Global IPO markets pause to take a breath

Inflation concerns, rising interest rates and the specter of war cast a more sober tone over equity markets in 2022 and through Q1 2023, throttling appetite for IPOs in most regions—but not all

It was clear in the opening months of 2022 that the winds had changed for the global IPO market as compared to the prior year, a rocky path that continued throughout the year and into the first quarter of 2023, but with a few notable bright spots

As we reported in last year's issue of the Global IPO Report, inflation concerns were starting to mount in early 2022 and investors were beginning to accept the prospect that central banks would need to step in to rein in demand. Against that backdrop, Russia invaded Ukraine, further disrupting already frayed supply chains and sending global energy prices soaring. This put further upward pressure on inflation and interest rates have been rising almost vertically since then.

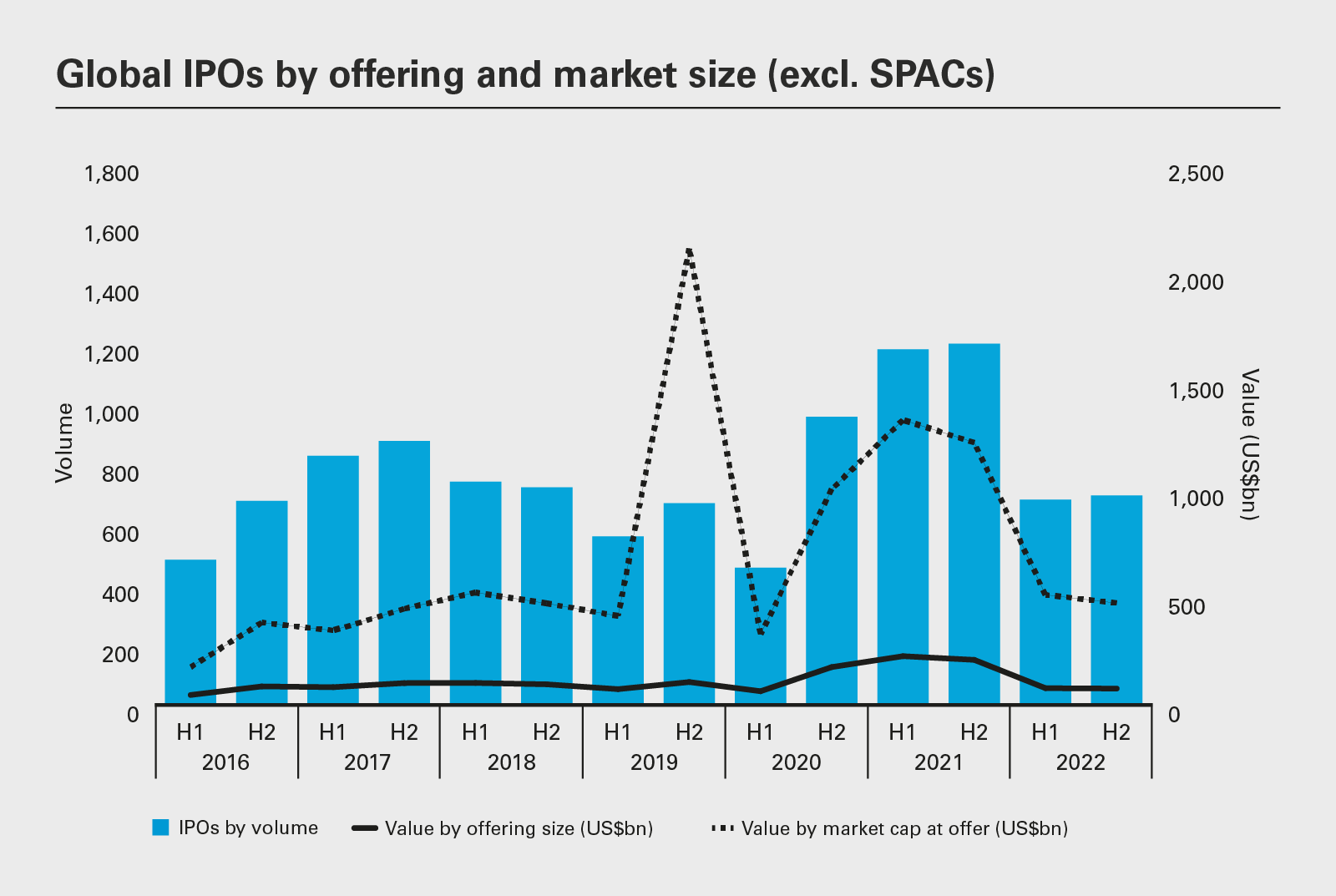

None of this has been kind to IPO sentiment. In 2022, total global IPO value, including SPACs, came in at US$170.7 billion, a decline of 72 percent year-on-year. Excluding SPACs, the total was US$153.9 billion, down 65 percent year-on-year. While 2021 had been a record-breaking year and was unlikely to be repeated under the best of circumstances, these were the lowest global IPO value totals stretching back to 2016.

This continued into Q1 2023, with only US$26 billion in IPOs, including SPACs, down 53 percent year-on-year. Excluding SPACs, this total came in at US$25 billion in IPOs, 42 percent lower than Q1 2022.

Having said that, some context is helpful. Although SPAC deal value declined as compared to 2021, 2022 levels were still well above levels seen prior to the pandemic and the emergency monetary stimulus that supercharged the markets. Banks and investors may have balked at the SEC's promise of stricter regulation, but SPACs have nonetheless cemented themselves as a credible strategy for swiftly accessing public market fundraising.

Moreover, global IPO volume held up surprisingly well despite the macro and market volatility. Of note, larger ticket listings have been concentrated on non-US exchanges, with the Asia-Pacific (APAC) region proving to be comparatively robust, and the Middle East making notable moves on the IPO stage.

