Strong foundations: Asian infrastructure is open for business

Despite the pandemic, optimism for Asia-Pacific infrastructure projects is increasing with investors looking at a plurality of regions and sectors

While some projects have been delayed, the sector has proven itself remarkably resilient. As has occurred with previous crises, there is now a growing expectation that infrastructure financing volumes will increase above and beyond historical values as the effects of the pandemic subside. And private investment is vital, considering the region’s infrastructure needs— demanding US$1.7 trillion annually in financing, according to the Asian Development Bank (ADB).

With this in mind, White & Case, in association with Inframation, set out to investigate the prospects for infrastructure investment across the APAC region. This new survey builds on our 2019 report Cutting Through the Noise.

The research reveals that, Black Swan events aside, investors remain extremely bullish over the long-term fundamentals of the Asia-Pacific infrastructure sector, with four clear trends emerging:

New frontiers

Investors see APAC as a land of opportunity. More than half of respondents cited ‘wealth of opportunity’ as the greatest benefit to investing in the region.

Growth plans

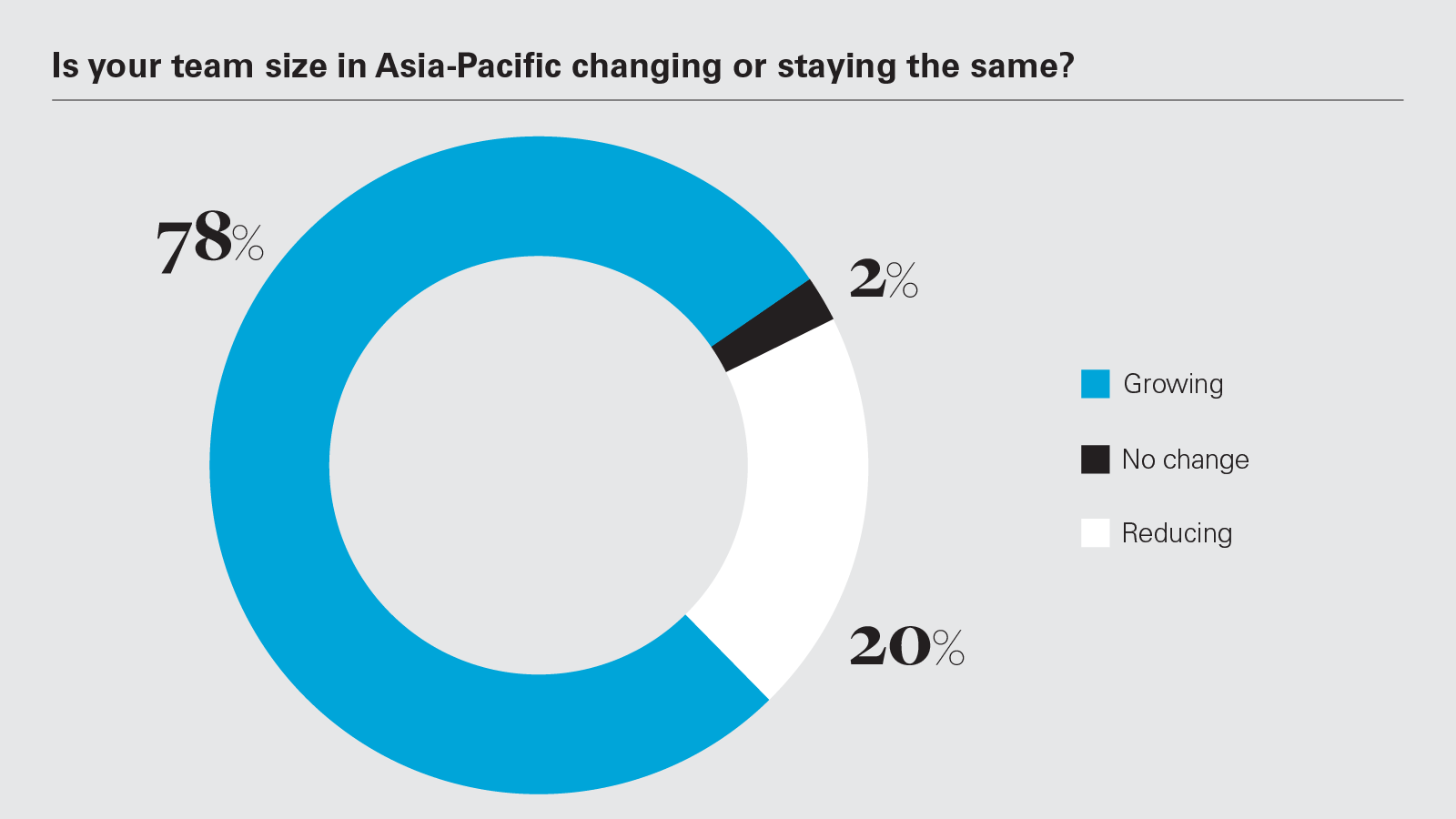

Despite concerns regarding aspects such as construction and delivery risk and political scrutiny, the outlook from respondents is overwhelmingly positive—78 per cent of firms intend to grow their teams in the region in 2021.

Social surges

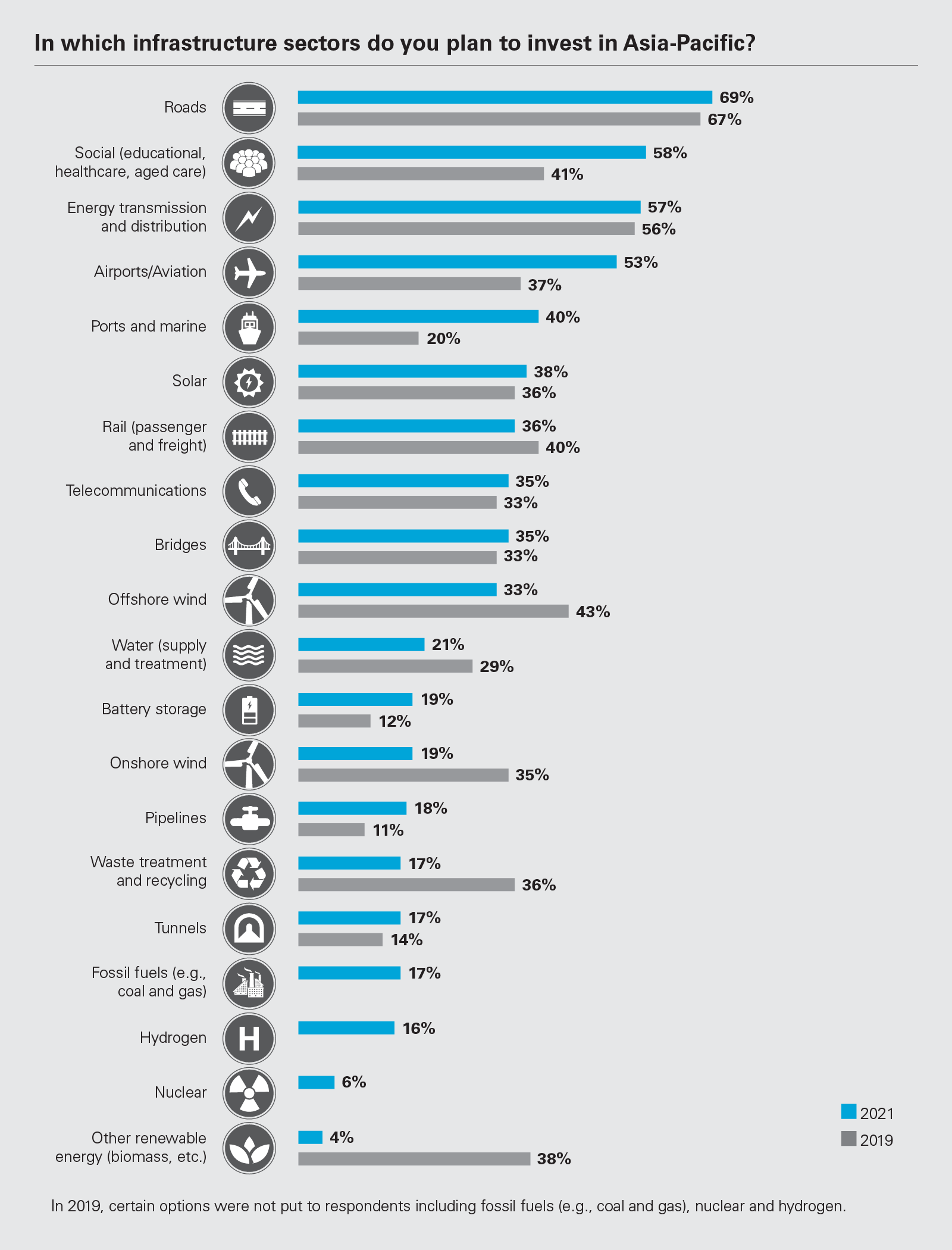

Mirroring the findings from our previous report, roads are once again seen as the key infrastructure sector destination. The most eye-catching trend is the significantly increased focus on social infrastructure, with 58 per cent of firms intending to invest.

Responsibility reigns

An increasing need for sustainable infrastructure management caused 60 per cent of respondents to cite environmental, social and governance (ESG) considerations as ‘very important’ when looking at their investment in the region.

Despite the pandemic, optimism for Asia-Pacific infrastructure projects is increasing with investors looking at a plurality of regions and sectors

Digitalisation and ESG are transforming the face of infrastructure. Here we explore how investors are reacting to the opportunities and challenges these forces present

The future is bright for the asset class in the region. Here we explore investor' vision for the future

Despite the pandemic, optimism for Asia-Pacific infrastructure projects is increasing with investors looking at a plurality of regions and sectors

World in Transition

Our views on changing dynamics in energy, ESG, finance, globalization and US policy.

Global infrastructure as an asset class continues to attract investors as it is less susceptible to major economic cycles and short-term fluctuations, and provides comparatively steady income streams.

A January 2021 report from research firm Cerulli found that private global infrastructure investments had risen to US$583 billion by the end of 2020. And our survey finds that respondents say 54 per cent of their total infrastructure spend is in Asia-Pacific compared with the rest of the world. This is up from 50 per cent in our 2019 survey.

