caused by strategic acquisitions and access to sensitive technology. The ongoing review of the FDI regulations in Norway is expected to result in more effective mechanisms to identify and deal with security threats in transactions and investors should be prepared to take this into account when planning future investments in Norwegian companies that engage in sensitive activities.

The Polish FDI regime governing the acquisitions of covered entities by non-EEA and non-OECD buyers has been extended until July 2025.

Transactions involving foreign natural or legal persons that allow direct or indirect control over strategic assets may be subject to FDI screening.

The Romanian regime regarding foreign direct investment has undergone a major change in 2022, when new legislation was enacted, and is aimed at implementing relevant European Union legislation.

The Federal Antimonopoly Service (FAS) tends to impose increased scrutiny in the sphere of foreign investments and has developed a number of amendments to the foreign investments laws that are aimed at eliminating legislative gaps in this sphere.

On November 29, 2022, Slovakia, for the first time, adopted full-fledged foreign direct investment legislation. This legislation is effective as of March 1, 2023.

Since May 31, 2020, certain foreign investments into Slovenian companies can be subject to review. Acquisition of real estate related to critical infrastructure may also be subject to review.

The restrictions imposed by the Spanish government on foreign direct investments during the COVID-19 outbreak have remained after the pandemic.

Other than security-related screening, Sweden is currently still without a general FDI screening mechanism.

Historically, Switzerland has been very liberal regarding foreign investments. However, there has recently been increased political pressure to create a more structured legal regime for foreign investment.

Making Türkiye an attractive investment destination continues to be a priority for the government.

Foreign direct investment is permissible in the UAE, subject to applicable licensing and ownership conditions.

The UK’s National Security & Investment Act has now been in place for a year and has already made its mark, prohibiting deals on national security grounds and also requiring remedies in cases that are not subject to the mandatory notification requirement. We expect a continued tough approach over the next year as global geo-political tensions bring national security concerns to the fore.

Australia requires a wide variety of investments by foreign investors to be reviewed and approved before completion of the investment.

China has further developed its national security regulatory regime by promulgating measures on cybersecurity review and security assessment of cross-border data transfer.

India continues to be an attractive destination for foreign investment, ranking as the world's seventh-largest recipient of FDI in 2021.

The Japanese government continues to review filings and refine its approach under the FDI regime following the 2019 amendments.

Korea is increasing the level of scrutiny of foreign investments due to growing concerns over the transfer of sensitive technologies.

Recent legislative reforms have increased the New Zealand government's ability to take national interest considerations into account, but have also looked to exclude lower-risk transactions from consent requirements.

All FDIs are subject to prior approval, but the investment climate is welcoming and liberal.

The UK’s National Security & Investment Act has now been in place for a year and has already made its mark, prohibiting deals on national security grounds and also requiring remedies in cases that are not subject to the mandatory notification requirement. We expect a continued tough approach over the next year as global geo-political tensions bring national security concerns to the fore.

