Global IPO markets pause to take a breath

Inflation concerns, rising interest rates and the specter of war cast a more sober tone over equity markets in 2022 and through Q1 2023, throttling appetite for IPOs in most regions—but not all

It was clear in the opening months of 2022 that the winds had changed for the global IPO market as compared to the prior year, a rocky path that continued throughout the year and into the first quarter of 2023, but with a few notable bright spots

As we reported in last year's issue of the Global IPO Report, inflation concerns were starting to mount in early 2022 and investors were beginning to accept the prospect that central banks would need to step in to rein in demand. Against that backdrop, Russia invaded Ukraine, further disrupting already frayed supply chains and sending global energy prices soaring. This put further upward pressure on inflation and interest rates have been rising almost vertically since then.

None of this has been kind to IPO sentiment. In 2022, total global IPO value, including SPACs, came in at US$170.7 billion, a decline of 72 percent year-on-year. Excluding SPACs, the total was US$153.9 billion, down 65 percent year-on-year. While 2021 had been a record-breaking year and was unlikely to be repeated under the best of circumstances, these were the lowest global IPO value totals stretching back to 2016.

This continued into Q1 2023, with only US$26 billion in IPOs, including SPACs, down 53 percent year-on-year. Excluding SPACs, this total came in at US$25 billion in IPOs, 42 percent lower than Q1 2022.

Having said that, some context is helpful. Although SPAC deal value declined as compared to 2021, 2022 levels were still well above levels seen prior to the pandemic and the emergency monetary stimulus that supercharged the markets. Banks and investors may have balked at the SEC's promise of stricter regulation, but SPACs have nonetheless cemented themselves as a credible strategy for swiftly accessing public market fundraising.

Moreover, global IPO volume held up surprisingly well despite the macro and market volatility. Of note, larger ticket listings have been concentrated on non-US exchanges, with the Asia-Pacific (APAC) region proving to be comparatively robust, and the Middle East making notable moves on the IPO stage.

In the first quarter of 2023, a positive sentiment was settling over the markets and there were high hopes that a more stable base was being formed from which companies could soon begin to launch their IPOs. In March, however, cracks began to show following the collapse of Silicon Valley Bank, as liquidity issues emerged at high-profile banks in both the US and Europe. Investors watched to see whether any more shoes might drop, as interest rates continued to climb in response to inflationary pressure. Nonetheless, there is cause for cautious optimism about what the remainder of 2023 may hold, as disinflationary signals begin to emerge.

Inflation concerns, rising interest rates and the specter of war cast a more sober tone over equity markets in 2022 and through Q1 2023, throttling appetite for IPOs in most regions—but not all

Last year was a volatile 12 months for the tech sector, with a steep sell-off in growth stocks and a drop in IPOs—but, although the sector was down, it was by no means out

No region demonstrated more resilience than APAC in 2022, with the largest deal globally, the greatest total IPO value and volume, and the smallest year-on-year declines

The US Securities and Exchange Commission has plans to regulate SPACs more closely and mandate ESG reporting—sponsors and companies should pay close attention

Recent months have been exceptionally quiet, especially for the North American and EMEA IPO markets, as the bears have taken the upper hand—and investors and issuers are now hoping for a more active second half in 2023

Last year was a volatile 12 months for the tech sector, with a steep sell-off in growth stocks and a drop in IPOs—but, although the sector was down, it was by no means out

Once again, the technology sector dominated worldwide IPOs in 2022, despite experiencing one of its worst years on public stock markets in over a decade. Nasdaq, the most closely watched tech-centric stock exchange in the world, did not have a single technology IPO valued over US$1 billion last year. The largest came in just below this mark, at US$990 million, which involved Intel spinning off its self-driving cars business Mobileye five years after acquiring it. The benchmark Nasdaq 100 saw a 33 percent year-on-year decline last year—its worst performance since 2008.

