Our ninth edition of Africa Focus shows Africa embarking on a period of unprecedented growth and opportunity.

We open this issue with a closer look at Article 6 of the Paris Agreement, which holds much promise for the African continent. Article 6 allows countries to voluntarily cooperate with each other to achieve emission reduction targets set out in their nationally defined contributions. The COP26 negotiations in Glasgow led to a set of agreed rules to help put Article 6 into practice. COP27 reaffirmed the previously agreed principles of Article 6, but sadly, challenges in reaching agreement on some contentious issues led to part of this being deferred to COP28 in 2023. The relevance of the Article 6 to community-based agriculture—an area of particular importance in Africa—is highlighted by our guest contributor, Dan Collison, Chief Executive of Farm Africa.

Natural synergies between the Middle East and Africa—geographic proximity, well-developed logistical networks and close political and economic ties—are key features in this edition. We ask the question, "Can the Middle East—with its vast capital and a booming Islamic finance market—provide the much-needed boost to the underserviced Muslim population in Africa?" Focusing on the Gulf Cooperation Council states of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates, we explore the growing investment and trade flows between the GCC states and Africa. Recent years have seen these ties expand south to include sub-Saharan Africa, and from an almost exclusive focus on oil and petrochemical-related products to a broad spectrum of other sectors.

Cross-border investors are always sensitive to the risk of wrongful conduct that the state hosting their investments, and that state’s organs, can inflict upon them. Many African countries have vowed to promote and protect foreign investments, and have taken steps to modify the investor-state dispute settlement system. One of our articles explores the current state of investment treaties in Africa and efforts to protect foreign investments in Africa as well as African investments abroad.

In many ways, Africa has emerged as a pioneer in financial services—a good market in which to do business and realize profits—beyond just the development projects. The way its people move money around the continent on their mobile phones is far ahead of even the more developed markets. Africa has long been of interest to private equity investors, and rounding off the range of topics covered in this edition, we have an interview with Bryce Fort, Chief Executive Officer of Emerging Capital Partners, who was the driving force behind the recent listing of IHS Towers, an African mobile telecommunications company, on NYSE. The interview explores current developments in private equity in Africa.

We hope that you will find the new edition of Africa Focus a thought-provoking read.

Africa has emerged as a pioneer in financial services—a good market in which to do business and realize profits—beyond just the development projects

Article 6 of the Paris Agreement: Opportunities for Africa

The possibility of climate markets has finally materialized into the draft stage at COP27, but many crucial decisions that would allow for carbon trading to begin in earnest were deferred to COP28.

Investment treaty protection: How to safeguard foreign investments in Africa

Prudent African investors—and investors within Africa—can ensure that their foreign investments are protected from wrongful conduct that the state and its organs can inflict.

Africa's coming of age: An interview with Bryce Fort

Bryce Fort, Managing Director and Founding Partner of Emerging Capital Partners (ECP) shares his insights on the current state of private equity funds in Africa.

Africa and the Gulf States herald a new era in trade and investment relations

Strong diplomatic and economic ties have long existed between the Gulf Cooperation Council (GCC) states and North Africa but there are other levers at play for deepening economic relations.

Credit where credit's due: Who's benefiting from the voluntary carbon market?

Projects that protect and restore the environment improve carbon storage and strengthen the livelihoods of smallholder farmers, says Dan Collison, Chief Executive of Farm Africa.

Investment treaty protection: How to safeguard foreign investments in Africa

Prudent African investors—and investors within Africa—can ensure that their foreign investments are protected from wrongful conduct that the state and its organs can inflict.

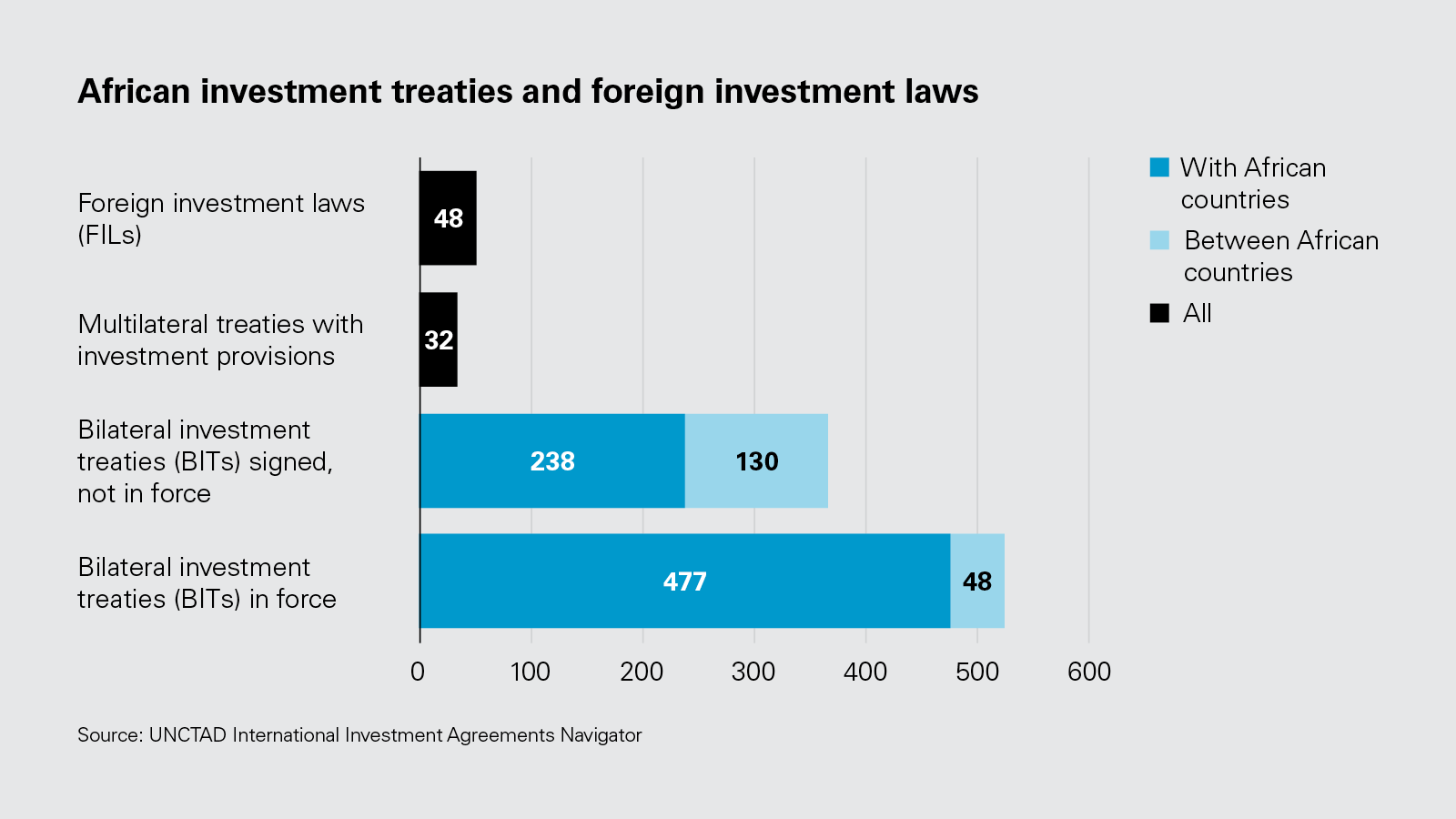

The influx of foreign direct investment into Africa has been reaching new highs, with tens of billions of US dollars pouring into various African countries every year and reaching a record high with US$83 billion invested in 2021. More is yet to come, with US$2.5 trillion worth of infrastructure projects estimated to be completed by 2025—and much of it will come from foreign investors. Many African countries have vowed to promote and protect such foreign investments. Indeed, the proliferation of bilateral investment treaties (BITs), other treaties with investment provisions and foreign investment laws (FILs) in Africa, along with the parallel rise in numbers of claims brought by African investors and claims brought against African states under such instruments, show that investment protection is an important consideration. At the same time, various African states have been revamping the system in recent years to emphasize the states' policy objectives.

As of October 2022, there were 525 Bilateral Investment Treaties (BITs) with African countries

Source: Market data

US$2.5tn

Value of infrastructure projects estimated to be completed in Africa by 2025

Source: McKinsey & Co

Efforts in Africa to protect foreign investments and investments of African investors abroad are across-the-board, covering the international, regional and domestic levels. At the core of the system are investment treaties concluded between two or more states that set out a number of protections in favor of foreign investors and their investments. If the state violates these protections, the investor can bring claims directly against the host state where its investment is located, typically before an international arbitration tribunal. Foreign investor protections may also be available in the host state's FIL or in an investment contract concluded between the foreign investor and the state.

As of October 2022, there were 525 BITs with African countries—including almost 50 intra-African BITs—in force, alongside more than 30 multilateral treaties with investment protections, including the COMESA (Common Market for Eastern and Southern Africa) Treaty (1993); the OIC (Organisation of Islamic Cooperation) Investment Agreement (1981); the Economic Community of the Western African States (ECOWAS) Supplementary Act for Common Investment Rules for the Community (2008) and the Common Investment Code (2019); as well as the Arab League of States' Arab Investment Agreement (1980). The extensive realm of investment protection also includes domestic FILs, which were adopted by almost 50 African states. It also covers non-binding instruments such as model BITs and the Pan-African Investment Code. Negotiations for the Investment Protocol of the African Continental Free Trade Area are currently underway. If adopted, it will be the first binding investment agreement at the continental level.

Who is eligible for protection?

To qualify for investment treaty protection, an "investor" must be a national—a physical or legal person—of a state other than the host state (the other contracting state). While this assessment is fairly straightforward for natural persons, it may be more cumbersome for legal persons, such as companies, in particular if, in addition to the place of incorporation, the treaty imposes further conditions, such as having substantial business activities.

As for "investments," treaties typically encompass "all kinds of assets" and include open catalogues of assets that are covered, including, e.g., shares, real estate property, concessions, claims to money and copyrights, among other things. To determine whether an investment was made, some investment tribunals also consider whether the investor has made a contribution of money/assets having a certain risk and duration to the host state's economy.

When there is no suitable investment treaty between the foreign investor's state of incorporation and the host state, some investors choose to (re-)structure their investments to ensure a sufficient level of investment protection. This is often done by inserting an entity established in a state that has an investment treaty in force with the host state into the ownership structure of the investment. While investment planning—such as tax optimization—is a legitimate tool, the timing of the (re-)structuring is key: Some tribunals have dismissed investment claims where the restructuring—presumably to gain protection under a treaty—has been carried out after a dispute with the state has arisen or become reasonably foreseeable.

What if the state violates its obligations under investment treaties?

Many African countries have vowed to promote and protect foreign investments

Under investment treaties, states assume a number of obligations toward such qualifying foreign investors and their investments. These typically are, e.g., to protect investments from unlawful expropriation and to ensure fair and equitable treatment, full protection and security and non-discriminatory treatment. If a state violates its treaty obligations, the qualifying investor may bring a claim directly against the state to a forum provided for in the treaty in accordance with its investor-state dispute settlement (ISDS) mechanisms.

Some investment treaties require that, as the first step to resolve any investor-state dispute and before turning to arbitration, an aggrieved investor send a notice of dispute to the state and attempt to resolve its dispute amicably. If there is no resolution within a prescribed time, often three to 12 months, the investor will typically be entitled to commence arbitration.

The arbitration forum and rules depend on a particular treaty, with African BITs often referring to ICSID (the International Centre for the Settlement of Investment Disputes) or UNCITRAL (the United Nations Commission on International Trade Law) arbitration. ICSID arbitration, which is held under the auspices of the World Bank, is available with respect to states that have signed and ratified the ICSID Convention (the Convention on the Settlement of Investment Disputes between States and Nationals of Other States). The vast majority of African states are parties to the ICSID Convention, with Angola, Equatorial Guinea, Eritrea, Libya, South Africa and Western Sahara being notable exceptions.

Once the investor initiates arbitration, typically each party to the dispute appoints one arbitrator, who then together appoint the presiding arbitrator and form a tribunal. The proceeding usually involves two rounds of written submissions submitted with witness, expert and documentary evidence, as well as a document production phase, and is followed by a hearing. On average, investor-state arbitrations last between three and four years.

If the tribunal finds the state to have violated its treaty obligations, it will issue an award in favor of the investor. The most frequent remedy for aggrieved investors is monetary damages, seeking to put the investor in the position it would have been but for the state's treaty violation. For example, in KCI v. Gabon, a Tunisian investor in the construction sector was awarded €4.3 million from Gabon for the latter's violation of the OIC Investment Agreement, a multilateral treaty with investment provisions to which a number of African states, including Tunisia and Gabon, are parties, while in Unión Fenosa Gas v. Egypt, a Spanish investor in the natural gas sector was awarded US$2.013 billion for Egypt's violation of the Egypt-Spain BIT.

Recent trends: Africa-related ISDS cases, the African efforts to revisit international investment law and growing numbers of African arbitrators in ISDS cases

Efforts in Africa to protect foreign investments and investments of African investors abroad are across-the-board, covering the international, regional and domestic levels

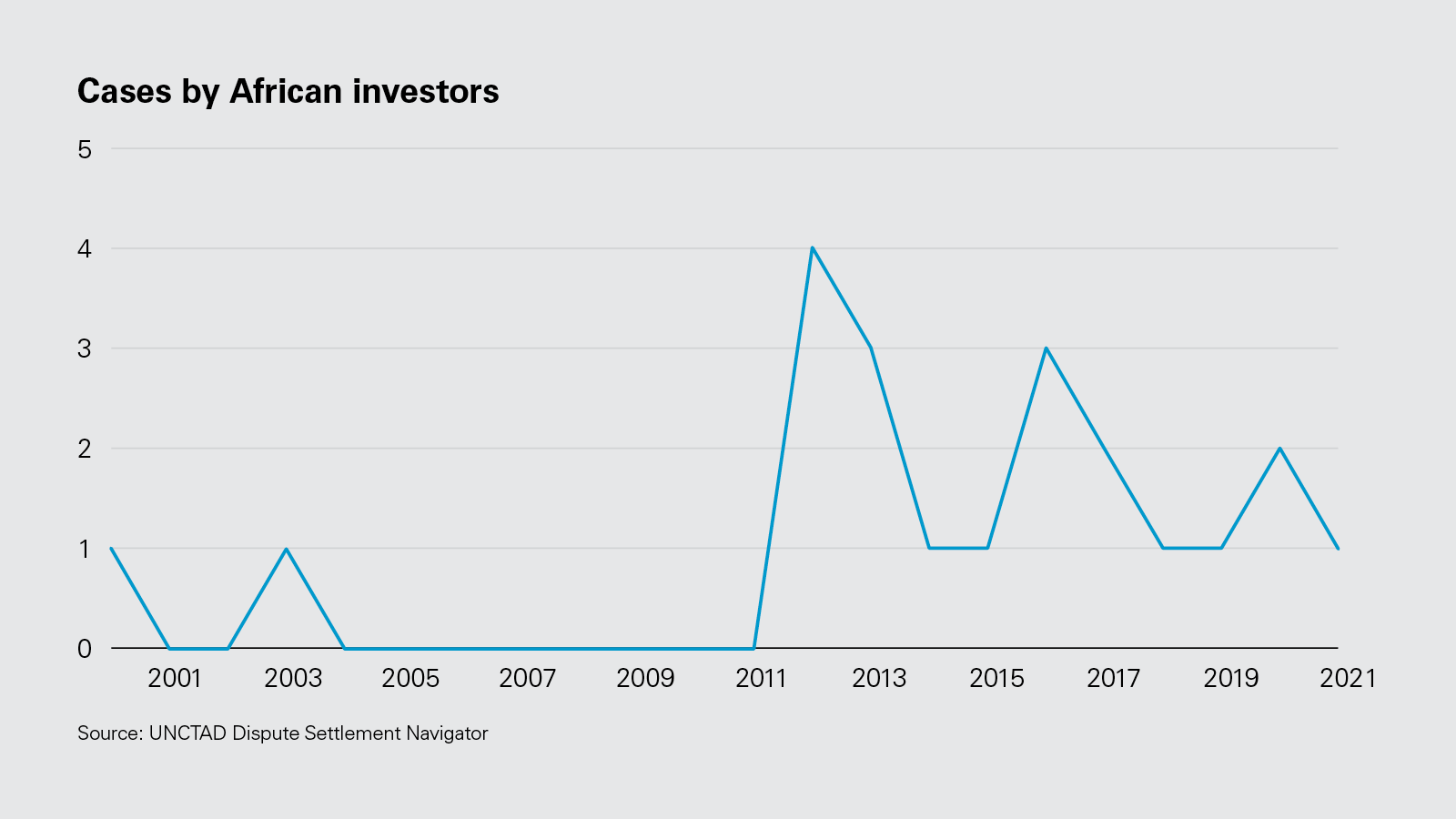

The overall number of ISDS cases were on the rise in the past two decades, with African investors having brought more than 20 cases during this time.

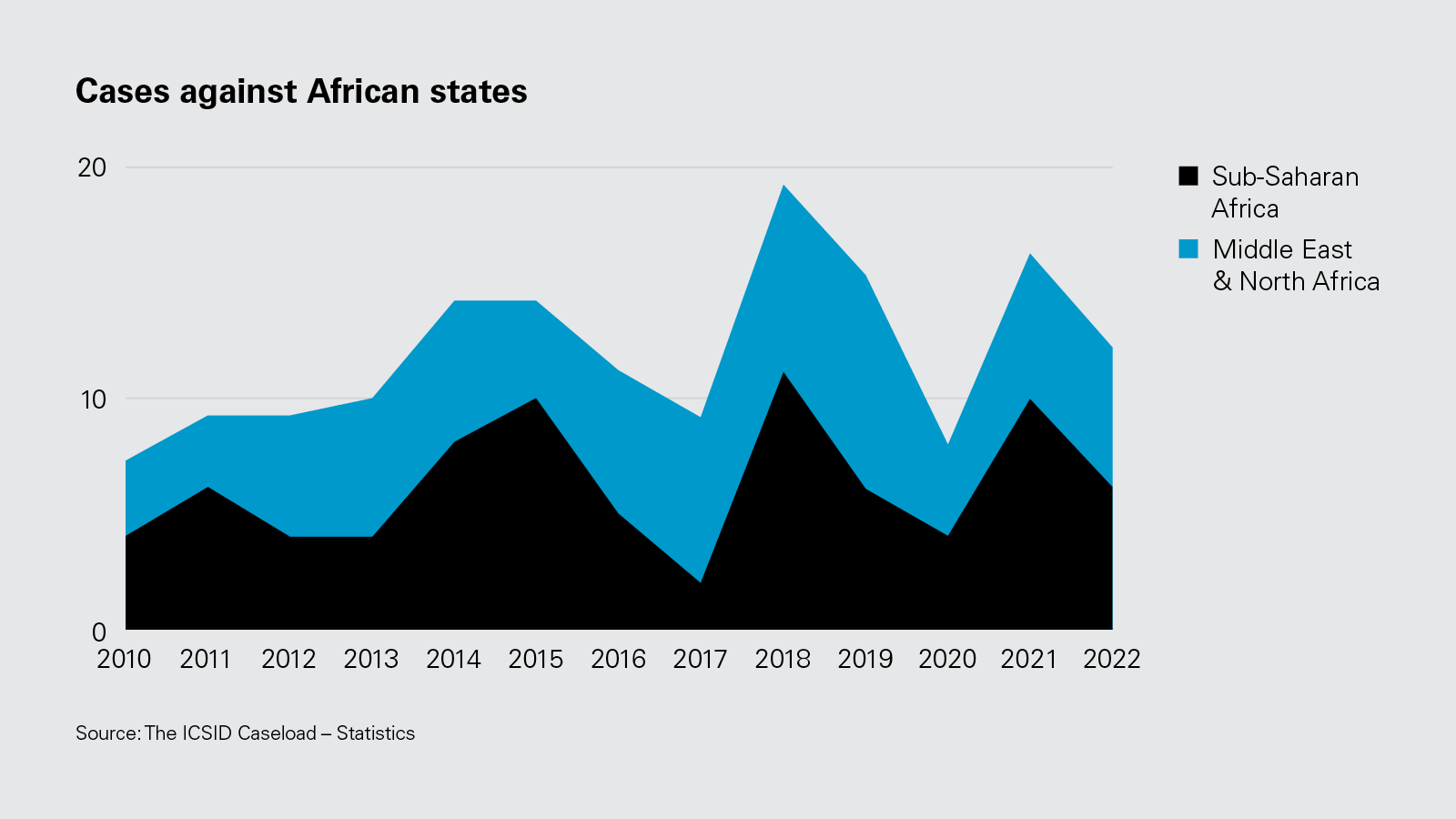

So too, however, were cases brought against African states, with 12 such cases registered by ICSID in the 2022 fiscal year alone. While this accounts for approximately one-quarter of cases registered by ICSID that year, it shows a significant drop from 2018 when ICSID registered almost 20 new cases against African states. Notably, two-thirds of all ISDS cases against African states were brought by investors from Europe alone.

The increasing numbers of ISDS cases have contributed to African states and institutions taking another look at the standards of protection and the ISDS mechanisms. These endeavors strive to move away from the treaties concluded in the past century and emphasize state policy objectives. For instance, on the domestic level, in 2015, South Africa (which decided more than a decade ago to terminate most of its BITs) promulgated the Protection of Investment Act, which replaces the classic fair and equitable treatment standard with "fair administrative treatment" and significantly limits access to international arbitration. On the international plane, the efforts span from emphasizing sustainability, investor obligations and protection of the host states' regulatory discretion in the newly concluded BITs; through placing direct obligations on investors, redefining investment protection standards and expressly providing for states' counterclaims in the African Union's Pan-African Investment Code, to featuring cultural attributes of African nations, including the principle of Ubuntu (translating to "human dignity and equality to any person"), and highlighting the protection of indigenous communities in the Africa Arbitration Academy 2022 model BIT for African States.

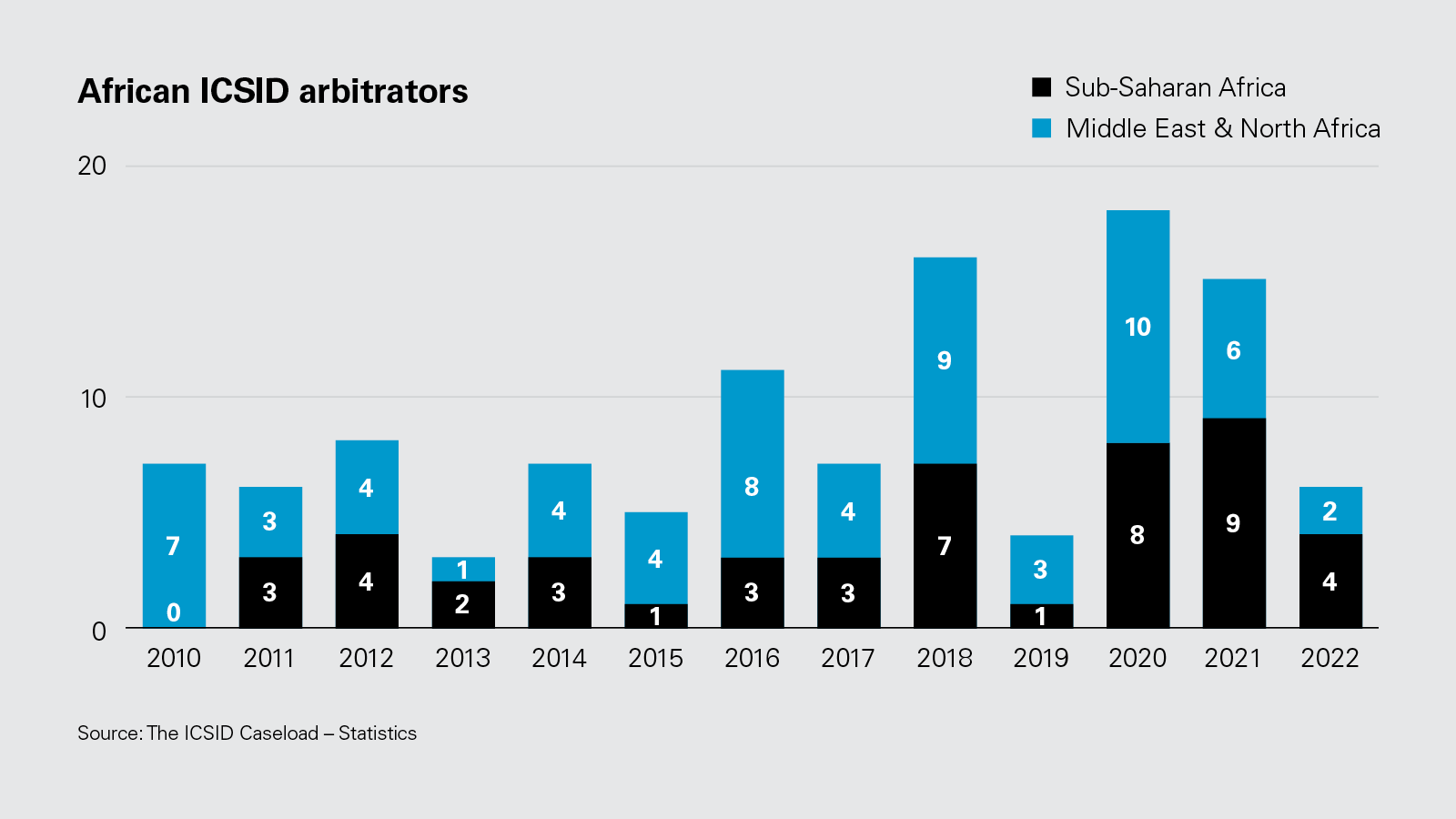

Against that background, the participation of African investors and arbitrators in ISDS has slowly increased in recent years. Over the same period, there has been a greater emphasis on diversity in arbitral appointments, as reflected in, e.g., the African Promise, an initiative launched in 2019, encouraging arbitration practitioners to sign a pledge to ensure fair representation of African arbitrators, and there are some positive indications. ICSID has reported a growing trend in the participation of African arbitrators, rising from only seven African arbitrators (and none from sub-Saharan Africa) appointed in 2010 to 18 African arbitrators, including eight from sub-Saharan Africa, appointed in 2020. Still, there is a way to go—notably, the number of African arbitrators appointed in ICSID cases has fallen to six in 2022.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: African investment treaties and foreign investment laws (PDF)

View full image: African investment treaties and foreign investment laws (PDF)

View full image: Cases by African investors (PDF)

View full image: Cases by African investors (PDF)

View full image: Cases against African states (PDF)

View full image: Cases against African states (PDF)

View full image: African ICSID arbitrators (PDF)

View full image: African ICSID arbitrators (PDF)