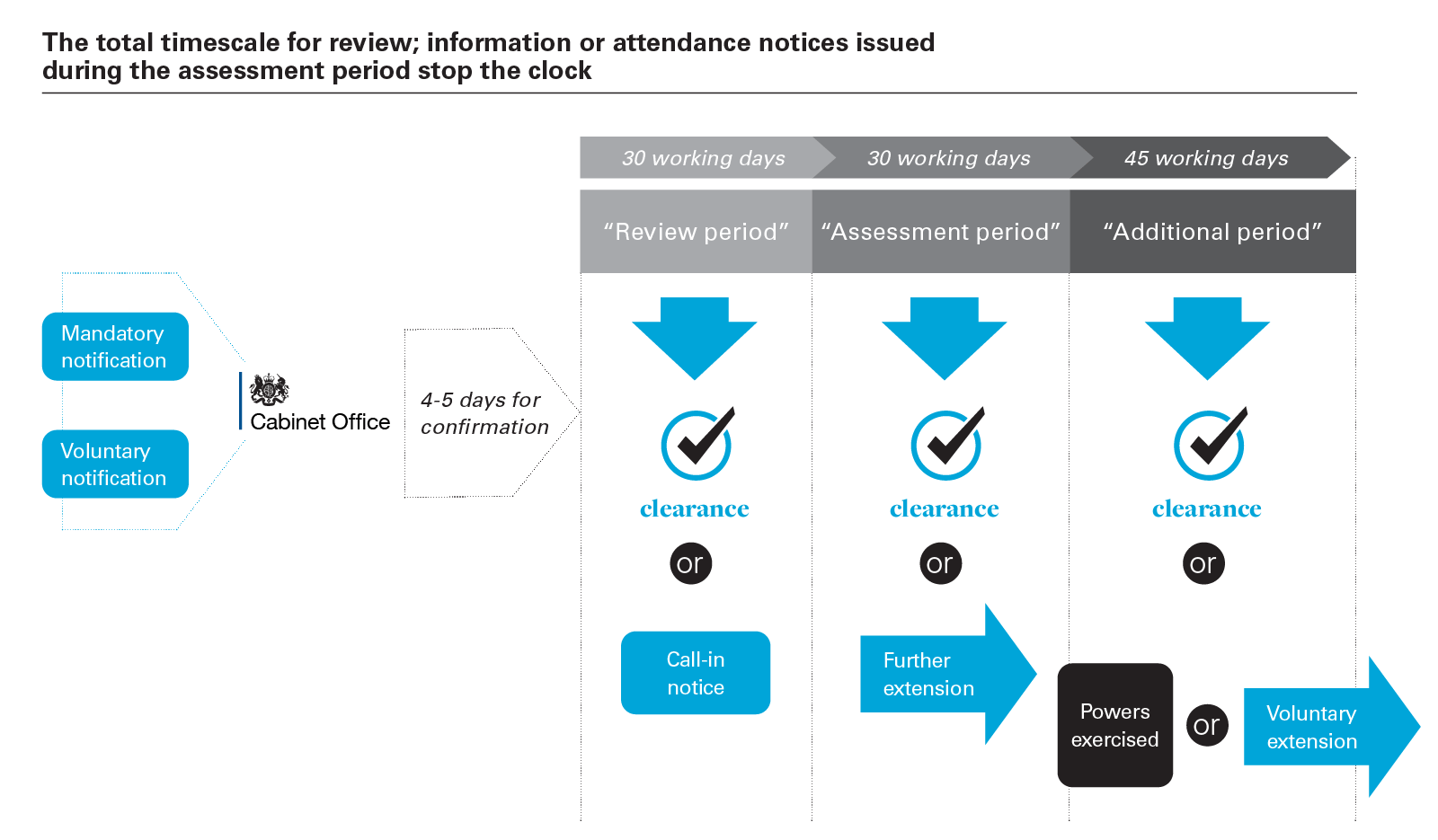

The National Security and Investment Act 2021 (NSIA) became operational on January 4, 2022, and has since become a regular feature of transactions. Certain transactions in 17 sectors require notification, but the regime can apply to any transaction, so voluntary filings are also made if an acquirer would like absolute certainty that a transaction will not be retrospectively reviewed. The regime is administered by the Investment Security Unit, which has been recently relocated to sit within the responsibility of the Cabinet Office, with the Chancellor of the Duchy of Lancaster and Secretary of State for the Cabinet Office (the Secretary of State) exercising final decision-making powers.

Qualifying transactions require notification if the target carries on specified activities in any one of 17 "sensitive sectors."

Unusually, the NSIA is not a true "foreign" direct investment screening mechanism, as it applies equally to UK and foreign investors alike. Indeed, the first conditional decision issued under the NSIA in July 2022, Epiris/Sepura, imposed conditions on UK-based investor Epiris in the context of its acquisition of the digital communications provider that supplies radio solutions to UK emergency services.

Mandatory notifications are filed by the investor. Voluntary notifications, however, can be filed by any party, i.e., the investor, the seller or the target itself.

Qualifying transactions require notification if the target carries on specified activities in any one of 17 “sensitive sectors”

Very little information about NSIA notifications is published. The very fact that a filing has been made is typically not made public, and only if a transaction is blocked, or subject to conditions will a final order (with minimal detail) be published. Transactions that are cleared are not publicized, and the total number of notifications will only be made public in the annual report covering the NSIA.

