Latin American arbitration in transition

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

By Carlos Viana, Latin America Interest Group Leader and Editor of Latin America Focus

We are delighted to introduce the first edition of Latin America Focus, a publication produced by the Latin America Interest Group at White & Case. Our intent with this publication is to provide market insights from our practices and proprietary research that could be valuable to senior decision-makers who have an interest in the region.

COVID-19 hit Latin America's economies more heavily than it hit any other region around the world. The region's economies contracted by nearly 7 percent in 2020, compared to a global average of only 3 percent. Current projections indicate a healthy recovery through the end of 2021, perhaps by as much as 6.9 percent according to S&P Global,1 and thereafter steady growth of about 2.5 percent per annum.

As we look forward to 2022 – 2023, Latin America, in very significant part, will likely continue to face the ebbs and flows of populism, resource nationalism and weak institutions that seem to take turns at flooding some of the countries in the region from time to time. Yet, we also see Latin America propelled away from the COVID-19 swamp by the powerful global engines of economic, social and technological evolution that will push heavy foreign investment into the region: unprecedented global liquidity and the search for yields in emerging markets, the energy transition, the commitments to mitigate climate change by global natural resources and energy companies, and the technology-driven push to digitize and automate the increasingly global world economy. We saw these global drivers, and foreign investors' net-net belief that Latin America will resurge in the medium term, supporting our cross-border business in the region through a 2020 – 2021 period that we expected at the outset could be cataclysmic for foreign investment in view of the region's endemic challenges.

In this edition of Latin America Focus, partners in our Latin America Interest Group have written articles based on their personal experiences in the trenches and market research that go to the very heart of both the latest sequel in the Latin American saga of transitions, and the current global forces of growth, the interplay of which will likely shape what is to come in post-COVID-19 Latin America.

Times of transition are frequently associated with greater incidences of disputes, notably investor-state disputes, but also commercial disputes, especially in times of supply-chain disruption. In "Latin American arbitration in transition," our team outlines the past and present of commercial arbitration in Latin America, and its prospects for the future.

Latin America has experienced many sovereign debt defaults over the past century. The most recent installment of these usually long-brewing crises played out as COVID-19 partly disabled the region, involving Ecuador, Argentina, Belize and Suriname. Meanwhile, Venezuela continues mired in default for more than three years as of the time of publication. In the article "Sovereign debt restructurings in Latin America: A new chapter," our team explores some of the lessons learned and innovations employed in these recent sovereign debt restructuring exercises, providing insights into the implications for the future of sovereign and sub-sovereign international finance and, more broadly, cross-border restructurings, in the region.

With the COP26 conference being held in Glasgow in November 2021 and concerns about climate change at an all-time high, it is unsurprising that environmental, social and governance (ESG) trends are a recurring sub-theme through several of the articles in this inaugural edition of Latin America Focus. In "Sustainable finance in Latin America," our team focuses directly on green, social and sustainability-linked (GSS) bonds. This article also covers other kinds of sustainable finance, and international environmental agreements in this area to which Latin American countries are signatories.

Our world is being transformed by what the World Economic Forum calls the 4th Industrial Revolution, and Latin America is no exception. Over the next few years, the region is expected to experience faster growth in interconnection bandwidth capacity than any other region in the world. This is especially important for Latin America given the role that connectivity and digital capacity play in driving inclusive economic growth and prosperity. In "Bridging Latin America's digital divide," our team takes a detailed look at investments in digital infrastructure across the region. We focus especially on mobile networks (including 5G), data centers and sub-sea cables, exploring also how these investments are being (and might be) funded.

Latin American equity markets proved remarkably resilient to COVID-19, in terms both of growth in their major indexes and in new initial public offerings (IPOs), and other stock and rights issuances. Brazil, in particular, saw a large number of new publicly listed companies emerge in 2020 – 2021. "Equity capital markets in Latin America" provides a current overview of the state of equity capital markets in Latin America, emphasizing key growth opportunities.

Finally, the first half of 2020 saw a sharp contraction in M&A in Latin America, but deal flow has rebounded strongly in 2021. In "M&A in post-COVID-19 Latin America," our team explores some of the factors that international investors need to take into account when investing in the region's growing markets in view of the current environment. Data drawn from White & Case's global M&A Explorer tool is used to show current trends among various cross-sections of deals.

We do hope that you enjoy reading these insights, and find them valuable. Please do not hesitate to let me know if there are any topics that you would like us to cover in future editions.

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

Sovereign debt restructuring solutions developed in Latin America during 2020 and 2021 create a new paradigm for sovereign debt restructurings in the region and globally

GSS bonds and other forms of sustainable finance have become a mainstream feature of Latin American debt capital markets

COVID-19 has created strong incentives for investment in digital infrastructure in Latin America, especially in 5G, private networks, data centers and fiberoptic cables

Strong pandemic-era performance and a look around the corner

Established trends driving M&A globally are also reflected in Latin American deal flow

COVID-19 has created strong incentives for investment in digital infrastructure in Latin America, especially in 5G, private networks, data centers and fiberoptic cables

Stay current on your favorite topics

In Latin America and the Caribbean, adopting digital solutions has been promoted as a unique opportunity to increase productivity and unlock solutions to sustainable development goals.

While the headline-grabbing responses to COVID-19 in emerging markets have been the production and dissemination of accessible and affordable vaccines,1 the post-pandemic reality of increased remote working and importance of virtual connectivity has prompted and accelerated investments in digital infrastructure. In Latin America and the Caribbean (LAC), following the coronavirus pandemic in particular, adopting digital solutions has been promoted as a unique opportunity to increase productivity and unlock solutions to sustainable development goals by facilitating access to finance, education and health.2 Notable examples such as Brazil's Clinical Telemonitoring Center, which provides integrated digital health services to facilitate the tracking of COVID-19, and Jamaica's digital platform for climate risk management developed by the Caribbean Climate Innovation Center illustrate the unique role digital technologies can play in tackling development needs. The World Bank estimates the digital economy is equivalent to 15.5 percent of global gross domestic product (GDP), growing two-and-a-half times faster than global GDP over the past 15 years, and that in certain emerging markets a 10 percent increase in mobile internet penetration may translate to a 2.5 percent increase in GDP.3

Considerable investments are needed, though, to build the infrastructure necessary in LAC to enable faster and more affordable access to mobile services and the internet. Government and multilateral efforts in the region have focused on connecting the unconnected, especially in rural areas, and improving data access through investments in backhaul infrastructure such as optical fiber. This article examines the particular challenges for financing digital infrastructure in LAC and the current key trends and opportunities for investment and financing.

The LAC region is not unique in facing supply-and-demand-side constraints to digital transformation. As of 2019, just under half of the world's population was still without internet access, the vast majority concentrated in emerging markets and principally in rural areas. This digital divide is particularly stark in LAC, however. A handful of countries such as Chile, Uruguay, the Dominican Republic and Costa Rica have more than 90 subscriptions per 100 inhabitants for mobile broadband, while the majority of Latin American countries are around 50 to 77 per 100 inhabitants and as low as 20 per 100 inhabitants in countries such as Cuba, Nicaragua and Guatemala. This divide is even more pronounced for fixed broadband connectivity.4

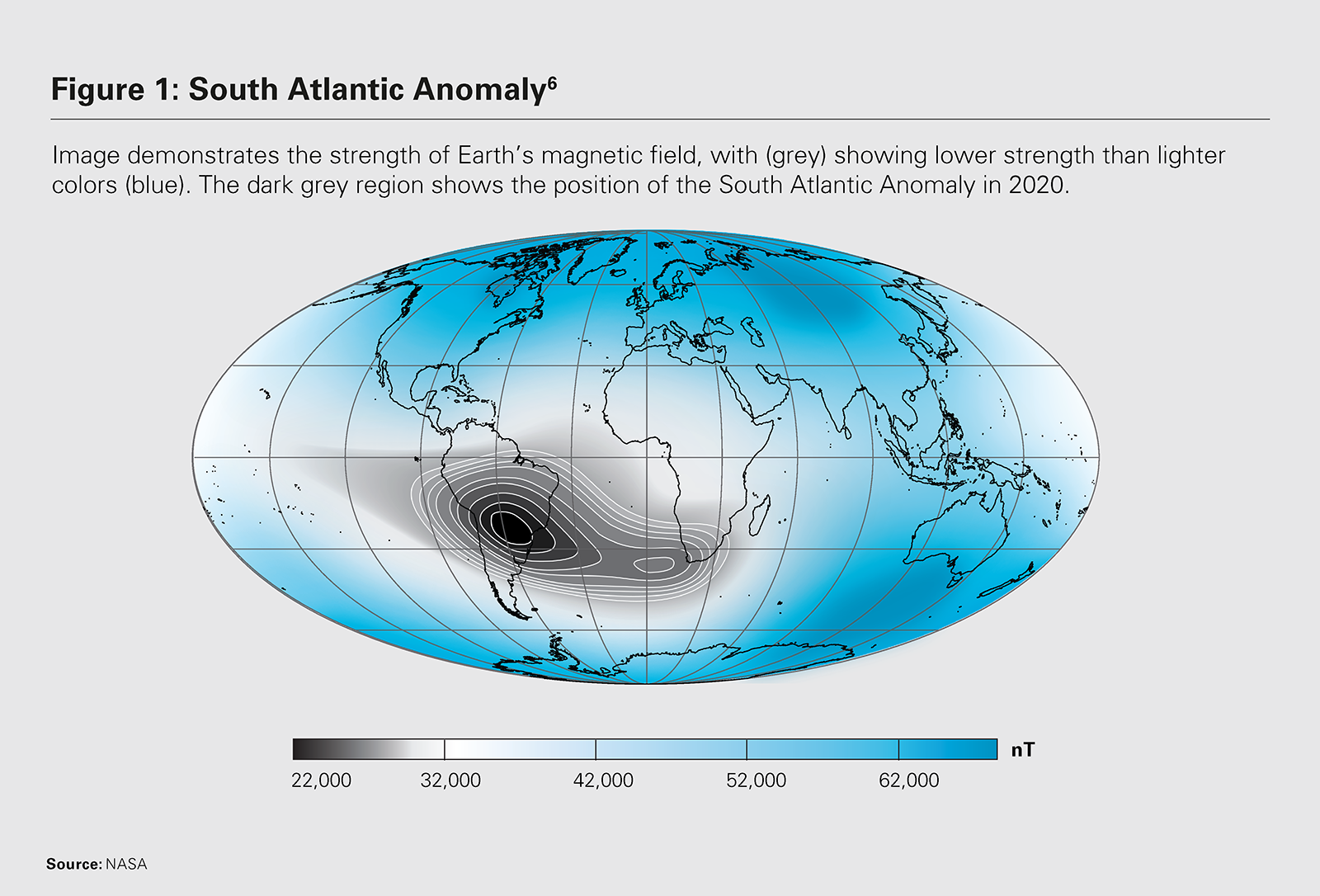

Several countries in LAC do not currently possess the necessary tools and environments to bridge the digital divide. Investment in basic, standard and advanced information and communication technology (ICT) skills is especially crucial. Such skills are severely lacking in most LAC countries, Chile being a notable exception. Cybersecurity skills are similarly in short supply, with the absence of regulatory frameworks posing additional constraints. Broadband connections in rural areas are a particular challenge, and one that cannot be easily addressed through deploying geostationary satellites due to the so-called "South Atlantic Anomaly." As an unusually weak spot in the Earth's magnetic field, which doses orbiting satellites with high levels of radiation, degrading their electronic components,5 this affects much of southern Latin America (see figure 1). Expanding connectivity into rural areas through fixed infrastructure (fiber or copper) requires high upfront capital costs, especially where challenging geographical terrains are involved (e.g., the Andean mountains, rainforests), while expanding mobile connectivity requires awarding and managing more spectrum. While most network operators in LAC were able to cope with the increased demand on their networks during the COVID-19 pandemic, these infrastructure gaps will hamper digital integration and accessibility in the region in the long-term if not addressed through large and sustained investments from private and public sector players.

As the so-called 4th Industrial Revolution unfolds, digital infrastructure will fundamentally enable and drive economic growth and productivity in all regions across the globe.

Paradoxically, the realities of the post-COVID-19 environment have created strong incentives to accelerate investment in digitalization efforts. While LAC is one of the smallest regions, it is expected to have the fastest growth of interconnection bandwidth capacity anywhere in the world. By the end of 2021, the region expects a compound annual growth rate of 59 percent, which would mean more than 755 terabits per second (Tbps) of installed capacity (from a current level of 118 Tbps), though this will be largely concentrated in São Paulo, Rio de Janeiro, Buenos Aires and Mexico City.7 It is estimated that operators in Latin America will invest more than US$70 billion in capex between 2021 and 2025, of which the lion's share will be 5G-specific.8 According to a study published in 2020 by IDC Latin America, 40 percent of the region's GDP will consist of digital businesses by 2022. This will require IT spending of up to US$460 billion. Of this total, 35 percent will be invested in cloud computing solutions. Four main regional trends appear to be driving investments in this space:

20 billion

The "Internet of Things" could be made up of 20 billion devices or more worldwide by 2022—more than three objects per person

OECD

The majority of investments in the digital infrastructure space have been private, and this is likely to continue to be so. In addition, it seems highly likely that they will, increasingly, involve commercial or development bank financing. The high upfront costs of constructing large capital assets such as data centers, combined with long-term revenue streams, could lend themselves to potentially limited or non-recourse financing structures, or a hybrid of those with leverage or real estate financing principles, depending on the type of lender involved.10

To date, however, most digital infrastructure projects have tended to be on a corporate or lease finance basis. Cable projects, for instance, have tended to be developed and financed by sponsors bringing their own debt financing on their balance sheet or an equity issuance. For instance, the US$461 million expansion of the Brazilian telecom Oi's fiber-optic network, which closed in April 2021, was funded through a private placement of convertible bonds. Cable companies typically contract for long-term capacity commitments or "indefeasible rights of use" (IRU). As this results in a lump-sum up-front payment for a right to use part of the capacity on the cable along with operation and maintenance payments over time, the need for long-term financing has been minimal. Further, cable companies tend to not fully contract cable capacity to maximize revenue streams, leaving the project exposed to merchant risk. For large intercontinental subsea cable projects in particular, the challenges inherent in securing the necessary rights to the cable's route across multiple jurisdictions, combined with the long-term risks of competitors or technological advancements (accentuated when the cable is not fully contracted with long-term commitments) typically deter project finance approaches.

Similarly, limited recourse or non-recourse financings for data centers in Latin America have yet to be seen on a major scale. In general, Latin American data centers are owned or developed by large investors such as Google, Oracle and HP. These companies tend to invest equity instead of approaching debt markets for funding. Nevertheless, encouraging signs exist that debt financing may become more prominent. The most recent deal to have closed in July 2021, the €320 million financing of Asterion Industrial Partners' data center business Nabiax, which owns a network of data centers in Spain and Latin America, was one of the first environmental, social and governance (ESG-linked) project financings in the sector, albeit with short (five-year) tenors on its term, capex and revolving credit facilities. Earlier in 2021, Odata, which is majority-owned by Brazilian private equity firm Patria Investments, received a US$30 million loan from the International Finance Corporation (IFC) to expand its colocation data center operations in Brazil and Colombia, though this was based on the balance sheet of the company. Significantly, this was the first-ever data center financing by the IFC, and upcoming projects in LAC and other emerging markets suggest that IFC and other agencies will be stepping up financing in this space in the near term.

The need for more structured financing solutions may grow as digital infrastructure assets necessitate large capital expenditures. Due to the high cost involved in the construction and operation of mega-data centers, the importance of deploying capital more efficiently may encourage a shift toward alternative funding sources. There is a growing demand for prefabricated data centers as they reduce the time between design and implementation by several months, which improves the return on investment of these projects. In Latin America, Brazil has become a regional export center for prefabricated data centers, including their design, assembly and testing. Financing prefabrication manufacturing facilities or exports could become an important growth area as the demand for data centers increases.

Further, the expansion of colocation data centers and competitive pricing of services depends increasingly on the optimization of energy consumption, which can account for up to 40 percent or more of a data center's operating expenses. Investment in advanced critical infrastructure and thermal systems (e.g., evaporative coolers and solutions that use water or air cooling) are increasingly adopted by colocation data centers in Brazil, Chile and Colombia, and may create opportunities for green financing techniques. For instance, the Nabiax project financing mentioned above linked pricing to the achievement of specific ESG targets, whereby an increased use of renewable electricity, reduced water consumption per megawatt, and hiring of more women would result in a lower interest rate (and conversely, penalties if such goals were not met).

As the so-called 4th Industrial Revolution unfolds, digital infrastructure will fundamentally enable and drive economic growth and productivity in all regions across the globe. Digital transformation can only be fully realized if high-quality access to communication networks and services is made available at affordable prices. The importance of these investments into digital infrastructure in Latin America and the Caribbean therefore cannot be overstated. Their impact on the growth of Latin American and Caribbean economies and on the livelihood of their people will be felt in years to come across all industry sectors. It will also be essential for ensuring that the LAC region does not fall behind in the "Internet of Things" (IoT), which is poised to transform the way in which data drives economies and societies. According to the OECD, the IoT could be made up of 20 billion devices or more worldwide by 2022—more than three objects per person. Without the necessary infrastructure being installed at scale, these transformational trends could make bridging the digital divide even harder to achieve in the future.

1 https://www.whitecase.com/news/press-release/white-case-advises-ifc-deg-proparco-and-dfc-funding-eu600-million-african-covid.

2 Antonio García Zaballos, Enrique Iglesias and Alejandro Adamowicz Rodríguez (2019), The Impact of Digital Infrastructure on the Sustainable Development Goals: A Study for Selected Latin American and Caribbean Countries, Washington, DC: Inter-American Development Bank, available at: https://publications.iadb.org/publications/english/document/The_Impact_of_Digital_Infrastructure_on_the_Sustainable_Development_Goals_A_Study_for_Selected_Latin_American_and_Caribbean_Countries_en_en.pdf.

3 https://www.worldbank.org/en/topic/digitaldevelopment/overview.

4 ITU (2021), Digital Trends in the Americas Region 2021, available at: https://www.itu.int/en/myitu/Publications/2021/04/26/09/33/Digital-trends-in-the-Americas-region-2021.

5 Doug Adler (2021), The Spacecraft-Killing Anomaly Over the South Atlantic, available at: https://astronomy.com/news/2021/02/hidden-spaceflight-danger-the-south-atlantic-anomaly

6 Ibid.

7 Global Interconnection Index (GXI) Volume 4, available at: https://www.equinix.com/gxi-report.

8 GSMA (2020), The Mobile Economy Latin America, available at: https://www.gsma.com/mobileeconomy/latam/.

9 Equinix (2021), Beyond COVID-19: Digital Transformation Trends in the Wake of the Pandemic [Equinix 2020-21 Global Tech Trends Survey], available at: https://www.equinix.com/resources/infopapers/equinix-tech-trends-survey.

10 https://www.whitecase.com/publications/alert/cloud-rise-data-center-financings.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: South Atlantic Anomaly (PDF)

View full image: South Atlantic Anomaly (PDF)