Global IPOs reached new highs

Fueled by strong stock markets and the need for yield, investors poured money into IPOs in 2021, resulting in a record-breaking year.

The global IPO market broke new records in 2021 on the back of robust stock market performances

The initial public offerings (IPO) market began 2021 with some questions as the world entered the second year of the COVID-19 pandemic. Would the recovery from the crisis seen during the second half of 2020 persist? Or would new developments related to the pandemic put the market back on ice, just as IPO activity had frozen during the first half of 2020?

As it turns out, the answers could not be clearer. Global IPO activity broke new records in 2021, with every region of the world recording significant increases in the number of businesses coming to market. The proceeds of these IPOs totaled more than US$600 billion—a new high.

With interest rates at rock bottom, investors poured money into capital markets—creating a supportive environment for IPOs. In addition, some of the impacts of the pandemic proved helpful to the IPO market. The way we live our lives is continuing to change rapidly, accelerating trends in how we work, shop and play, and the environmental imperative is more front of mind than ever. In industries such as financial services, life sciences and, particularly, technology, this is creating huge opportunities for innovative new businesses.

These trends—the energy transition and growing digitalization across all industries—will continue to motivate corporate activity, including IPOs. The market dynamics, however, may not be as supportive for new issuance this year as they were in 2021. As worries about inflation began to dominate headlines, and there were signs that central banks were planning to raise rates, equity markets began to cool at the end of 2021. Russia’s invasion of Ukraine and the continuing conflict there have increased volatility considerably—never good for IPOs. It is still unclear, however, how long the disruptions will last. Already the global economy was struggling with pandemic-related supply chain issues—these could be exacerbated by the impact of the situation in Ukraine, including sanctions on Russia.

The levels of IPO activity in 2021 would always have been a tough act to follow, but despite the significant headwinds equity capital markets face, the broad secular trends are in place to support further IPOs. It’s just a question of when.

Fueled by strong stock markets and the need for yield, investors poured money into IPOs in 2021, resulting in a record-breaking year.

After a flurry of new listings in the first quarter of 2021, SPAC IPOs slowed down considerably, but the asset class remains a viable path for companies to go public.

While IPO activity was robust throughout Europe, the Nordic region stood out.

IPOs of Latin America-based companies enjoyed a robust year in 2021, especially when it came to listings in Brazil in sectors like fintech.

The dust is settling after the flurry of activity in 2021, and the IPO market is facing considerable headwinds.

Fueled by strong stock markets and the need for yield, investors poured money into IPOs in 2021, resulting in a record-breaking year

3,022

The number of global listings in 2021

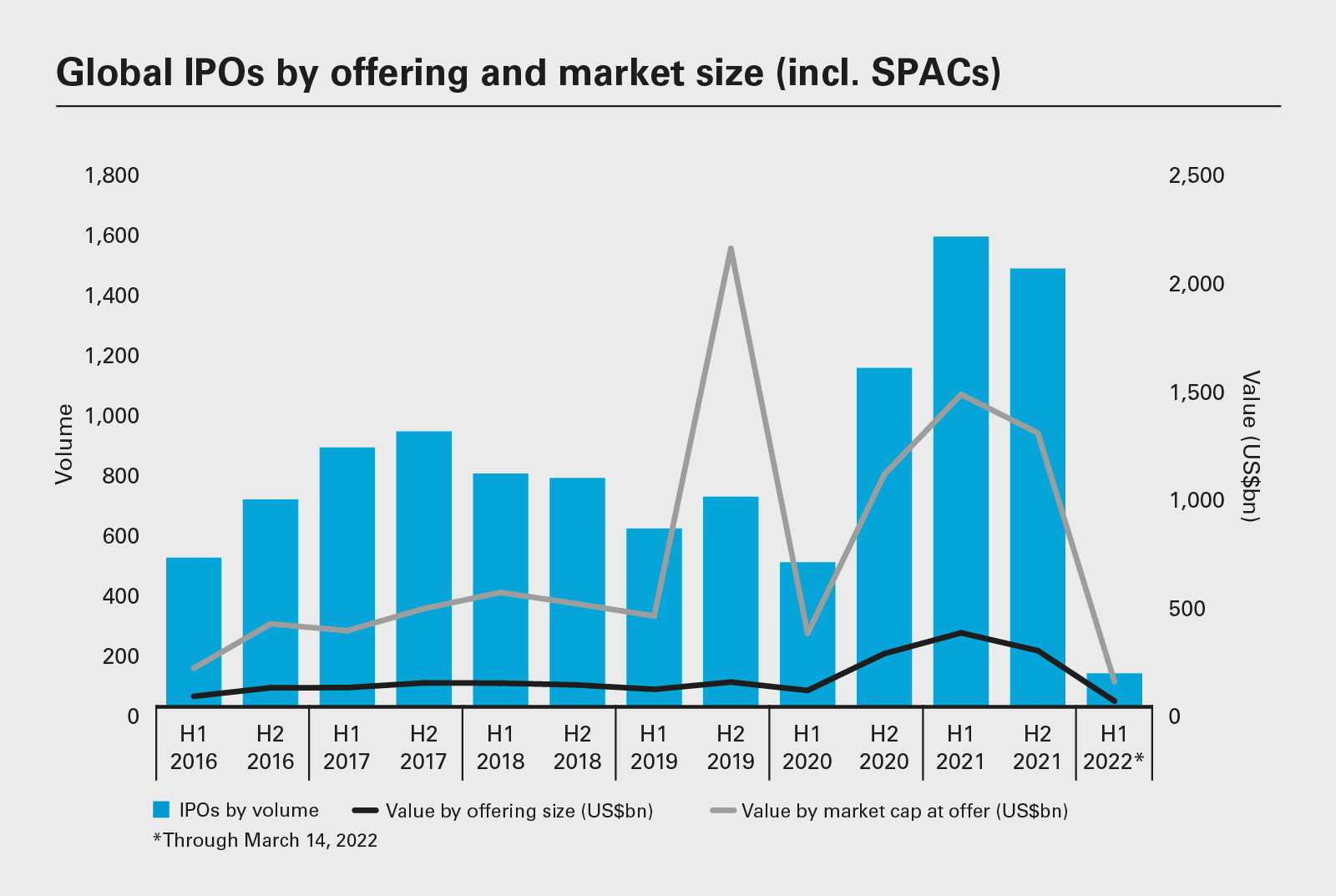

Global IPO activity hit an all-time high in 2021 as the market continued to roar back after a strong second half in 2020. A total of 3,022 new listings globally were announced last year, which raised US$601.2 billion among them.

To put those figures into context, they represent an 88 percent and 87 percent increase in volume and value terms, respectively, compared to 2020. No previous year has seen global IPO numbers break the 2,000 mark or raise more than US$350 billion. By any measure, last year was phenomenal.

Moreover, "global" accurately describes the stellar year for IPOs, with every region and sector seeing significant activity. Although the Americas remained the biggest market for IPOs—with 1,094 deals worth US$293.8 billion, increases of 133 percent and 83 percent, respectively, over 2020—other regions also registered sharp rises in activity. There were 1,338 IPOs in the Asia-Pacific region (APAC), worth US$188.6 billion in 2021 (up 48 percent and 47 percent, respectively, over 2020), while the Europe, the Middle East and Africa region (EMEA) saw 590 deals worth US$118.8 billion (increases of 150 percent and 271 percent, respectively, over 2020).

This spread is evidenced from the top of the deal charts downward. The biggest IPO of 2021 took place in the US, where the electric vehicle manufacturer Rivian Automotive raised US$13.7 billion. But the next largest deal took place on the other side of the world, as Hong Kong's Kuaishou, the live streaming and online marketing business, completed its US$6.2 billion listing. In Europe, meanwhile, the IPO of Poland's InPost, an e-commerce delivery business, raised US$3.9 billion, which also took it into the top-five listings of the year.

