Canada

The Canadian government announced a strict framework to evaluate foreign investments in the critical minerals sector by state-owned enterprises and state-linked private investors, especially if from “non-likeminded” countries.

Now in its seventh year of annual publication, White & Case's Foreign Direct Investment Reviews provides a comprehensive look into rapidly evolving foreign direct investment (FDI) laws and regulations in approximately 40 national jurisdictions and two regions. This 2023 edition includes more than 15 new jurisdictions in addition to those covered in previous editions and summarizes high-level principles in the European Union and Middle East. Our expansion in coverage reflects the rapid global proliferation of FDI regimes and our market leading position in the field.

FDI regimes are wide-reaching in scope, from national security to public health and safety, law and order, technological superiority, and continuity and integrity of critical supply chains. They are divergent with respect to jurisdictional triggers across countries, and are almost always a black-box process.

The following are some general observations, in large part based on the 2022 CFIUS and EU annual reports:

Investors conducting cross-border business need to understand FDI restrictions as they are today—and how these laws are evolving over time—to avoid disruption to realizing synergies, achieving technological development and integration, and ultimately securing liquidity.

We would like to extend a special thank-you to all of our external authors, who have provided some insightful commentary on the FDI regimes in a number of important jurisdictions. The names of these individual contributors and their law firms are provided throughout this publication.

We would also like to extend a special thank-you to James Hsiao of our Hong Kong office and Tim Sensenig of our Washington, DC office for their tireless efforts and dedication to the publication of this edition.

The Canadian government announced a strict framework to evaluate foreign investments in the critical minerals sector by state-owned enterprises and state-linked private investors, especially if from “non-likeminded” countries.

Foreign direct investments, whether undertaken directly or indirectly, are generally allowed without restrictions or without the need to obtain prior authorization from an administrative agency.

Most deals are approved, but expanded jurisdiction, mandatory filings applying in certain cases, enhanced focus on national security considerations, and a substantially increased pursuit of non-notified transactions have changed the landscape.

Driven by the European Commission's guidance, Member States keep expanding their investment screening regimes. A similar trend is observed in Europe at large.

In Austria, the Austrian Federal Investment Control Act (Investitionskontrollgesetz or the ICA) introduced a new, fully fledged regime for the screening of Foreign Direct Investments (FDI) and came into effect on July 25, 2020. With its wide scope of application and extensive interpretation by the competent authority, the number of screened investments has soared.

The new Foreign Investments Screening Act took effect in May 2021, and completed its first full year in operation in 2022.

The scope of the Danish FDI regime is comprehensive and requires a careful assessment of investments and agreements involving Danish companies.

In France, FDI screening authorities have issued new guidelines to improve the transparency of the FDI process.

The Federal Ministry for Economic Affairs and Energy continues to tighten FDI control, but the investment climate remains liberal in principle.

The need for FDI screening remains in focus for deals with Hungarian dimensions.

Ireland anticipates adopting and implementing an FDI screening regime by Q1 2023.

Italian "Golden Power Law:" Ten years old and continuously expanding its reach.

The Russian Federation's invasion of Ukraine has precipitated the inclusion of provisions blocking Russian and Belarussian nationals from direct investment in a number of sectors.

All investments concerning national security are under the scope of review.

Luxembourg has introduced a bill of law to regulate foreign direct investments. The law is currently being discussed before the Luxembourg Parliament.

Malta's recently introduced FDI regime captures a substantial number of transactions that must be notified to the authorities and, in some cases, will be subject to screening.

The Middle East continues opening to foreign investment, subject to licensing approvals and ownership thresholds for certain business sectors or in certain geographical zones.

The Netherlands prepares for its first effective year of new FDI regulation.

Changes in the geopolitical situation have resulted in increased awareness of security threats caused by strategic acquisitions and access to sensitive technology. The ongoing review of the FDI regulations in Norway is expected to result in more effective mechanisms to identify and deal with security threats in transactions and investors should be prepared to take this into account when planning future investments in Norwegian companies that engage in sensitive activities.

The Polish FDI regime governing the acquisitions of covered entities by non-EEA and non-OECD buyers has been extended until July 2025.

Transactions involving foreign natural or legal persons that allow direct or indirect control over strategic assets may be subject to FDI screening.

The Romanian regime regarding foreign direct investment has undergone a major change in 2022, when new legislation was enacted, and is aimed at implementing relevant European Union legislation.

The Federal Antimonopoly Service (FAS) tends to impose increased scrutiny in the sphere of foreign investments and has developed a number of amendments to the foreign investments laws that are aimed at eliminating legislative gaps in this sphere.

On November 29, 2022, Slovakia, for the first time, adopted full-fledged foreign direct investment legislation. This legislation is effective as of March 1, 2023.

Since May 31, 2020, certain foreign investments into Slovenian companies can be subject to review. Acquisition of real estate related to critical infrastructure may also be subject to review.

The restrictions imposed by the Spanish government on foreign direct investments during the COVID-19 outbreak have remained after the pandemic.

Other than security-related screening, Sweden is currently still without a general FDI screening mechanism.

Historically, Switzerland has been very liberal regarding foreign investments. However, there has recently been increased political pressure to create a more structured legal regime for foreign investment.

Making Türkiye an attractive investment destination continues to be a priority for the government.

Foreign direct investment is permissible in the UAE, subject to applicable licensing and ownership conditions.