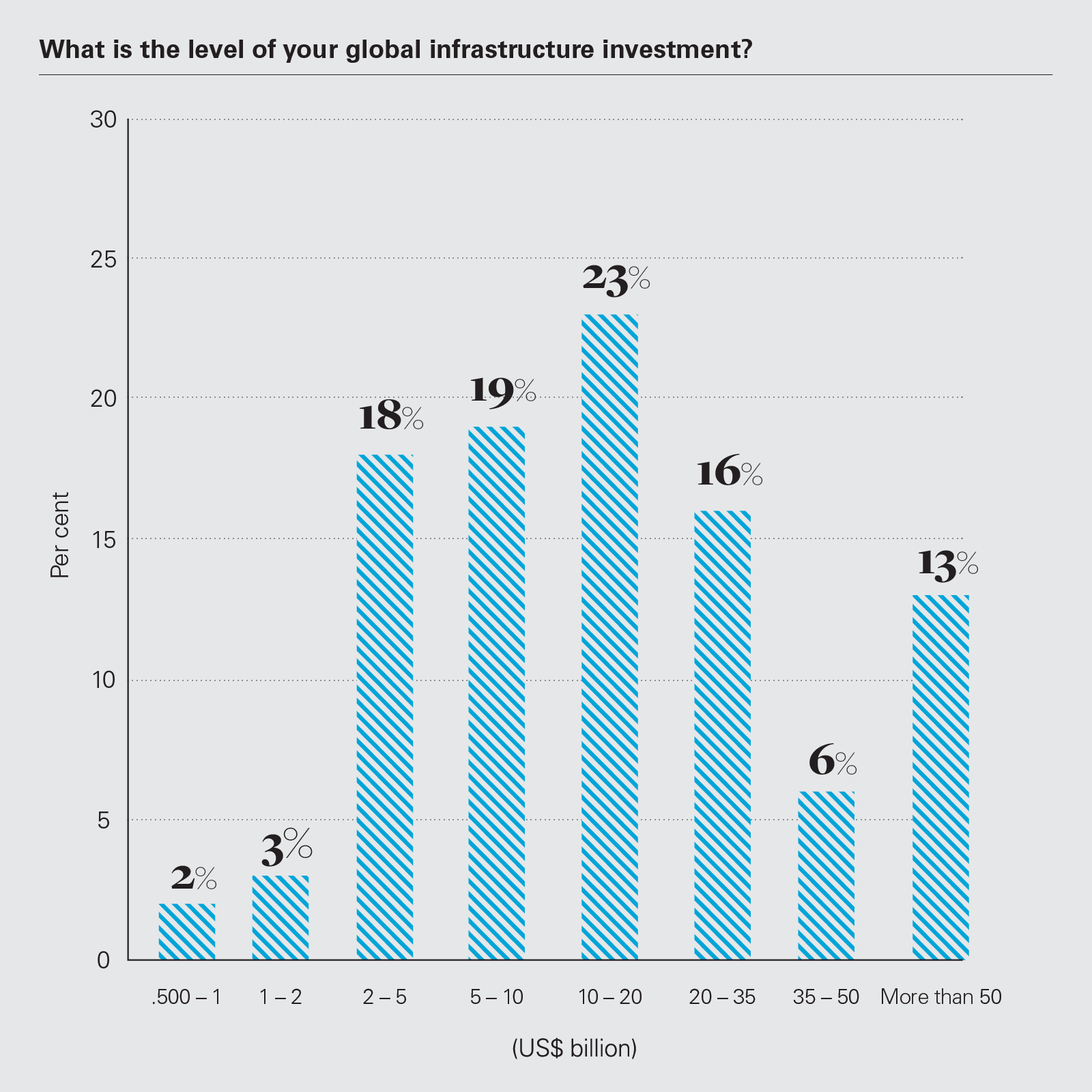

Global infrastructure as an asset class continues to attract investors as it is less susceptible to major economic cycles and short-term fluctuations and provides comparatively steady income streams. And our survey finds that respondents will continue to invest heavily in the asset class. A majority (95 percent) intend to invest in excess of US$2 billion in 2021.

Given that there remains an annual infrastructure financing deficit of US$459 billion, investment of this volume is vital. Government and private sector funding will be needed to fund the huge infrastructure pipeline that is essential for an infrastructure-led recovery in Asia -Pacific.

78%

Of investors intend to grow their teams in Asia in 2021

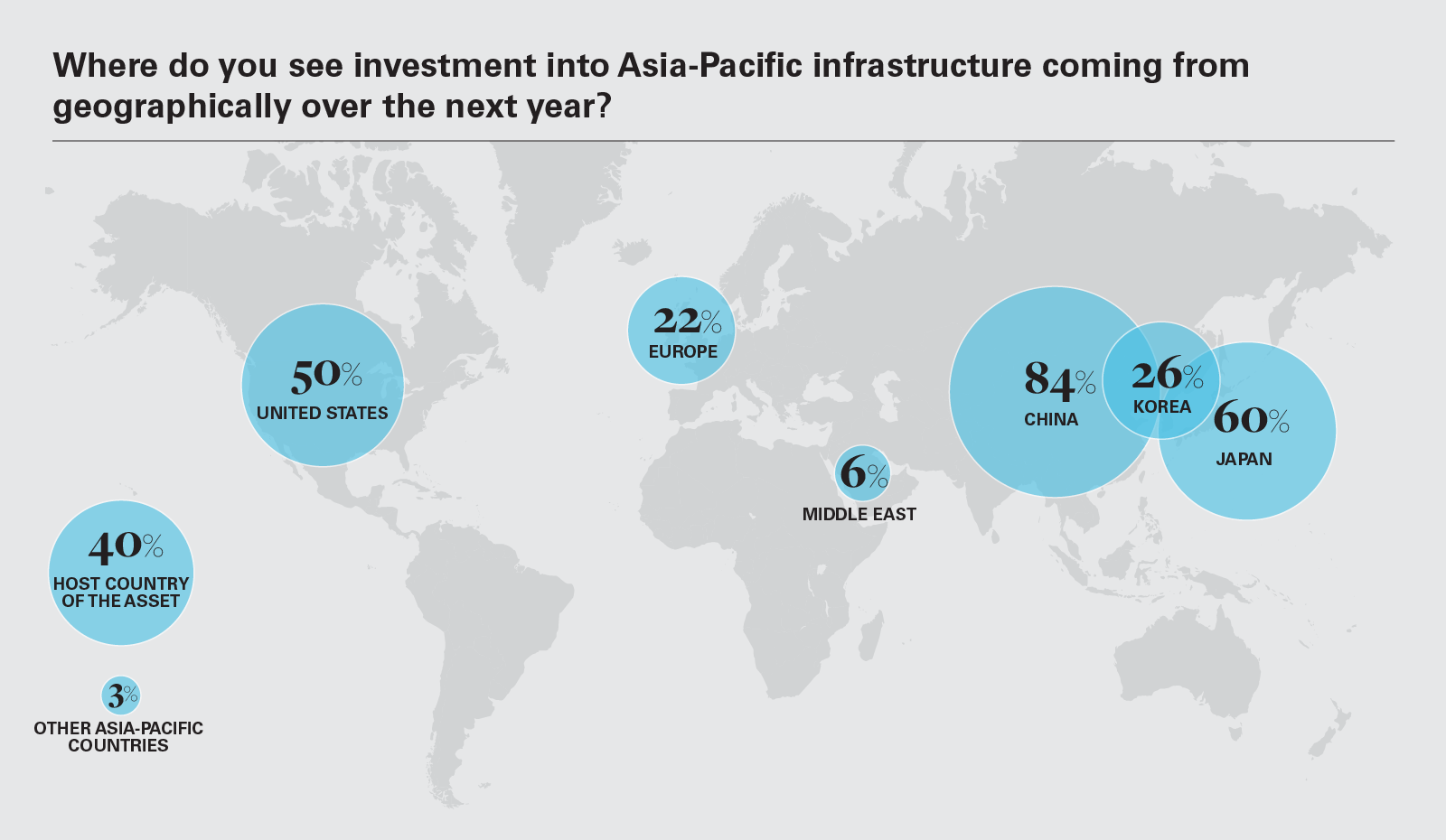

The majority of this investment is coming from Asia. Our survey reveals a gulf between intercontinental money and Western investment in the region—87 per cent of APAC respondents say that their investment is in Asia, compared to respondents from the Americas and EMEA whose investment in Asia is 19 per cent and 21 per cent, respectively.

As was the case two years ago, infrastructure investment in the region is primarily coming from China and Japan, as the world's second and third-largest economies continue to compete for assets. Japan's projects are concentrated in three of the region's largest economies: the Philippines, Singapore and Vietnam. China, meanwhile, is intent on resuming many of its listed Belt and Road Initiative (BRI) projects, such as its East Coast Rail project in Malaysia.

The gap between East and West is also seen in the numbers looking to grow their teams in the region. Overall, 78 per cent of firms intend to grow their teams in Asia in 2021—and although this is down 10 per centage points on our 2019 survey, the breakdown of results is more nuanced. Nearly all Asia- Pacific respondents (96 per cent) are looking to expand their teams in the region while the overall figure is pulled down by the 68 per cent and 52 per cent of Americas and EMEA respondents, respectively, who say the same. The latter numbers are likely down due to concerns over the pandemic as stringent cross-border travel restrictions are still in place across much of the West. In addition, Asian investment mandates are more likely to focus on their own region.

However, it is worth noting that there has been no 'decoupling' from Asia – as evidenced by the six per cent year-on-year rise in US investments into China during the first half of 2020.

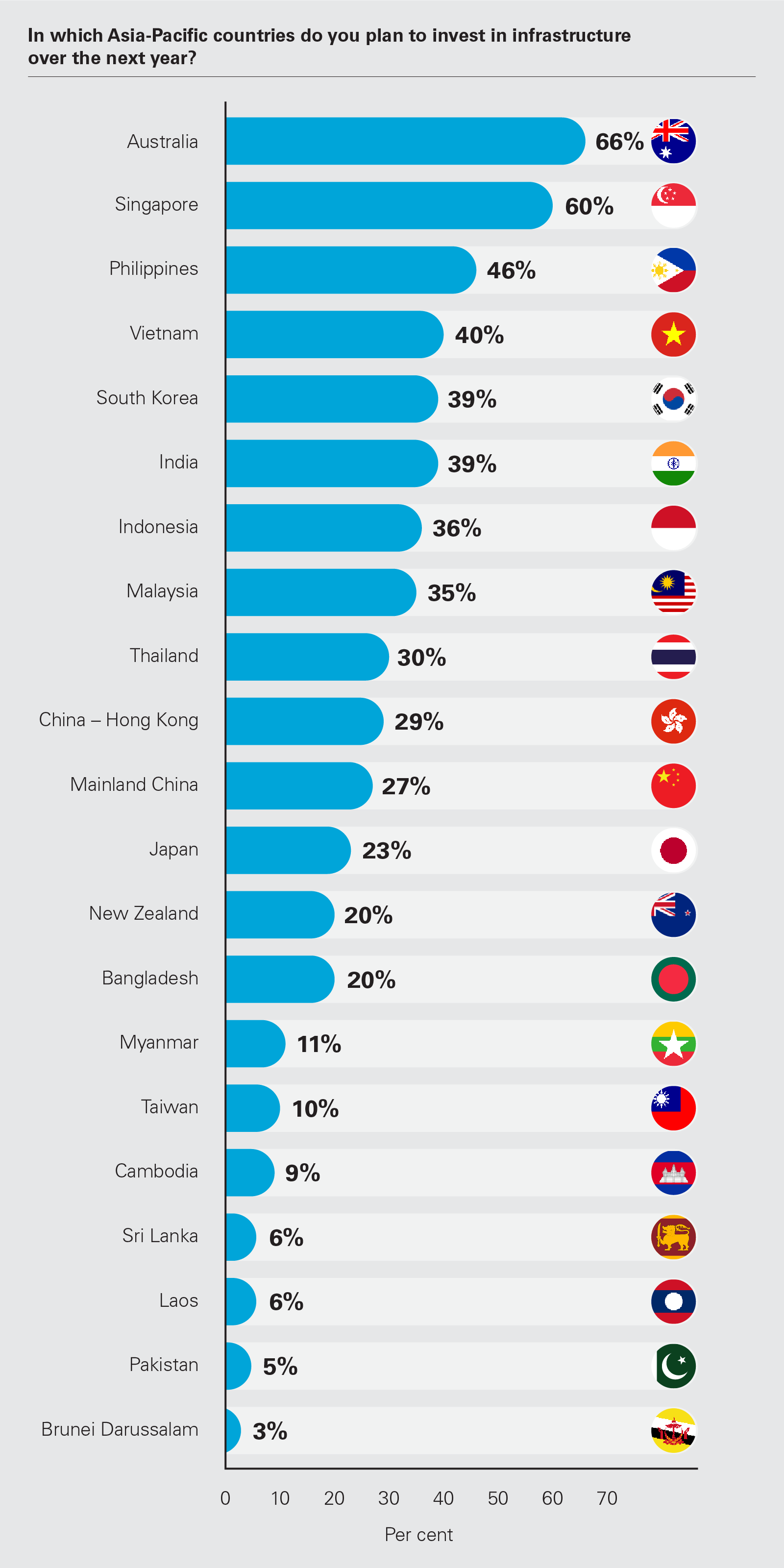

While investors are eyeing up prospects across the region, our research reveals that the majority are looking at countries with healthy economies, stable political systems and reliable legal frameworks. Once again, Australia is proving most popular with investors, with 66 per cent of respondents citing it as a key destination for infrastructure investment over the next year.

66%

plan to invest in Australian infrastructure over the next year

The popularity of Australia is particularly interesting as it has long been one of the more competitive markets in the world for infrastructure investment. And entry was potentially made harder in March 2020, when in response to COVID-19's potential impact on the economy, the Australian government announced that nearly all foreign investment would require screening and prior approval through the Foreign Investment Review Board (FIRB). While these measures were rolled back from 1 January 2021, it remains the case that most foreign investors will require FIRB approval for their investments in Australian infrastructure assets.

Chinese and Japanese companies have long been searching for opportunities in the Australian infrastructure sector, and are likely to continue pursuing acquisitions and joint venture opportunities with local players in order to establish a competitive platform on the ground. As Australia continues to transition away from fossil fuel-based energy, the greatest opportunities will be found in transition fuels (primarily gas) and renewables platforms.

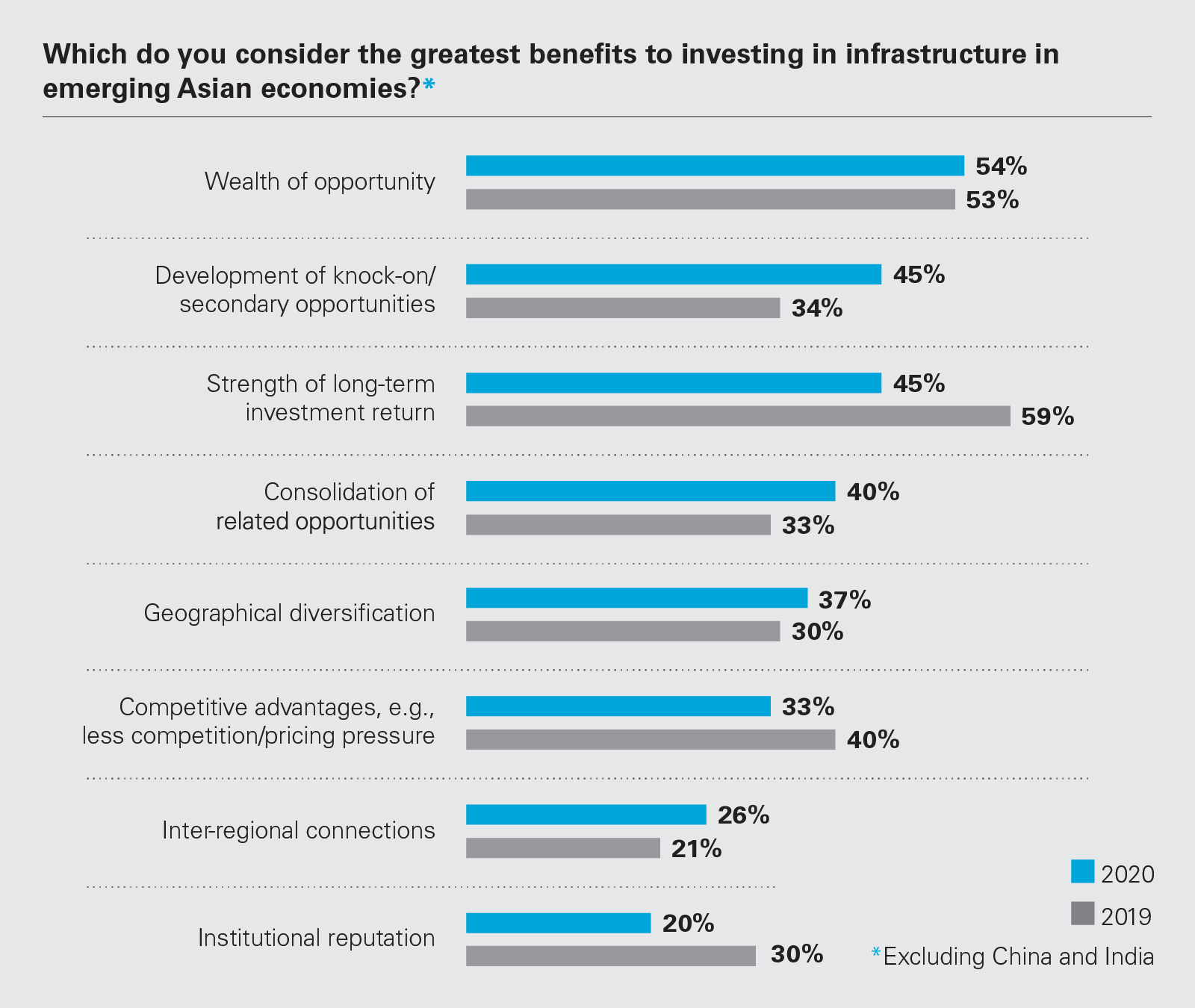

54%

consider wealth of opportunity to be the greatest benefit to investing in infrastructure in emerging Asia

Forty-six per cent of respondents plan to invest in the Philippines in 2021, with almost the same number (40 per cent) targeting Vietnam. Such emerging markets provide significantly different value propositions for investors.

For example, although Vietnam's economy in 2020 grew at its slowest pace in at least three decades due to the effects of COVID-19, its comparative success in containing the virus saw it record gross domestic product (GDP) growth of 2.91 per cent, one of the highest in the world. However, with domestic energy demand growing by 10 per cent each year as a result of economic growth and a rising population, the lack of energy infrastructure could soon lead to power shortages and blackouts.

Foreign investors are therefore increasingly targeting opportunities in renewables, as the Vietnamese government seeks to diversify away from traditional energy sources and increase the proportion of renewables in the country's energy mix, from around nine per cent in 2018 to 21 per cent by 2030.

There are manifold reasons behind the surge in past traditional locations such as India and more developed nations such as Japan. Fifty-four per cent of respondents cited 'wealth of opportunity' as the greatest benefit to investing in the emerging economies, with 45 per cent looking forward to both the 'development of knock-on/ secondary opportunities' as well as the 'strength of long-term investment return'.

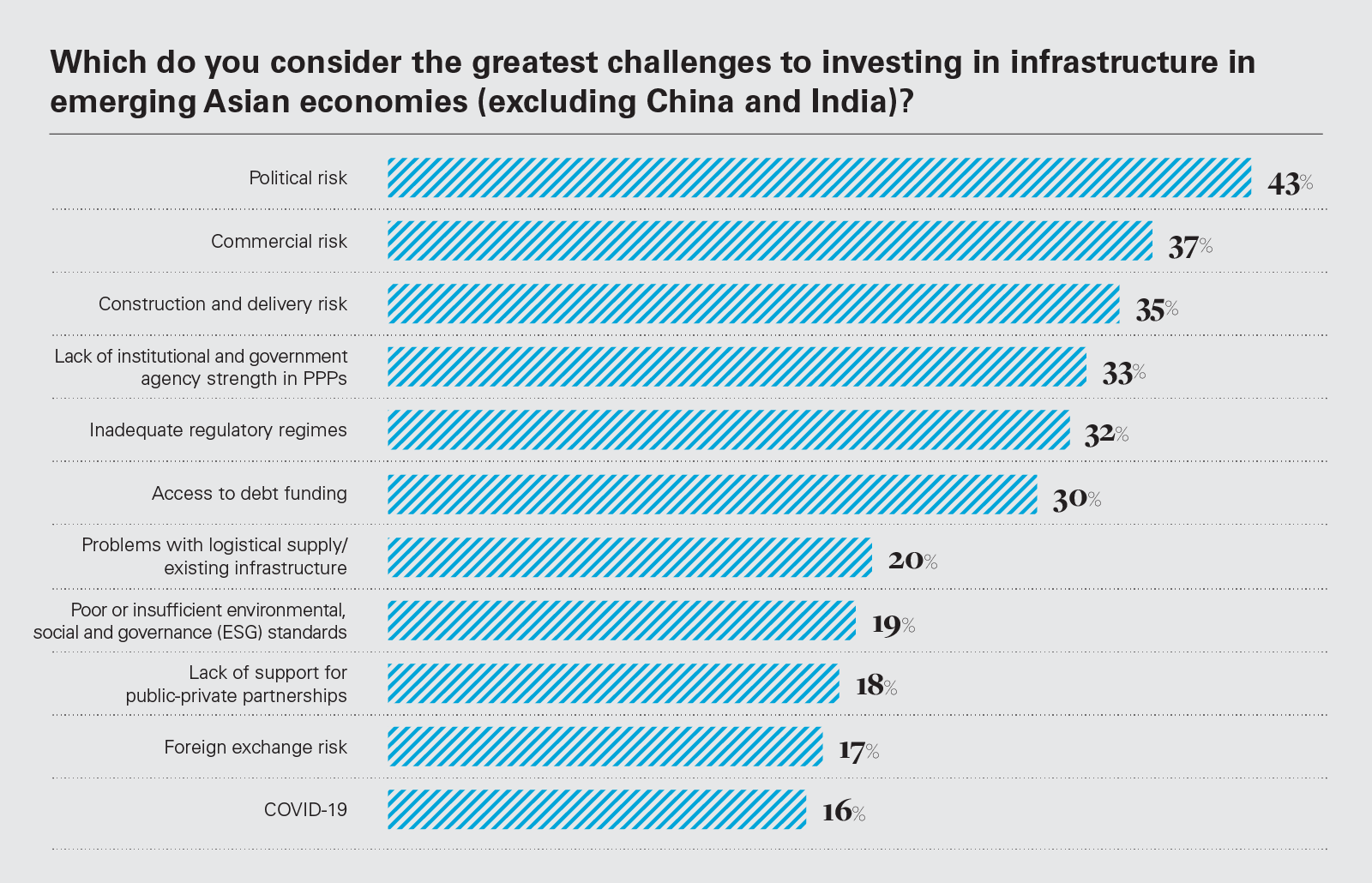

However, while opportunities may abound, investors also noted numerous challenges—principal among these was political risk. Forty-three per cent of respondents considered it to be the biggest challenge, with concern most pronounced among investors in the Americas.

"Political risk has increased in the wake of the spread of coronavirus," said the director of investment at one US investment fund. "Countries have become more protective about letting in new investors."

One project that has been abandoned due to politics and policy issues is the US$25 billion Kuala Lumpur-to-Singapore high-speed rail project. After years of delays, two changes of government in Malaysia and the expectation of reduced travel volume in the coming years as a result of COVID-19, the Malaysian government will now pay Singapore a termination fee.

The situation in Malaysia demonstrates that governments need to provide a level of political and legal stability if they hope to attract investors.

Linked to political risk, inadequate regulatory regimes are cited by 32 per cent of respondents, with investors often facing uncertainty over their basic contractual rights against local partners and sovereign entities in underdeveloped legal jurisdictions.

"When we invest in Europe, we are aware of the regulatory expectation and scrutiny levels," said the managing director of one Swiss investment bank. "When investing in Asia-Pacific, especially the emerging cultures, inadequate regulatory regimes are tough to deal with. The conditions are somewhat uncertain."

To mitigate risks associated with inadequate regulatory regimes, investors need to maintain close working relationships with relevant regulatory authorities and government-backed partners. And they are encouraged, during the pandemic, to pursue joint ventures with domestic partners as a means of conducting on-the-ground deal execution and due diligence.

Commercial risk was cited by 37 per cent of respondents as the greatest challenge to investing in APAC infrastructure. Concerns around the bankability and commercial viability of large-scale public projects is arguably the most significant trend that has been accelerated by the pandemic. In November, the government of the Malaysian state of Melaka terminated an agreement with the main developer of the US$10.5 billion Melaka Gateway, a BRI infrastructure port that had promised huge trade opportunities but had raised environmental red flags.

Thirty-five per cent of respondents highlighted construction and delivery risk as the main challenge facing investors, suggesting perhaps a maturing market with investors gaining a better understanding of the inherent risks of each jurisdiction. This was a particular concern among APAC investors, with 46 per cent citing it compared to 28 per cent of EMEA investors and only 20 per cent of investors in the Americas.

"Once construction starts, contractors have to be careful about construction and delivery risk," said the director of investment at one Australian investment fund. "Maintaining the quality of projects is important. Unless this is achieved, projects will be faced with regulatory risks down the line. If regulatory scrutiny increases, we have to be prepared."

Our research shows that transportation and energy transmission and distribution remain the most popular sectors for investment. Sixty-nine per cent of firms cited roads, up from 67 per cent in 2019, while 57 per cent mentioned energy transmission and distribution, an increase of 1 per cent from 2019.

However, it is another transportation asset class—airports/ aviation—that is seeing the biggest surge in investor interest, with 53 per cent planning to invest in the sector, up from 37 per cent in 2019.

While air transport has been one of the sectors most adversely affected by COVID-19 due to travel restrictions and lockdowns, with airports the hardest hit infrastructure class, travel demand should remain healthy in the long run and pricing is likely to be attractive as a result of the pandemic. "Investing in the aviation sector will derive better revenue long term," said the managing director of one Swiss investment fund. "We cannot judge the industry solely on recent events. There will be more development projects initiated once COVID-19 cases reduce."

Meanwhile, with many APAC countries continuing their transition towards becoming low-carbon economies, investments in onshore and offshore wind generation are being assessed. "Offshore wind development projects will be undertaken," said the director of M&A at one Spanish sponsor. "We understand the risks and prospects well, which is why opportunities will be pursued in this segment."

Thirty-three per cent of firms are planning to invest in offshore wind development projects in 2021, while 19 per cent are targeting opportunities in onshore wind. This is down from 43 per cent and 35 per cent, respectively, in our 2019 survey. It is likely that these drop-offs are due to previous high levels of activity in the space and the maturation of a number of developments. That said, the APAC market is expected to be one of the key hubs for both onshore and offshore wind construction activity over the next decade with many countries adding substantial volume over the short to medium term.

The big increase in sector interest is in social infrastructure, with 58 per cent of firms intending to invest in educational, healthcare and aged care management. This is up from 41 per cent in 2019, when the asset class was only the fifth highest priority for investors. This growth is most likely a direct result of the COVID-19 outbreak and the health crisis that has ensued; however it is yet to be seen whether actual opportunities can emerge quickly enough to capitalise on this sentiment.

"Amid the pandemic, social infrastructure development and the creation of health centres has been given more importance," said the head of infrastructure investments at one Singaporean investment fund. "This theme will continue in order to ensure that countries are self-sufficient to manage a health crisis."

As with all regions of the world, the pandemic has had a hugely detrimental impact on the development of infrastructure in the Asia-Pacific region

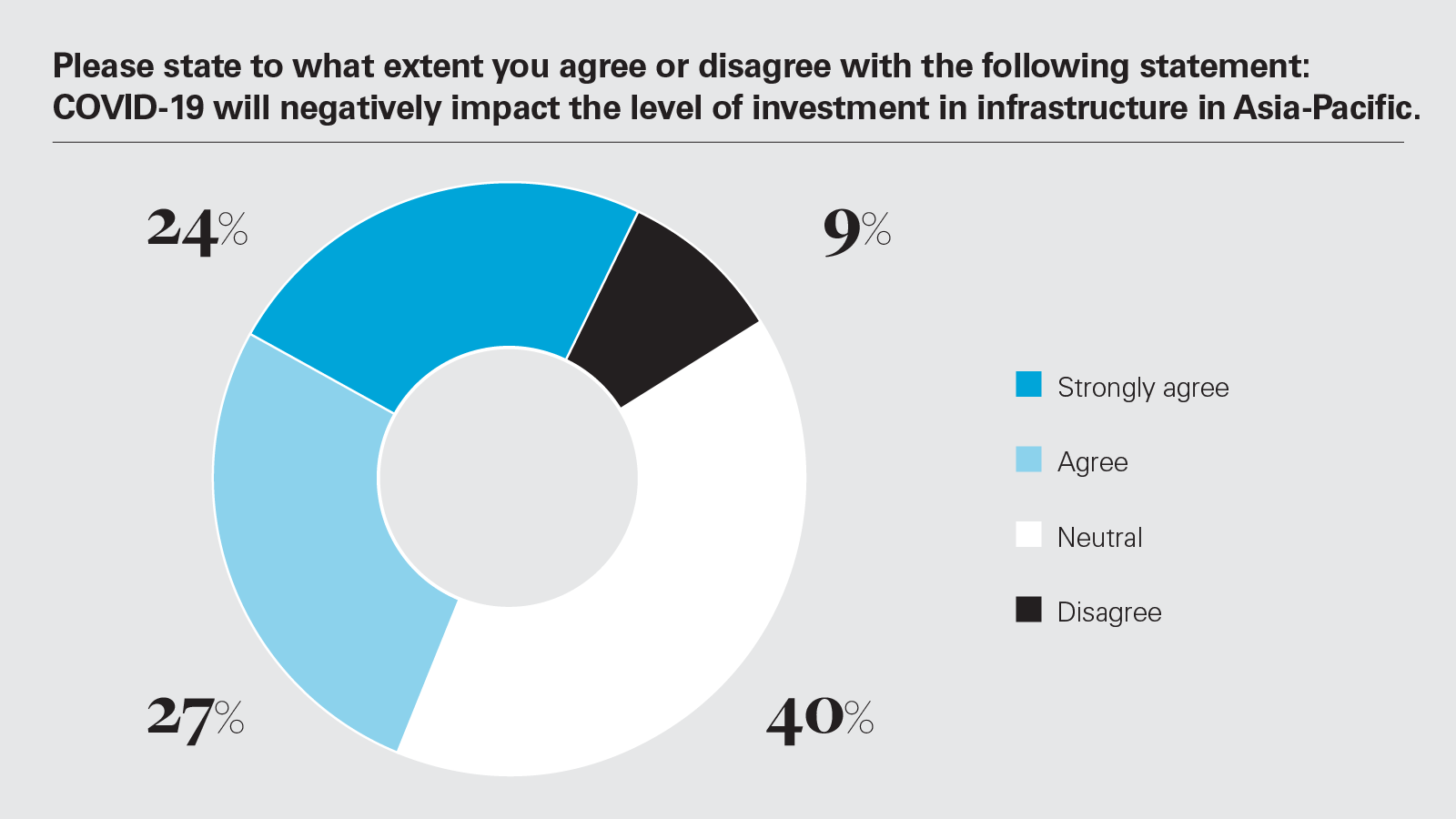

51%

agree that COVID-19 would negatively impact the level of investment in APAC infrastructure in 2021

COVID-19 will dictate the key themes in the Asia-Pacific infrastructure market in 2021. In regions where there are more cases, governments will be attentive to social and health concerns rather than massive railway or roadway development

For example, Chinese-sponsored projects that source construction labour and machinery from Chinese factories were suspended in the early days of the outbreak, while planning and progress for new projects was delayed.

Our survey reveals that 51 per cent of respondents agreed (24 per cent strongly) that COVID-19 would negatively impact the level of investment in APAC infrastructure in 2021. However, the perspective on this differs greatly by region. While 48 per cent of respondents from EMEA and 28 per cent from the Americas strongly agreed, only 10 per cent of APAC investors are overly concerned. This again can likely be attributed to the region's capacity to take COVID-19 mitigating measures.

In many ways, the pandemic has accelerated trends that were already evident. China was already becoming increasingly commercial and risk-aware with its overseas funding, and has for some time been shifting its focus more towards technology projects connected to its Digital Silk Road.

While it might not have been unreasonable to have expected a rise in opportunities to secure distressed infrastructure assets in 2020 as a result of the impact of COVID-19, a combination of resilient debt and equity markets globally and the stable nature of the asset class itself reduced the number of opportunities available.

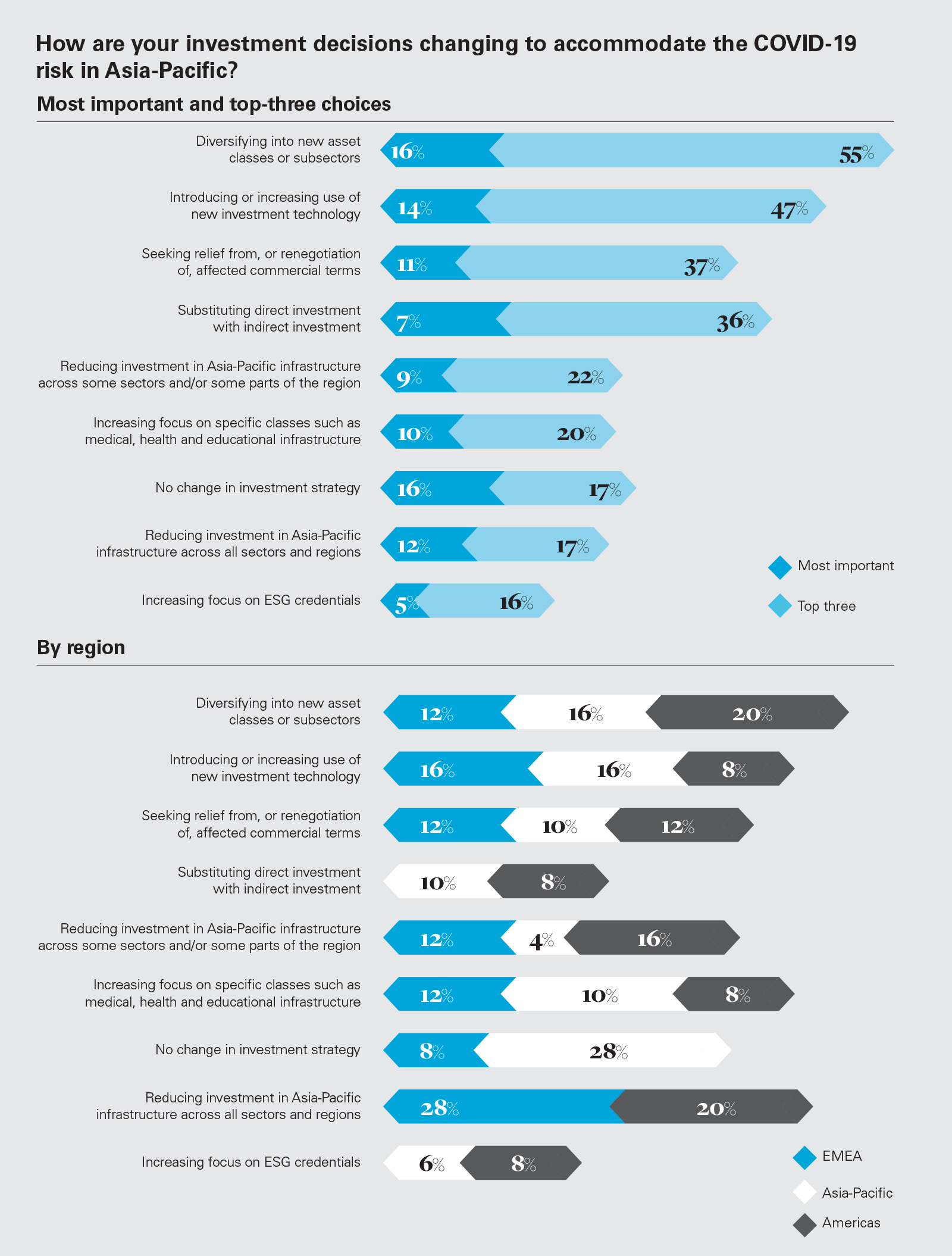

Instead, in order to accommodate the COVID-19 risk, 55 per cent of respondents said that diversifying into new asset classes or subsectors was among their top-three investment decisions, with 16 per cent citing it as their most important decision. Introducing or increasing use of new investment technology was also mentioned by 47 per cent of respondents. "COVID-19 will dictate the key themes in the Asia-Pacific infrastructure market in 2021," said the director of investment and corporate finance at one Spanish sponsor. "In regions where there are more cases, governments will be attentive to social and health concerns rather than massive railway or roadway development."

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

What is the level of your global infrastructure investment? (PDF)

What is the level of your global infrastructure investment? (PDF)

Where do you see investment into Asia-Pacific infrastructure coming from geographically over the next year? (PDF)

Where do you see investment into Asia-Pacific infrastructure coming from geographically over the next year? (PDF)

Is your team size in Asia-Pacific changing or staying the same? (PDF)

Is your team size in Asia-Pacific changing or staying the same? (PDF)

In which Asia-Pacific countries do you plan to invest in infrastructure over the next year? (PDF)

In which Asia-Pacific countries do you plan to invest in infrastructure over the next year? (PDF)

Which do you consider the greatest benefits to investing in infrastructure in emerging Asian economies?* (PDF)

Which do you consider the greatest benefits to investing in infrastructure in emerging Asian economies?* (PDF)

Which do you consider the greatest challenges to investing in infrastructure in emerging Asian economies (PDF)

Which do you consider the greatest challenges to investing in infrastructure in emerging Asian economies (PDF)

In which infrastructure sectors do you plan to invest in Asia-Pacific? (PDF)

In which infrastructure sectors do you plan to invest in Asia-Pacific? (PDF)

Please state to what extent you agree or disagree with the following statement (PDF)

Please state to what extent you agree or disagree with the following statement (PDF)

How are your investment decisions changing to accommodate the COVID-19 risk in Asia-Pacific? (PDF)

How are your investment decisions changing to accommodate the COVID-19 risk in Asia-Pacific? (PDF)