Financial institutions M&A: Sector trends - September 2025

Financial Services M&A: Sector Trends

We highlight the key UK and European M&A trends in H2 2024 and H1 2025, and provide our insights into the outlook for M&A going forward.

Introduction

In the 13th edition of our report, we bring you the key deal highlights and M&A trends across UK/Europe in the past 12 months which have shaped the financial services landscape. Focusing on the following verticals:

Fintech: Fragility of private and public capital fundraising markets drives consolidation activity.

Asset/Wealth Management: M&A landscape remains consistently hot—private equity drives mergers-of-equals and turbocharges trade consolidation in the last 12 months.

Payments: While Global Payments' US$24.25 billion acquisition of Worldpay from FIS and FIS's US$13.5 billion response acquisition of Global Payments' issuer solutions have dominated headlines, the sheer volume of deals in the payments space speaks for itself.

Financial Market Infrastructure: Mega private equity buy-outs shape Europe's FMI landscape—KKR seeks to emulate Blackstone's Refinitiv success through acquisition of OSTTRA.

Brokers/Corporate Finance: It's all about the people—M&A activity centres around acquiring sector expertise, client relationships and local market knowledge.

Consumer Finance: Is anyone talking about anything other than Klarna's long-awaited US equity debut?

Specialty Finance/Marketplace Lending: Complexity of deal-making has materially increased in the last 12 months. Debt, in the form of warehouses, revolvers and notes, often plays a pivotal role even in "vanilla" deals.

While Global Payments' US$24.25 billion acquisition of Worldpay from FIS and FIS's US$13.5 billion response acquisition of Global Payments' issuer solutions have dominated headlines, the sheer volume of deals in the payments space speaks for itself.

Complexity of deal-making has materially increased in the last 12 months. Debt, in the form of warehouses, revolvers and notes, often plays a pivotal role even in "vanilla" deals.

Mega hostile bids finally make a comeback: Live bids across Italy, Spain and Germany provide daily doses of excitement and intrigue.

Challenger banks deliver a steady supply of M&A activity: While statistics suggest that challengers are making inroads into banking segments occupied by established lenders, exits confirm that larger incumbents have the appetite to swallow smaller rivals. Will any challenger banks remain?

Regional consolidation fever takes hold: The numbers speak for themselves—>50 sizeable consolidation deals in the last 12 months.

It has been 5 years since Intesa / UBI Banca. Finally, the floodgates of European bank public M&A are open, accompanied by a flurry of private M&A. H2 2025 and H1 2026 will be anything but dull.

Hyder Jumabhoy

Current market

New era of deal-making

We are seeing

Big bank bearhug bonanza—unsolicited Italian bids dominate broadsheet headlines:

Italy

Banca CF+'s takeover bid for Banca Sistema (ongoing)

Monte dei Paschi di Siena's takeover bid for Mediobanca (ongoing)

Mediobanca's takeover bid for Banca Generali (aborted)

UniCredit's takeover bid for Banco BPM (aborted)

BPER Banca's takeover bid for Banca Popolare di Sondrio (successful)

Banca Ifis' takeover bid for illimity Bank (successful)

Spain

BBVA's takeover bid for Banco Sabadell (ongoing)

Germany

UniCredit's takeover bid for Commerzbank (ongoing)

United Kingdom

Shawbrook's / Pollen Street Capital's takeover approach to Metro Bank (aborted)

NatWest's takeover bid for Santander UK (aborted)

Nationwide's takeover bid for Virgin Money (successful)

Consolidation fever grips UK & European lenders, with >50 consolidation deals in the last 12 months:

Europe's systemic banks finally return to buy-side fervour (e.g., Eurobank's and Alpha Bank's respective acquisitions of Hellenic Bank and AstroBank)

Regional consolidation, as Europe-centric powerhouses triumph in competitive auction processes (e.g., VeloBank's, ABN Amro's and BAWAG's respective acquisitions of Citi Handlowy's consumer banking business, Hauck Aufhäuser Lampe and Barclays Consumer Bank Europe

High Street lenders swallow challengers (e.g., Santander's and Barclays' respective acquisitions of TSB and Tesco Bank's business)

Challengers hunt their local rivals (e.g., Coventry Building Society's and Nationwide's respective acquisitions of The Co-operative Bank and Virgin Money)

Domestic mergers, primarily across the Nordics (e.g., Fynske Bank & Nordfyns Bank, Sparebanken Norge & Oslofjord Sparebank and Sparbanken Vastra Malardalen & Sparbanken Rekarne mergers in Denmark, Norway and Sweden, respectively)

Governments lead deal-making—drawing a line under the global financial crisis:

UK: return of NatWest to non-government ownership

Ireland: return of AIB to non-government ownership

Greece: reduction of HCAP's stake in National Bank of Greece to 8.4%

Germany: reduction of Federal Republic of Germany's stake in Commerzbank to 12.11%

Netherlands: reduction of NL Financial Investments' stake in ABN Amro to 30%

Key drivers

Availability of high-quality targets:

Banks offload >40 sizeable non-core subsidiaries / operating businesses in the last 12 months— Standard Chartered clocks the highest count (e.g., disposal of Angola, Cameroon, Sierra Leone, Tanzania and The Gambia units), followed by HSBC (e.g., South African business, HSBC Assurances Vie, German custody business and Bahrain retail banking business) and then Société Générale (e.g., Société Générale Benin, British and Swiss private banking units and Société Générale Madagasikara)

Challenger banks deliver a steady supply of performing loan portfolios (e.g., Metro Bank's £2.5 billion residential mortgage and £584 million unsecured personal loan portfolio sales)

Financial sponsors cash-out (e.g., 4finance's exit from tbi Bank and 7 funds' exit from The Co-operative Bank)

Diverse buyer universe:

Hungry trade consolidators (e.g., Access Bank makes 6 acquisitions in 12 months)

Organic originators tap inorganic growth (e.g., Kaspi.kz's acquisition of Rabobank Turkey)

Private equity sees value (e.g., Balchug's and Advent's respective acquisitions of Goldman Sachs Russia and tbi Bank)

Tech acquire banking partners (e.g., Lesaka Technologies' and GSCF's respective acquisitions of Bank Zero Mutual Bank and IBM Deutschland Kreditbank)

Ultra high-net-worth / family offices with deep pockets (e.g., Alkemi's (Serhiy Tihipko) acquisition of Idea Bank Ukraina and Parasol V27's (Ruth Parasol) equity investment in Recognise Bank)

Financial market infrastructure (e.g., Boerse Stuttgart's participation in Solaris' Series G funding round), insurer (e.g., Direct's acquisition of A1 Bank) and sovereign wealthinvestors dip their toes in

Challenger / neo banks strive for growth and profitability:

Trends

Market examples

Availability of equity cheques for well-known challenger / neo banks

>10 successful equity funding rounds in the last 12 months, with Tyme, Solaris and Zopa executing the largest

Challenger / neo banks welcome debt funding

e.g., Zopa's £80 million AT1 funding round and Finora Bank's partial AT1 funding round

Multilateral development banks support newer market entrants

e.g., EBRD and IFC led TBC Uzbekistan's Series A funding round

Scaled challengers expand through acquisitions

e.g., OakNorth's acquisition of Community Unity Bank and Multitude Bank's "try before you buy" minority stake in Lea Bank

Scaled challengers expand through partnerships

e.g., Revolut's card transfers JV with Visa

Trends to watch

Precedent-setting Southern European bank M&A activity:

European Commission delivering warnings over political interference

Governments raising eyebrows to warn-off hostile bids

Legislatures reconsidering "golden power" rules

Prudential and competition regulators clashing over differing prerogatives

Softer equity capital markets necessitating dual-track exit strategies for challenger banks (e.g., delay of Klarna's announced U.S. IPO until late-2025 and termination of Redwood's reverse merger with R8 Capital)

Shareholder activism taking many and varied forms:

Ultra high-net-worth individuals encouraging deals from within shareholder ranks

Trade unions disrupting M&A activity (e.g., UGT's and Comisiones Obreras' petition to block the BBVA / Banco Sabadell merger)

Holding management to account (e.g., 56 pre-submitted questions for Société Générale's 2025 AGM focusing on matters including governance gaps and executive pay)

Pushing geopolitical agendas (e.g., pro-Palestine disruption of Barclays' 2025 AGM and anti-Russia disruption of Raiffeisen's 2025 AGM)

Pushing climate change agendas (e.g., Patience Nabukalu's CEO letter ahead of HSBC's 2025 AGM)

Our M&A forecast

Large-scale M&A activity will continue being driven by ideal celestial alignment—returning many of Europe's largest lenders into non-government hands, material reduction of NPL stocks, better capitalisation and higher interest rates resulting in well-stocked M&A war chests. We expect Germany and Poland to join Italy and Spain in the spotlight.

Challenger bank consolidation is likely to continue in the medium-term, as investor focus on profitability sharpens and watersheds for private equity / venture capital exits loom closer.

6 key considerations for UK & European bank consolidation M&A

White & Case has advised many UK & European banks on successfully navigating the myriad of legal, regulatory and practical considerations associated with consolidation transactions.

Here's our top 6 things to consider: *

Early planning

Has the offeror bank preconsulted its financial regulators?

Top tip: financial regulators do not like surprises. Early-stage "no target name" consultation with prudential relationship managers could yield a helpful preliminary steer on regulator support.

When and how will the approach be made to the target bank / its exiting shareholders?

Top tip: a courtesy chairperson-to-chairperson heads-up, before formal approach, builds important rapport.

Who are the sellers / majority shareholders?

Top tip: capital stacks of many UK & European banks have been built organically over time, which may mean that multiple demographics and classes of shareholders / debtholders require identification in order to determine who really "calls the shots".

Are external advisers on standby to engage quickly?

Top tip: embarrassment could follow for the offeror bank if a favourable sell-side reaction is met with buy-side radio silence, while professional advisers clear conflicts.

What measures are in place to minimise leak risk?

Top tip: team members should be brought "over the wall" on an as-needed basis, and engagement letters (containing robust confidentiality restrictions) should be signed in advance with external advisers. How quickly can a written offer be delivered? Top tip: swift submission of a well-considered non-binding offer letter will enhance the offeror bank's credibility.

Transaction structure

What will be bought / sold (i.e., share vs. asset deal)?

Top tip: not all legal frameworks support mergers by absorption. For example, in the UK, a "merger" may require a banking business transfer scheme under Part VII of the Financial Services and Markets Act 2000.

Will all target shareholders exit on the same basis (or on different terms)

Top tip: the offeror bank will need to deliver a prompt response to the inevitable "when will I get my money?" question. Exit mechanics, payment waterfalls, rollovers, lock-ups, etc., need analysis as a priority.

Are the commercial prerogatives of all target shareholders fully aligned? Does any seller have a deal veto right?

Top tip: if the target bank has multiple shareholders, the ability of the majority to "drag" minorities is critical. Amending "drag" rights for a particular deal can be complex.

What does the offeror bank intend to do with the target bank after closing

Top tip: target-side speculation is unhelpful—operate on a standalone basis (i.e., OneSavings / Charter Court) or merge into existing business (i.e., UniCredit Romania / Alpha Bank Romania) or hybrid (i.e., Barclays / Kensington).

What is the most tax-efficient deal structure?

Top tip: tax treatment of a share deal vs. asset deal could be materially different from stamp duty and other tax perspectives.

What will integration involve?

Top tip: process / workstreams, timing, resources needed, etc.

M&A process

Will the target bank be sold via competitive auction or bilateral negotiation

Top tip: an auction process may not necessarily be the best route for target shareholders to maximise deal value.

What is the proposed deal timeline?

Top tip: consider customary financial regulatory, anti-trust and FDI approvals as well as bespoke commercial conditions (e.g., key supplier change-in-control approvals, regulatory remediation completion, etc.).

What due diligence materials will be available?

Is target bank senior management supportive of the deal process?

Top tip: participation via management presentations and customary Q&A will expedite offeror bank due diligence.

Any specific considerations for disclosure of target bank information?

Top tip: wall-crossing of target bank "heads of", document redaction for data protection / anti-trust reasons, approval for disclosure of financial regulatory correspondence, etc.

Do any special arrangements need to be put in place?

Top tip: insider lists, clean team agreements, standstill arrangements, W&I insurer protocols, etc.

How will target bank staff loyalty be maintained?

Top tip: employee NDAs, transaction bonuses / management incentives, etc.

How will deal negotiations work in practice?

Top tip: target shareholders often jointly appoint a single "sellers' representative" to negotiate terms on their behalf, but a clear shareholder communication protocol is still needed.

Deal value

How will the target bank be valued?

Top tip: consider likely metrics and adjustments. Book value may not be the only metric if the target bank is technology-driven.

Purchase price mechanics can be highly complex and time-consuming to lock down:

How will the price be determined?

Top tip: "locked box" (i.e., fixed price, subject to customary leakage covenant) vs. closing accounts (i.e., price determined by reference to specific metric on closing, subject to post-closing true-up).

What will the price comprise?

Top tip: cash only, offeror bank shares or mix & match.

Are there any securities laws restrictions on offer of share consideration? What reverse due diligence is needed?

Top tip: there could be restrictions on the offeror bank's ability to promote / offer share consideration to foreign target shareholders.

When will the price be paid?

Top tip: bullet payment at closing vs. contingent consideration (e.g., contingent liability non-crystallisation, earn-out, etc.) vs. deferred over time post-closing.

How will the price be paid?

Top tip: consider engagement of paying agents, share consideration custodians and / or escrow agents.

Is any offeror bank certain funds needed?

Top tip: transaction deposit (very rare), escrow, equity commitment letter, debt funding term sheet, bank guarantee, etc.

Will tax-efficient options be offered to target shareholders?

Top tip: loan note alternative.

Closing certainty

Closing is not only about the financial regulator nod:

Financial regulatory approvals: change-in-control applications depend on banking / financial licences held by the target bank and whether the target bank is European Central Bank supervised.

Top tip: "senior manager function" / equivalent approvals often necessitate separate application processes.

Anti-trust clearances: depends on "dominance" of the offeror bank as well as overlapping revenue footprint of offeror bank and target bank.

Top tip: anti-trust regulators view bank consolidations through different lenses from financial regulators. Expect RFIs with significantly different focus.

FDI clearances: depends on operations and product suite of the target bank.

Top tip: at minimum, cater for a desktop analysis. Not simply a question of whether financial services is a 'sensitive sector' under applicable FDI laws.

Risk mitigation can take multiple forms, and often a combination:

Oversight / control until closing over material target bank management decisions.

Non-acceptance of "material conditions" in financial regulatory / anti-trust approvals.

Termination rights linked to warranty bring-down, TCR threshold, regulatory intervention, etc.

MAC walk-away rights.

Top tip: achieving the optimal balance is mission critical, and can serve as commercial leverage to re-calibrate the purchase price after signing.

It's about the people— winning hearts & minds

A key deal driver is often securing and retaining talented banking professionals:

Who are the "key individuals" without which the target bank will struggle

Top tip: early identification of these individuals and understanding their remuneration packages is central to an effective strategy for retaining them post-closing.

What is the impact of the deal on existing target bank management incentives?

Top tip: early vesting triggers could increase transaction costs / impact purchase price.

What retention packages would the offeror bank be willing to provide to key target bank staff?

Top tip: new service contracts for key staff, "skin in the game" through new incentive programme, etc.

How does the offeror bank's own remuneration structure compare to the target bank's?

Top tip: sweeteners for key target bank staff may breed disharmony amongst the offeror bank's own ranks.

What does the post-closing governance structure of the combined group look like?

Top tip: it's not only about short-term money, but longer-term job security and working conditions are equally important. Financial regulators will also focus on governance continuity, well-considered succession plans and any proposed headcount optimisation exercises.

Are key man / woman conditions to closing ever a good idea?

Top tip: leaving the deal certainly in the hands of one or a few individuals is (very) rarely sensible.

*For simplicity, our assessment is in a private M&A context, as UK Takeover Code / UKLR and equivalent regimes across Europe necessitate jurisdiction-specific considerations.

Here’s what is driving consolidation amongst UK & European banks

Many of Europe's largest lenders are finally free from the shackles of government ownership, in place since the global financial crisis.

Well-stocked M&A war chests—higher interest rates have driven profitability, with the top 20 European banks generating US$600 billion in excess capital over the last 3 years.

Fragmented European banking markets—particularly across Germany, Italy, Spain and Poland—are ripe for consolidation. Fewer, stronger lenders could boost more effective competition with U.S. rivals.

Banking is a complex web of scale and scope. Continual growth of product offerings and access to new customers are critical for survival.

Thirst for digital transformation and distribution. European banks have emerged as the heaviest consumers of new technology.

Activist campaigns pressure European bank boards to deliver enhanced shareholder value. Banks remain behind other European stocks, underperforming over the long term.

What are we seeing in other key financial markets?

Middle East perspective

Success rate of bank consolidations is higher than other geographies: many consolidations are pre-aligned at G-2-G level, sponsored by local governments or endorsed by prudential regulators as part of broader reform plans.

Financial regulator involvement: banking regulators often assume a highly proactive role in bank M&A transactions, which has recently developed into market practice of informal notification at a very early stage (often before key deal terms are even agreed between the merging parties).

Political considerations often play a pivotal role in deal structuring: determination of the surviving bank in the case of a statutory merger (or the offeror bank in the case of an acquisition) can become a bottleneck to deal negotiations, and final decisions may necessitate political intervention.

Robust integration plans are mission critical: a key area for regulatory challenge is integration. Financial regulators expect both banks to evidence a clear process, bolstered by detailed steps and evidence of sufficient recourses. Particularly complex areas include integration of core IT systems, cross-border customer data processing and conversion of operations from conventional to Islamic.

HR-related synergies are often difficult to realise: employee-friendly national laws, influential labour unions and conditions set by national regulators relating to retention of local workforces require careful navigation.

U.S. perspective

Trump 2.0 U.S. bank regulation: the U.S. Federal Deposit Insurance Corporation and the U.S. Office of the Comptroller of the Currency have reverted to lighter-touch regulations and approval processes for bank consolidations in 2025. Additionally, "Basel III Endgame" capital requirements, which are currently only partially adopted in the U.S., are expected to be eased by the U.S. Federal Reserve in a new plan anticipated in 2026.

No concept of "U.S. passporting": there is no single, unified bank regulatory framework across the 50 U.S. states. Both federal and relevant state regulators have competent jurisdiction in U.S. bank consolidation transactions.

Market fragmentation drives consolidation M&A: generally speaking, the U.S. is overbanked, resulting in the banking system being fragmented. In the U.S., geographic spread of branch networks, scope of products and brand recognition are 3 key ingredients to growing core deposits.

Importance of customer communication: key threat to successful U.S. bank M&A is customer attrition. The importance of customer communication should not be underestimated. Brand confusion and service disruption concerns can quickly erode trust and result in customers defecting to competitors.

Unleashing the power of AI: the U.S. is ahead of the curve on AI adoption. Bank M&A in the U.S. is not only about consolidating geographic presence but also about capturing larger customer data sets to feed well-developed AI models.

Banks – Publicly reported deals & situations

Restructurings & corporate reorganisations

Deal highlights:

White & Case advised Citi on the separation of its Mexican corporate banking business from its consumer & SME banking business, resulting in a new financial group, Grupo Financiero Citi México, comprised of Banco Citi México and a broker-dealer, Citi México Casa de Bolsa.

White & Case advised Landesbank Baden-Württemberg on its commercial real estate finance realignment project, which involved the integration of assets and liabilities of Berlin Hyp into Landesbank Baden-Württemberg.

Market commentary:

UK banks and building societies will need to weigh-up if local communities lack access to cash services, like branches and ATMs, and plug significant gaps, under new rules from the Financial Conduct Authority (Finextra-July 2024).

UK banks and building societies have closed 6,443 branches since January 2015, at a rate of around 53 each month, representing 64% of the branches that were open at the start of 2015 (Which-June 2025).

Santander's British subsidiary has announced a reorganisation of its branch network, which will involve the closure of 95 branches, 21% of the 444 it currently has (The Corner-March 2025).

Operational synergies:

Landesbank Baden-Württemberg: Integration of assets and liabilities of Berlin Hyp (July 2025)

Deutsche Bank: Restructuring of origination and advisory units (July 2025)

Santander Consumer Finance: Acquisition of 60% of Santander Consumer Bank (June 2025)

Bank Pekao: Combination of insurance operations of PZU Group and Bank Pekao (June 2025)

Citi: Restructuring of Mexican corporate and consumer/ SME banking divisions (January 2025)

Credit Europe Bank Netherlands: Merger with Credit Europe Bank Romania (January 2025)

HSBC: Completion of next stage of global reorganisation (December 2024)

MUFG Bank: Acquisition of MUFG; Securities EMEA, MUFG; Securities Asia and MUFG; Securities Canada (December 2024)

Lunar: Migration of banking services division into Moonrise (November 2024)

Cost reduction:

Barclays: 90 UK branch closures in 2024 (June 2025)

Halifax: 76 UK branch closures in 2024 (June 2025)

NatWest: 68 UK branch closures in 2024 (June 2025)

Bank of Scotland: 31 UK branch closures in 2024 (June 2025)

TSB: 28 UK branch closures in 2024 (June 2025)

Ulster Bank: 10 UK branch closures in 2024 (June 2025)

Danske: 4 UK branch closures in 2024 (June 2025)

Deutsche Bank: 125 German branch closures in 2024 (March 2025)

Lloyds: 60 UK branch closures in H2 2024 and H1 2025 (July 2024)

Capital returns

Market commentary:

European banks' wait time for regulatory approvals for their shareholder payout plans is about to get shorter, as the European Central Bank steps up efforts to boost efficiency (The Luxembourg Times-June 2025).

ING: Implementation of 2025 share buy-back programme of c. €5 million (July 2025)

Ringkjobing Landbobank: Announcement of 2025 & 2026 share buy-back programme of up to DKK 1 billion (June 2025)

BNP Paribas: Launch of 2025 share buy-back programme of €1.084 billion (May 2025)

Deutsche Bank: Launch of 2025 share buy-back programme of up to €750 million (April 2025)

SEB: Announcement of 2025 Class A share buy-back programme of up to SEK 2.5 billion (April 2025)

Nordea: Launch of 2025 share buy-back programme of up to €250 million (March 2025)

Banco Santander: Announcement of 2025 & 2026 share buy-back programme of up to €10 billion (February 2025)

Danske Bank: Announcement of 2025 & 2026 share buy-back programme of up to DKK 5 billion (February 2025)

Société Générale: Launch of 2025 share buy-back programme of up to €872 million (February 2025)

Barclays: Launch of 2025 share buy-back programme of up to £1 billion (February 2025)

Lloyds Banking Group: Launch of 2025 share buy-back programme of up to £1.7 billion (February 2025)

UniCredit: Completion of share buy-back program, acquiring 43.3 million shares (2.65% of share capital), for c. €1.7 billion (November 2024)

Banco Santander: Launch of 2024 share buy-back programme of up to US$1.7 billion (August 2024)

Government-led transactions

Deal highlight:

White & Case advised Qatar-based Lesha Bank on its acquisition of Kazakhstan-based Bereke Bank from Kazakh state-managed fund Baiterek National Management Holding in the first bank acquisition by a Qatari entity in Central Asia.

Market commentary:

NatWest has concluded its full privatisation, with the UK government selling its remaining shares, marking the end of a 17-year period of state ownership (Reuters-May 2025).

Southern European economies continue to outperform the core. In Greece, bank shares have doubled on average since the end of 2022 (Financial Times-September 2024).

European governments have offloaded more than €16 billion of bailed-out bank stocks over the past year, as they seek to draw a line under the long-running effects of the global financial crisis (Financial Times-September 2024).

Privatisations:

HM Treasury: UK, Disposal of all remaining shares in NatWest (June 2025)

Ireland Department of Finance: Ireland, Disposal of remaining stake in AIB Group (June 2025)

Dutch Government / NL Financial Investments: Netherlands, Reduction of stake in ABN Amro to 30% (May 2025)

Government of Norway: Norway, Disposal of 15% of Eksportfinans (March 2025)

HM Treasury: UK, Disposal of 89 million shares in NatWest (March 2025)

Government of Benin: Benin, Disposal of 33% of BIIC (March 2025)

Ireland Department of Finance: Ireland, Disposal of 5% of AIB Group (January 2025)

HM Treasury: UK, Disposal of 2.8% of NatWest Group (November 2024)

Baiterek National Management Holding: Kazakhstan, Disposal of Bereke Bank (October 2024)

Hellenic Financial Stability Fund: Greece, Disposal of 10% of National Bank of Greece (October 2024)

German Government: Germany, Disposal of 4.49% of Commerzbank (September 2024)

Dutch Government / NL Financial Investments: Netherlands, Disposal of 9% of ABN Amro (September 2024)

Domestic mergers:

Hellenic Financial Stability Fund: Greece, Merger by absorption between Attica Bank & Pancreta Bank (July 2024)

Nationalisations:

Turkey Savings Deposit Insurance Fund: Turkey, Acquisition of 79% of Bank Pozitif (March 2025)

State of Benin: Benin, Acquisition of 93.43% of Société Générale Benin (August 2024)

Strategic acquisitions

Deal highlight:

White & Case advised UniCredit on its acquisition of Vodeno, the Polish banking-as-a-service solutions provider, from Warburg Pincus.

Acquisitions (home territory):

Belfius Bank: Belgium, Acquisition of 33% of Candriam (May 2025)

Enity Bank: Mortgage brokerage, Acquisition of remaining 51% of Eiendomsfinans (May 2025)

Victoriabank / Banca Transilvania: SME lending, Acquisition of Microinvest (August 2024)

Mediobanca: Leasing, Acquisition of remaining 40% of SelmaBipiemme Leasing (April 2025)

DNB Bank: Export finance, Acquisition of 15% of Eksportfinans (March 2025)

Banco Santander: Alternative investment management: Acquisition of 89.9% of Tresmares Capital (March 2025)

Banca Etica: EGS investment management, Acquisition of 70% of Impact Sgr (January 2025)

BNP Paribas: Asset management, Acquisition of Axa's asset management business (December 2024)

Arquia Banca: Insurance, Acquisition of stake in CA Life Insurance Experts (December 2024)

S-Bank: Private banking, Acquisition of Svenska Handelsbanken's private customer, asset management and investment services business (November 2024)

DNB: Investment banking, Acquisition of Carnegie (October 2024)

UniCredit: BaaS, Acquisition of Vodeno (July 2024)

Acquisitions (international):

BNP Paribas: Germany, Acquisition of HSBC Continental Europe's German custody business (June 2025)

Alpha Bank / Alpha Services and Holdings: Cyprus, Acquisition of Axia Ventures Group (March 2025)

BNP Paribas: Germany, Acquisition of HSBC Germany's private banking business (September 2024)

Arion Bank: UK, Acquisition of Arngrimsson Advisors (September 2024)

Yapi Kredi: Germany, Acquisition of Bankhaus J. Faisst OHG (July 2024)

Non-core disposals

Market commentary:

The European Union has agreed on a new round of sanctions against Moscow, including limiting Russian banks' access to funding (Financial Times-July 2025).

Only a handful of Western banks, including Austria's Raiffeisen and Italian lenders UniCredit and Intesa Sanpaolo, are still operating in Russia nearly three years after the war in Ukraine began (Reuters-January 2025)

Non-Russia / Ukraine conflict related:

HSBC Continental Europe: Germany, Disposal of German custody business (January 2025)

HSBC: South Africa, Disposal of South African clients and assets (January 2025)

Standard Chartered: Angola, Cameroon,The Gambia & Sierra Leone, Disposal of Angola, Cameroon, The Gambia and Sierra Leone banking subsidiaries (January 2025)

Standard Chartered: Tanzania, Disposal of Tanzania consumer, private and corporate banking business (June 2025)

SJF Bank: Denmark, Disposal of 25% of Nordfyns Bank (June 2025)

Citi Handlowy: Consumer banking, Disposal of consumer banking business (May 2025)

Piraeus Bank: ATM network, Disposal of 80.1% of Kea (May 2025)

Santander: Poland, Disposal of 49% of Santander Polska (May 2025)

Banco BPM: Italy, Disposal of 40% of SelmaBipiemme Leasing (April 2025)

Piraeus Bank: Greece, Acquisition of 90.01% of Ethniki Insurance (March 2025)

Rabobank Group: Turkey, Disposal of Rabobank Turkey (March 2025)

Saxo Bank: Netherlands, Disposal of Dutch / Belgian, SaxoWealthCare and SaxoPensioen business (March 2025)

HSBC Bank Middle East: Bahrain, Disposal of Bahrain retail banking business (February 2025)

UniCredit Bank Austria: Austria, Disposal of 50.1% of Card Complete Service Bank (February 2025)

Raiffeisen Bank International: Austria, Disposal of 25% of Card Complete Service Bank (February 2025)

Mediocredito Centrale: Italy, Disposal of 85.3% of Cassa di Risparmio di Orvieto (January 2025)

HSBC: Insurance, Disposal of HSBC Assurances Vie (France) (December 2024)

Santander: France, Disposal of 30.5% of CACEIS (December 2024)

Svenska Handelsbanken: Finland, Disposal of Finnish private customer, asset management and investment services business (November 2024)

UBS: Switzerland, Disposal of 50% of Swisscard (October 2024)

HSBC: Germany, Disposal of German private banking operations (September 2024)

Raiffeisen Bank International: Belarus, Disposal of 87.74% of Priorbank (September 2024)

Société Générale: Benin, Disposal of 93.43% of Société Générale Benin (August 2024)

Société Générale: UK and Switzerland, Disposal of British and Swiss private banking units to Bancaire Privee (August 2024)

Société Générale: Madagascar, Disposal of 70% of Société Générale Madagasikara (August 2024)

Barclays Bank Ireland: Germany, Disposal of Barclays Consumer Bank Europe (July 2024)

Rabobank International Holding: Turkey, Disposal of Rabobank Turkey (July 2024)

Goldman Sachs: Russia, Disposal of Goldman Sachs Russia (April 2025)

Getin Holding: Ukraine, Disposal of Idea Bank Ukraine (March 2025)

Mikhail Fridman and Petr Aven: Russia, Disposal of stakes in Alfa-Bank (February 2025)

ING: Russia, Disposal of Russian business (January 2025)

Sberbank: Russia, Disposal of L -153 to RM Management (August 2024)

Financial asset management—disposals, collaborations and outsourcings

Deal highlights:

White & Case advised Alpha Bank on its majority disposal of c. 600 Greek real estate assets to a consortium of Greek real estate developers comprising Dimand and Premia.

White & Case advised Hamburg Commercial Bank, as senior investor, on the securitisation of a non-performing loan portfolio of Lowell Danmark, one of the largest credit management service providers in Europe.

White & Case advised doValue, a leading pan-European financial services provider, on:

its acquisition of coeo Group, a German-headquartered digital receivables management platform, from Waterland Private Equity and certain minority shareholders; and

its acquisition of Gardant, the Italian credit management business.

Market commentary:

Portugal's financial institutions have managed to reduce their stock of NPLs from €21 billion 5 years ago to just €5 billion as at March 2025 (Essential Business-March 2025).

Primary market NPL / UTP disposals - banks:

Turkiye Garanti Bankasi: Turkey, Disposal of TL 512,690,008.28 of Turkish NPLs to Sumer Varlik Yonetim (May 2025)

Turkiye Garanti Bankasi: Turkey, Disposal of TL 510,639,573.82 of Turkish NPLs to Gelecek Varlik Yonetimi (May 2025)

Morrow Bank: Norway, Disposal of €9 million of Finnish credit card loans to Kredinor (April 2025)

Santander: Spain, Disposal of €700 million unsecured NPLs to Axactor Espana and Cabot Financial Spain (March 2025)

Santander: Spain, Disposal of €90 million secured NPLs to KKR (February 2025)

Cajamar: Spain, Dispoal of €17.5 million "Project Atenea II" mortgage NPLs to Goriz Advisor and Gannet (February 2025)

First Abu Dhabi Bank: UAE, Disposal of US$800 million NPL portfolio to Deutsche Bank (January 2025)

Santander: Spain, Disposal of €330 million unsecured NPLs to Fortress (December 2024)

Santander: Spain, Disposal of (undisclosed quantum) secured NPLs to undisclosed acquirer (September 2024)

UCI: Spain, Disposal of (undisclosed quantum) unsecured NPLs to undisclosed acquirer (September 2024)

Banco Cetelem: Spain, Disposal of (undisclosed quantum) NPLs to undisclosed acquirer (August 2024)

Banco Cetelem: Spain, Disposal of (undisclosed quantum) NPLs to undisclosed acquirer (July 2024)

Caixabank: Spain, Disposal of (undisclosed quantum) secured NPLs to undisclosed acquirer (July 2024)

Procobro Debt Solution: Spain, Acquisition of €1.4 billion unsecured NPLs from Sociedad de Gestion de Activos Procedentes de la Reestructuracion Bancaria (May 2025)

Sumer Varlik Yonetim: Turkey, Acquisition of TL 512,690,008.28 of Turkish NPLs from Turkiye Garanti Bankasi (May 2025)

Gelecek Varlik Yonetimi: Turkey, Acquisition of TL 510,639,573.82 of Turkish NPLs from Turkiye Garanti Bankasi (May 2025)

Hoist Finance: Spain, Acquisition of €115 million unsecured NPLs and REOs from Unicaja Banco (April 2025)

Kredinor: Norway, Acquisition of €9 million of Finnish credit card loans from Morrow Bank (April 2025)

Axactor Espana and Cabot Financial Spain: Spain, Acquisition of €700 million unsecured NPLs from Santander (March 2025)

Goriz Advisor and Gannet: Spain, Acquisition of €17.5 million "Project Atenea II" mortgage NPLs from Cajamar Bank (February 2025)

Cabot Financial Spain: Spain, Acquisition of (undisclosed quantum) unsecured NPLs from Axactor Espana (November 2024)

Financiera El Coste Ingles EFS: Spain, Disposal of (undisclosed quantum) unsecured NPLs to undisclosed acquirer (April 2025)

Caixabank Payments & Consumer EFC EP SA: Spain, Disposal of (undisclosed quantum) unsecured NPLs to undisclosed acquirer (July 2024)

Primary market acquisitions - banks:

Deutsche Bank: UAE, Acquisition of US$800 million NPL portfolio from First Abu Dhabi Bank (January 2025)

Secondary market NPL / UTP disposals:

KRUK: Czech Republic, Disposal of CZK 1.6 billion consumer NPLs to APS Investments (June 2025)

Sociedad de Gestion de Activos Procedentes de la Reestructuracion Bancaria: Spain, Disposal of €1.4 billion unsecured NPLs to Procobro Debt Solution (May 2025)

PQH: Greece, Disposal of €4.8 billion NPLs in 3 tranches:

Secured retail NPLs to Fortress and Bain Capital;

Secured corporate NPLs to Bracebridge Capital; and

Unsecured / low secured NPLs to Fortress (January 2025)

Debitos: Italy, Disposal of €18 million consumer UTPs portfolio to undisclosed acquirer

Debitos: Italy, Disposal of €16 million consumer UTPs portfolio to undisclosed acquirer (December 2024)

Axactor Espana: Spain, Disposal of (undisclosed quantum) unsecured NPLs to Cabot Financial Spain (November 2024)

Securitisations:

Hamburg Commercial Bank: Germany, NPL securitisation by Lowell Danmark (May 2025)

Acquiring debt servicing capability / capacity:

doValue: Germany, Acquisition of coeo Group (July 2025)

doValue: Italy, Acquisition of Gardant (July 2024)

Intrum: Spain, Acquisition of 15% of Aktua Soluciones Financieras Holding (July 2024)

Performing loan sellers:

Metro Bank: UK, Disposal of £584 million of unsecured personal loans (February 2025)

Santander Consumer Bank: Norway, Disposal of €353 million performing Swedish and Norwegian credit card portfolio to Avida Finans (September 2024)

Orange Bank: France, Disposal of €1.9 billion of loans to LCM Partners / KKR (August 2024)

Metro Bank: UK, Disposal of £2.5 billion residential mortgages portfolio to NatWest (July 2024)

Performing loan buyers:

Avida Finans: Norway, Acquisition of €353 million performing Swedish and Norwegian credit card portfolio from Santander Consumer Bank (September 2024)

LCM Partners / KKR: France, Acquisition of €1.9 billion of loans from Orange Bank (August 2024)

NatWest: UK, Acquisition of £2.5 billion residential mortgages portfolio from Metro Bank (July 2024)

REO sales:

Cajamar: Spain, Disposal of €14.2 million "Project Eros II" residential REOs to KKR (April 2025)

Unicaja Banco: Spain, Disposal of €115 million unsecured NPLs and REOs to Hoist Finance (April 2025)

Santander: Spain, Disposal of €90 million "Project Cosmos" hotel financing loan portfolio to Bank of America Corp (April 2025)

Alpha Bank: Bulgaria, Disposal of Bulgarian property portfolio to Atex Properties (March 2025)

Alpha Bank: Greece, Disposal of 65% of Skyline Real Estate to Dimand, Premia Properties and EBRD (December 2024)

REO acquisitions:

KKR: Spain, Acquisition of €14.2 million "Project Eros II" residential REOs from Cajamar (April 2025)

Bank of America Corp: Spain, Acquisition of €90 million "Project Cosmos" hotel financing loan portfolio from Santander (April 2025)

Atex Properties: Bulgaria, Acquisition of Bulgarian property portfolio from Alpha Bank (March 2025)

Dimand, Premia Properties and EBRD: Greece, Acquisition of 65% of Skyline Real Estate from Alpha Bank (December 2024)

Market consolidation

Deal highlights:

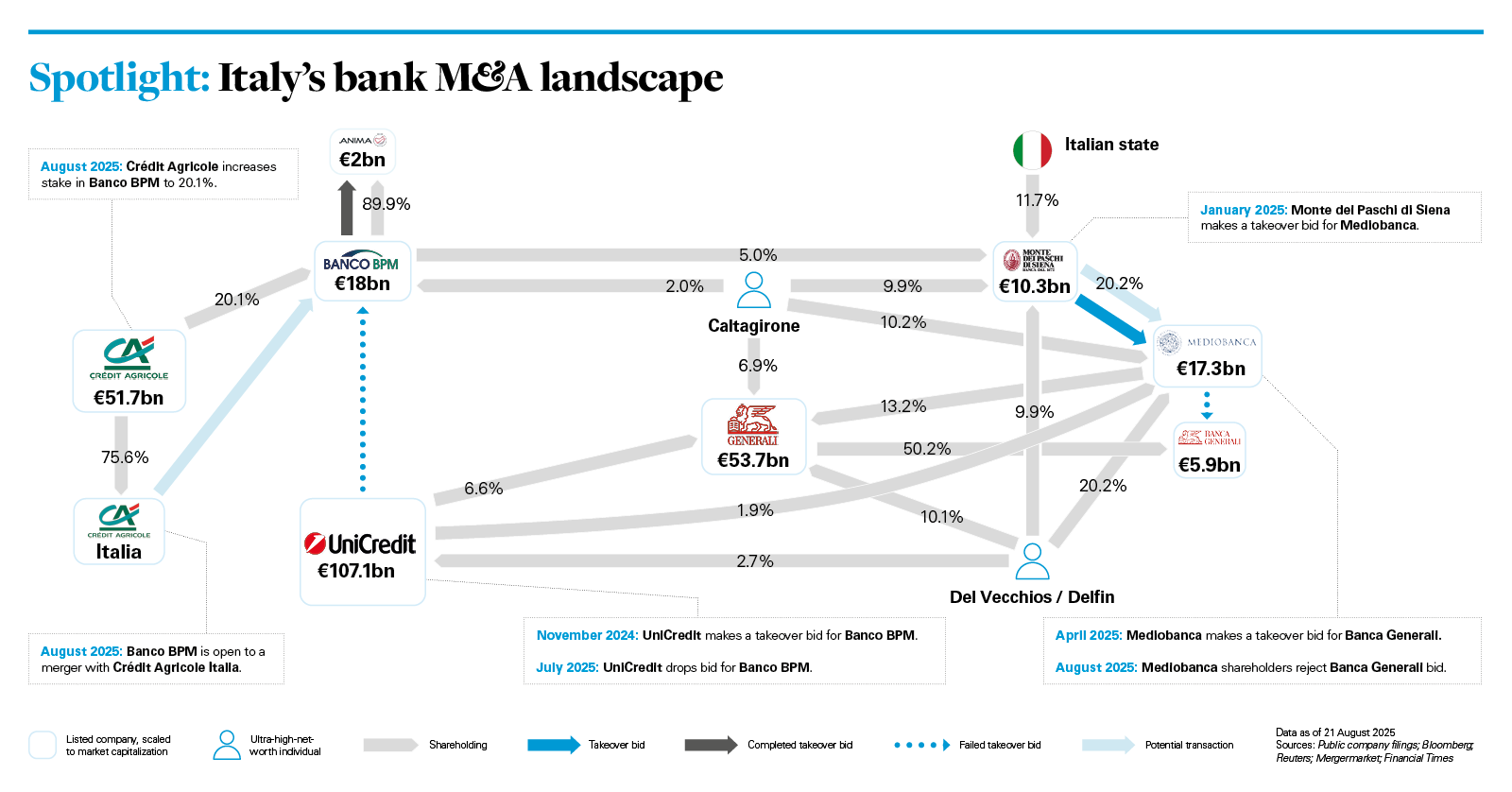

White & Case is advising Banca Monte dei Paschi di Siena on its €13.3 billion takeover bid for Mediobanca.

White & Case advised UniCredit on its acquisition of Aion Bank, the Brussels-headquartered fully digital bank, from Warburg Pincus. White & Case represented the board of directors of The Co-operative Bank (as independent legal advisers) on the sale of the bank by its shareholders, GoldenTree, Silver Point, Anchorage, Cyrus, Invesco, J.C. Flowers and Bain Capital, to Coventry Building Society.

Market commentary:

Hostile bids for European banks have made a comeback after a 5-year hiatus (Mergermarket-June 2025).

Italy's exuberant financial institutions will stay in the spotlight in H2 2025, thanks to a precedent-setting unsolicited bid and growing regulatory support for consolidation (Mergermarket-July 2025).

Banco BPM is open to a potential merger with Crédit Agricole Italia, Crédit Agricole being its largest shareholder with a 20.1% stake (Mergermarket-August 2025).

BPER Banca secures 58.49% stake in Banca Popolare di Sondrio by way of voluntary public tender and exchange offer (Reuters-July 2025).

Mediobanca has made a €6.3 billion bid for Banca Generali, to build a major wealth management business (Generali Group RNS-April 2025).

Monte dei Paschi di Siena has received the European Central Bank's approval for its proposed takeover of larger Italian lender Mediobanca (Reuters-June 2025).

UniCredit has received European Central Bank authorisation for its €14 billion all-share offer to acquire smaller rival Banco BPM (UniCredit RNS-May 2025).

BBVA has received 2 of the most significant approvals in Europe, the approval of the UK Prudential Regulation Authority and the European Central Bank on 3 September 2024 and 5 September 2024, respectively, for its proposed acquisition of Banco Sabadell (BBVA RNS-March 2025). Higher interest rates and improved capital buffers have strengthened European banks' ability to pursue acquisitions (Global Finance Magazine-February 2025).

Senior European Union policymakers have sharply criticised the German government over its opposition to a takeover of Commerzbank by Italian rival

UniCredit (Financial Times-October 2024).

European Commission has expressed concerns over potential political interference in BBVA's takeover bid for Banco Sabadell (Mergermarket-May 2025).

Italy has no plans to strengthen its "golden power" legislation to intervene in mergers and takeovers in the financial sector (Reuters-January 2025).

The federal government of Germany has told UniCredit to exit its investment in Commerzbank, stating that hostile takeovers are not appropriate in the banking sector (Mergermarket-December 2024).

Poland's fragmented banking system is ripe for consolidation, which is likely to be driven by both existing players and new entrants (Mergermarket-June 2025).

Mergers:

Sparebanken Norge & Oslofjord Sparebank: Norway, Merger (May 2025)

Fynske Bank & Nordfyns Bank: Denmark, Merger (May 2025)

VUZ-Bank & Ural Bank for Reconstruction and Development: Russia, Merger (June 2025)

Sovcombank & Home Bank: Russia, Merger (April 2025)

Rosbank & TBank: Russia, Merger (January 2025)

Bureaucrat / Realist Bank: Russia, Acquisition of Natixis Bank (January 2025)

VTB Bank: Russia, Acquisition of stake in Post Bank (December 2024)

Acquisitions:

Banca Ifis: Italy, Acquisition of 92.5% of illimity Bank (July 2025)

BPCE: Acquisition of 75% of Novobanco (June 2025)

Emirates NBD: UAE, Acquisition of remaining shares in Emirates Islamic Bank (June 2025)

FirstRand: South Africa, Acquisition of HSBC South Africa's clients and assets (June 2025)

Eurobank: Cyprus, Acquisition of remaining shares in Hellenic Bank (June 2025)

Access Bank: Angola, Cameroon,The Gambia & Sierra Leone, Acquisition of Standard Chartered's Angola, Cameroon, The Gambia and Sierra Leone banking subsidiaries (June 2025)

Access Bank: Tanzania, Acquisition of Standard Chartered's Tanzania consumer, private and corporate banking business (June 2025)

Middelfart Sparekasse: Denmark, Acquisition of 25% of Nordfyns Bank (June 2025)

MagNet Bank: Hungary, Acquisition of Polgari Bank (June 2025)

ForteBank: Kazakhstan, Acquisition of Home Credit Bank (June 2025)

Santander: UK, Acquisition of TSB Bank (June 2025)

Nykredit: Norway, Acquisition of over 90% of Spar Nord Bank via public tender offer (May 2025)

VeloBank: Poland, Acquisition of Citi Handlowy's consumer banking business (May 2025)

Bank al Etihad: Jordan, Acquisition of INVESTBANK (May 2025)

KBC: Slovakia, Acquisition of 98.45% of 365.bank (May 2025)

Erste Group Bank: Poland, Acquisition of 49% of Santander Polska (May 2025)

Nykredit: Denmark, Acquisition of 80% of Spar Nord Bank (March 2025)

Kaspi.kz: Turkey, Acquisition of Rabobank Turkey (March 2025)

Alpha Bank: Cyprus, Acquisition of AstroBank (February 2025)

Bank of Bahrain and Kuwait: Bahrain, Acquisition of HSBC Bank Middle East (Bahrain branch)'s retail banking business (February 2025)

Burgan Bank: Bahrain, Acquisition of United Gulf Bank(January 2025)

MagNet Bank: Hungary, Acquisition of Polgari Bank (January 2025)

Coventry Building Society: UK, Acquisition of The Co-operative Bank (January 2025)

Banca del Fucino: Italy, Acquisition of 85.3% of Cassa di Risparmio di Orvieto (January 2025)

Access Bank: South Africa, Acquisition of Bidvest Bank (December 2024)

Signet Bank: Latvia, Acquisition of 51% of AgroCredit Latvia (December 2024)

Barclays: UK, Acquisition of Tesco Bank's retail banking business (November 2024)

Bank Dhofar: Oman, Acquisition of Bank of Baroda's Oman business (October 2024)

ABN AMRO: Germany, Acquisition of Hauck Aufhäuser Lampe (September 2024)

Union Bancaire Privee: UK and Switzerland, Acquisition of British and Swiss private banking units from Société Générale (August 2024)

BRED Banque Populaire: Madagascar, Acquisition of 70% of Société Générale Madagasikara (August 2024)

BAWAG: Germany, Acquisition of Barclays Consumer Bank Europe (July 2024)

Nationwide: UK, Acquisition of Virgin Money (July 2024)

Delen Private Bank: Belgium, Acquisition of Dierickx Leys (July 2024)

UniCredit: Belgium, Acquisition of Aion Bank (July 2024)

BPCE: Belgium, Acquisition of Bank Nagelmackers (July 2024)

Liechtensteinische Landesbank: Austria, Acquisition of Zürcher Kantonalbank Österreich (July 2024)

Fintech investment

Please refer to the 'Fintech' report in this series.

Wide investor universe

Deal highlight:

White & Case advised Index Ventures and Balderton Capital on the secondary sales of certain shares in Revolut to funds managed by Goldman Sachs, Dragoneer Investment and Durable Capital.

Venture capital:

Janngo Capital, SANAD Fund for MSMEs, Partech, Oikocredit, Enza Capital and Y Combinator: Neo-banking, Participation in US$17 million funding round in Djamo (April 2025)

Fulgur Ventures: Switzerland Participation in US$58 million funding round in Sygnum (January 2025)

TQ Ventures, Sequoia Capital, Y Combinator, ACE Ventures and Proton Foundation: Switzerland, Participation in US$18 million Series A investment round in nsave (January 2025)

AP Moller: UK, Participation in £80 million funding round in Zopa Bank (December 2024)

M&G Catalyst Fund: South Africa & Philippines, Participation in US$250 million Series D funding round in Tyme Group (December 2024)

Mangrove Capital Partners: UK, Participation in £42 million funding round in Bank of London (September 2024)

Private equity:

Capstone Capital: Greece, Acquisition of majority stake in Cooperative Bank of Epirus (April 2025)

Balchug Capital: Russia, Acquisition of Goldman Sachs Russia (April 2025)

Advent: Bulgaria, Acquisition of TBI Bank (April 2025)

Centerbridge Partners: Italy, Acquisition of 99.82% of Banca Progetto (subsequently aborted) (September 2024)

Local non-bank:

GK Autoretail: Russia, Acquisition of Ingosstrakh Bank (March 2025)

Global Development: Russia, Acquisition of ING's Russian business (January 2025)

Ronesans Holding: Turkey, Acquisition of Rabobank Turkey (July 2024)

Multilateral development banks:

IFC: Morocco, Acquisition of minority equity stake in Holmarcom Finance Company (December 2024)

Financial market infrastructure:

Boerse Stuttgart: Germany, Participation in successful €140 million Series G funding round in Solaris (February 2025)

Insurers:

Direct: Austria, Acquisition of A1 Bank (June 2025)

Fennia / Henki-Fennia: Finland, Acquisition of Sp-Henkivakuutus (April 2025)

Tech partners:

Lesaka Technologies: South Africa, Acquisition of Bank Zero Mutual Bank (June 2025)

GSCF: Germany, Acquisition of IBM Deutschland Kreditbank (January 2025)

Foreign non-bank:

Gojo & Company: Georgia, Acquisition of additional 16.6% of JSC Credo Bank (March 2025)

SBI Group: Germany, Participation in successful €140 million Series G funding round in Solaris (February 2025)

Gojo & Company: Georgia, Acquisition of 16.8% of Credo Bank (December 2024)

Soven 1 Holding: Belarus, Acquisition of 87.74% of Priorbank (September 2024)

First mover digital banks:

Nubank: South Africa & Philippines, Participation in US$250 million Series D funding in for Tyme Group (December 2024)

Ultra high-net-worth / family offices / private investment groups:

Serhiy Tihipko / Alkemi: Ukraine, Acquisition of Idea Bank Ukraina (March 2025)

David Amaryan / Balchug Capital: Russia, Acquisition of Goldman Sach's Russian unit (January 2025)

Ruth Parasol / Parasol V27: UK, £25 million equity investment in Recognise Bank (November 2024)

SWFs:

Mubadala: Digital banking, Acquisition of minority equity stake in Revolut (September 2024)

Public market:

Ahli United Bank of Bahrain: Oman, Disposal of 35% of Ahli Bank Oman (February 2025)

Prem Watsa / Fairfax: Greece, Disposal of stake in Eurobank (January 2025)

Aaron Frenkel: Israel, Disposal of stake in Bank Leumi (January 2025)

Santander Bank Polska: Poland, Accelerated bookbuild of 5.2% (September 2024)

Kuwait Finance House: UAE, Disposal of 18.18% of Sharjah Islamic Bank (August 2024)

Sponsors cash-out

Deal highlight:

White & Case advised international consumer finance business, 4finance, on its sale of tbi Bank to Advent International (subject to customary regulatory approvals).

QIA: Qatar, Disposal of partial stake in Doha Bank (June 2025)

4finance: Bulgaria, Disposal of TBI Bank (April 2025)

GoldenTree, Silver Point, Anchorage, Cyrus, Invesco, J.C. Flowers and Bain Capital: UK, Disposal of The Co-operative Bank (January 2025)

Oaktree Capital Management: Italy, Disposal of 99.82% of Banca Progetto (subsequently aborted) (September 2024)

Challenger banks weather capital raising

Deal highlight:

White & Case advised an internationally recognised investment fund on its US$50 million equity participation in Tyme Group's US$250 million Series D funding round.

Market commentary:

Chase UK has topped a league table of retail banks, marking its fifth successive year, on customer satisfaction (Financial Times-February 2025).

Digital challengers are chipping away at the dominance of UK high street giants, with 9% of Brits now holding their main debit card with a neobank (Finextra-February 2025).

Bank of London was handed a winding-up order by HMRC over unpaid bills days after founder Anthony Watson stepped down as CEO (Finextra-September 2024).

Challengers raise growth equity:

Djamo: West Africa, Successful US$17 million funding round led by Janngo Capital (April 2025)

Getir Finans: Turkey, Successful US$70 million investment from undisclosed provider (March 2025)

myTU: Lithuania, Successful €10 million funding round (March 2025)

Solaris: Germany, Successful €140 million Series G funding round led by SBI Group and Boerse Stuttgart (February 2025)

Sygnum: Switzerland, Successful US$58 million funding round (January 2025)

nsave: Switzerland, Successful US$18 million Series A investment round led by TQ Ventures (January 2025)

Zopa Bank: UK, Successful £80 million funding round led by AP Moller (December 2024)

Tyme Group: South Africa & Philippines, Successful US$250 million Series D funding round led by Nubank (December 2024)

Recognise Bank: UK, Successful £25 million equity investment from Parasol (November 2024)

Bank of London: UK, Successful £42 million funding round led by Mangrove Capital Partners (September 2024)

Yuze: UAE, Successful US$30 million equity investment from Osten Investments (August 2024)

Finora Bank: Lithuania, Successful €5.6 million CET1 and Additional Tier 1 debt funding round (August 2024)

TBC Uzbekistan: Uzbekistan, Successful US$15 million funding round led by European Bank for Reconstruction and Development and International Finance Corporation (July 2024)

Challengers raise growth debt:

Zopa Bank: Digital banking, Successful £80 million AT1 funding round (May 2025)

Challengers scale operations through acquisitions:

OakNorth: U.S. SME banking, Acquisition of Community Unity Bank (March 2025)

Banking Circle: Clearing and settlement, Acquisition of Australian Settlements (January 2025)

New licences:

Bank Aston: Guernsey, Grant of Guernsey banking licence (June 2025)

D360 Bank: Saudi, Grant of Saudi banking licence (November 2024)

Indexo: Latvia, Grant of Latvian banking licence (October 2024)

Revolut: UK, Grant of UK banking licence (July 2024)

Turbulent exit opportunities? Only for some, successes for others

Deal highlight:

White & Case advised Guaranty Trust Holding Company on the admission of its shares to listing in the Equity Shares (International Commercial Companies Secondary Listing) category of the Official List of the UK Financial Conduct Authority and to trading on the Main Market for listed securities of the London Stock Exchange.

Capital markets turbulence:

Klarna: Sweden, Delay of announced U.S. IPO until late-2025 (April 2025)

Capital markets successes:

Guaranty Trust Holding Company / Guaranty Trust Bank: UK, LSE Main Market IPO (July 2025)

M&A turbulence:

Addiko Bank: Austria, Failure of Nova Ljubljanska Banka's voluntary public takeover bid (August 2024)

Addiko Bank: Austria, Withdrawal by Alta Pay of application to Austrian Financial Market Authority to acquire qualifying holding (July 2024)

Redwood Bank: UK, Termination of announced reverse merger with R8 Capital Investments (December 2024)

Long-only vs. activist vs. strategic stake-building

Market commentary:

UK banks want the government to publicly defend their financing of defence companies, saying they have faced a wave of protests accusing them of enabling war crimes (The Banker-May 2025).

ING will dump large clients it believes are not making sufficient progress on reducing their climate impact, in the latest sign of divergence between European and U.S. banks over the risks of global warming (Financial Times- September 2024).

Long-only (in):

Reggeborgh: Netherlands, Acquisition of 3.04% of ABN Amro (March 2025)

Zurich Insurance Group: Spain, Acquisition of 3% of Banco Sabadell (October 2024)

Long-only (out):

Banca Mediolanum: Italy, Disposal of 3.5% stake in Mediobanca (June 2025)

GQG Partners: Spain, Disposal of entire shareholding in BBVA (October 2024)

Strategic stake-building:

UniCredit: Greece, Acquisition of additional 9.7% of Alpha Services and Holdings / Alpha Bank (May 2025)

Credit Agricole: Belgium, Acquisition of 9.9% of Crelan (May 2025)

Credit Agricole: Increase in stake to 19.9% of Banco BPM (April 2025)

Barclays: Germany, Acquisition of direct 7.7% and indirect 8.3% (via derivatives) of Commerzbank (January 2025)

Citigroup: Germany, Acquisition of 7.7% of Commerzbank (January 2025)

Crédit Agricole: Italy, Acquisition of 5.2% of Banco BPM (December 2024)

UniCredit: Germany, Acquisition of derivative instruments to increase stake in Commerzbank (December 2024)

Banco BPM: Italy, Acquisition of 5% of Banca Monte dei Paschi (November 2024)

U.S. states turn activist:

NatWest: Texas added NatWest to a list of firms that "boycott" energy companies, potentially restricting the bank's business with public agencies (August 2024)

Trade unions turn activist:

UGT and Comisiones Obreras: Spain, Petition to Comisión Nacional de los Mercados y la Competencia to block BBVA / Banco Sabadell merger (August 2024)

Activists disrupt 2025 AGMs:

Société Générale: 56 pre-submitted questions for 2025 AGM covering governance gaps, executive pay and sustainability progress (May 2025)

Barclays: Disruption of 2025 AGM by pro-Palestinian protesters (May 2025)

HSBC: Patience Nabukalu's CEO letter ahead of 2025 AGM covering financing the expansion of oil, gas and coal projects in Africa (May 2025)

Raiffeisen: Disruption by BankTrack, B4Ukraine, Attac Austria and WeMove Europe of 2025 AGM over links to Russia (April 2025)

Banco BPM: 6.51% shareholder group, including ENPAM and Fondazione Cassa di Risparmio di Lucca, opposing UniCredit's bid (March 2025)

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View the full image here (PDF)

View the full image here (PDF)