The UK’s National Security & Investment Act has now been in place for a year and has already made its mark, prohibiting deals on national security grounds and also requiring remedies in cases that are not subject to the mandatory notification requirement. We expect a continued tough approach over the next year as global geo-political tensions bring national security concerns to the fore.

Australia requires a wide variety of investments by foreign investors to be reviewed and approved before completion of the investment.

China has further developed its national security regulatory regime by promulgating measures on cybersecurity review and security assessment of cross-border data transfer.

India continues to be an attractive destination for foreign investment, ranking as the world's seventh-largest recipient of FDI in 2021.

The Japanese government continues to review filings and refine its approach under the FDI regime following the 2019 amendments.

Korea is increasing the level of scrutiny of foreign investments due to growing concerns over the transfer of sensitive technologies.

Recent legislative reforms have increased the New Zealand government's ability to take national interest considerations into account, but have also looked to exclude lower-risk transactions from consent requirements.

All FDIs are subject to prior approval, but the investment climate is welcoming and liberal.

Driven by the European Commission's guidance, Member States keep expanding their investment screening regimes. A similar trend is observed in Europe at large.

While there is no standalone foreign direct investment (FDI) screening at the EU level, the EU continues to push for a coordinated approach among Member States toward foreign direct investments into the EU.

The European Commission (the Commission or EC) also contemplates revising the current EU Screening Regulation1 to strengthen its functioning and effectiveness, taking into account experience drawn from the past two years of cooperation and the actions taken in the context of the COVID-19 crisis and the aggression of Russia against Ukraine.

While the Screening Regulation as the key FDI instrument has now been complemented by the Foreign Subsidies Regulation (FSR),2 the EC is further considering whether new tools are necessary with respect to outbound strategic investments controls.3

The final say in relation to any FDI undergoing screening or any related measure remains the sole responsibility of the Member State

The EU Screening Regulation falls short of delegating any veto or enforcement rights to the EU, which means that Member States remain in the driver's seat for FDI controls.

It is primarily a means of harmonizing and coordinating the widely differing review mechanisms in place at the Member State level throughout the EU. It ensures each affected Member State as well as the EU as a whole are aware of ongoing FDI reviews and can weigh in.

In particular, the Regulation introduced a coordination mechanism whereby the EC may issue non-binding opinions on FDI reviews performed in Member States. "Non-reviewing" Member States may provide comments to the "reviewing" Member States. Member States and the EC may also provide comments on a transaction that is not being reviewed because it takes place in a Member State with no FDI regime, in a Member State in which the transaction does not meet the criteria for an FDI review by the government, or the reviewing Member State decided to waive screening of a particular investment. In the latter case, the Member State concerned with the FDI must provide a minimum level of information to the other relevant Member States and/or the EC on a confidential basis without undue delay.

The cooperation mechanism may also apply to a completed investment that is subject to scrutiny under a Member State's post-closing regime (most Member States, however, have adopted pre-closing FDI regimes), or an investment that has not been scrutinized within 15 months after the investment has been completed.

The final say in relation to any FDI undergoing screening or any related measure remains the sole responsibility of the Member State conducting the review pursuant to its national FDI screening procedures. However, it cannot be ignored that (in particular) smaller Member States may find themselves under considerable pressure to conform to opinions or comments issued by the EC or other Member States.

National FDI authorities take different approaches when implementing the EU Screening Regulation. Certain FDI authorities have systematically notified, under the EU cooperation mechanism, every transaction involving non-EU investors, while others do so under specific circumstances only. According to the EC's 2021 Annual FDI Report, while 13 Member States submitted a total of 414 notifications under Article 6 of the FDI Screening Regulation in 2021, five Member States (Austria, France, Germany, Italy and Spain) were responsible for more than 85 percent of them.

Given that the review remains under the control of the Member States, investors may face multiple national FDI notifications in transactions where the target has a multijurisdictional presence in the EU. The EC's 2021 Annual Report shows that 28 percent of the cases notified in 2021 were multijurisdictional FDI transactions. These transactions concerned predominantly the sectors of information and communication technology (39 percent), manufacturing (20 percent) as well as wholesale and retail (11 percent).

The key effects of the Regulation, therefore, are largely procedural. In particular, the new role of the EC and the other Member States has increased the number of stakeholders weighing in on the national investment screening review processes, which has an impact on timing, albeit it remains clear that the reviewing Member State has the final say.

