Global IPO markets pause to take a breath

Inflation concerns, rising interest rates and the specter of war cast a more sober tone over equity markets in 2022 and through Q1 2023, throttling appetite for IPOs in most regions—but not all

It was clear in the opening months of 2022 that the winds had changed for the global IPO market as compared to the prior year, a rocky path that continued throughout the year and into the first quarter of 2023, but with a few notable bright spots

As we reported in last year's issue of the Global IPO Report, inflation concerns were starting to mount in early 2022 and investors were beginning to accept the prospect that central banks would need to step in to rein in demand. Against that backdrop, Russia invaded Ukraine, further disrupting already frayed supply chains and sending global energy prices soaring. This put further upward pressure on inflation and interest rates have been rising almost vertically since then.

None of this has been kind to IPO sentiment. In 2022, total global IPO value, including SPACs, came in at US$170.7 billion, a decline of 72 percent year-on-year. Excluding SPACs, the total was US$153.9 billion, down 65 percent year-on-year. While 2021 had been a record-breaking year and was unlikely to be repeated under the best of circumstances, these were the lowest global IPO value totals stretching back to 2016.

This continued into Q1 2023, with only US$26 billion in IPOs, including SPACs, down 53 percent year-on-year. Excluding SPACs, this total came in at US$25 billion in IPOs, 42 percent lower than Q1 2022.

Having said that, some context is helpful. Although SPAC deal value declined as compared to 2021, 2022 levels were still well above levels seen prior to the pandemic and the emergency monetary stimulus that supercharged the markets. Banks and investors may have balked at the SEC's promise of stricter regulation, but SPACs have nonetheless cemented themselves as a credible strategy for swiftly accessing public market fundraising.

Moreover, global IPO volume held up surprisingly well despite the macro and market volatility. Of note, larger ticket listings have been concentrated on non-US exchanges, with the Asia-Pacific (APAC) region proving to be comparatively robust, and the Middle East making notable moves on the IPO stage.

In the first quarter of 2023, a positive sentiment was settling over the markets and there were high hopes that a more stable base was being formed from which companies could soon begin to launch their IPOs. In March, however, cracks began to show following the collapse of Silicon Valley Bank, as liquidity issues emerged at high-profile banks in both the US and Europe. Investors watched to see whether any more shoes might drop, as interest rates continued to climb in response to inflationary pressure. Nonetheless, there is cause for cautious optimism about what the remainder of 2023 may hold, as disinflationary signals begin to emerge.

Inflation concerns, rising interest rates and the specter of war cast a more sober tone over equity markets in 2022 and through Q1 2023, throttling appetite for IPOs in most regions—but not all

Last year was a volatile 12 months for the tech sector, with a steep sell-off in growth stocks and a drop in IPOs—but, although the sector was down, it was by no means out

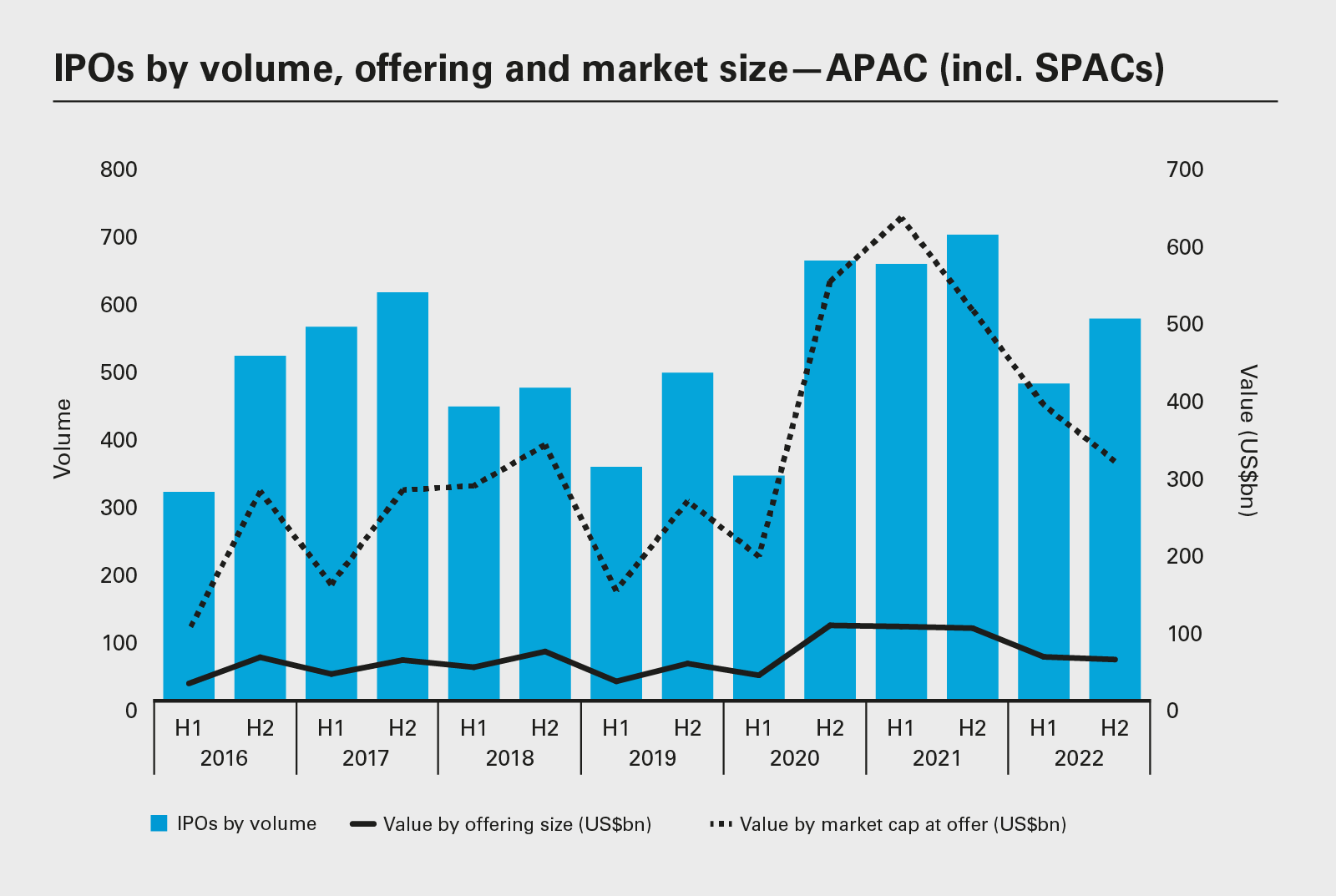

No region demonstrated more resilience than APAC in 2022, with the largest deal globally, the greatest total IPO value and volume, and the smallest year-on-year declines

The US Securities and Exchange Commission has plans to regulate SPACs more closely and mandate ESG reporting—sponsors and companies should pay close attention

Recent months have been exceptionally quiet, especially for the North American and EMEA IPO markets, as the bears have taken the upper hand—and investors and issuers are now hoping for a more active second half in 2023

No region demonstrated more resilience than APAC in 2022, with the largest deal globally, the greatest total IPO value and volume, and the smallest year-on-year declines

APAC is proving to be the most resilient regional IPO market by some distance. In Q1 of this year, there were 223 deals (including SPACs) worth an aggregate US$17.6 billion, representing year-on-year declines of 5 percent and 50 percent, respectively. Compare that with North America, which saw a 60 percent annual fall in IPO volume and value plummet 76 percent (in both cases, including SPACs) in the first three months of 2023.

23%

The year-on-year decrease in volume in the APAC IPO market in 2022 (including SPACs)

The strength of the APAC region was also on full display the previous year. There were 1,034 deals (including SPACs) recorded in 2022, a drop of only 23 percent year-on-year (as compared to declines of 77 percent in North America and 60 percent in EMEA) and the third-highest annual performance going back to 2017.

Mirroring this robustness, while value fell by 42 percent to US$110.4 billion (including SPACs), it remained well above pre-pandemic totals, significantly outperforming both North America and EMEA combined in absolute dollar terms.

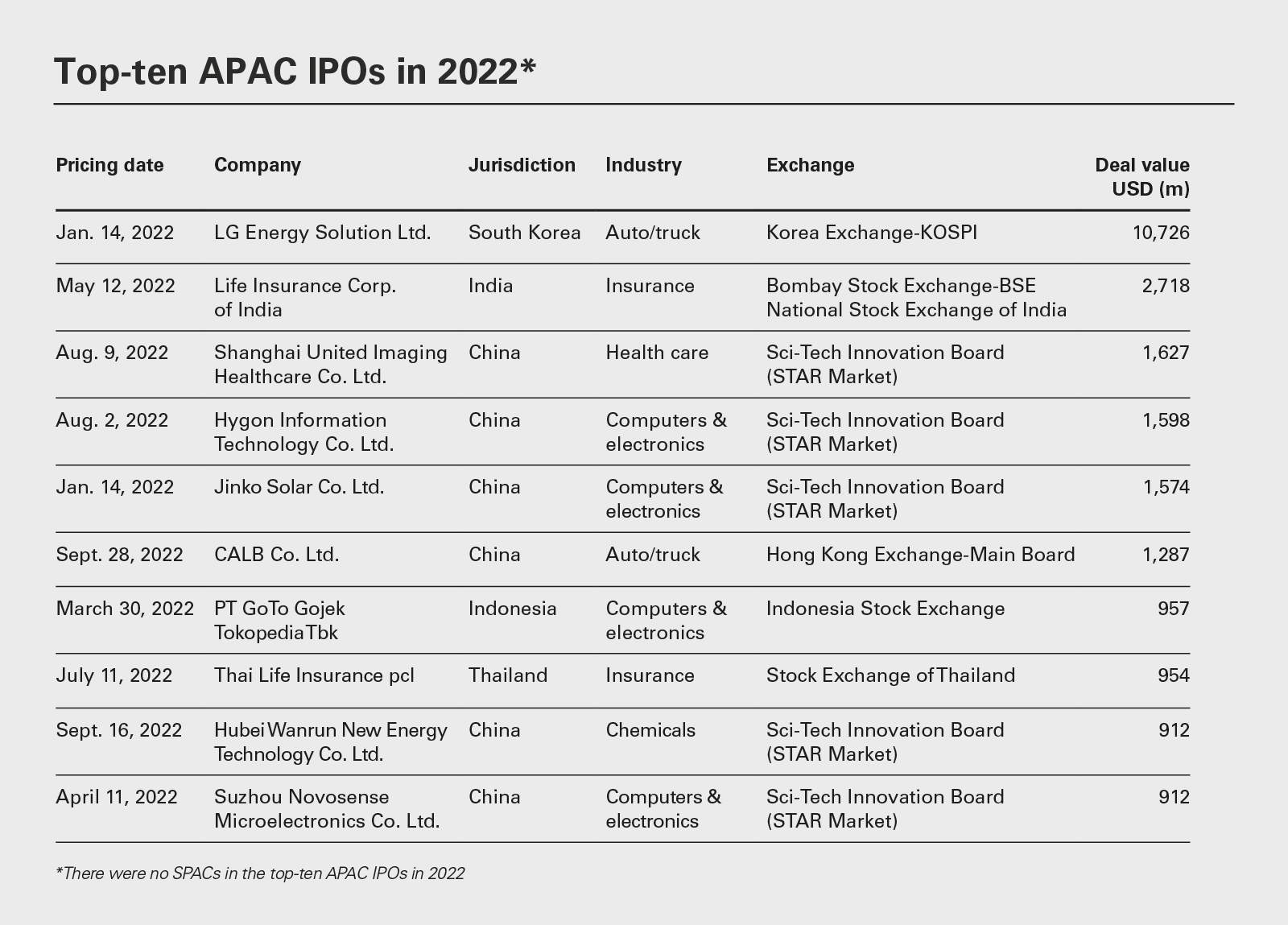

Looking at the top deals across the region, many records were broken in APAC's IPO market in 2022. For example, the US$10.7 billion LG Energy Solution listing was South Korea's largest IPO ever and the largest deal globally in the year.

State-operated insurer Life Insurance Corp. of India (LIC)—APAC's second biggest IPO of 2022—earned the same distinction in India. LIC pulled in US$2.7 billion in an oversubscribed offering for a 3.5 percent stake in the business, giving it a total valuation of nearly US$77.7 billion. This made it the largest business to go public in the world in 2022 and placed it among India's top 10 listed companies.

No other IPO in India came close to LIC in terms of value. However, what India lacked in large listings, it more than made up for in volume. India saw a 22 percent increase in the number of IPOs in 2022, according to Mergermarket, thanks to its large domestic investor base and impressive economic growth. India is expected to be the fastest-growing major economy in 2023, according to the International Monetary Fund (IMF). The agency predicts India's GDP will rise by 6.1 percent during its 2023-2024 fiscal year, even with the Reserve Bank of India's (RBI) monetary tightening policy.

And, while the largest Chinese deal—Shanghai United Imaging—came in third place in APAC IPOs by value in 2022 at US$1.6 billion, Mainland China was responsible for the lion's share of the region's largest deals in the year. More than a third of the top 25 largest global IPOs last year took place on the STAR Market, China's Nasdaq-style stock exchange, and the Shenzhen Stock Exchange.

China's capital markets are experiencing something of a paradigm shift lately. Last year, foreign investors were net sellers in the country's bond markets and mostly kept their distance from its equity markets. Meanwhile, the IPO pipeline has been increasingly influenced by the government.

In the past 10 years, vehicles known as "government guidance funds" have reportedly raised over US$900 billion to ensure early funding for companies in preferred industries such as high-end manufacturing, biotech and renewables. Additionally, policymakers have implemented reforms to enable faster listings once these companies are ready to go public.

The STAR Market is playing an essential role in the development of local pioneering tech firms. Launched in July 2019, the bourse is unique in that it allows companies without a profit history to list, unlike other Chinese stock exchanges. It also has a registration-based system that simplifies the IPO process and expedites the listing process. The market has seen rapid growth since its inception, with over 500 companies listed and a total market capitalization of over US$460 billion as of March 23, 2023.

China has recently expanded the STAR Market's registration-based IPO system to its other exchanges, which could further fuel activity. Under the previous regime, new listings had to be approved by the China Securities Regulatory Commission (CSRC), and now they only need to register with the regulator. It was announced on February 1, 2023 that this more streamlined approach would be expanded to all of Mainland China's exchanges, consolidating the IPO rules of the various bourses.

Hong Kong has its own plans to streamline its listing regime. In a move aimed at boosting its standing as a hub for innovative tech companies, the Hong Kong Stock Exchange published a consultation paper on October 19, 2022, proposing an alternative route for floating pre-profit, high-growth potential science and technology innovators that do not meet the existing listing requirements. The consultation period ended on December 18, 2022 and, once adopted, the new rules are expected to improve access to public markets among these early-stage companies by employing an approach similar to Nasdaq.

Previous concerns over the lack of transparency available to US investors in equity securities of China-based companies are showing signs of subsiding and will likely improve confidence. The Public Company Accounting Oversight Board (PCAOB), the US accounting watchdog, was granted access starting in the third quarter of 2022 to fully inspect and investigate Mainland China and Hong Kong-based PCAOB-registered auditing firms, which audit China-based companies listed on US exchanges. Prior to this, more than 100 China-based companies, including Alibaba, Baidu and JD.com, among others, faced the risk of delisting from the New York Stock Exchange and the Nasdaq.

The ability of PCAOB inspectors to fully inspect and investigate the relevant auditing firms could pave the way for more IPOs of China-based companies on US equity markets, which historically have been the deepest, most liquid in the world.

On the China regulatory front, on February 17, 2023, the CSRC introduced a new set of regulations that took effect on March 31, 2023, requiring domestic Chinese companies and those with a majority of operations and/or assets in China, generally, to seek approval before listing in other jurisdictions. The new rules also come with a set of obligations imposed on underwriters. While this is generally viewed as a positive step toward increasing transparency and streamlining the approval process, the potential impact on timetables and implications for underwriters remain to be seen.

The APAC region is highly diverse, which makes it difficult to draw many generalizations. Nevertheless, this market has arguably the most attractive underlying growth characteristics of anywhere in the world, including present-day GDP performance and long-run potential.

At a more granular level, there is a lot of divergence, particularly with regard to inflation. China stands out globally as taking a tentatively more dovish approach. While the Federal Reserve issued its first rate hike in June 2022 and other central banks followed its lead, which had the effect of quelling confidence in the equity markets, China trimmed its benchmark lending rate in August 2022. In the following months, as monetary policy was tightened further in other countries, China held its rate steady at 3.65 percent in an effort to stimulate business lending and economic growth.

That is a very different picture from other parts of APAC. India, for example, had its first hike in May 2022, finishing the year with a rate of 6.25 percent, and the RBI is currently expected to tighten rates further in 2023 to deal with inflation.

It's similar in Southeast Asia where the lending rate in Indonesia, the Philippines and Vietnam ranged between 5.75 and 6 percent by the end of last year. Indonesia finally left its key rate unchanged in February 2023, following six consecutive hikes. In the Philippines, inflation reached a 14-year high of 8.75 percent in January 2023, prompting its central bank to raise the benchmark interest rate by 50 basis points. Vietnam, meanwhile, also raised its rates by 100 basis points in October 2022 after a string of hikes (though, in March 2023, the country's central bank announced it was cutting several policy rates as the country's inflation was under control).

There were only two US$1 billion (approximately) raisings in Southeast Asia last year: Indonesia’s GoTo, which raised US$957 million, and Thai Life Insurance with US$954 million raised. GoTo has been closely watched following its genesis from the 2021 merger of Indonesia's two most valuable startups—ride-hailing giant Gojek and e-commerce firm Tokopedia. The company, which contributes an estimated 2 percent of Indonesia's GDP, is made up of three arms: Gojek, Tokopedia and fintech services business GoTo Financial. The stock fell since its listing in April, in line with the wider tech sell-off during this period, closing the year down nearly 75 percent.

Thai Life, meanwhile, was the largest ever insurance IPO in Southeast Asia and the region's third-largest IPO of a financial institution to date. While its stock climbed in the first two months after listing on the Stock Exchange of Thailand in July 2022, the trajectory subsequently shifted, with the stock ending just over 10 percent below its listing price by February 2023.

High inflation and interest rates are clear headwinds, just like in western markets. However, there are numerous variables at play. The underlying growth in Southeast Asia and its high proportion of young people—the IMF estimates that more than half of the population is under 30—is highly attractive to investors, especially with economic performance cooling in developed markets.

This growth and dynamism across the broader APAC region combined with its vast size could keep the region's IPO activity in the lead through 2023. Thematic tailwinds such as consumer demand for technology and fintech services, and necessary physical and digital infrastructure upgrades in an increasingly urban population, will support the right deals.

In a further possible boost to IPO activity in the region, recently, foreign investors have been rekindling their appetite for Chinese equities. In January 2023, there was more recorded volume from these buyers for already listed stock than for the whole of 2022. If this return of overseas investors persists, Chinese IPOs should see strong demand after going live. Reduced COVID-19 restrictions in the country and the wider region combined with capital market reforms will further catalyze an IPO market that has already displayed comparatively impressive momentum.

Strong narratives will continue to play a central role. In mid-April 2023, Harita Nickel raised approximately 10 trillion rupiah (US$672 million) in Indonesia's biggest listing this year. The company owns the country's first high-pressure acid leaching plant, which processes low-grade nickel ore from Harita's mining projects into mixed hydroxide precipitate, a precursor to the battery-grade nickel sulfate used for electric vehicle batteries. The share price surged on the first day of trading, which is a testament to the strength of the business's thematic tailwinds.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP

View full image: IPOS by volume, offering and market size-APAC (incl. SPACS) (PDF)

View full image: IPOS by volume, offering and market size-APAC (incl. SPACS) (PDF)

View full image: Top-ten APAC IPOS globally in 2022 (PDF)

View full image: Top-ten APAC IPOS globally in 2022 (PDF)