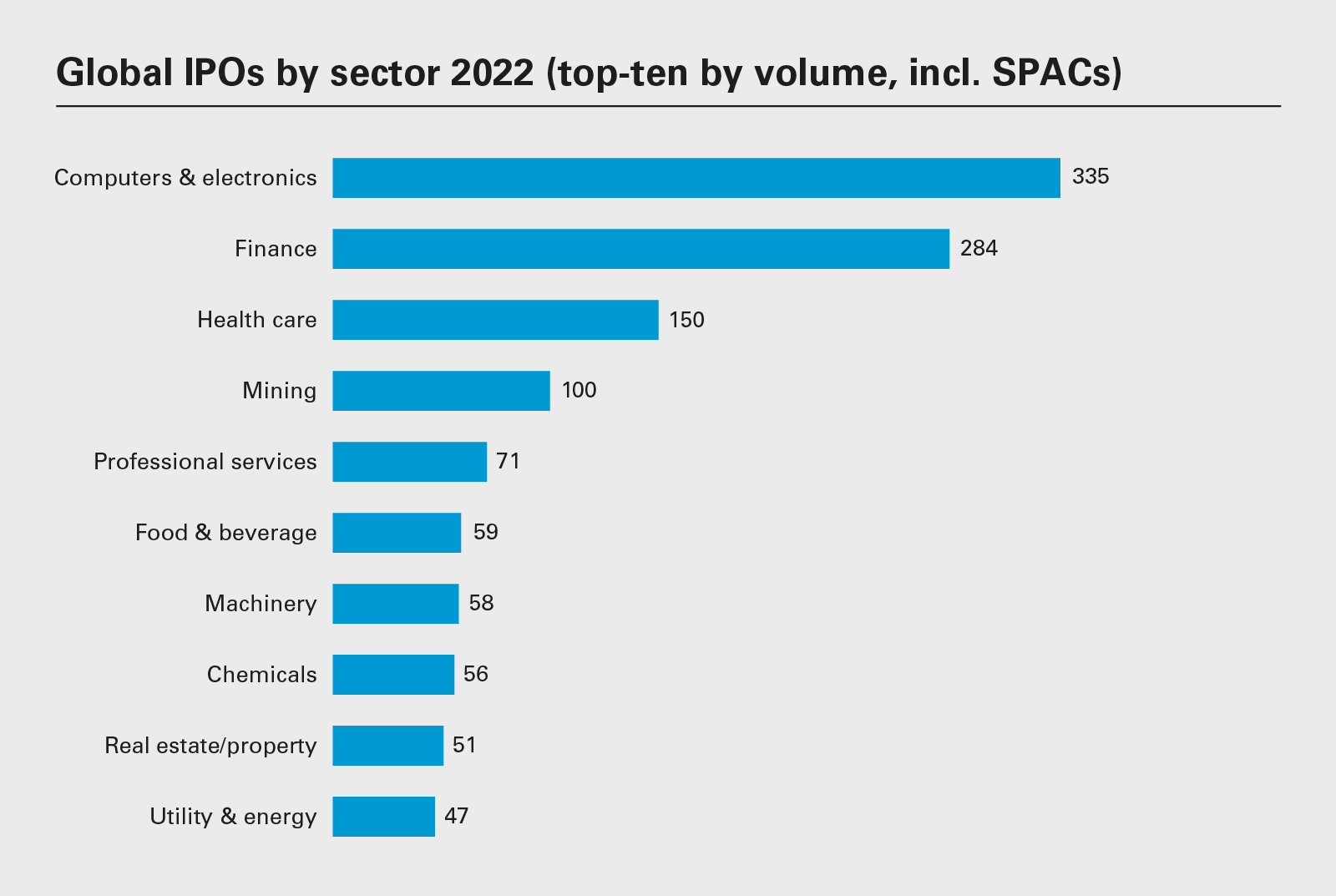

335

The total number of tech listings in 2022 (including SPACs)

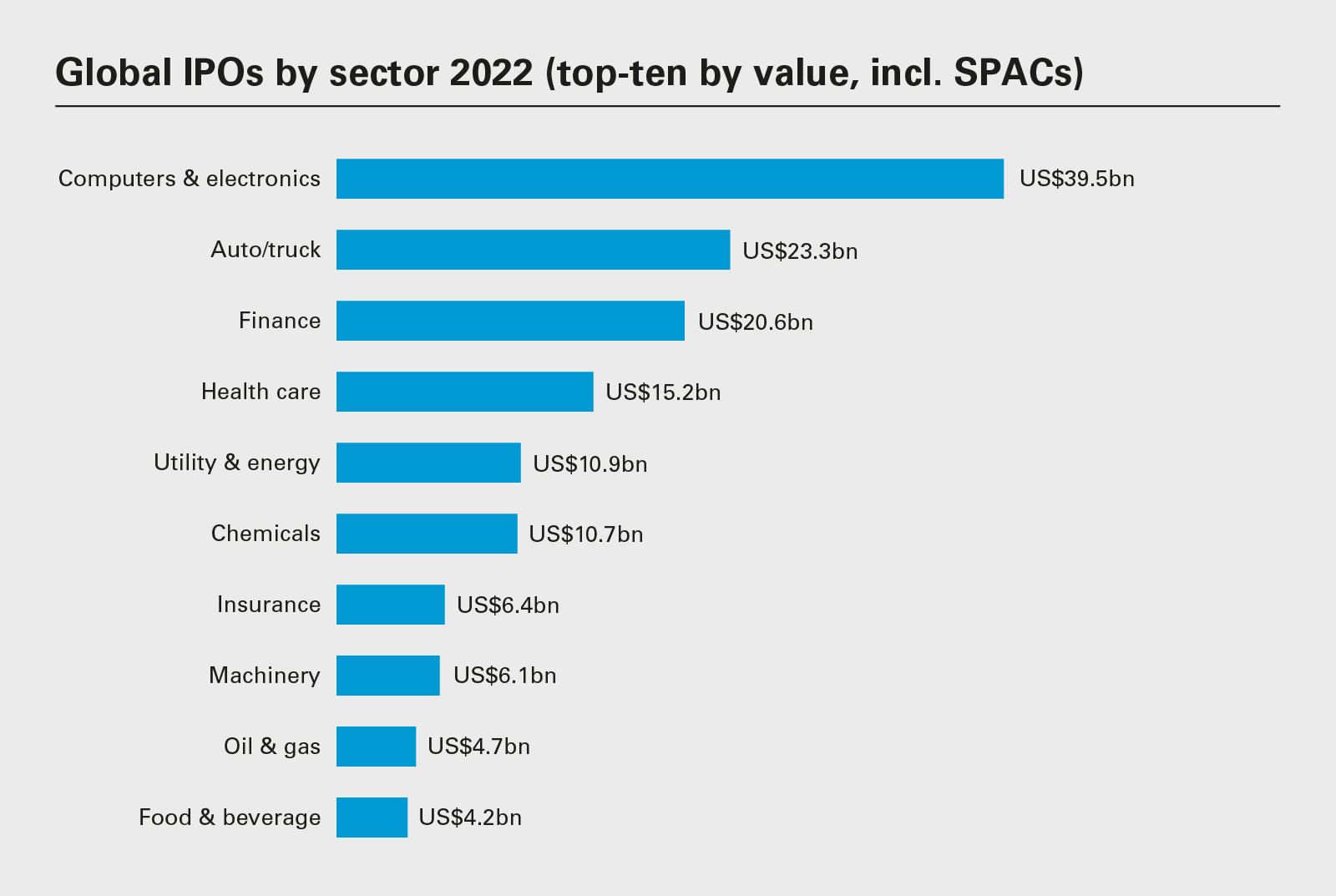

Notwithstanding the downturn in IPO activity, the tech sector had more public offerings in 2022 than any other sector—even with a 47 percent drop in volume year-on-year to 335 IPOs (including SPACs) in the sector globally. It was also the highest value sector for IPOs during the same period, although there was a 75 percent decline, year-on-year, to US$39.5 billion.

This downturn in activity reflects the fact that the US tech IPO market became a relative ghost town following an unprecedented run. The previous year saw a slate of highly anticipated IPOs, including electric vehicle company Rivian, Toast (a software firm that provides solutions for restaurants), GitLab and HashiCorp (both cloud software vendors) and the stock-trading application Robinhood, not to mention the direct listings of crypto platform Coinbase and video game smash Roblox.

In 2022, that momentum came to a halt. At the start of 2022, risk-averse investors took a more cautious approach, favoring solid financial fundamentals such as present-day earnings, inflation-resistant business models and cash-heavy balance sheets to help withstand an economic downturn and sustained higher interest rates. This caused some pre-IPO companies to revise their plans, having observed their counterparts in the public market experience significant declines in their stock prices, some dropping by as much as 90 percent from the record highs achieved in the previous year.

While traditional venues may have been quiet, a lot of action took place on China's Sci-Tech Innovation Board, part of the Shanghai Stock Exchange and also known as the STAR Market. This included the largest tech IPO globally: Hygon Information Technology, which makes and distributes computer components and is on a US Department of Commerce watchlist requiring American companies to seek approval before selling goods and services to Hygon.

Notably, 18 of the top 25 finance-related IPOs in North America were SPAC offerings. These deals were possible because investors benefit from optionality.

Mainland China's IPOs primarily focus on local investors due to the challenges posed by capital controls that restrict foreign investors from participating in the initial IPO allocation (but not post-IPO trading). As a result, these IPOs generally experience significant price increases when they begin trading. The Hygon IPO was no exception, trading up by 67 percent on its first day.

In a similar fashion, shares of Jinko Solar had a first-day surge of 111 percent on the STAR Market as overseas investors crowded into one of the world's largest solar panel manufacturers post-IPO. The company raised just under US$1.6 billion from the offering, putting it in second place in the technology sector to Hygon, with Mobileye's return to the Nasdaq representing the industry's third biggest float.

The second most active sector globally behind tech on a volume basis was financial services (excluding insurance), which performed relatively well by volume at 284 deals (including SPACs) despite a 67 percent fall, year-on-year, but IPO values dropped dramatically, raising US$20.6 billion during the same period, a 90 percent decline.

TPG's float was big news because it had been a long time coming and the PE firm joined the ranks of The Carlyle Group, Apollo, KKR and Blackstone. The latter mega fund managers have enjoyed a change of fortune in recent times, following years of relatively tepid post-IPO share price activity. By adding new strategies and scaling up their assets under management, public market investors have come to recognize their inherent value.

Notably, 18 of the top 25 finance-related IPOs in North America were SPAC offerings. These deals were possible because investors benefit from optionality. SPACs raise at a nominal share price of US$10, offer a yield and investors can redeem their cash once a merger target has been found because either they do not like the deal or have changed their opinion on the state of the overall market. Notwithstanding looming regulatory questions, these factors and their fast route to market make SPACs comparatively painless IPOs in contrast to traditional corporate deals.

Having said that, these IPOs were on the smaller side. After the US$750 million Screaming Eagle Acquisition Corp. float, the next largest was the US$525 million Gores Holdings IX IPO. No other SPAC in North America was valued over US$500 million and this trend toward smaller deals is likely to continue until further notice is provided by the SEC.

The health care sector came in a distant third place by volume at 150 listings (including SPACs), a 58 percent drop year-on-year. These were valued at US$15.2 billion in aggregate, putting the sector in fourth place by value behind technology, automotive and finance. Health care listings were also of the smaller variety. Only one health care IPO made it into the top 25 deals across all regions: Shanghai United Imaging Healthcare's US$1.6 billion debut, which was also APAC's third-largest deal. Similar to Hygon and Jinko, United Imaging's shares flew after opening. United Imaging (a medical imaging and radiotherapy equipment manufacturer) claims to own the world's largest medical equipment production base and its market dominant position made it a must-have for institutional investors.

Generally, health care has proven to be a haven for investors. Case in point: The S&P 500 Health Care Sector Index was flat in 2022 against a backdrop of falling indices. Demographic pressures mean that demand for care services continues to climb irrespective of the macroeconomic climate and companies in the sector often benefit from large margins. These are the kinds of characteristics that investors are looking for in today's inflationary environment. However, even with these perennial tailwinds, health care IPO value was still down year-on-year, falling by as much as 75 percent.

In 2022, companies were waiting for calmer waters before choosing to float. This means that pipelines have built up and these businesses are now seeking signs of stabilization in 2023 to act on their plans.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP

View full image: Global IPOs by sector 2022 (top-ten by volume, incl. SPACs) (PDF)

View full image: Global IPOs by sector 2022 (top-ten by volume, incl. SPACs) (PDF)

View full image: Global IPOs by sector 2022 (top-ten by volume, incl. SPACs) (PDF)

View full image: Global IPOs by sector 2022 (top-ten by volume, incl. SPACs) (PDF)