In the first quarter of 2023, a positive sentiment was settling over the markets and there were high hopes that a more stable base was being formed from which companies could soon begin to launch their IPOs. In March, however, cracks began to show following the collapse of Silicon Valley Bank, as liquidity issues emerged at high-profile banks in both the US and Europe. Investors watched to see whether any more shoes might drop, as interest rates continued to climb in response to inflationary pressure. Nonetheless, there is cause for cautious optimism about what the remainder of 2023 may hold, as disinflationary signals begin to emerge.

Inflation concerns, rising interest rates and the specter of war cast a more sober tone over equity markets in 2022 and through Q1 2023, throttling appetite for IPOs in most regions—but not all

Last year was a volatile 12 months for the tech sector, with a steep sell-off in growth stocks and a drop in IPOs—but, although the sector was down, it was by no means out

No region demonstrated more resilience than APAC in 2022, with the largest deal globally, the greatest total IPO value and volume, and the smallest year-on-year declines

The US Securities and Exchange Commission has plans to regulate SPACs more closely and mandate ESG reporting—sponsors and companies should pay close attention

Recent months have been exceptionally quiet, especially for the North American and EMEA IPO markets, as the bears have taken the upper hand—and investors and issuers are now hoping for a more active second half in 2023

Inflation concerns, rising interest rates and the specter of war cast a more sober tone over equity markets in 2022 and through Q1 2023, throttling appetite for IPOs in most regions—but not all

Global IPO activity has pulled back sharply since the all-time records set in 2021. The start of 2023 has been exceptionally quiet. The 284 IPOs (excluding SPAC listings) listed in Q1 of this year is the lowest recording since COVID-19 first affected markets in Q2 2020, while total deal value came to just US$25 billion. For perspective, the pandemic-stricken second quarter of 2020 saw US$35.7 billion in deals.

1,380

The number of global listings in 2022 (excluding SPACs)

Looking back on 2022, a total of 1,380 IPOs (excluding SPAC listings) was recorded globally—a 42 percent decline on the previous year's tally, according to Mergermarket data. Nonetheless, this was still a solid showing. The six-year trailing average is 1,562 IPOs globally per year and this figure is clearly inflated by 2021's neck-bracing rally in activity. Last year comfortably outperformed the volumes seen in 2019 and was not far off 2020, though there was a material softening in the second half of 2022 as the market deteriorated.

It is in the value of proceeds raised where softness really showed. The US$153.9 billion in deals (excluding SPACs) was down 65 percent year-on-year, the lowest level since 2016. The trailing average for the previous six years is US$227.8 billion, which, again, is significantly enlarged by 2021's phenomenal performance. Even so, 2022 was something of a reset, as investors caught their breath following the whirlwind of the previous year.

One of the most defining characteristics of last year was how dramatically the regional distribution of IPOs shifted. The Americas, dominated by the New York Stock Exchange and Nasdaq, went from being a global deal value powerhouse in 2021 to the quietest regional market in the world. Excluding SPACs, IPO value came to US$7.4 billion—down 95 percent year-on-year—and these proceeds were shared among just 179 listings, a similarly steep annual decline of 67 percent.

Several factors contributed to this underperformance. One is that the US equity markets had leaned heavily into the technology sector, which has been especially prone to inflation and the rising cost of capital. The Federal Reserve (Fed) has also embarked on a far more aggressive monetary tightening cycle than anywhere else, measured by the rate of change, particularly compared with Europe.

The APAC region, by contrast, was something of an outlier. The region led on both value and volume measures, with US$107.4 billion in IPOs and 967 separate listings (excluding SPACs). This equated to year-on-year falls of only 42 percent and 25 percent respectively. APAC typically leads all other regions due to the scale of its collective economy—the largest in the world—but it has been interesting to see the market's relative strength under the circumstances, undergirded by a fast-paced macro environment.

Europe, the Middle East and Africa (EMEA) sat between the Americas and APAC, in both absolute and relative terms. The US$39.1 billion in IPOs spread over 234 deals (excluding SPACs) represented annual declines of 63 percent and 59 percent respectively. Russia's invasion of Ukraine loomed large over European equity markets and energy price inflation dented investor confidence throughout the year.

US $153.9 billion

The total amount raised by global IPOs in 2022 (excluding SPACs)

IPO activity across EMEA is a tale of two markets. The Middle East was a stronghold in the region, contributing three of the world's top 10 largest IPOs and seven of the largest 25 deals. The conflict in Ukraine soured confidence in Europe, but also sent the price of crude skywards, bolstering economies in the Middle East, while also emboldening investors and attracting foreign capital.

Several factors are contributing to the region's continued strength. For one, Saudi Arabia continues to ease restrictions on foreign investors in its capital markets and attract foreign blue chip companies to dual list their securities on the Saudi Stock Exchange, as the Kingdom seeks to draw more international capital, modernize its economy and raise its standing on the world stage. This includes allowing foreign qualified financial institutions with more than US$500 million in assets under management to participate in IPOs and hold securities listed in Saudi Arabia.

As part of these modernization efforts, governments throughout the Middle East are embarking on an ongoing privatization push. For example, in November 2021, Sheikh Maktoum bin Mohammed bin Rashid Al Maktoum, the ruler of Dubai, announced plans to sell 10 government and state-owned companies on the Dubai Financial Market, with the goal of expanding Dubai's principal stock market to AED3 trillion (US$817 billion).

In addition, sovereign wealth funds in the subregion, such as Saudi's Public Investment Fund (PIF) and the Abu Dhabi Investment Authority, have become major players in global finance in recent years. Their assets under management have swelled from accumulating large natural resource revenue surpluses. The common aim of these funds is to diversify their countries' wealth, leading them to be active direct investors. This is building a pipeline of potential IPOs that may come to fruition in the next three to five years, at the same time foreign capital is flowing into the region and demonstrating a clear appetite for offerings.

Case in point: In March 2023, as a banking liquidity crisis was unfolding in the US and Europe, shares in the 50x oversubscribed IPO of Adnoc Gas climbed as much as 25 percent in its first day of trading.

However, there may be some recalibration in the region's IPO markets in 2023. The price of oil is a strong proxy for investor appetite in the region and the price of crude fell steadily from mid-2022 before stabilizing from November 2022 to March 2023. The commodity showed further weakness in mid-March 2023 and investors will be watching this closely. However, the Middle East remains in a favorable position to weather any global headwinds. Local governments are also sure to do their part to maintain recent IPO activity.

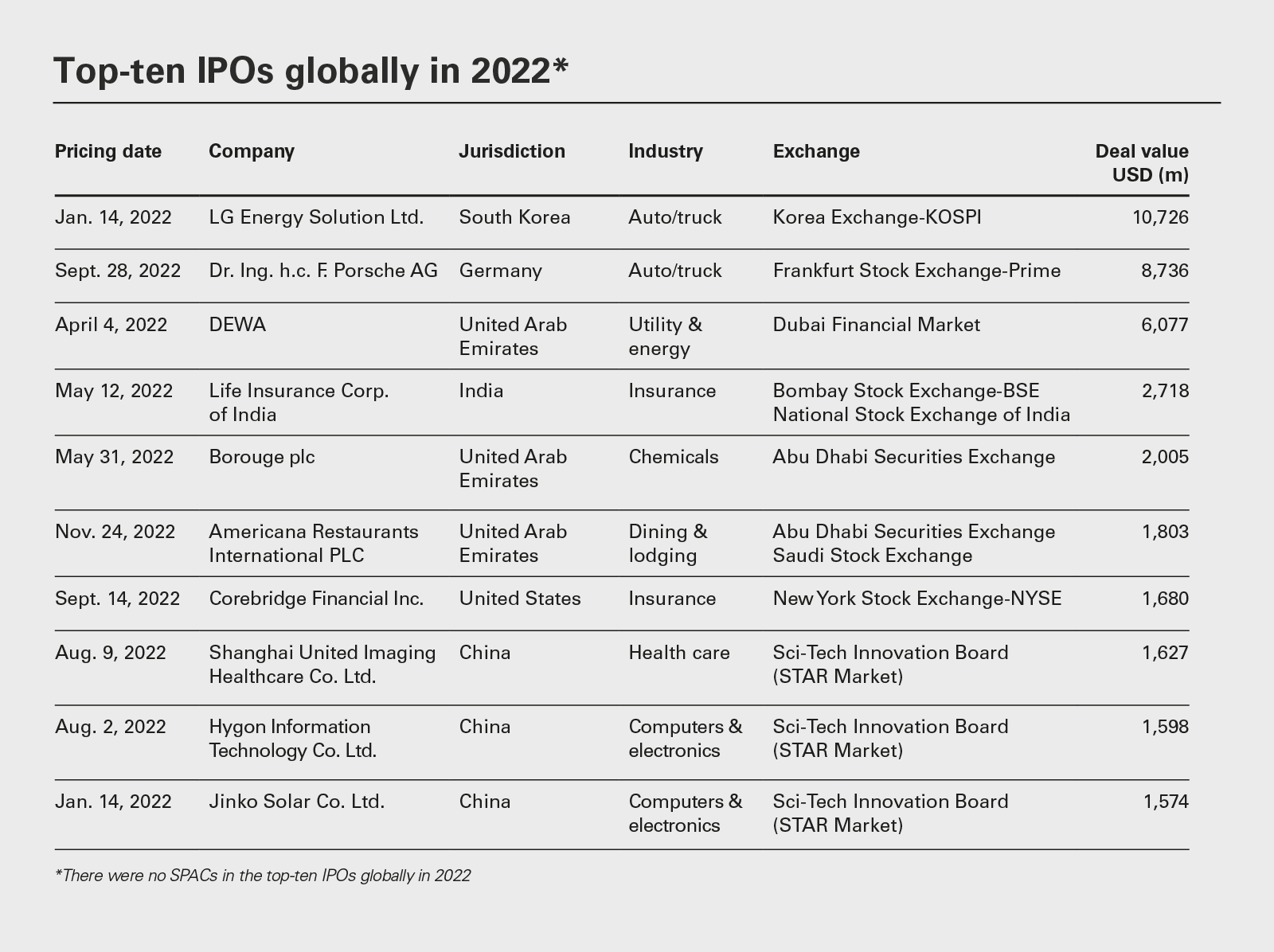

Meanwhile, reflecting APAC's dominance in 2022 is the fact that half of the top 10 largest IPOs worldwide came from the region, including the biggest: South Korean electric vehicle (EV) battery manufacturer LG Energy Solution. The company's US$10.7 billion share offering was also notable because it set a new IPO record in the country and is one of South Korea's most valuable companies after Samsung Electronics and SK Hynix.

Overall, the broader APAC region and Middle East subregion were beacons of strength in what was an otherwise cooler, more risk-averse market.

The LG Energy IPO was very much a carryover from the previous year, when there were several noteworthy listings in the automotive space driven in part by the global shift to electric vehicles. In 2021, the biggest IPO was EV manufacturer Rivian Automotive, which raised US$13.7 billion. In 2022, the second biggest offering after LG Energy was Volkswagen's spin-off carmaker Porsche in a US$8.7 billion share sale. On the face of it, the IPO may seem like a pure luxury automotive play, but Porsche will use the proceeds to fund its transition to electric vehicles.

APAC showed impressive strength and should continue to support activity through 2023 as it sets the pace of global economic growth. All eyes continue to be focused on interest rates and how much further there is to go to tame inflation.

Even in a less stable equity environment, deals can still be executed if they have fundamentally strong narratives, which Porsche's sustainability angle delivered. The demand for EVs and the batteries that power them is being driven by environmental concerns, technological advancements, government policies and changing consumer preferences. Battery manufacturers are investing heavily in developing higher energy density, a longer lifespan and faster charging times. These advancements will make electric cars more practical and affordable for consumers, further fueling demand.

Governments around the world are also offering incentives to promote the adoption of EVs and major automakers are shifting their production focus in this direction, ensuring that this is no passing fad.

There were also sustainability hallmarks in the third-largest IPO of 2022. Dubai's state water and power utility, DEWA, launched on the Dubai Financial Market in a US$6.1 billion sale, the first ever government entity in Dubai to go public. The company seeks to explore the use of new and innovative storage technologies in renewable energy and extend its district cooling services to Saudi Arabia, Qatar and other regional markets.

Dubai is racing to become one of the planet's most sustainable cities, reflecting the recognition by governments in the region that they must adapt to changing times after bringing in vast revenues from the boom in demand for fossil fuels in past decades. The UAE capital is also growing fast, supporting demand for essential water and electricity. It is expected that the city's population will almost double, from approximately 3.5 million people today to 5.8 million by 2040.

These table-topping IPOs have presented mixed results for investors. For example, LG Energy's share price climbed more than 20 percent between its market debut in late January 2022 and March 2023, while Porsche's stock was up by nearly 40 percent in the less than five months since it began trading. DEWA, however, was down by more than 8 percent through March 2023 since it hit the Dubai Financial Market at the beginning of July 2022.

On a six-month post-IPO basis, deals have been hit-and-miss, with an almost even split between those that traded up from their listing price and those that slipped lower. For example, 50 percent of floats (excluding SPACs) saw their price rise over this timeframe, 1 percent were flat and 49 percent came in below par. This was slightly worse than 2021, when 52 percent were up, 1 percent were flat and 47 percent were down. This makes for a surprisingly strong comparison given the weaker equity environment throughout much of 2022.

However, it is worth noting that more than a quarter of IPOs (28 percent) were down between 11 percent and 50 percent in 2022, versus the 27 percent that fell to this degree a year prior. This is the highest proportion of companies that fit this lagging group going back to 2018.

In Q4 2018, public equity markets softened as trade tensions between the US and China were dominating headlines. At the time, there were rising concerns over decelerating global economic growth after a ten-year expansionary phase in the wake of the global financial crisis. The Fed raised interest rates four times that year. In many ways, 2022 and to date in 2023 echoed that similarly choppy period.

Every sector last year saw a fall in IPO activity in both value and volume. Technology led the charge on both measures, with 335 deals (excluding SPACs) worth a combined US$39.5 billion, representing declines of 47 percent and 75 percent year-on-year respectively. As was the case across the board, on average, these were smaller IPOs due to a reduced appetite among investors for new assets and tech-related offerings in particular.

US companies were also notably absent from tech-related proceedings following a full slate in 2021. Chinese computer components manufacturer Hygon Information Technology was the largest tech IPO of 2022 with its US$1.6 billion float.

This reflects the pronounced shift in sentiment witnessed last year. In the second half of 2020 and through 2021, the technology sector was driven by the mass of liquidity washing through markets that were in search of growth assets at any cost amid rock-bottom yields. The pandemic cemented the idea that technology was the answer in a socially distanced, digital world. Of course, technology continues to play a fundamental and growing role in society, with money flowing into pre-profit growth companies on the back of the loosest possible monetary conditions. By 2022, it became clear that surging inflation would need to be contained and the shift in central bank policy that followed resulted in a decline in these valuations.

The automotive industry, meanwhile, had a bigger relative impact on deal value in 2022. Year-on-year, it had a consistent performance, with a drop of only 2 percent to US$23.3 billion (excluding SPACs), putting the sector in second place behind tech. This was made possible by the stock offerings of LG Energy and Porsche—combined, they contributed more than 83 percent of the total automotive IPO value for the year. By contrast, there were only 28 automotive stock market launches globally, an annual fall of 46 percent, putting the sector in the fifteenth position by volume.

The third-highest sector by value and number two by volume (excluding SPACs) was health care. A total of US$15.2 billion was raised by companies in the industry across 150 offerings, representing large year-on-year downturns of 75 percent and 58 percent respectively. Big deals were thin on the ground, with just one health care listing appearing in the global top 25 IPOs of the year in 2022— Shanghai United Imaging Healthcare, worth just US$1.6 billion.

If there was one area that exemplified last year's change of heart regarding the prospects for initial listings of early stage companies, it was SPACs. No SPAC IPO raised more than US$1 billion in 2022, the largest being a US$750 million offering by Screaming Eagle Acquisition Corp. After an incredibly strong year in 2021, in which a record US$172.5 billion was raised globally, this total fell by 90 percent year-on-year to just US$16.8 billion. Global volume also fell 76 percent during the same period to 162 listings.

Last year confirmed that SPACs are particularly sensitive to a downturn in market conditions. One reason for this is the lag between de-SPAC announcements and deals closing. Particularly, in today's higher rate environment, SPAC investors earn a yield on their public shares, and if market valuations decrease between the announcement of a de-SPAC and the closing, there is greater incentive to redeem their cash with a return rather than stay on board and watch the value of the company adjust to fit depressed market conditions.

Another challenge has been the move by the US Securities and Exchange Commission (SEC) to impose additional regulations and potential liability on various SPAC market participants, including certain institutions that provide financial advice and other services in connection with a de-SPAC transaction (see "IPO hopefuls digest forthcoming regulatory changes"). This led many investment banks to decline to participate in these deals.

Despite these challenges, SPACs are likely to remain a meaningful alternative for companies seeking a route to public markets that may not be available through a traditional IPO. Once there is greater clarity from the SEC, banks could be more willing to support these transactions and investor appetite for these deals could potentially improve in line with a more supportive equity market.

It would be easy to characterize 2022 as a bad year for IPOs. US issuance slowed dramatically amid the Fed's aggressive tightening and Europe was understandably stricken by the specter of war. But APAC showed impressive strength and should continue to support activity through 2023 as it sets the pace of global economic growth. All eyes continue to be focused on interest rates and how much further there is to go to tame inflation.

Promisingly, several key indices ran up in Q4 of last year, bringing equity prices back to levels seen in mid-2022. This year started on a relatively optimistic note, suggesting that 2023 could deliver another solid IPO performance.

Recently, however, attention has shifted to the turmoil in the banking sector. Following the collapse of Silicon Valley Bank and troubles at mid-sized lender First Republic Bank, the Federal Open Market Committee said, on March 22, 2023, that the US banking system is "sound and resilient."

Simultaneously, in Europe, UBS agreed to a deal to rescue Credit Suisse, Switzerland's oldest bank.

It is not clear how much, if any, contagion there may be from these events. Certainly, these developments have dampened sentiment and, at the very least, will make investors more cautious about allocating capital to IPOs as they wait to see how the situation unfolds.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP

View full image: Global IPOS by offering and market size (excl. SPACs) (PDF)

View full image: Global IPOS by offering and market size (excl. SPACs) (PDF)

View full image: Top-ten IPOs globally in 2022 (PDF)

View full image: Top-ten IPOs globally in 2022 (PDF)