These three mega-IPOs took place in three different regions and three different sectors. Still, a common theme unites these transactions and forms an important part of the explanation for why IPO activity was so strong last year. Each of the deals speaks to the way the world has changed—and at an accelerated pace—in the wake of COVID-19.

For example, Kuaishou's successful IPO was on top of the trend toward technology-enabled home entertainment—embraced in even greater numbers during a time when people were often stuck at home because of pandemic restrictions. InPost is in prime position to benefit from the continuing rise of e-commerce, another trend accelerated by COVID-19.

As for Rivian Automotive, its innovative technologies—focused on industrial vehicles as well as passenger cars—carry huge potential as the world confronts climate-related issues. Despite the strong decarbonization trend in the automotive sector, however, Rivian has faced supply-chain challenges and inflationary issues which have forced the company to cut back on production targets. The announcement of its cut in production has led to a dramatic drop in the company's share price.

Indeed, the COVID-19 crisis cemented the perception that the world is undergoing a period of disruption and transformation. Consumers changed their behavior and a new generation of fast-growth companies that met their needs evolved at speed—and drove activity in the IPO market, as boards sought the financial firepower to support their journeys.

Innovation and technology sit at the heart of that story. But while last year's IPO markets saw a surge of activity in the technology sector, it is important to recognize the key role of convergence; many of the biggest deals last year involved companies in other industries whose potential is being enabled by technology, rather than pure tech firms.

In Brazil, the US$2.6 billion flotation of Nu Holdings was the biggest Latin American IPO of the year; Nu's digital banking services leverage the latest advances in fintech innovation. Another good example of this phenomenon is Coupang, the South Korean business that completed a US$4.6 billion IPO last year. Its commitment to e-commerce fulfillment and logistics innovation proved compelling to investors.

It helped that these businesses—and IPOs from across every sector—knew they could land in a supportive market. Although the end of the year saw increased volatility due to the rise of the Omicron variant of the COVID-19 virus, global stock markets were relatively stable and buoyant through the majority of 2021.

Indeed, while the second half of 2020 saw a bounce in IPO activity from the lows of the pandemic, 2021's IPO figures almost certainly reflect at least some pent-up demand. Businesses that had originally hoped to list in 2020 took the plunge in 2021 instead, as it became clear that the market environment would remain welcoming.

On the demand side, moreover, the appetite of potential investors for IPOs was strong. The loose monetary policies pursued by central banks over the past two years—instrumental in protecting the global economy from the COVID-19 crisis—flooded the markets with capital, but left yield and return in short supply. Investors were eager for new opportunities to deploy their cash.

Indeed, that demand was an important factor in the strong performance of one area of the IPO market in particular. Special purpose acquisition

US $601.2 billion

The total amount raised by global IPOs in 2021

companies (SPACs) boomed in the first part of 2021, before regulatory headwinds slowed down activity.

Last year's global IPO figures include 681 new SPACs, which raised US$172.3 billion in the aggregate. That was a major leap compared to 2020, itself a record year for SPACs, with the SPAC market up 166 percent year-on-year in volume terms, and 105 percent by value. Seven SPACs each raised more than US$1 billion last year.

The record levels of IPOs were not just due to the SPAC boom. Even stripping out these SPAC figures, IPO activity hit levels never previously seen. Excluding SPACs, the IPO market around the world saw 2,341 new issues raising US$428.9 billion during 2021. That was higher than in any previous year on record. By volume, IPO activity excluding SPACs rose 73 percent last year compared to 2020; in value terms, 2021 was 81 percent ahead.

Against this overall backdrop, very few sectors of the global market saw a fall-off in IPO activity; indeed, real estate and property was the only notable sector to see fewer IPOs in 2021 than in 2020—and the decline was small.

Still, three sectors dominated. Among them, finance, technology and life sciences accounted for more than half of all 2021 IPOs worldwide—and raised more than half of the total proceeds.

