US M&A hits record highs

The US enjoyed record levels of M&A activity in H1 2021, as dealmakers made up for lost time caused by pandemic-related disruptions

US M&A surged to record levels in the face of pandemic-related challenges and potentially dramatic regulatory shifts

We are just heading into August, but it is already safe to say that 2021 is a historic year for US M&A. Deal value rose to a new high of US$1.27 trillion in H1 2021. This was a 324 percent increase compared to H1 2020—and was virtually equivalent to the total value recorded in all of 2020.

This torrent of deals was the result of a perfect storm of activity on the part of strategic, PE and SPAC dealmakers. The pandemic drove many corporates to offload non-core divisions and acquire digital capabilities. Corporates that thrived during the pandemic used M&A to consolidate gains. PE firms strove to deploy their massive troves of dry powder. And SPACs searched for opportunities to invest the record levels of funds they raised.

The election of Joe Biden as President significantly reduced political uncertainty that may have dampened activity in 2020 and this spurred dealmaking in 2021. However, the administration's policies could also complicate dealmaking.

The Biden Administration is taking vigorous steps to reshape antitrust policies and practices in the US. In July, the President issued an Executive Order to promote competition and lower prices throughout the economy through increased antitrust enforcement. These efforts are likely to intensify during the run-up to the US midterm elections in November 2022. The effects were already visible in the recent decision by Aon and Willis Towers Watson to call off their merger, which they first announced in March 2020. The deal would have created the world's largest insurance broker, but the Department of Justice opposed the deal on the grounds that it would eliminate competition, reduce innovation and lead to higher prices.

CFIUS has shown that it will mostly continue with the more aggressive approach to evaluating deals for national security concerns that was established by the previous administration. And with the appointment of Gary Gensler as Chair of the Securities and Exchange Commission, the administration signaled it will take a more aggressive approach to securities law enforcement.

There are a number of other looming risks as well. The possibility of rising inflation and the end of government support measures related to the pandemic could shock the market. And dealmakers are concerned about potentially frothy valuations.

But perhaps the greatest variable remains the uncertain trajectory of the pandemic. Though the US was on a course of increasing optimism as vaccines were rolled out, recent concerns about the Delta variant of COVID-19 have raised questions—and exacerbated political divisions—about how quickly economies should open up.

Despite these challenges, the outlook for dealmaking remains very positive. US GDP forecasts are upbeat, stock markets are at historic highs, and interests remain low. Moreover, the Biden Administration's economic stimulus efforts and ambitious plans for energy transition and infrastructure development will inject large sums of capital into the economy. We expect US M&A to remain very active in the second half of 2021.

The US enjoyed record levels of M&A activity in H1 2021, as dealmakers made up for lost time caused by pandemic-related disruptions

US private equity has rallied following pandemic lockdowns, thanks to adaptations to remote deal processes and record dry powder

TMT M&A tops the sector charts again

After a year of volatility, the oil & gas industry has stabilized and M&A activity has resumed

Technology M&A activity is thriving in 2021 as dealmakers continue to turn to the sector in search of assets with high-quality earnings and growth prospects

The value of healthcare M&A in H1 surpassed pre-pandemic levels

Deals in the consumer and retail sector show signs of recovery as consumer spending

rallies post-pandemic

The power and renewables industry is positioned for a sustained period of strong deal

activity as the US focuses on hitting net zero carbon emissions by 2050

M&A value among real estate firms quadrupled year-on-year in H1, after a tough 2020

After a pause, investment in infrastructure has ballooned, even before the Biden administration's US$1 trillion-plus plan is passed

After campaigning for the presidency on a platform that included more aggressive antitrust enforcement, Joe Biden has taken early steps to honor those pledges

President Joe Biden's approach to the national security risks posed by foreignbacked M&A may differ in style from his predecessor, but not in substance

Even as economies pick up, dealmakers have maintained focus on managing the risk of broken deals

New Securities and Exchange Commission Chair Gary Gensler has put scrutiny of

SPACs and private funds at the top of his agenda

In the first half of 2021, Delaware courts issued several decisions affecting M&A dealmaking

After a turbulent 18 months which saw M&A crash before an impressive return to form, H2 2021 is set for continued strong deal activity, as well as new challenges

TMT M&A tops the sector charts again

Stay current on global M&A activity

Explore the data

The tech industry has seen strong growth over the last 12 months, as businesses, employees, consumers and students have relied on technology to continue trading, working, shopping and studying.

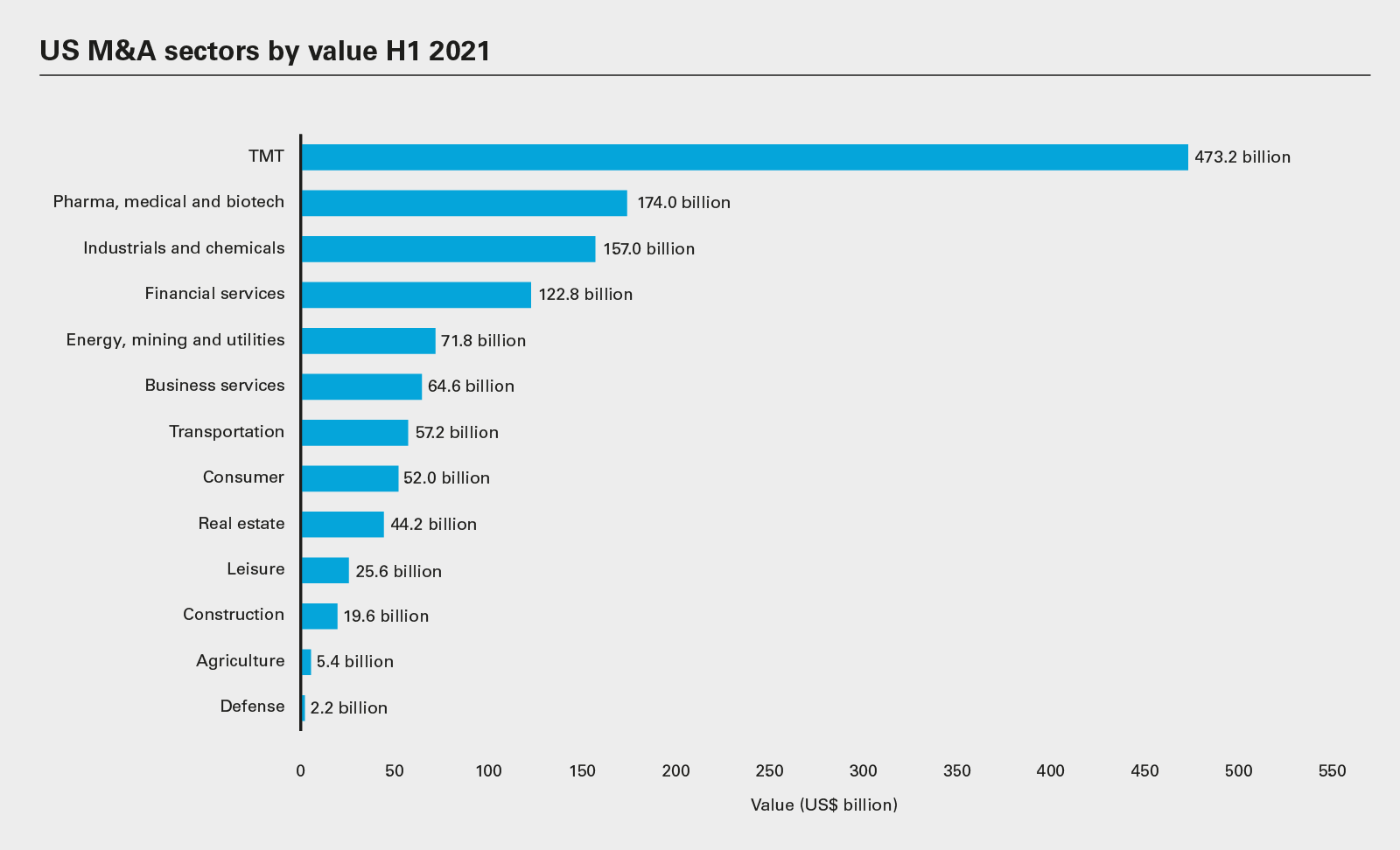

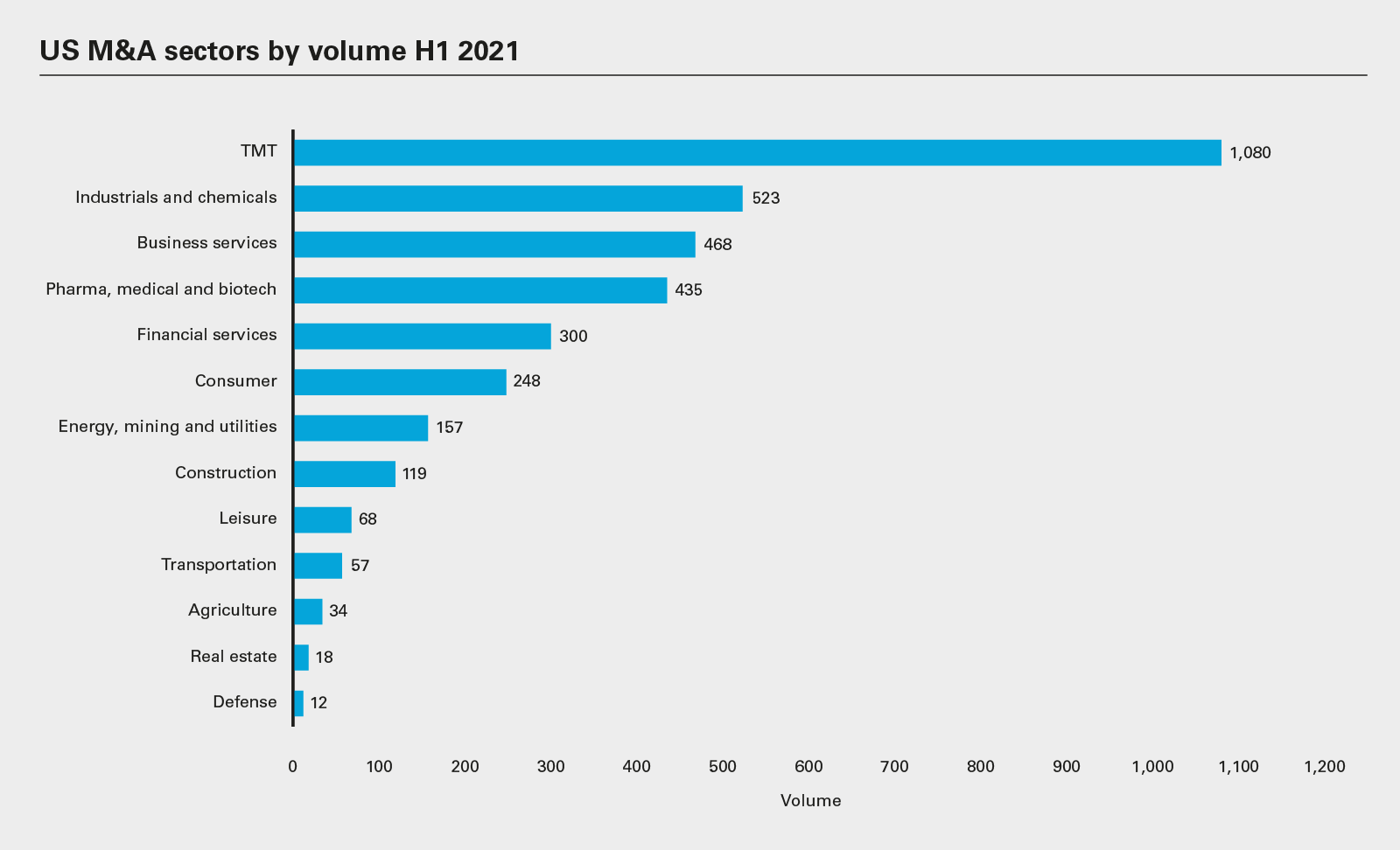

The TMT sector led US M&A activity through H1 2021 and was the largest by both deal value and deal volume, carrying momentum from 2020 into the first six months of this year.

The value of TMT M&A in the US totaled US$473.2 billion in the first half of the year, up more than sixfold on H1 2020 levels. Volume was up 62 percent to 1,080 transactions.

The tech industry has seen strong growth over the last 12 months, as businesses, employees, consumers and students have relied on technology to continue trading, working, shopping and studying.

PMB ranked as the next largest sector by deal value but was some distance behind TMT, with value totaling US$174 billion. The sector was the fourth largest by volume, recording 435 deals, a 24 percent rise on H1 2020 levels.

Industrials and chemicals was the second largest sector by deal count, with 523 deals recorded in H1 2021—a 29 percent rise on the same period in 2020. Value also rose, more than doubling from US$59.9 billion in H1 2020 to US$157 billion in the same period this year—making it the third biggest sector by value.

Business services was the third largest by deal volume, with the number of transactions in the sector increasing from 383 in H1 2020 to 468 over the first six months of this year. Business services was only the sixth largest sector by deal value, even as value climbed significantly from US$18.2 billion in H1 2020 to US$64.6 billion.

The leisure and consumer sectors, which were both directly impacted by lockdowns, showed encouraging signs of recovery through the course of H1 2021 as the US economy reopened and vaccine roll-outs accelerated. Leisure deal value has improved from just US$5.3 billion in H1 2020 to US$25.6 billion—and deal volume has gone up from 37 to 68. In the consumer space, deal volumes have improved from 192 transactions to 248, while value more than doubled from US$20.2 billion over the first six months of last year to US$52 billion in H1 2021.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View the full image: US M&A sectors by value H1 2021 (PDF)

View the full image: US M&A sectors by value H1 2021 (PDF)

View full image: US M&A sectors by volume H1 2021 (PDF)

View full image: US M&A sectors by volume H1 2021 (PDF)