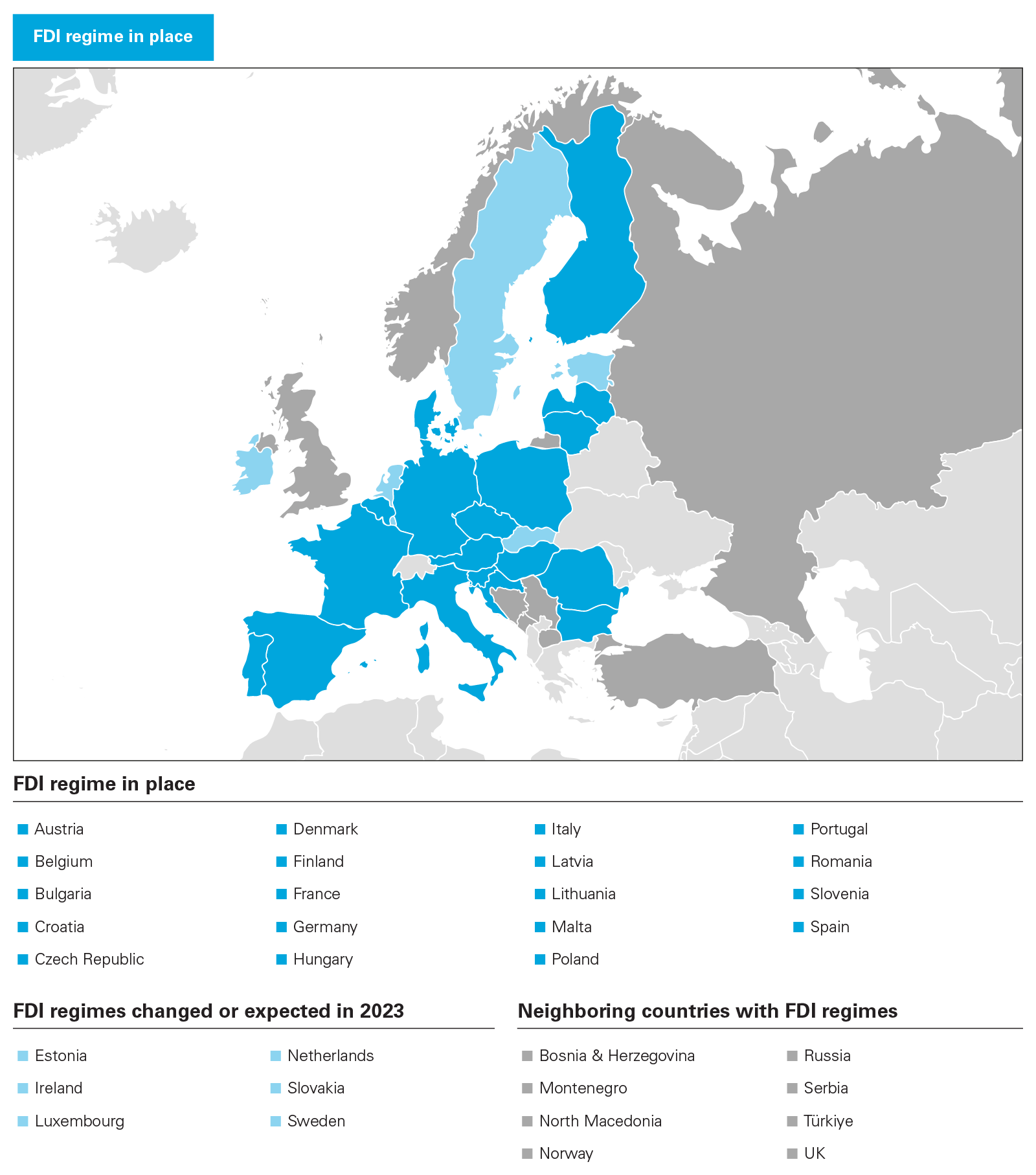

While the Screening Regulation does not oblige Member States to introduce a national FDI review process, the trend is set: In its 2021 Annual Report, the EC reported that it anticipated all 27 Member States to have one in place in the future. The EU Screening Regulation has prompted Member States to consider establishing a new national security review regime (where one did not already exist). A number of additional Member States have done so over the past year, such as the Netherlands, Sweden, Denmark, Czech Republic, Poland, Slovakia and Ireland, and more are currently contemplating the adoption of FDI regimes. To date, only Bulgaria has not reported any initiative.

In addition, despite the fact that Member States remain responsible for any enforcement action post-FDI, the implementation of the Screening Regulation has created an impetus for Member States to align themselves better with the Regulation. For instance, Germany broadened and clarified the thresholds for mandatory review to align itself more with the EU Regulation, and Hungary enacted legislation to harmonize its national regime with the EU Regulation. However, the EC's 2021 Annual Report still evidences divergence in national schemes (see section below).

In terms of substantive requirements, the Screening Regulation sets out the following cornerstones that an FDI regime should reflect:

In 2022, following Russia's aggression against Ukraine, the EC urgently encouraged Member States to develop FDI screening mechanisms to address transactions that could create a risk to security or public order in the EU.4

The FSR is extremely far-reaching

On November 28, 2022, the Council of the European Union adopted the Foreign Subsidies Regulation (FSR), to address the issue of subsidies granted by non-EU countries (i.e., foreign subsidies) to companies active in the EU, which have so far escaped the control of the EC. The EC believes the FSR closes an important enforcement gap in its toolbox, as it will gain the power to investigate and assess whether companies operating in the EU have been backed by foreign subsidies, and whether these impact competition in the internal market.5

The FSR will apply as of July 12, 2023, and the filing obligation for M&A transactions and public tenders will take effect as of October 12, 2023. An implementing regulation as well as the notification forms for M&A transactions and public tenders were published for four-week consultation on February 6, 2023.6 The final implementing regulation and the notification forms are expected to be adopted by summer 2023.

The FSR targets all companies that are active in the EU and have received any form of direct or indirect foreign financial contributions (FFCs) from a non-EU country.7 This is particularly the case with those companies that engage in M&A transactions or public tenders in the EU.

Unlike the FDI rules, which remain within the competence of EU Member States, the EC will be the sole enforcer of the FSR. It will have far-reaching investigative powers under two regimes: (i) the ex-ante mandatory filing regime and (ii) the ex officio investigation regime.

