United States

US antitrust agencies were active in merger enforcement in 2019 and 2020, reflecting the agencies’ commitment to antitrust enforcement particularly in transactions involving nascent competitors and technologies

17 min read

Subscribe

Stay current on your favorite topics

The antitrust agencies have adapted to the practical challenges of the pandemic through implementation of a successful HSR e-filing system, and investigations have continued mostly

unabated

*Accurate as of February 2021

Key developments

US antitrust agencies were active in merger enforcement in 2019 and 2020, similar to recent years, despite the COVID-19 pandemic.

In the first half of 2020, the Federal Trade Commission (FTC) was even on pace for one of its busiest years in two decades. The FTC sued to block five mergers, caused eight mergers to be abandoned and reached seven settlements with divestitures.

The Department of Justice's (DOJ) 2021 projection of 70 merger investigations is consistent with 2020 and 2019.

2019 was equally busy for merger enforcement; the DOJ and FTC issued second requests at the highest rate in three years in 2019. State antitrust enforcers were also active, with state attorneys general challenging UnitedHealth's acquisition of DaVita and T-Mobile's merger with Sprint, despite settlements with federal antitrust agencies.

The enforcement activity levels reflect the agencies' commitment to antitrust enforcement. This appears particularly true for transactions involving nascent competitors or technology, where a business or technology has begun impacting competition in a relevant market, but is anticipated to impact competition even more in the future.

This focus is evidenced by the FTC's challenges to Edgewell Personal Care's proposed takeover of Harry's, Illumina's merger with Pacific Biosciences, and the DOJ's challenge to Sabre's acquisition of Farelogix. These cases also reflect that the agencies are still focused on killer acquisition theories, with the DOJ alleging, for example, that Sabre's purchase of Farelogix was an attempt to neutralize or eliminate an innovative competitor.

Digital, data and technology markets generally also continue to be areas of focus for the antitrust agencies. The FTC even established the Technology Enforcement Division (TED) in 2019, which focuses on investigating antitrust conduct in technology markets.

The FTC is also examining prior acquisitions by large technology firms that were not reportable under the Hart-Scott-Rodino (HSR) Act, suggesting that non-reportable technology transactions will face increasing scrutiny in the future.

The DOJ reorganized in 2020, with a section solely devoted to technology matters, including the review of technology and digital platforms mergers.

With this level of enforcement activity, including bringing difficult and sometimes novel cases, it is not surprising that the FTC and DOJ lost key merger challenges in federal court.

After a string of victories, the FTC lost its challenge of Evonik's US$625 million acquisition of hydrogen peroxide manufacturer PeroxyChem. The court rejected the FTC's novel "swinging" supply theory—that suppliers are able to easily shift facilities between providing different products—for defining the relevant product market.

The DOJ successfully resolved 100 percent of its merger challenges in 2017 and 2018, but lost its challenge of Sabre's US$360 million proposed acquisition of Farelogix in the airline booking industry in 2019. The court rejected the DOJ's characterization of Farelogix as a nascent competitor finding instead that Farelogix, although an innovator in the past, was no more innovative than other competitors.

State antitrust enforcers also suffered a significant merger loss this past year in federal court when 14 attorneys general challenged the T-Mobile/Sprint merger, and failed to show how a deal that had received FCC and DOJ approval harmed competition.

Impact on merging parties

Despite the numerous impacts of COVID-19 on all aspects of the economy and the regulatory agencies, the antitrust agencies have adapted to the practical challenges created by the pandemic through implementation of a successful HSR e-filing system. Investigations and litigation have continued mostly unabated, despite typical disruptions and challenges caused by remote working.

However, it is sensible for parties to build in time for potential delays in agency review caused by COVID-19 disruption. They may want to negotiate longer termination dates to account for slower than usual industry input necessary for agency investigations. Parties might also consider whether any closing conditions may be in jeopardy, including because a material adverse effect may have occurred as a result of the economic impact of COVID-19.

With a rise in bankruptcies due to COVID-19, there has been an increase in the "failing firm" defense. This is an absolute defense to an otherwise unlawful merger, but only can be asserted where a financially distressed party's exit from the relevant market is imminent.

For example, Dairy Farmers of America contended that Dean Foods' bankruptcy was indicative of a grave possibility of business failure. In its approval subject to divestiture, the DOJ acknowledged that the dairy industry, due in part to diminished school milk demand, was impacted severely by COVID-19.

The failing firm defense is not a panacea, however, given the stringent requirements. The alternative weakened firm defense is easier to establish and was accepted by a federal court in T-Mobile/Sprint, although this predated COVID-19.

Cross-jurisdictional merger control cooperation continues, regardless of COVID-19. Parties should plan for cross-border considerations such as timing requirements and potentially divergent theories of harm. During complex merger reviews that affect multiple jurisdictions, the DOJ and FTC may, in certain circumstances, communicate and share information with other antitrust enforcement agencies.

For example, the DOJ and the UK's Competition and Markets Authority (CMA) shared confidential information about Sabre's acquisition of Farelogix, and the DOJ dealt with accusations that it had improperly coordinated with the CMA to block the deal.

In response to criticism, the DOJ reiterated that it conducts separate investigations and reaches independent conclusions when sharing information with other antitrust enforcement agencies. This example underscores the potentially high level of coordination among regulators, and parties facing multiple merger control regulators can benefit from streamlining information collection through a single, cohesive process to ensure strategic alignment on key issues across jurisdictions.

In addition to international cooperation, there has been and continues to be coordination between federal and state agencies on merger investigations. Sometimes, however, the federal and state agencies do not agree on a resolution, and parties need to plan for the possibility that state and federal investigations may diverge.

The most recent example of this involved the T-Mobile/Sprint merger. The DOJ approved a divestiture package, while 14 attorneys general elected to challenge the merger settlement in federal court. The court did not agree that the merger, with the divestiture to Dish Network, would harm consumers.

Despite this, parties should be prepared for a potential increase in state-led antitrust enforcement that deviates from federal enforcement. For example, Colorado recently passed a bill enabling the Colorado attorney general to challenge mergers that the federal agencies investigate and decline to challenge, which was previously prohibited under the Colorado Antitrust Act.

Senator Amy Klobuchar, ranking member of the Senate judiciary subcommittee that includes antitrust, predicts a record year of law-making for antitrust in 2021

Recent changes in priorities

The antitrust agencies have increasingly been focusing on transactions involving nascent or killer acquisitions. The agencies also continue to investigate nonreportable, finalized mergers, and agency actions at the time of writing that suggest that non-reportable technology mergers could soon be an enforcement priority.

The agencies may challenge any merger, regardless of whether it is reportable under the HSR Act or how much time has passed since consummation, although it is rare for an agency to challenge a transaction long after consummation or clearance. For example, the FTC has challenged Axon's completed 2018 non-reportable US$13 million acquisition of VieVu, a body-worn camera competitor, and an FTC administrative trial is scheduled.

Since February 2020, the FTC also has been engaged in a study of prior non-reportable acquisitions by large technology companies from 2010 to 2019. The FTC issued special orders under section 6(b) of the FTC Act to large technology companies requesting information about prior unreported acquisitions since 2010.

The use of special orders for antitrust purposes is rare—indeed the last time the FTC issued such orders was in 2014 when it studied patent assertion entities.

The latest requests for information, in part, were driven by the FTC learning through its hearings on competition and consumer protection in the 21st century in 2018 and 2019 that digital platform companies had conducted hundreds of non-reportable transactions in recent years.

The study could lead to the FTC taking steps to unwinding years- old deals or, more likely, serve as the basis for future amendments to HSR reporting requirements. In September 2020, FTC former chairman Joseph Simons said the commission may issue a special order requiring certain large technology firms to notify transactions falling below the HSR reporting thresholds.

The 6(b) study, which is closely examining how small companies perform after they are acquired by large technology companies, may also serve as a mechanism for the agencies to sharpen their enforcement practices with respect to nascent acquisitions. There could be similar reviews of other sectors such as the healthcare industry in the future, in particular the dialysis, pharmaceutical and hospital industries.

In an unrelated trend, there has been an unusual level of DOJ scrutiny of deals related to the cannabis industry. There are indications that this was due to political implications, as suggested by a DOJ whistle blower, but the DOJ found no wrongdoing after conducting an investigation.

The agencies issue second requests for information in only about 2 percent of reported transactions, yet the DOJ has issued ten second requests in the cannabis industry since March 2019—29 percent of the DOJ's 2019 second requests. Regardless of the motivation for this, parties and counsel in this industry should be aware of the high rate of second requests when evaluating transactions.

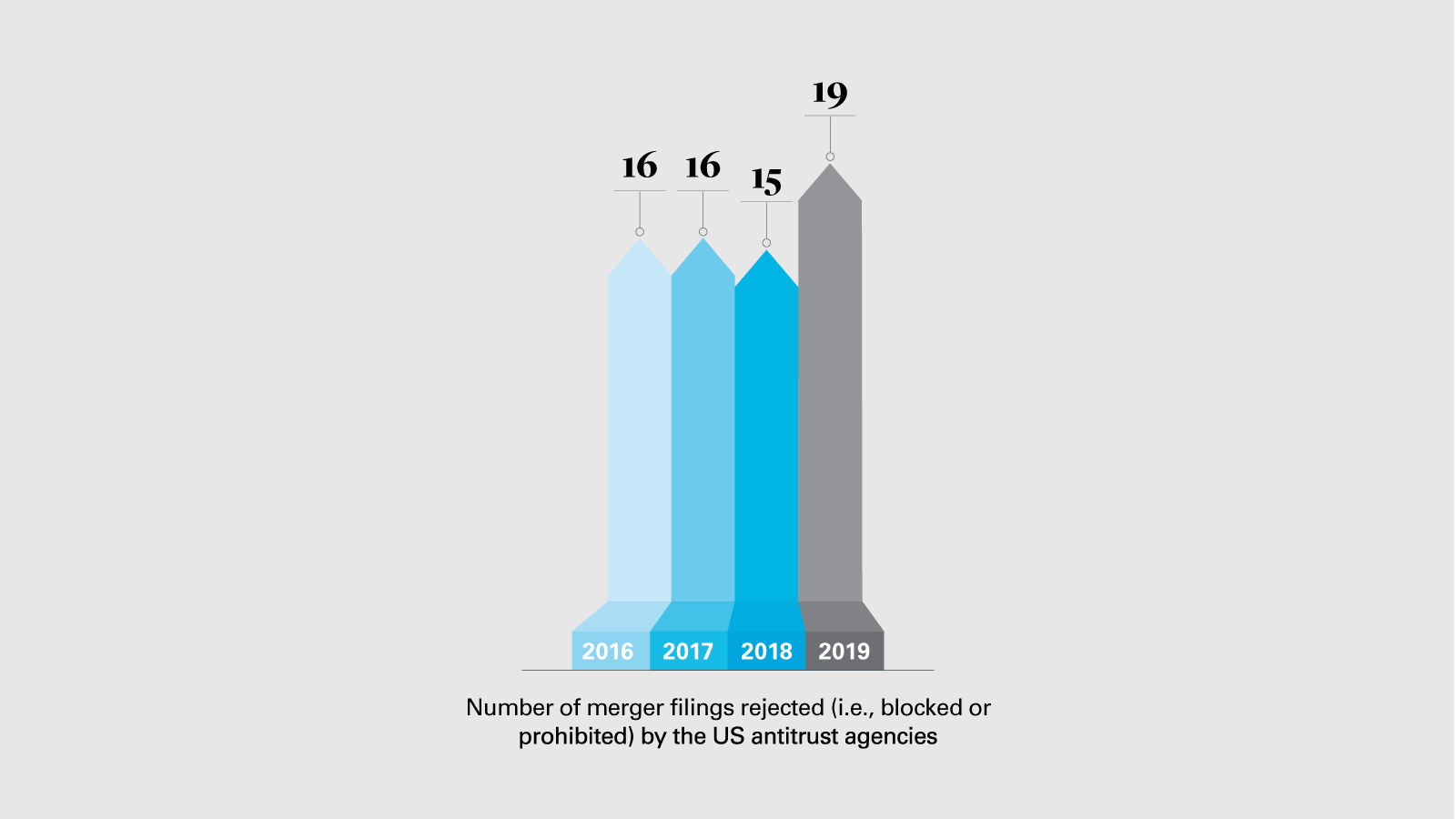

View full image: Number of merger filings rejected (PDF)

View full image: Number of merger filings rejected (PDF)

Key enforcement trends

The agencies have been focusing increasingly on acquisitions of nascent competitors and related theories of killer acquisitions. In particular, they have raised concerns about acquisitions of nascent competitors in platform industries because these markets are prone to quickly gaining market share by being a favored platform through enhanced network effects and economies of scale.

Accordingly, the agencies are carefully reviewing acquisitions of smaller players, especially those that are innovative or disruptive. Successive acquisitions of potential entrants could qualify as an antitrust violation where the takeover of a potential competitor could be viewed as excluding a nascent threat.

In the Edgewell/Harry's case, the parties ultimately abandoned their US$1.37 billion shaving industry transaction after the FTC voted 5-0 to challenge it. The FTC alleged that Edgewell's acquisition of Harry's, which was founded as a direct-to-consumer wet-shave brand, would eliminate an innovative and disruptive competitor that reduced prices.

Interestingly, the FTC's perception of Harry's as an innovative but smaller competitor in a concentrated industry did not stem from the introduction of a ground breaking product, but from the sale of a no-frills century-old product at a low price point. This is a good reminder that innovation takes many forms, and the agencies do not limit their focus on nascent competitors to those developing cutting-edge or technologically advanced products.

In the case of the Illumina/Pacific Biosciences deal, the parties abandoned their US$1.2 billion next-generation DNA sequencing systems transaction after the FTC authorized an administrative complaint alleging that the acquisition would harm competition by eliminating Pacific Biosciences as an innovative force that pushed other competitors to develop new products.

Pacific Biosciences did not have a large market share and had lost more than US$100 million just a year earlier. However, the FTC claimed that Illumina had monopoly power and that it attempted to stamp out Pacific Biosciences' competition, as the latter's technological advancements made its product more comparable to Illumina's. This serves as a warning to companies considering transactions with what might be described as a uniquely innovative, but not established or profitable competitor.

The DOJ has also pushed for a novel new process for resolving merger objections, and has demonstrated a willingness to use arbitration as an alternative to going to court to challenge potentially anticompetitive mergers.

The DOJ was prepared to challenge Novelis' proposed US$2.6 billion acquisition of Aleris. The parties agreed to divest certain facilities if the DOJ won on a single-issue arbitration, which focused on whether the relevant product market for aluminum auto body sheets included only procurement or both procurement and design.

This was the first time that a federal antitrust agency used its arbitration authority and the DOJ's challenge was successful, which could lead the agencies to consider arbitration more often.

The antitrust agencies have also continued to enforce negotiated remedies. In 2020, Alimentation Couche-Tard (ACT), a Canadian gas station and convenience store operator, agreed to pay a US$3.5 million civil penalty to settle FTC allegations that it violated an order requiring the divestiture of ten retail gas stations by June 2018. According to the FTC's complaint, although ACT ultimately divested the gas stations, it had missed the deadline in the consent agreement.

The DOJ also continues to bring enforcement actions against consent decree violators. For example, CenturyLink agreed to settle the DOJ's allegations that it violated the court-ordered final judgment over its merger with Level 3. The settlement included the establishment of a monitoring trustee and an extension by two years of the original non-solicitation agreement in one geographic area.

Additionally, the DOJ settled Live Nation and Ticketmaster's violation of a final judgment that prohibited retaliatory conduct toward concert venues that used different ticketing companies, by extending all obligations on Live Nation by five years, and appointing a monitoring trustee and an antitrust compliance officer.

The DOJ also created a civil conduct task force to enforce judgments and consent decrees, and issued the Merger Remedies Manual, an update to the 2004 policy guide to merger remedies. The manual reflects the DOJ's renewed focus on enforcing obligations in consent decrees through the newly created Office of Decree Enforcement and Compliance and preference for structural remedies.

Recent studies and guidelines

In June 2020, the DOJ and FTC replaced the 1984 Non-Horizontal Merger Guidelines with an updated version of the document, referred to as the Vertical Merger Guidelines (VMG). After 35 years, the prior guidelines no longer accurately reflected the agencies' approach to investigating the competitive impact of vertical mergers.

The VMG apply to vertical mergers that combine firms or assets at different stages of the same supply chain, as well as "diagonal" mergers that combine firms or assets at different stages of competing supply chains. The VMG also apply to vertical issues that can arise from mergers of complements, but do not apply to mergers of complements or portfolio additions where there is no apparent risk of competitive effects involving the same supply chain.

The VMG are a reflection of the agencies' current approach. They focus on potential harm, including foreclosure, raising of rivals' costs, access to competitively sensitive information and resulting coordination, as well as the potential procompetitive effects of a vertical merger, such as streamlining production, increased innovation and the elimination of double marginalization (EDM).

Still, there are some important issues that are not addressed in the VMG. The draft VMG issued in January 2020 suggested a market share screen if the parties' market shares in the relevant market were less than 20 percent, and the related product was used in less than 20 percent of the relevant market.

While this "safe harbor" was omitted from the final VMG, the market share threshold reflects how vertical effects are evaluated as a practical matter. The guidelines also do not address remedies in vertical merger cases. This omission may be due to agency divergence, as the DOJ has been reluctant to issue behavioral remedies for vertical harms.

It will be interesting to see how the agencies apply the VMG to vertical and diagonal mergers going forward. While the guidelines do provide transparency for how the agencies assess vertical mergers, they mostly gather previously known information about vertical mergers, are general, and lack explicit guidance on how the agencies analyze vertical mergers in a practical sense.

The VMG do not contain concrete screens or data points, unlike both the 2010 Horizontal Merger Guidelines and the 1984 Non-Horizontal Merger Guidelines. Recognizing these shortcomings, FTC commissioner Rohit Chopra criticized the VMG as focusing too heavily on economic theory rather than real-world modern market realities.

For example, the VMG emphasize the benefits of EDM; however, it is unclear whether EDM is always actually realized. Additionally, while the agencies rarely litigate vertical merger cases, courts had noted previously that the old guidelines were outdated. With the rush to publish over two FTC commissioner objections, it is unclear how heavily courts will rely on the VMG.

Looking ahead

We do not expect significant merger control changes without a change in the political balance in Congress or change in the administration.

However, Senator Amy Klobuchar, ranking member of the Senate judiciary subcommittee that includes antitrust, predicts a record year of law-making for antitrust in 2021. Over the past year, Democrats have floated various modifications to merger control law, some of which garnered bipartisan support. Klobuchar and Senator Chuck Grassley introduced bipartisan legislation, the Merger Filing Fee Modernization Act of 2019, which would increase filing fees to provide the agencies with more enforcement resources.

Klobuchar also introduced the Consolidation Prevention and Competition Promotion Act of 2019, which would modify the Clayton Act's prohibition on mergers that "substantially" lessen competition to "mergers that, as a result of consolidation, may materially lower quality, reduce choice, reduce innovation, exclude competitors, increase entry barriers or increase price".

Lowering this standard could produce an uptick in enforcement actions, as "material" is defined as "more than a de minimis amount of harm to competition" and the proposal shifts the burden from the agencies to the merging parties to prove that the consolidation does not harm competition.

In 2019, Senator Elizabeth Warren also released a draft of new antitrust legislation, the Anti-Monopoly and Competition Restoration Act. Among other provisions, this would amend the Clayton Act to ban megamergers that meet certain revenue thresholds or market share thresholds.

The legislation would shift the burden to the merging parties to prove that a merger is not anticompetitive in large mergers that meet certain revenue if either company has violated antitrust laws within the previous seven years. Currently, the agencies bear the burden of showing that a merger may substantially lessen competition or tend to create a monopoly.

The House Judiciary's subcommittee on antitrust has also been active, holding a series of bi-partisan hearings on digital platforms in order to document competition problems in the digital economy, and to evaluate whether the current antitrust framework is able to properly address them. Among other issues, the hearings probed previous acquisitions by large technology companies, suggesting that the technology sector could be the impetus for bipartisan changes to merger control rules.

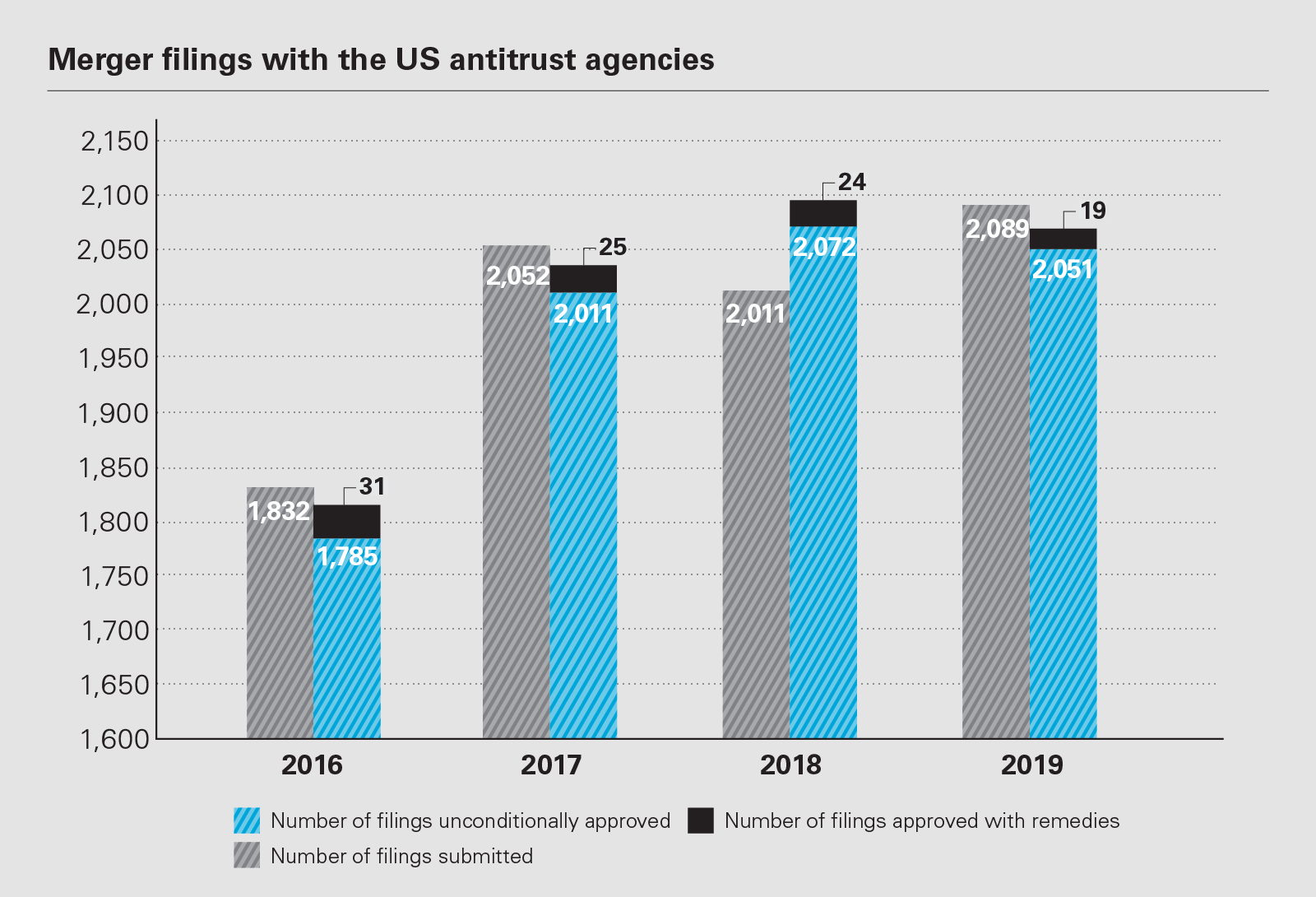

View full image: Merger filings with the US antitrust agencies (PDF)

View full image: Merger filings with the US antitrust agencies (PDF)

THE INSIDE TRACK

What should a prospective client consider when contemplating a complex, multijurisdictional transaction?

Early planning and coordination between companies and advisers enables timely clearance for complex, multijurisdictional transactions. Anticipating and planning for a clear process for lawyers to review and advocate across jurisdictions with different agency procedures also helps to minimize the burden on parties, who often face multiple similar, yet distinct, requests for information from competition authorities.

In your experience, what makes a difference in obtaining clearance quickly?

Thorough pre-filing analysis can make all the difference in obtaining clearance quickly. By front-loading the process and having a deep understanding of all aspects of a business before making the HSR filing, advisers can engage quickly with the FTC or DOJ.

It is important to pre-collect and prepare key documents and other information normally requested through a voluntary access letter, to enable the reviewing agency to focus their area of investigation earlier. A deep dive early in merger discussions also enables the parties to anticipate and mitigate deal risk, and plan for potential divestitures or other remedies, if necessary.

What merger control issues did you observe in the past year that surprised you?

Historically, after the HSR filing, US antitrust agencies would use an informal process to allocate or "clear" the investigation of the merger to one of the agencies. During the last year, however, the FTC and DOJ engaged in protracted clearance disputes, even in industries where historically the transactions had always cleared to one of the agencies. A dispute can impact deal timing by erasing most, if not all, of the initial HSR waiting period. Familiarity with the agencies enables advisers to win back time lost from the initial waiting period by jumping at opportunities during the clearance dispute to advocate about the benefits of the transaction.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP