What will drive issuance in a post-COVID-19 world?

Foreword

Halfway through 2021, we take stock of leveraged finance in the United States and consider the road ahead for both borrowers and lenders. After more than a year of COVID-19, are things returning to normal? Or are we just starting a whole new journey?

In many ways, COVID-19 had far less of an impact on leveraged finance markets than expected. Activity dropped in the second quarter of 2020, primarily in leveraged loan issuance, but a year later numbers returned to pre-pandemic levels. In fact, leveraged loan and high yield bond values reached record highs by the end of Q1 2021—the highest quarter since Q2 2018 and the second-highest quarter, respectively, on Debtwire Par record going back to 2015.

What drove this relatively high-speed recovery? First, the Coronavirus Aid, Relief and Economic Security (CARES) Act, signed into law in March 2020, protected many businesses from the full brunt of the pandemic. At the same time, many businesses shored up their finances, taking on debt to ensure liquidity as lockdown measures continued to have an impact through the second half of 2020. Issuances rose and that upward trajectory carried on into 2021.

By the end of Q1 2021, the picture had changed once again. Vaccines were being distributed quickly and efficiently, raising hopes for a post-COVID-19 future. The economy was also improving, as various states began to open up and a year of pent-up consumer demand was released. By May, core retail sales in the US had reached levels typically only seen over the Christmas period, according to the National Retail Federation. An air of optimism crept into the market, with lenders increasingly willing to take more risks on borrowers in their pursuit of yield. Financing earmarked for M&A and buyout activity also began to climb, hinting at growth plans for the months ahead. Perhaps most significantly, the low interest rate environment gave businesses an opportunity to reprice and refinance their maturing debt in droves.

What's next for 2021?

While these are all very positive signs for lenders in the leveraged finance space, there are still a few red flags on the horizon. First is inflation—in July, the Bureau of Labor Statistics reported that the US consumer price index had climbed 5.4 percent in the 12 months to June, a level not seen in 13 years. These growing inflationary pressures are part of the rush to reprice and refinance existing debt, as businesses try to avoid any unpleasant surprises if interest rates begin to climb as well.

Second, companies in robust sectors that enjoyed a degree of preferential treatment from lenders during the pandemic may find that sentiment shifting in the months ahead as other sectors begin to recover. The "flight to quality" witnessed in the early days of the pandemic will likely return to a more evenly balanced state of affairs. Documentation may also go through some changes in the coming months, as adjustments brought in during COVID-19 are phased out.

Finally, as the dust settles in debt markets, issues that were gaining ground before the pandemic will return in force, especially environmental, social and governance factors, which continue to take on increasing importance among borrowers and lenders alike.

All of which means the road ahead is not quite as clear as many would like, but there will be fewer obstacles blocking the path.

The US leveraged finance story so far

Leveraged loan issuance reached US$763.5 billion in the first half of 2021, up 60 percent from US$478.1 billion in the same period in 2020

High yield bond market issuance also rose 22 percent year-on-year, from US$219.6 billion to US$267.1 billion

Refinancings and repricing deals accounted for 62 percent of overall loan issuance in H1 2021

How distressed companies are avoiding full-blown bankruptcies

Announced US corporate bankruptcies climbed to 630 cases in 2020, according to Standard & Poor's—up from 2019 levels, but still lower than expected

Bankruptcies ticked higher early in 2021—from 14 cases in January to 23 cases in March, before dropping to 11 in June—but are still well below 2020 levels according to Debtwire Par

Covenant relief and uptiering, as well as drop down deals and other liability management structures have offered companies a variety of levers to pull to avoid entering bankruptcy situations

Refinancing, repricing, M&A and buyout activity all surged in the early months of 2021, but then lenders shifted gears in pursuit of yield and borrowers realized they could tap the market for more than just liquidity. Where will this fork in the road lead for the rest of 2021?

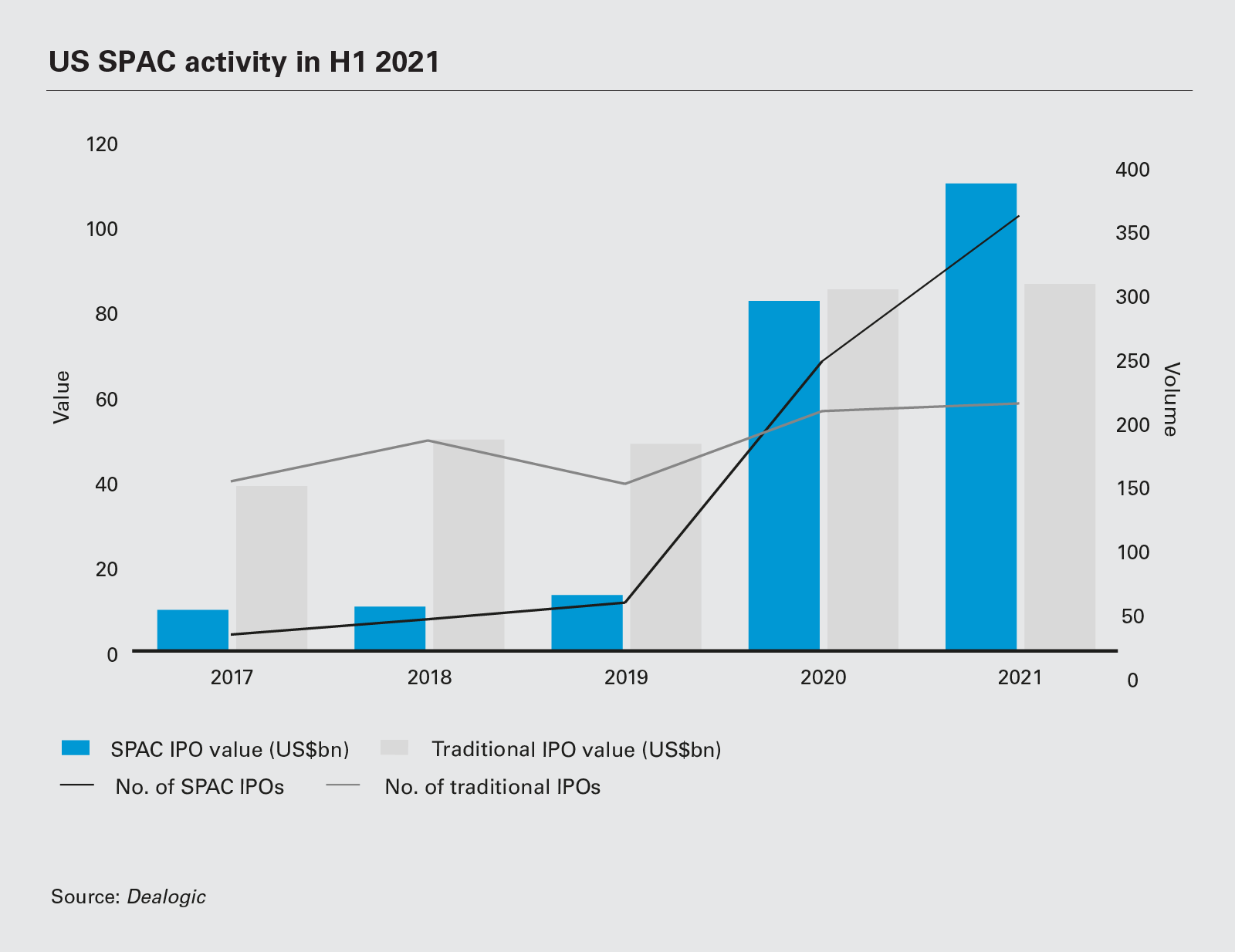

248 SPACs listed in 2020, raising US$82.6 billion—a more than six-fold rise on 2019 issuance

362 SPAC vehicles raised US$110.2 billion in H1 2021

176 M&A deals worth more than US$386.1 billion have been completed via SPACs in H1 2021

176M&A deals worth more than US$386.1 billion were completed via SPACs in H1 2021

Special purpose acquisition companies (SPACs) continued to top fundraising records through the first half of 2021 despite the market's pause for breath after Q1 2021.

After cresting at an all-time high of US$82.6 billion in 2020, global investor appetite for SPACs—blank check companies that raise equity on stock markets to invest in M&A transactions—showed no sign of slowing in 2021. By May of this year, the market had already surpassed last year's record, with 330 SPAC vehicles raising US$103.8 billion, according to Dealogic.

And while some of the heat has left the SPAC market recently—shares in some SPACs have fallen post-acquisition in recent weeks, as retail investors and institutions have traded out—the vast overhang of capital that has already been raised and is ready for deployment over the next two years will continue to generate deal flow for lenders and other M&A market participants through the rest of 2021.

The unprecedented levels of SPAC fundraising have already sparked a corresponding uplift in M&A activity involving SPACs. These vehicles typically have 24 months to either consummate an M&A transaction (known as a "de-SPAC," where the acquisition target merges into the SPAC to become the listed company) or return capital to investors. The market has already seen a wave of de-SPACs this year, with Dealogic recording 176 such deals worth in excess of US$386.1 billion.

Even with this rate of dealmaking, these de-SPAC deals trail the pace of new SPAC IPOs announced in Q1 2021, meaning there are many SPACs still seeking targets. This sets the stage for sustained high levels of dealmaking from SPACs through the rest of the year, with these vehicles being used more aggressively and pursuing deals quickly. According to PitchBook, the median time gap between a SPAC IPO and a de-SPAC reverse merger in 2020 was only seven-and-a-half months.

For debt markets, this wave of activity has opened up windows for companies to pay down debt. SPACs are also targeting ever-bigger deals which, in time, could see SPACs start to tap debt markets more actively to secure the financing needed to reach higher valuations.

In most SPAC deals in the market so far, however, companies have moved to either refinance or pay down debt, especially when the vendor is a PE firm that has used leverage in previous deal structures.

In many cases, Standard & Poor's has issued improved ratings or ratings outlooks for companies that have done deals with SPACs and reduced their leverage multiples post-transaction.

For example, the ratings agency lifted the credit outlook on hardware and home improvement company Hillman Cos from B-/CreditWatch stable to B-/Positive after the business reduced its leverage multiple from 8x to 4.5x following a SPAC deal.

Whole Earth Brands, meanwhile, saw its credit rating improve from CCC/Negative to B/Positive after post-SPAC deal debt reduction. Advantage Sales & Marketing, a marketing agency backed by buyout firms Bain Capital, CVC and Leonard Green & Partners, shifted from a CCC/Negative rating and outlook to B/Stable following a US$5.2 billion deal that reduced its leverage multiple from 7.3x to 4.9x.

SPAC deals have also allowed certain acquisition targets to take the opportunity to enter into new credit facilities, sometimes on improved terms.

After the announced acquisition by the Conyers Park II Acquisition Corp SPAC, for example, Advantage Sales & Marketing lined up new senior secured credit facilities comprising a US$2.1 billion term loan facility and a US$400 million asset-based credit revolver.

In another example, the acquisition of Platinum PE-backed data center cooling equipment manufacturer Vertiv by the GS Acquisition Holdings Corp SPAC—sponsored by Goldman Sachs and run by former Honeywell chief executive David Cote—saw Vertiv raise a US$2.2 billion term loan to refinance its existing term loan and high yield bonds. The new term loan was priced at LIBOR +3 percent—a margin 1 percent lower than that of its previous term loan.

Larger SPAC targets keep lenders in the mix

Although de-SPAC transactions see target companies take on public company listings, which usually infer lower debt multiples than in private market deals, the sheer volume of activity by SPAC sponsors, coupled with the fact that SPACs are aiming at ever larger target companies, could see lending markets play an increasingly important role in supplying financing to help SPACs reach target company valuations.

According to PitchBook, the size of target companies is expanding relative to the size of the SPAC after its IPO, reaching an average of 5.3x early in 2021. At the extreme end of the scale, there are cases like Grab, the Singapore-based Southeast Asian ride hailing app, which achieved a US$39.6 billion valuation after agreeing to a merger with Altimeter Growth Corp, a Nasdaq-listed SPAC. Altimeter Growth Corp only raised US$450 million when it listed as a SPAC.

To date, SPAC sponsors have primarily opted to bridge the gap to company valuations through private investment in public equity (PIPE) deals, where private investors club together to fund deals in companies about to go public. In the case of the Grab investment, for example, asset managers BlackRock, Fidelity and T. Rowe Price, along with Morgan Stanley's Counterpoint Global fund and Singaporean sovereign wealth fund Temasek, put together a US$4 billion PIPE to support the SPAC deal for Grab.

But as SPAC deal sizes increase, PIPEs could prove insufficient to bridge the gap to valuations alone—rollover equity as well as debt may be required.

Debt could also be increasingly used in SPAC deals to refinance a target's existing borrowings, top up balance sheets, cover fee costs or make distributions to shareholders.

Software company E2Open, for example, agreed to a US$2.5 billion SPAC merger and then went to market to raise a US$525 million term loan B and a US$75 million revolver for these purposes, according to S&P.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image 'US SPAC activity in H1 2021' PDF

View full image 'US SPAC activity in H1 2021' PDF