The technology sector led the way, accounting for 631 IPOs during 2021, with a collective value of US$158.2 billion. That was an increase of 80 percent in deal volumes and 106 percent by value year-on-year. Indeed, the sector was responsible for three of the five largest IPOs of the year, and five of the top ten. The theme of convergence is very apparent here—those larger deals, such as the IPOs of Kuaishou and Coupang, were at the confluence of technology and other business activities.

In the life sciences sector, meanwhile, there were 366 IPOs around the world last year, up 67 percent compared to 2020. These IPOs collectively raised US$60.5 billion, a 34 percent increase over the same period. By and large, deals in this sector in 2021 tended to be smaller—not one life sciences IPO made it into the top 20 by size—with businesses in areas such as biotech and digital health naturally of a more modest scale. Still, there were some larger issues. South Korean vaccines specialist SK Bioscience raised US$1.3 billion from its listing and Agilon Health, a US-based platform for primary care providers, generated US$1.2 billion.

Finance was in third place (excluding SPAC listings), with 176 IPOs worth US$25.9 billion over the course of the year, up 238 percent and 150 percent, respectively. Notable deals include the Nu Holdings IPO in Brazil, as well as the listing of mobile-only bank Kakao Bank in South Korea, which raised US$2.2 billion. Both transactions demonstrate the ongoing convergence between finance and technology—a global trend that is still ramping up.

With so much issuance taking place, one question mark for the global IPO market last year might have been its ability to digest the new arrivals. In fact, despite a few high-profile examples of companies trading under their listing prices, post-listing performance was respectable: 70 percent of IPOs rose on their first day of dealings last year—and only 7 percent fell back, broadly in line with previous years.

Moreover, that performance was typically sustained: Six months after the IPO, 50 percent of IPOs were trading above their listing price, including 45 percent that were up by more than 11 percent. Although this did not quite match 2020, when 87 percent of IPOs were trading at least 11 percent above their IPO prices six months after listing, it is in line with pre-pandemic years. For instance, 45 percent of firms that listed in 2019 were trading 11 percent or more above their IPO prices six months post-IPO.

Notable exceptions include Rivian, which faced manufacturing delays due to supply-chain issues, and video content sharing app Kuaishou, the second biggest IPO of the year. Kuaishou saw its share price drop, which has been attributed in part to worries around intensifying regulatory scrutiny of technology companies by the Chinese government.

A blockbuster year like 2021 would have been a tough act to follow in any circumstances. But strong headwinds could mean that 2022 will be a far quieter time for equity capital markets. Heading into the new year, the IPO markets faced the challenges of rising inflation, slowing economic growth, and the waning albeit continued threat of further COVID-19-related shutdowns, as well as continued geopolitical tensions.

Of course, all of this has been further exacerbated if not eclipsed by the situation in Ukraine, requiring the global markets to assess and absorb the possibility of a much less interconnected world economy going forward. In the short term, there have been disruptions to the global economy, as sanctions and other measures begin to impact the energy markets. While the European IPO market may be the most directly affected in the short term, all regions of the global markets have started to feel the repercussions.

The decision by the US Federal Reserve to raise its benchmark interest rate in March has only further dampened enthusiasm for equities, as has its messaging that it plans to take an aggressive approach to raising rates for the rest of 2022 and into 2023.

Already, companies have been waiting longer before listing, thanks to the high levels of funding available in private markets. With conditions for new listings becoming less welcoming, firms mulling an IPO may decide to stay private for longer, sitting out this period of volatility.

That said, the structural drivers at play in the IPO markets, as the global economy shifts to accommodate bold new trends, and the technology convergence story continues, show no sign of dissipating. Although the number of listings will almost certainly be lower than last year, there are still reasons to expect healthy IPO activity—especially outside of the EMEA region.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: Global IPOs by offering and market size (incl. SPACs) (PDF)

View full image: Global IPOs by offering and market size (incl. SPACs) (PDF)