Taiwanese businesses and investors must weigh foreign direct investment considerations

While most FDI regimes encourage foreign investment, the growing number and greater sophistication of regimes can add to transaction uncertainty.

After withstanding the impact of COVID-19 in 2020, 2021 witnessed a sharp rebound globally across capital markets, private equity, finance and other corporate deal-making. The rebound was expected—the combination of the pressure to deploy significant amounts of raised capital and pandemic-driven asset value distortion presented attractive value propositions for many stakeholders. The magnitude of the rebound, however, was unexpected.

The exuberance carried over into early 2021, but when the Ukraine conflict started in February 2022, it exacerbated ongoing geopolitical fractures and economic decoupling, quickly dampening any optimism for sustained deal-making in 2022. The security of energy, food and other commodities became a key risk theme in 2022.

However, volatility is not necessarily a bad thing. With careful planning (many steps ahead) on how to manage the current volatility, we believe investors and businesses in Taiwan will be in a prime position to capitalize on Taiwan's critical role in global trade once normalcy resumes.

Following our 2022 Taiwan webinar series in September and October, we hope this year's report for Taiwanese businesses and investors provides helpful guidance during a volatile time.

We begin with an overview of the current state of affairs related to global regulatory developments in foreign direct investment (FDI). Various black swan events in 2022 drove, and will continue to drive, geopolitical fractures and economic decoupling globally. In addition, global FDI regulatory regimes have rapidly matured to the point where it is critical for Taiwanese investors and businesses to ensure maximum deal certainty by considering FDI analysis as probably the most important task they need to manage before embarking on any cross-border investments relating or peripheral to critical infrastructure and technologies.

We then summarize recent European Union court judgments that established what is deemed anti-competitive behavior in the context of exclusivity rebates. Taiwanese businesses trading in dominant positions in the EU should carefully weigh the impact of these judgments on trading practices.

Next, we provide our thoughts on the trends and headwinds in M&A and corporate transactions relating primarily to Taiwan and the rest of the Asia-Pacific region. We hope the thematic investment developments, changing jurisdictional focus and the excess liquidity data points flagged in the overview will help guide investors and businesses in their quest for low-beta high-alpha investments.

To underscore emerging thematic investment developments and value discovery in Taiwan and globally, this year we introduced a webinar session focusing on ESG. This is a rapidly evolving theme which, given its growing importance in the capital markets, financing and corporate transactions, is driving increasing regulatory regimes globally. Because of differing ESG compliance standards globally, investors and Taiwanese businesses should carefully consider the complexities in structuring a compliant and bankable ESG-focused transaction.

This year, we also introduced a webinar session focusing on fund formation. In our report, we summarize the concept of a continuation fund, a fund product that may be of interest amid volatility, and which has affected fund exits.

And finally, we summarize the state of affairs in global sanctions. The CHIPS and Science Act, which came into force in August 2022, is particularly relevant to Taiwan semiconductor companies. Given Taiwan's dominant position in the global semiconductor industry, this legislation has significant impact on the industry's supply chain and economics.

We look forward to discussing these and other issues with you.

While most FDI regimes encourage foreign investment, the growing number and greater sophistication of regimes can add to transaction uncertainty.

Key 2022 judgments apply a five-factor analysis outlined by the EU's highest court in 2017.

How Taiwanese and other firms have weathered 2021’s perfect storm and its aftermath.

As stakeholders embrace ESG considerations, risks, opportunities and challenges to integration remain

These funds create opportunities, but can present legal and business challenges.

Understanding the recent ban of certain chips to China and the new semiconductor-related export controls

These funds create opportunities, but can present legal and business challenges

The private equity (PE) secondaries market is witnessing continued growth, both globally and especially in recent years, within the Asia-Pacific region.

Managers are increasingly seeking ways to actively manage their trophy assets (and to some extent, their distressed assets) and to proactively generate liquidity for their investors. The secondaries market has become more attractive in the wake of recent events—including the pandemic, geopolitical tensions, volatile public markets and the underperformance of certain sectors—all of which are creating a challenging environment for exits and pushing managers to find alternative solutions to provide liquidity.

General partner-led restructurings and, in particular, continuation funds, have been viewed as one of the potential means to bridge the gap in providing liquidity to managers and their investors. Continuation funds are typically set up and managed by the same manager selling the asset(s). Instead of selling the asset to a third party, the manager of an existing fund sets up a new vehicle and rolls the asset from the existing vehicle into the new one.

Given that the manager sits on both the sell- and buy-sides, continuation funds have been controversial due to perceived conflicts of interest. This article offers some of the key points for investors—on both the buy and sell sides—to consider when participating in a continuation fund transaction.

Historically, continuation funds have been used in situations where a manager or sponsor is unable to sell a problematic or distressed asset at the end of the fund’s life. More recently, continuation funds have been designed to achieve two outcomes: to enable managers to retain their well-performing assets as their existing funds near the end of their terms, allowing for later exits at more optimal times, and to allow existing investors seeking liquidity to cash out of their investments. In addition, it is common for new investors—often market participants in the fund secondaries industry—to be brought in as investors in the continuation fund.

The sponsor will typically also commit to the continuation fund—often using the carried interest earned from the existing fund that crystalized upon the rollover—to ensure better alignment with its investors.

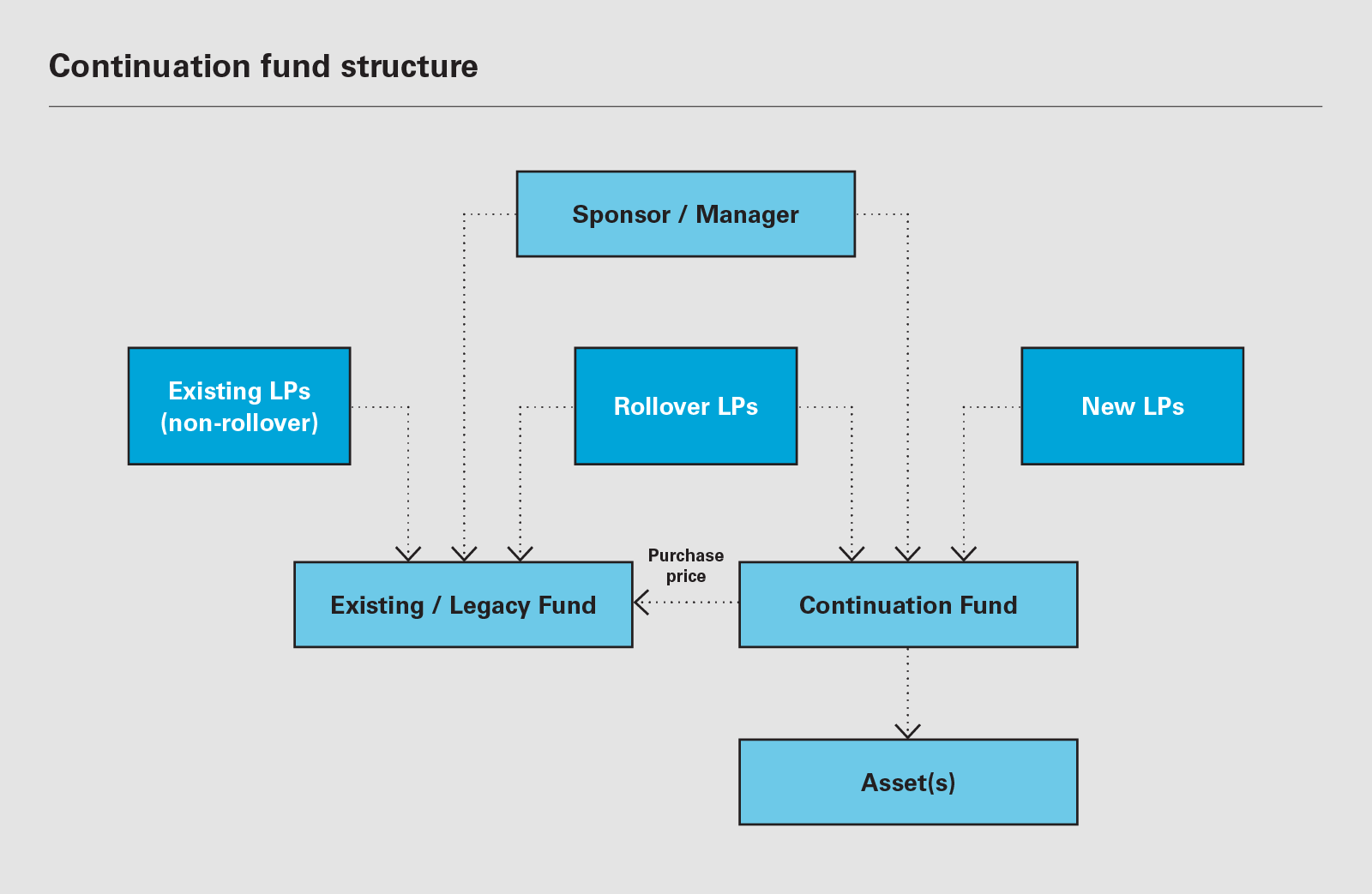

A typical continuation fund structure is set out below:

Investors in the existing funds who choose not to cash out on the sale of the portfolio company or asset have the option to roll over their interest by taking an equity stake in the newly-established continuation fund for the specific purpose of purchasing the portfolio company or asset.

The same sponsor or manager will often continue to manage the assets of the continuation fund. Additional capital commitments in the continuation fund may be earmarked for follow-on investments.

In a continuation fund restructuring, investors who choose to roll over their interest will often subscribe for a new interest in the continuation fund as part of that rollover. These investors have the advantage of a longer term hold on an investment, which can be beneficial in terms of retaining significant upside potential. They also may be given the ability to retain their existing terms of investment or otherwise renegotiate new terms. As part of subscribing for a new interest in the continuation fund, an investor may also be asked by the sponsor to subscribe for a “stapled interest” in a newly-raised primary fund established by the sponsor. On the other hand, an investor who elects to cash out has the benefit of receiving liquidity on its investment—when no such liquidity might otherwise exist—locking in unrealized gains and gaining the ability to rebalance and de-risk their portfolios and re-deploy their capital elsewhere.

Sufficient time and transparency will be key factors for investors who are deciding whether to cash out or roll over their fund interests. On the buy-side, secondaries opportunities are attractive to investors as they provide them with exposure to mature, pre-identified assets or portfolios with holding periods that are shorter, relative to the holding period of a primary fund. Key considerations for investors on the buy-side typically focus on due diligence on the underlying asset or portfolio, valuations, any competitive bidding processes and the negotiation of the terms of the proposed continuation fund. In situations where a consortium of investors will be involved, there may be one or more lead investors who take a more active role in the bidding process and negotiate with the manager, while the other investors take a more passive role.

Finally, as previously noted, the manager will continue to manage the asset and to receive fee and income from the asset. Management fees in continuation vehicles are often charged out at a lower rate than management fees payable on a primary fund, and carried interest is often tailored for stronger alignment. Managers will frequently push for a super carry—sometimes a higher carry percentage than the one used in the existing fund, for example, 25 percent in the continuation fund versus 20 percent in the existing fund, or a tiered carry where the carried interest percentages ratchet up to 25-30 percent as the continuation fund hits its return targets.

While there are advantages to tapping into the growing secondaries market, continuation funds often present significant legal and commercial issues that must be considered. Conflicts of interest are one area that often require close scrutiny.

The conflicts primarily relate to the fact that the manager sits on both the sell-side (i.e., the existing fund) and the buy-side (i.e., the continuation fund). This often leads to a perceived conflict regarding the pricing of the underlying assets, and the manager’s motivation in selling the asset to a related vehicle. There are particular concerns regarding the economic terms that the manager may receive from investors in that vehicle (i.e., often higher carry and a continuation of the fee income in the form of management fee).

To address this potential perceived conflict, it is not unusual for a manager to bring the transaction to the existing fund’s investor advisory committee or board for approval. While this often helps mitigate any potential conflict on the manager’s part, in some situations it may not be adequate as the investors (or their representatives who sit on the fund’s investor advisory committee or board) may themselves be perceived to have a potential conflict if they also sit on both sides of the transaction (due to their investments in both the existing fund the new continuation fund).

A thorough review and knowledge of the fund documents is often important so that both the manager and the investors understand their rights and obligations in any proposed continuation fund transaction. Various mechanisms can be put in place to potentially regulate conflicts—including a requirement for investor consent or an independent valuation of an asset, and recusal requirements at the investor advisory committee or board level where a potential conflict of interest exists. These issues may need to be considered upfront; in particular, some managers are beginning to hardwire the express ability to create continuation funds as part of the main fund establishment process, specifying the requirements (often investor advisory committee or board consent or a form of price validation) needed for the main fund to transfer an asset to a continuation fund.

Regulators are also starting to pay attention to conflicts of interest in these transactions. The SEC, for instance, has recently proposed rules that would require the issuance of a third-party fairness opinion for any adviser-led secondary transaction, in addition to a summary of any material business relationships the adviser or any of its related persons has, or has had, within the past two years, with the independent opinion provider.

GP-led restructurings come in many forms. A successful GP-led restructuring is a win for all parties. Alignment of interest, transparency and adequacy of information, actively managed conflicts, continuous dialogue and a well-planned timetable are critical to achieving this result.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: Continuation fund structure (PDF)

View full image: Continuation fund structure (PDF)