During 2022, 14 transactions were the subject of "final orders" either imposing conditions on the transactions or prohibiting the transaction outright.

Prohibitions were issued in five instances. Notably, of the five, four of these prohibitions concerned investors from China/Hong Kong. Two of these prohibitions ordered the unwinding of transactions that had already been concluded before the mandatory filing requirements under the NSIA came into force. This power is a feature of the NSIA, which allows the UK government to "call in" any transaction concluded from Novemeber 12, 2020. This retroactive power to call in a transaction for review ordinarily applies for up to five years from the date of the transaction, although this can be reduced to six months if the Secretary of State becomes aware of the transaction (e.g., as a result of a voluntary notification).

Conditions were imposed on nine transactions. In terms of the sensitive sectors that have been subject to conditional decisions—energy; defense/military and dual-use; satellite and space technology; quantum technology and communications—all feature.

Conditions vary by sector and have included, for example:

Again, Chinese investors feature prominently, with at least four of the conditional decisions imposed on Chinese investors. However, conditions have also been imposed in transactions with UAE, UK and US investors.

The scope of the review under the NSIA is three-pronged, with the ISU assessing:

The timeline under the NSIA runs from the date that the notifying party receives confirmation that the notification is accepted as complete. Typically this takes three to four working days (WD) from the submission of the notification.

Once this confirmation is received, the review process is divided into two parts:

These timelines are illustrated below. In graphic below, should read: Call-in notice, Review period, Assessment period, Additional period, Mandatory notification, Voluntary notification

It is, of course, crucial to understand whether or not a transaction requires a mandatory notification. As this analysis is all target-focused, engaging due diligence of prospective targets early on for these purposes is very important.

Thus far, the focus in terms of probing transactions, and imposing conditions, has been on information ring-fencing and securing continuity of supply to critical services in the UK. Therefore, it is important to have a clear narrative in place around the control, information-sharing and intentions that an investor has for a sensitive target in the UK.

In terms of transaction certainty, investors may want to consider judicious use of the voluntary notification option. For example, while mandatory notifications are only required with respect to share sales—asset deals that would otherwise trigger if structured as a share deal—would be a good candidate for voluntary pre-clearance. This also eliminates the prospect of a retrospective call-in after the transaction has closed.

For transactions that are subject to call-in review, it is notable that often there will be limited, if any, engagement with the ISU. The ISU has the power to issue information notices (and attendance notices) but will not necessarily do so. Nonetheless, an investor always has the option to submit further information for the Secretary of State's attention that must be taken into account in his/her decision under the provisions of the NSIA, and selective use of this option can help to allay potential concerns.

It is also important to keep in mind, however, that the vast majority of transactions will be cleared without a "call-in" review.

The chief decision-maker under the NSIA is the Secretary of State. Since the regime has come into force, there have been four decision-makers, with the latest, Oliver Dowden MP, assuming responsibility for the NSIA on February 7, 2023. Doubtless, there is some learning to be expected from Mr. Dowden's decision-making, therefore, in terms of the projects and types of investors that he prioritizes for review.

Indeed, the difference in approach between the men who have occupied this position since the regime took effect in January 2022, is ably demonstrated by the November prohibition decision on Nexperia's concluded acquisition of 86 percent of Newport Wafer Fab, the Britain-based semi-conductor company. Kwasi Kwarteng, the first NSIA Secretary of State, was originally told not to call in the transaction at all, according to a letter written by Tom Tugendhat, MP to then-Prime Minister Boris Johnson, in July 2021, urging intervention. This position was reversed, however, with the deal being exposed to further scrutiny under the NSIA call-in process before eventually being prohibited, mandating an unwinding of the completed transactions, under a decision taken by the previous office-holder, Grant Shapps MP, on November 16, 2022.

In terms of sectoral focus and decision-making practice, the NSIA mandates the publication of an annual report, covering the period from April 1 to March 31 each year. Per those requirements, we can expect an annual report in the spring of 2023, which should provide further insight into the sectors that are featuring most prominently in notifications, the percentage of deals being cleared without detailed "call-in" review, and the average timescales attaching to each step in the NSIA process.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP