Taiwanese businesses and investors must weigh foreign direct investment considerations

While most FDI regimes encourage foreign investment, the growing number and greater sophistication of regimes can add to transaction uncertainty.

After withstanding the impact of COVID-19 in 2020, 2021 witnessed a sharp rebound globally across capital markets, private equity, finance and other corporate deal-making. The rebound was expected—the combination of the pressure to deploy significant amounts of raised capital and pandemic-driven asset value distortion presented attractive value propositions for many stakeholders. The magnitude of the rebound, however, was unexpected.

The exuberance carried over into early 2021, but when the Ukraine conflict started in February 2022, it exacerbated ongoing geopolitical fractures and economic decoupling, quickly dampening any optimism for sustained deal-making in 2022. The security of energy, food and other commodities became a key risk theme in 2022.

However, volatility is not necessarily a bad thing. With careful planning (many steps ahead) on how to manage the current volatility, we believe investors and businesses in Taiwan will be in a prime position to capitalize on Taiwan's critical role in global trade once normalcy resumes.

Following our 2022 Taiwan webinar series in September and October, we hope this year's report for Taiwanese businesses and investors provides helpful guidance during a volatile time.

We begin with an overview of the current state of affairs related to global regulatory developments in foreign direct investment (FDI). Various black swan events in 2022 drove, and will continue to drive, geopolitical fractures and economic decoupling globally. In addition, global FDI regulatory regimes have rapidly matured to the point where it is critical for Taiwanese investors and businesses to ensure maximum deal certainty by considering FDI analysis as probably the most important task they need to manage before embarking on any cross-border investments relating or peripheral to critical infrastructure and technologies.

We then summarize recent European Union court judgments that established what is deemed anti-competitive behavior in the context of exclusivity rebates. Taiwanese businesses trading in dominant positions in the EU should carefully weigh the impact of these judgments on trading practices.

Next, we provide our thoughts on the trends and headwinds in M&A and corporate transactions relating primarily to Taiwan and the rest of the Asia-Pacific region. We hope the thematic investment developments, changing jurisdictional focus and the excess liquidity data points flagged in the overview will help guide investors and businesses in their quest for low-beta high-alpha investments.

To underscore emerging thematic investment developments and value discovery in Taiwan and globally, this year we introduced a webinar session focusing on ESG. This is a rapidly evolving theme which, given its growing importance in the capital markets, financing and corporate transactions, is driving increasing regulatory regimes globally. Because of differing ESG compliance standards globally, investors and Taiwanese businesses should carefully consider the complexities in structuring a compliant and bankable ESG-focused transaction.

This year, we also introduced a webinar session focusing on fund formation. In our report, we summarize the concept of a continuation fund, a fund product that may be of interest amid volatility, and which has affected fund exits.

And finally, we summarize the state of affairs in global sanctions. The CHIPS and Science Act, which came into force in August 2022, is particularly relevant to Taiwan semiconductor companies. Given Taiwan's dominant position in the global semiconductor industry, this legislation has significant impact on the industry's supply chain and economics.

We look forward to discussing these and other issues with you.

While most FDI regimes encourage foreign investment, the growing number and greater sophistication of regimes can add to transaction uncertainty.

Key 2022 judgments apply a five-factor analysis outlined by the EU's highest court in 2017.

How Taiwanese and other firms have weathered 2021’s perfect storm and its aftermath.

As stakeholders embrace ESG considerations, risks, opportunities and challenges to integration remain

These funds create opportunities, but can present legal and business challenges.

Understanding the recent ban of certain chips to China and the new semiconductor-related export controls

As stakeholders embrace ESG considerations, risks, opportunities and challenges to integration remain

ESG, sustainability, climate change adaptation and mitigation, social impact investing and related themes have become ubiquitous concepts that seem to be top of mind for every board director, financier and investor. While there is no universal consensus on the precise meaning of these terms (and there may never be, nor does there necessarily need to be), within business and finance circles they are largely understood to represent a set of environmental, social and corporate governance considerations that can impact a business's strategy and its ability to create value over the long term.1

During the past decade (and particularly in the past two to three years), this understanding has brought about a seismic shift in business practices, reflecting a growing appreciation across sectors and geographies that integrating ESG considerations into corporate decision-making is not only "good for business" or a "nice to have," but rather, it is a strategic imperative.

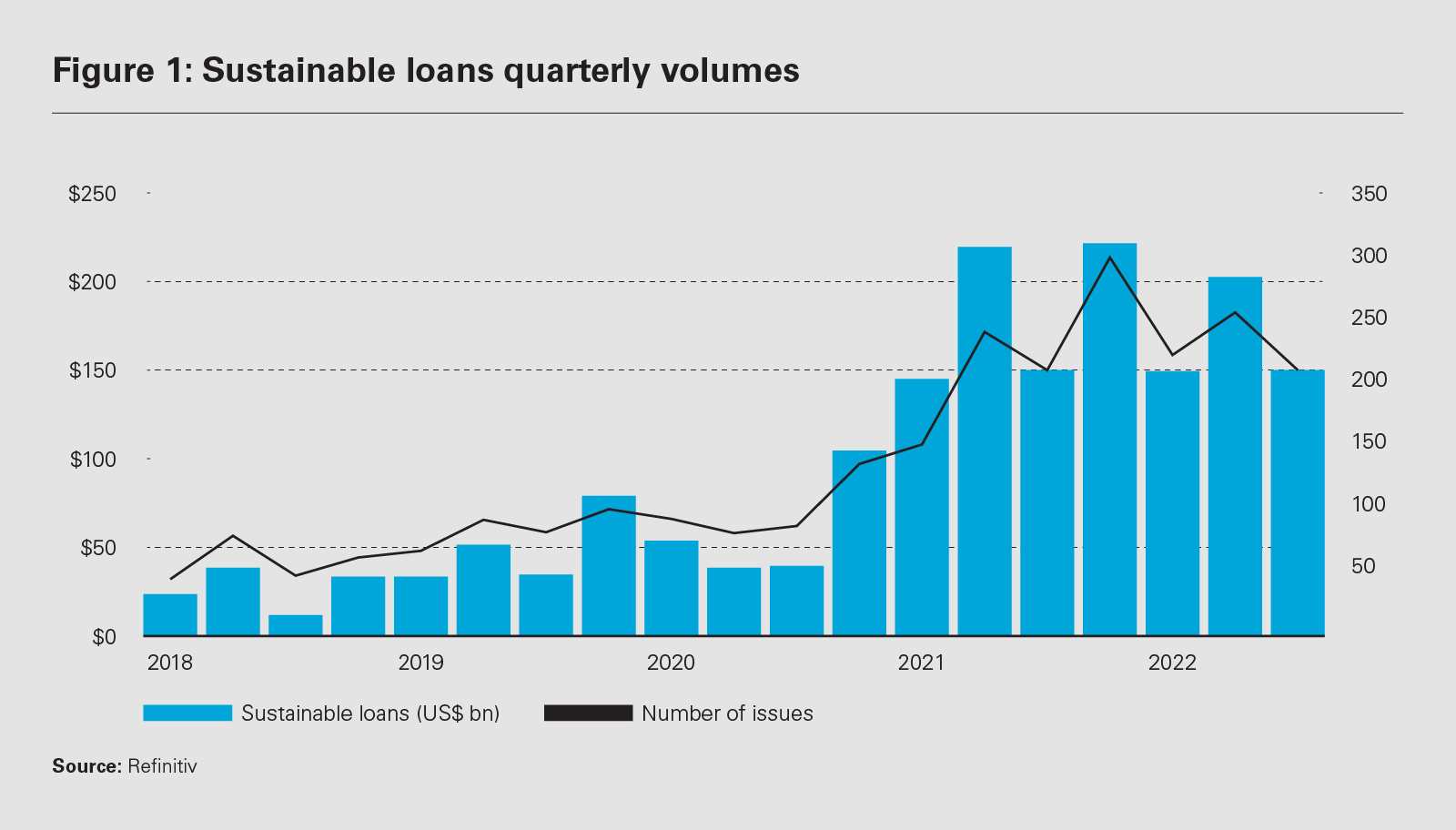

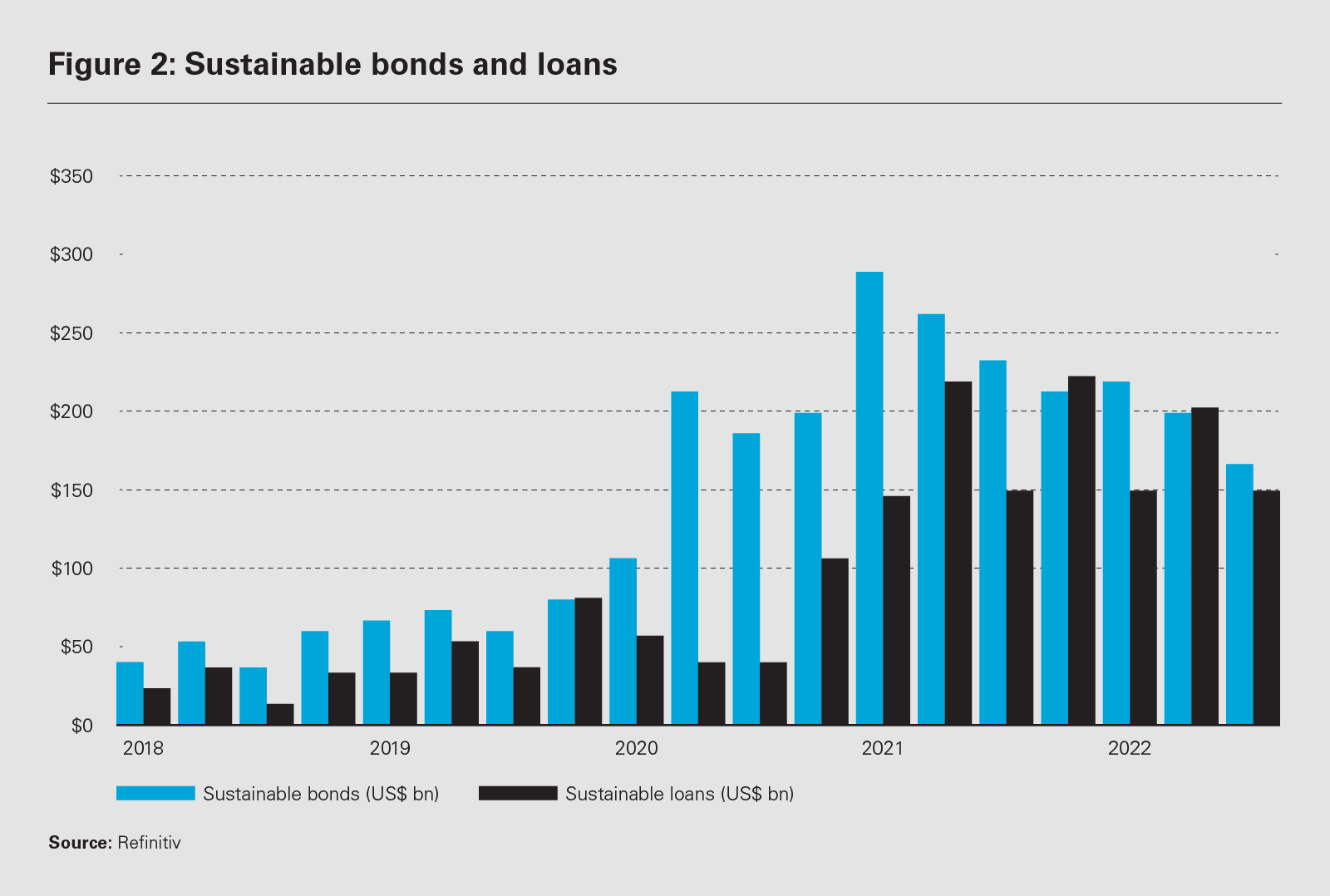

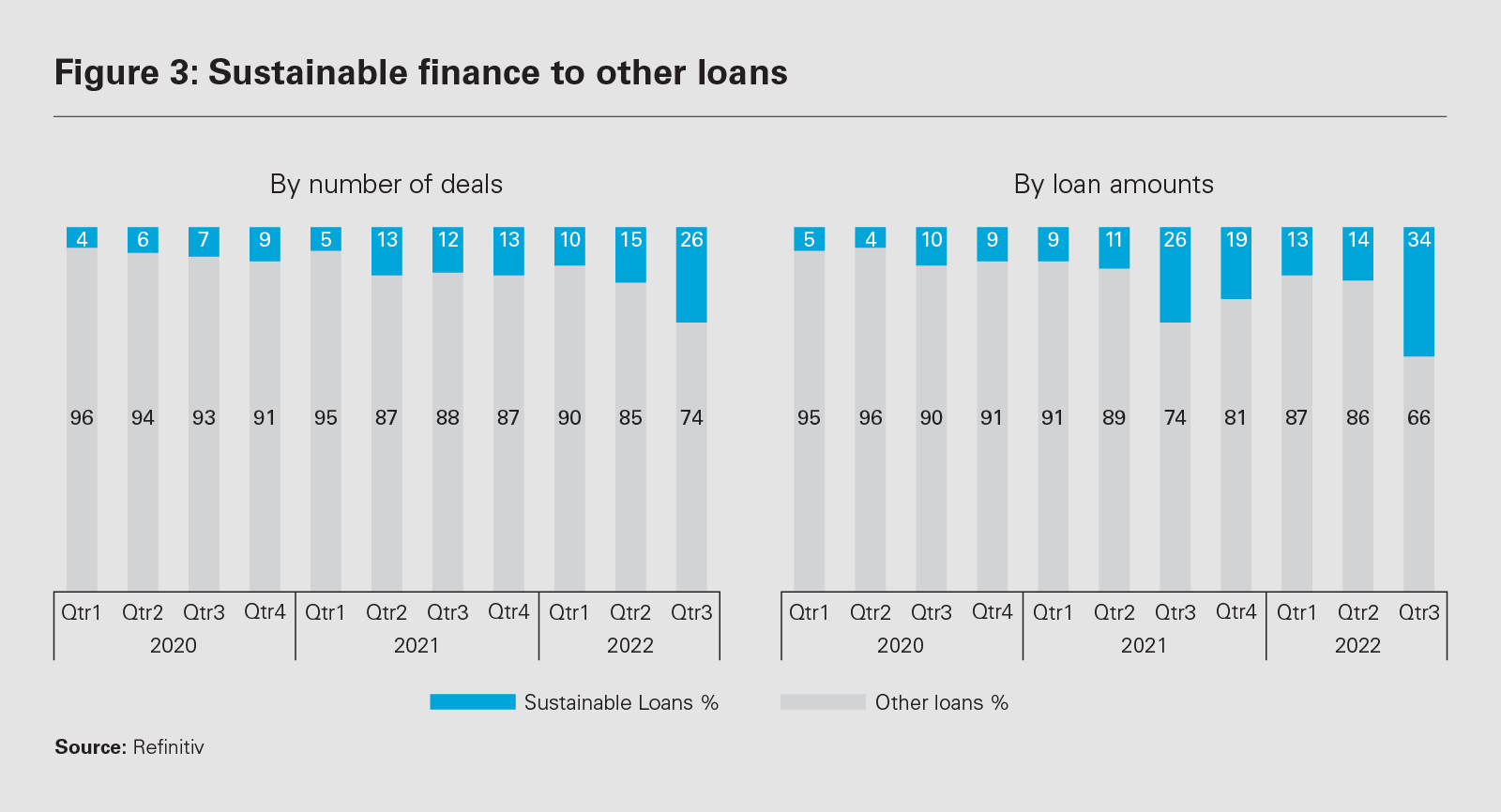

The importance of ESG considerations is apparent in global financial markets. While global market volatility has accounted for drops in deal volumes and values generally in 2022, to-date relative to 2021, green, social, sustainable and sustainability-linked bonds, loans and other financial products continue to represent, year-on-year, ever-larger slices of the overall market in both volume and value (See figures 1-3).

Vanilla bonds and loans are also no longer the only products receiving the ESG treatment. Sustainability-linked derivatives are on the rise, as are green and social securitizations and other more esoteric structured products. In addition, a stream of regulatory and industry-driven initiatives that target financial transactions and institutions are being launched, steadily implemented and scheduled for implementation in the coming years.2

The mainstreaming of sustainable finance asset classes showcases the successful efforts of stakeholders—regulators, government authorities, industry bodies, financial institutions, corporations and, of course, the general public—to enable efficiencies when connecting increasingly ESG-minded investors with investment targets and, ultimately, to boost both the supply of, and demand for, ESG-related financial products. In this context, both cause and effect are seen in the range of developments discussed below.

Governments and economic blocs (against the backdrop of their commitments under the Paris Agreement and agreed more recently at COP26 and COP27) are incentivized to encourage3 ESG integration across all walks of business life. These incentives include voluntary and mandatory disclosure regimes, implemented or planned, such as:

In addition, industry bodies continue to publish best practice standards and guidance for structuring sustainable finance transactions in ways that achieve the level of consensus needed to scale up sustainable finance transactions. These industry bodies include the International Capital Markets Association (ICMA), ASEAN Capital Markets Forum (ACMF), Loan Market Association (LMA), Asia Pacific Loan Market Association (APLMA), Loan Syndications and Trading Association (LSTA) and International Swaps and Derivatives Association (ISDA). The standards and guidance have developed from initially broad categorizations of eligibility—such as under the core tenets of the ICMA Green Bond Principles, ASEAN Green Bond Standards and APLMA Green and Social Loan Principles—to more detailed guidance on industry-specific key performance indicators (KPIs) for sustainability-linked bonds and loans. These include ICMA's updated registry of approximately 300 sector-specific KPIs for SLBs published in June 2022 and the APLMA's publication of its SLL appendix to its standard-form term sheet in September 2022.

Consistent with these trends, banks, PE firms and investment funds are becoming more selective and implementing stricter policies regarding who they lend to, arrange financing for and invest in. This selectivity is often driven by their clients, shareholders, limited partners and investors' ESG investment and eligibility criteria, which may in turn be designed pursuant to industry-level guidance, such as the European Leveraged Finance Association's ESG Exclusion Checklist. Published in January 2022, the checklist is meant to be completed by arranging banks at the time of a new corporate loan or bond syndication and aims to help investors to quickly determine if a corporate borrower is a suitable investment candidate based on the firm's or fund's specific ESG criteria.

Prospective borrowers and issuers recognize that improved ESG credentials can affect their access to, and cost of, capital, particularly in an environment where financiers and investors are chasing a combination of yield and ESG criteria and actively steering clear of certain industries and entities that are viewed as lacking, at the very least, a transition story or, at worst, are viewed as stranded assets.

Market participants are also becoming more cognizant of stakeholder activism and the very real risk of disputes which can lead to consequential legal liability and commercial losses. They recognize that a real or perceived failure to meet ESG expectations may make them vulnerable and they are taking steps to mitigate the risks, for example by aligning their policies, business and financing activities with relevant regulatory and industry standards and guidance.

While global financial markets have proven keen to embrace ESG integration, systemic hurdles to the growth and credibility of sustainable finance remain—and have existed since the first green-labeled bonds were issued in the early 2010s. For example, data measurement and reporting remain a critical consideration for stakeholders. Where the data required to make informed decisions when structuring, monitoring or conducting diligence for transactions is unavailable or lacking in quality, reliability or consistency, it becomes more difficult to assess (i) the ESG credentials of an organization and, accordingly, whether the organization is investable or fundable; (ii) whether a borrower is achieving or failing to achieve sustainability-linked KPIs; or (iii) whether a green bond issuer's green bond issuance framework meets prospective bondholders' investment criteria.

As mentioned in the introduction, the real or perceived lack of sufficient consensus on precisely which use of proceeds, KPIs or general activities are or should be deemed to fulfill the relevant E, S and G parameters remains. Where different groups of stakeholders may have divergent views on whether the relevant borrower, lender or other party has strayed too far from the standards they follow or consider customary, this can expose transaction parties to the risk of greenwashing (and its reputational and monetary consequences).

As sustainable finance products become more widely used funding tools, transaction volumes will increase, as will the range and novelty of real-world use of proceeds, projects and sustainability-linked KPIs that may be used to justify the relevant ESG label. Against this backdrop, standardization arguably becomes both more important in principle and more difficult to achieve in practice, despite the best efforts of regulators and industry bodies. This potentially rings particularly true for multinational corporations, financial institutions and other organizations with global operations.

The drive for standardization is further complicated by practical and, in some cases, region-specific socioeconomic and cultural nuances across jurisdictions. For instance, companies in economies and industries that have historically relied on coal (including several major APAC economies) and where, accordingly, their local supply chains may not be as clean from an environmental (or broader ESG) perspective, may find it inherently more challenging to market a labeled green bond issuance to, or position themselves as attractive recipients of green or sustainability-linked loans for, investors and lenders who are under more scrutiny than ever to carefully select where they deploy their capital (transition finance, a relatively nascent subset of sustainable finance, may be useful here, but that is beyond the scope of this article).

It is also worth noting that, as the focus shifts from the "E" to the "S" part of ESG (as social financing transactions increase), what may be considered "S" in one part of the world may not pass muster in another, as the subjectivity of regional cultural viewpoints may come into play more in the context of identifying and agreeing socially beneficial use of proceeds or KPIs. Moreover, social metrics are arguably harder to measure, unlike environmental or climate-related metrics which are, on the face of it, more empirical and objective. A one-size-fits-all approach to sustainable finance (and broader ESG) standards may not, therefore, be where the market is heading.

Nonetheless, the trend remains clear and the pace of growth of the sustainable finance market does not look like it will slow any time soon. In this fast-moving environment (juxtaposed by the very real socioeconomic pressures to provide financial support to markets and industries that have been hit by, and continue to suffer from, the economic fallout of the COVID-19 pandemic, the war in Ukraine and consequent energy security concerns), it will be critical for financial institutions and prospective issuers and borrowers to stay up-to-speed with the component parts of the evolving sustainable finance ecosystem (in each case in the jurisdictions in which they operate) in order to be able to seize financing opportunities and build resilience to ESG-related risks.5

1 White & Case connects clients to help build a more sustainable world

2 The Global ESG Regulatory Framework toughens up

3 Environmental, social and governance factors enter the mainstream

4 SEC Proposes Amendments to Rules to Regulate ESG Disclosures for Investment Advisers & Investment Companies

5 ESG: A sustainable approach in turbulent times

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: Figure 1: Sustainable loans quarterly volumes (PDF)

View full image: Figure 1: Sustainable loans quarterly volumes (PDF)

View full image: Figure 2: Sustainable bonds and loans (PDF)

View full image: Figure 2: Sustainable bonds and loans (PDF)

View full image: Figure 3: Sustainable finance to other loans (PDF)

View full image: Figure 3: Sustainable finance to other loans (PDF)