For M&A transactions, the FSR imposes on the parties filing and standstill obligations for transactions when certain thresholds are met, namely if:

For EU public tenders, the filing obligation arises where the contract has a minimum value of €250 million (or €125 million if the tender is divided into lots) and if the bidding party or its holding or subsidiaries, or its main suppliers or subcontractors, have received FFCs equal to or more than €4 million per third country in the three years before the filing.

Non-notifiable M&A transactions or EU public tenders may be concluded before they are approved by the EC. However, the EC may also request that it be notified of M&A transactions and EU tenders falling below the filing thresholds before they are concluded if the EC suspects that these transactions may be backed by distortive foreign subsidies. The EC's assessment related to the foreign subsidies will run in parallel with the merger (or FDI) control and the public tender proceedings. If the EC starts a preliminary review in a transaction that has been subject to an FDI review, it shall inform the relevant Member State(s).

In the case of notifiable transactions, companies should plan for an FSR review, in addition to the merger control and FDI reviews. The FSR covers all economic sectors, including those that are of strategic interest to the EU, as mentioned in the EU FDI Regulation. Deal documentation will have to be adapted accordingly, and deal timing considerations should be taken into account. We are now likely to see more complaints filed with the EC during and after the notification of the M&A deals.

The FSR also grants ex officio powers to the EC, including that it may retrospectively investigate M&A deals and public tenders that have already been concluded, as well as any other market situation, in which foreign subsidies may be involved.

The EC's review procedure will follow a two-tier structure: a preliminary review to assess whether there are sufficient indications that a company has been granted a foreign subsidy that distorts the internal market, followed by an in-depth investigation if that is the case. If such subsidies are deemed to create market distortions, the EC will now have wide-ranging powers to impose corrective measures, block deals or public awards and even dissolve previously concluded concentrations. Companies may be requested to offer far-reaching commitments if they want transactions to be approved or to close the ex officio investigation. The EC can also impose fines and periodic penalty payments for procedural infringements, for failure to notify, and/or for supplying incorrect or misleading information.

In general, a foreign subsidy would be considered distortive if it could improve the business's competitive position in the EU and, in doing so, negatively affect competition in the internal market. Subsidies likely to be distortive include supporting failing businesses, unlimited guarantees and facilitating a concentration or a participation in a tendering procedure.

If there is a distortion, the EC will conduct a balancing test before deciding whether to block the transaction or award. In such a scenario, the EC will consider the positive effects of the subsidy, such as benefits of the subsidized economic activity on the internal market and whether it supports a broader EU policy.

The FSR is extremely far-reaching and will increase the regulatory risk and burden for companies operating or investing in the EU with support from foreign states. It may also open up new opportunities for strategic complaints by competitors.

The new measures will add complexity to the regulatory clearance path for M&A by state-backed investors involving EU targets, as in addition to the "regular" merger control at the EU or national level, and the national FDI proceedings, companies will now potentially have to file for an FSR clearance, prior to closing their transactions.

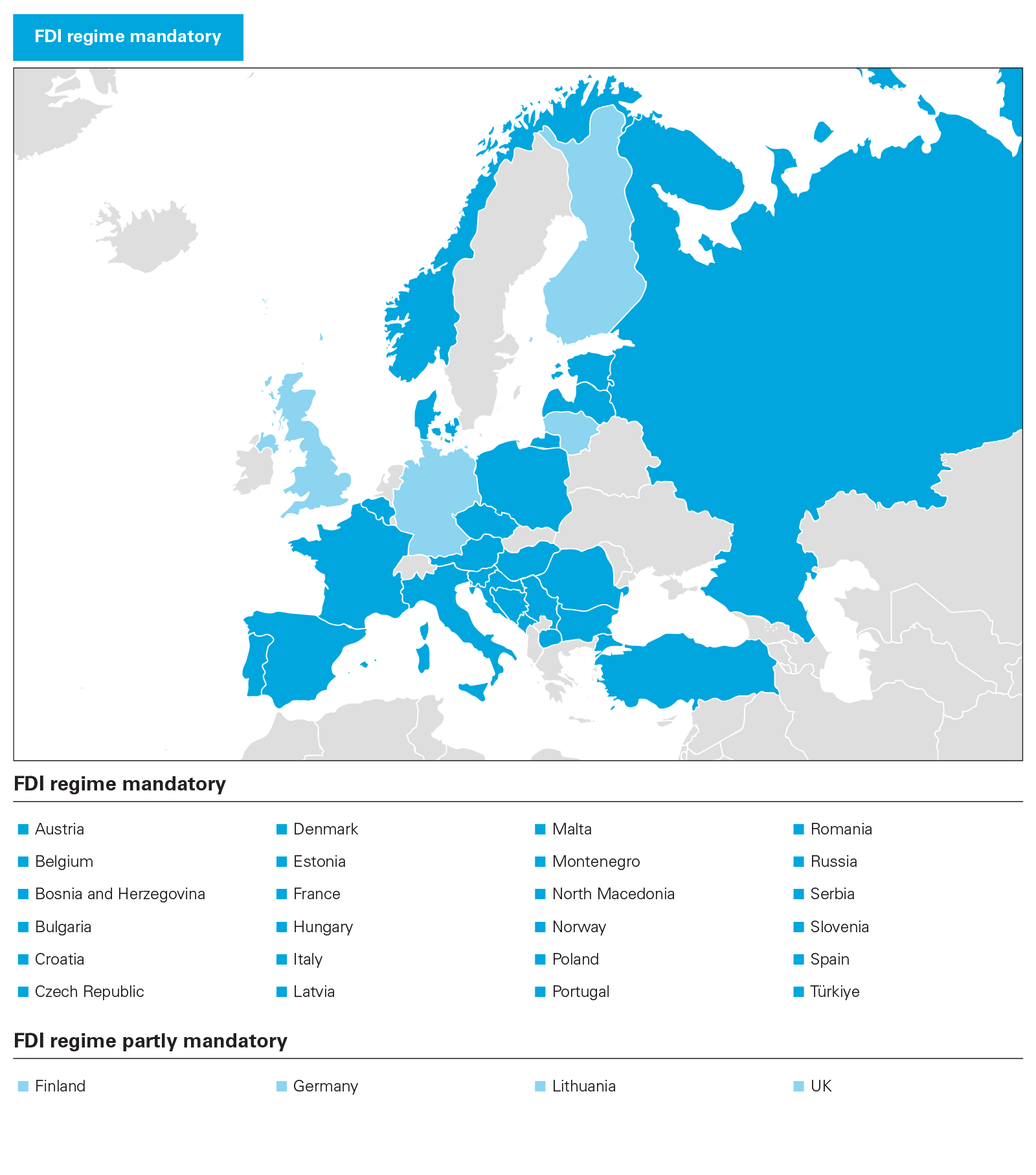

Eighteen of the 27 EU Member States have a screening regime. The regimes differ widely in terms of:

Some regimes are truly hybrid, and the answer to these questions depends on the target's activities and other factors.

There is broad divergence among legislative regimes regarding whether they provide for mandatory filings, voluntary filings, ex officio investigations or a mixture thereof. The German regime is illustrative—as set out in the chapter "Germany," it provides for a mandatory filing requirement based on the target's activities, the size of the stake (voting rights) acquired and the "nationality" of the investor.

If these thresholds are not met, the government may still intervene, and investors may hence consider making voluntary filings, under certain circumstances. For an ex officio investigation, there needs to be a direct or indirect acquisition of at least 25 percent of the voting rights of a German target; an increase of an existing stake above 40, 50 or 75 percent, or an acquisition of "atypical control" by a non-EU/EFTA-based investor—otherwise the government does not have jurisdiction to review the transaction. The regime provides for a standstill obligation where filings are mandatory, but not where they are voluntary.

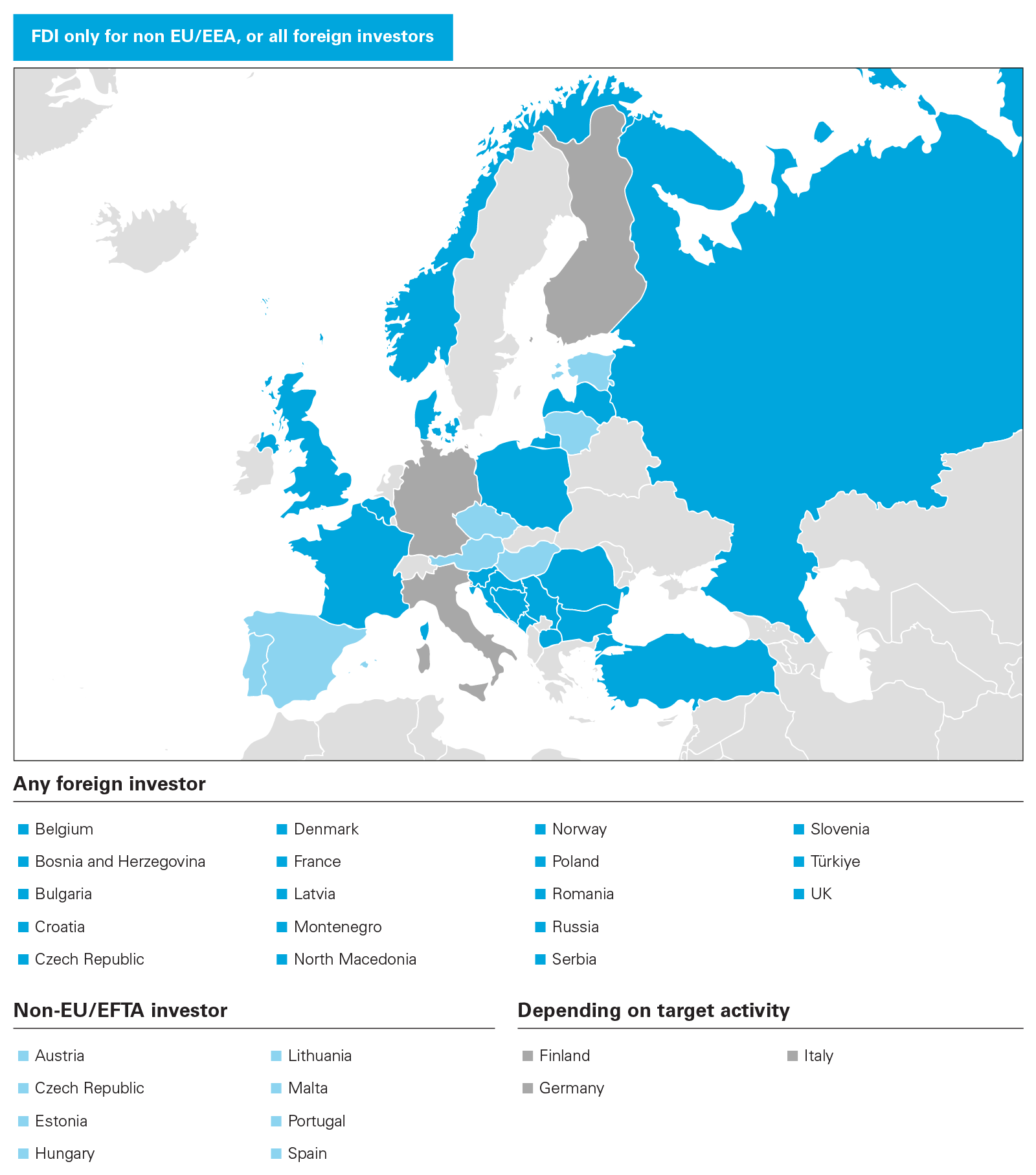

The various national regimes also differ in terms of whether they only cover investments by non-EU-based investors or any non-domestic acquirer. Some regimes are, again, hybrid: For example, the German regime scrutinizes investments by any non-domestic acquirer in the defense/crypto-tech sector (having a 10 percent stake), while in all other sectors, investments by EU or EFTA-based acquirers do not trigger a filing requirement and cannot be reviewed ex officio (although the government takes a very broad view as to whether an investor is non-EU/EFTA-based).

The French regime captures acquisitions of control by any non-French investor, but minority acquisitions only if the investor is non-EU/EEA-based (having 25 percent of voting rights for all kinds of entities).

In contrast, the Spanish regime only captures acquisitions by non-EU/EFTA investors if they exceed a 10 percent share or control threshold and the target is active in certain sensitive sectors. However, a filing is required irrespective of the target's activities if the investor meets certain circumstances (being government-controlled, being subject to sanctions or illegal activities or having already invested in sensitive sectors in another Member State). In addition, EU/EFTA investors are required to make an FDI filing in Spain if the investment in Spain exceeds €500 million in a non-listed company or involves the acquisition of more than 10 percent of a Spanish listed company.

Similarly, the regime in the Czech Republic defines "foreign investor" for filing purposes as one from a non-EU country.

Views across the US, Europe and elsewhere keep converging such that so-called "sensitive" sectors need to be protected from what is being described in the US as "adversarial capital" in a more or less coherent way. This trend is displayed through both the lowering of thresholds that trigger FDI reviews and an expansion of what qualifies as a sensitive sector for purposes of FDI reviews, export controls and international trade compliance. As an example, Germany added 16 new case groups to its screening scope while France supplemented the list of critical technologies with technologies involved in the production of renewable energy.

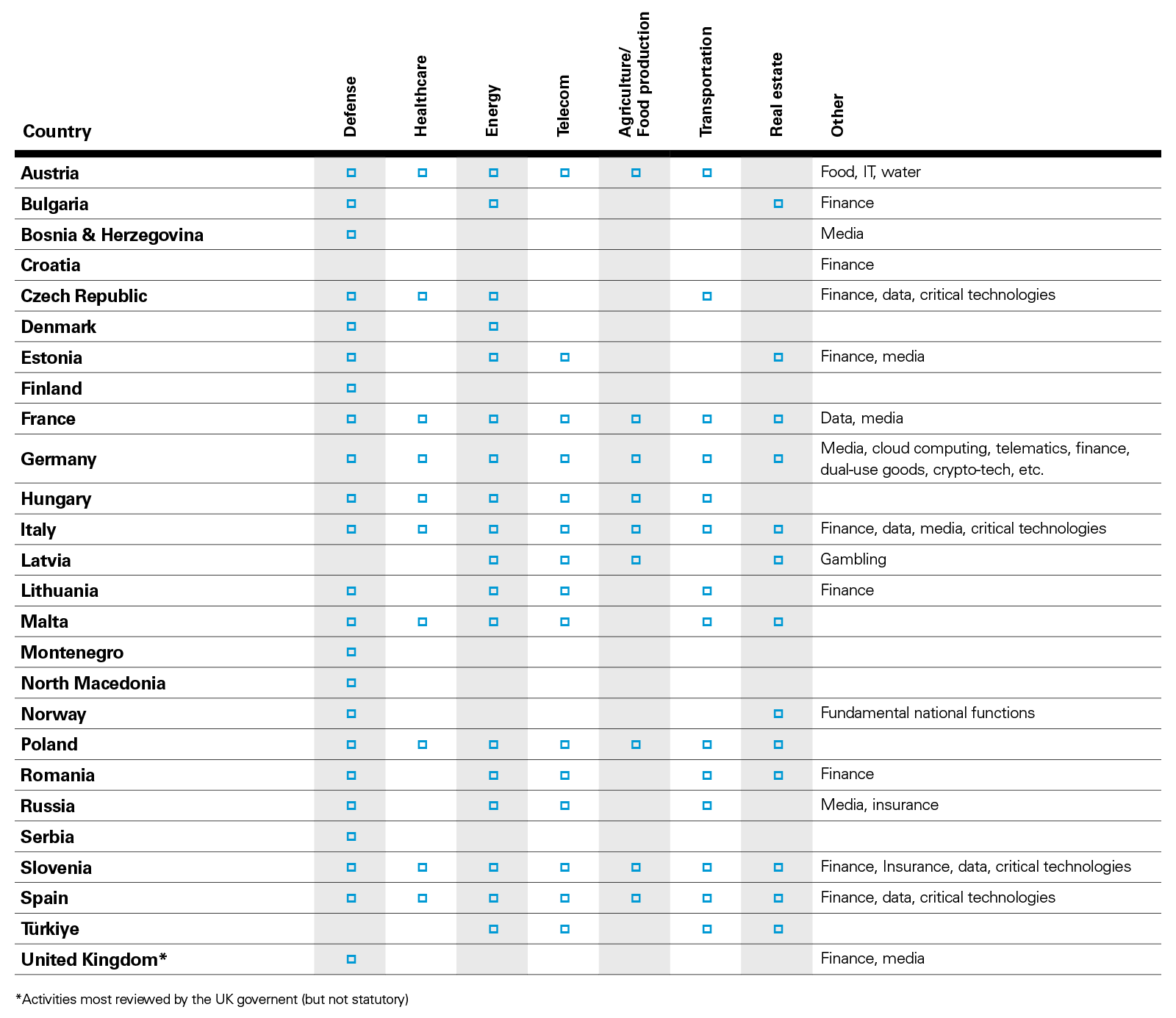

Sensitive sectors are no longer limited to the traditional sectors associated with national security at a macro level (defense, energy or telecom), but are now expanding to biotechnologies, hi-tech, new critical technologies such as artificial intelligence or 3D printing, and data-driven activities.

Moreover, the COVID-19 pandemic brought FDI into sharper focus and accelerated movement on a national level across Europe. Governments were concerned about foreign investors taking advantage of European companies being in distress and, of course, the crisis led the governments to add the healthcare sector to the sensitive industries. In line with the EU Screening Regulation, FDI screening is also expanding to the area of food security, which has become a priority concern in the EU. Investments in the agri-food sector are subject to review in several Member States like Estonia, France, Germany, Italy, Latvia, Malta, Poland and Spain.

Finally, 5G technology has become a source of concern for certain Member States that had issued specific rules to ensure FDI screening in relation to 5G networks/equipment. In Italy, the government's "Golden Power" preclearance process is mandatory for contracts or agreements with non-EU persons relating to the supply of 5G technology infrastructure, components and services. France introduced a specific ad hoc authorization process for operating 5G technology in French territory. In Germany, the Federal Network Agency has published a security catalog for telecoms and data processing, highlighting the critical nature of 5G networks, and the federal government is contemplating supplementing the technical security check for 5G networks with a political review process.

Despite the converging views as to what sectors are considered critical, the exact definition of critical activities may differ greatly between Member States (e.g., which steps of the semiconductor value chain are covered—only the production as such, or also required equipment, input materials, chip design.

Some national FDI regimes determine filing requirements or intervention rights based solely on the size of the stake acquired, and cover share deals and asset deals alike; others rely on different or additional factors, such as the target's revenues.

By way of illustrative example, in the healthcare sector, the German regime provides for a filing obligation for an investment by a non-EU/EFTA-based acquirer of:

Prior approval is required in Austria only if the target company employs ten persons or more, and if it has annual turnover and/or annual balance equal to or more than an annual revenue of €2 million or more.

Even where transactions are out of the formal scope of the FDI regimes, Member States may be prepared to intervene through targeted measures. The following measures adopted in Germany are illustrative:

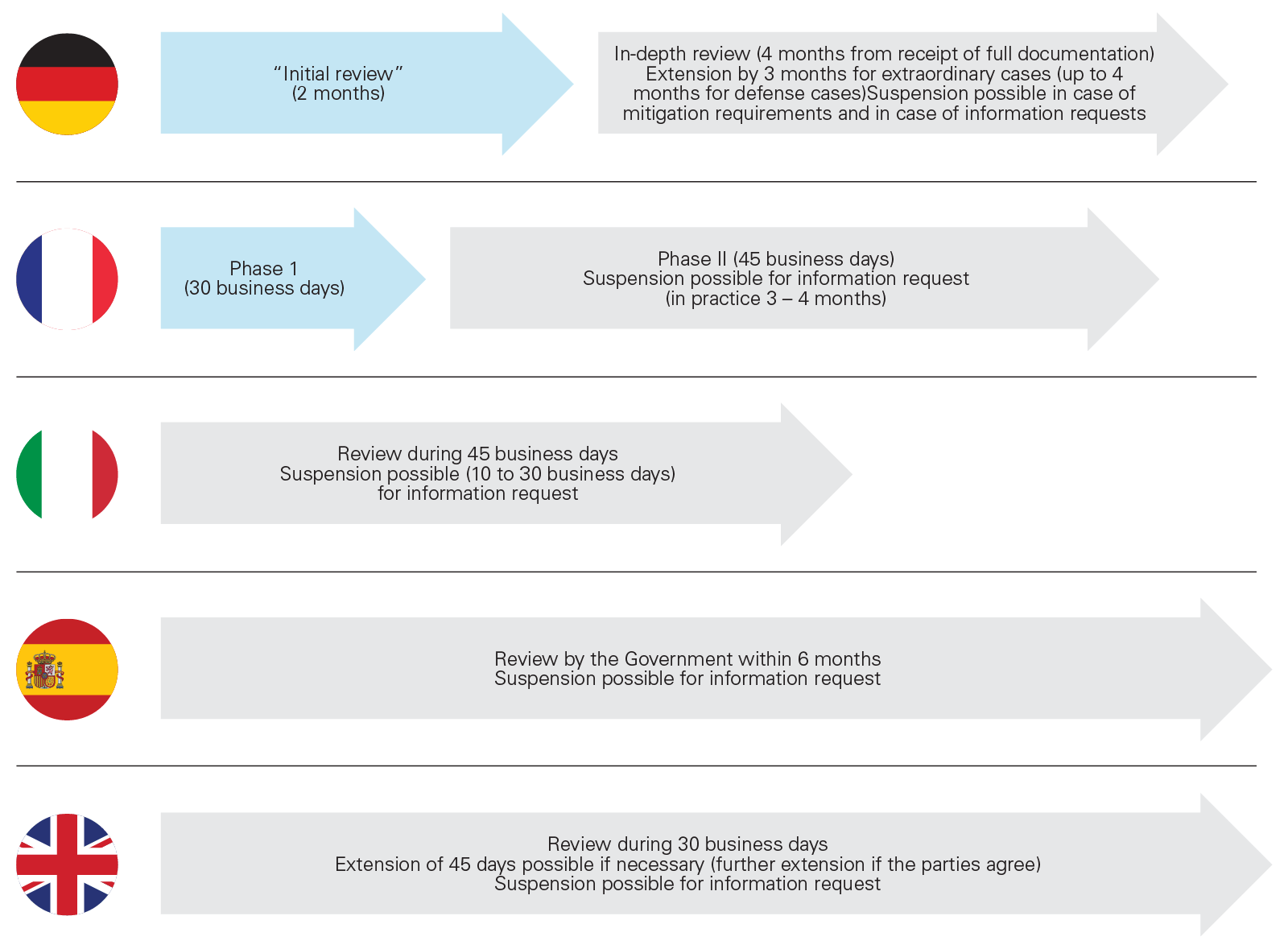

The duration of proceedings differs widely between jurisdictions. Generally, the process takes several months, and many feature a two-phase process (initial review period followed by in-depth review) and provide for stop-the-clock mechanisms, such as suspension based on information requests, or negotiation of mitigation requirements.

Blocking decisions on national security grounds remains an exception in most Member States

Blocking decisions on national security grounds remains an exception in most Member States. The EC's 2021 annual report indicates that only 1 percent of all decided cases were eventually blocked by national authorities. Issuing a formal veto to a potential foreign investor may leave the target business without a new investor, as illustrated by the recent Photonis and Carrefour examples in France. In March 2020, the French Minister of the Economy issued an informal objection to US company Teledyne Technologies Inc.'s contemplated investment in Photonis, a French producer and supplier of light intensifier tubes using digital technology with military applications.

Teledyne finally decided to withdraw its offer. In January 2021, French finance minister Bruno Le Maire expressed public opposition to Canadian store operator Alimentation Couche-Tard Inc.'s proposed €16.2 billion takeover of French retail group Carrefour. Le Maire reportedly said Carrefour is a "key link in the chain that ensures the food security of the French people" and that its acquisition by a foreign competitor would put France's food sovereignty at risk. Couche-Tard finally decided to withdraw its offer.

Clearance with "remedies" (mitigation agreements) is becoming customary in an increasing number of Member States. According to the EC's 2021 annual report, 23 percent of the decisions involved an approval with conditions or mitigating measures. Remedies generally include maintaining sufficient local resources related to the sensitive activities; restrictions on the use of intellectual property rights or on the governance of the target company; mandatory continuation of sensitive contracts to ensure continued services; appointing an authorized security officer within the target company and reporting obligations, etc. In extreme cases, national authorities may also impose mandatory disposal of sensitive activities to an approved acquirer.

According to the EC's 2021 annual report, the five main countries of origin of the 414 cases notified to the EC were the US (40 percent), the UK (10 percent), China (7 percent), the Cayman Islands (5 percent) and Canada (4 percent). Russia accounted for less than 1.5 percent of the cases and Belarus for 0.2 percent.

The investor origin continues to be one of the most relevant considerations in making the risk assessment. For example, Germany issued or threatened an increasing number of prohibitions on transactions originating from China and Russia. A prominent recent example concerns the partial prohibition of the proposed investment by Chinese state-owned company Cosco Shipping Group in a container terminal in the Port of Hamburg. While the investment originally was of 35 percent, the German Chancellor only authorized the acquisition of a stake below 25 percent.

1 Regulation (EU) 2019/452 of the European Parliament and of the Council of 19 March 2019 establishing a framework for the screening of foreign direct investments into the Union. The Regulation entered into force on October 11, 2020.

2 Regulation of the European Parliament and of the Council on foreign subsidies distorting the internal market, 2021/0114(COD).

3 EC's Communication of 18 October 2022, Commission's work program 2023, A Union standing firm and united, section 3.3.

4 EC's 2022 Guidance to Member States on FDI from Russia and Belarus.

5 A foreign subsidy shall be deemed to exist where the public authorities of a non-EU country (or private companies the actions of which can be attributed to the State) provides direct or indirect FFCs that confer a benefit to an undertaking engaging in an economic activity in the EU and the contribution is limited to one or more undertakings or industries.

6 https://ec.europa.eu/info/law/better-regulation/have-your-say/initiatives/13602-Distortive-foreign-subsidies-procedural-rules-for-assessing-them_en.

7 FFCs are defined very broadly and include any transfer of state funds, foregoing of state revenues as well as any provision or purchase of goods or services, which until further guidance from the EC is issued, may be interpreted to include all the contracts of companies with non-EU public bodies (or entities entrusted with public function). These FFCs may come from a central government, but also any public or private entity whose actions can be attributed to a third country. A key factor in the analysis will be whether such financial contributions or contracts with public bodies have been entered at market terms.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP