Is anyone talking about anything other than Klarna’s long-awaited US equity debut?

Current market:

- Marginal uptick in M&A activity

We are seeing:

- Buy-now, pay-later providers attract the most private capital interest in the last 12 months:

| Hottest consumer lending verticals for fundraising activity in the last 12 months |

1st | BNPL Announced funding rounds: | - SeQura (€410 million debt and equity funding round)

- Tabby (US$160 million Series E funding round)

- Axio (US$20 million equity investment from Amazon)

|

2nd | Credit cards Announced funding rounds: | - Pliant (US$40 million Series B funding round)

- Yonder (£23.4 million early-stage funding round and equity investment from NatWest)

- Mynt (€22 million Series B funding round)

|

3rd | Digital lending Announced funding rounds: | - Money Fellows (US$13 million pre-Series C funding round)

- Fido (US$20 million Series B funding round)

- Abound (£250 million debt funding round)

|

Established banks:

- Go whale hunting (e.g., Barclays' acquisition of General Motors' card business)

- Prefer funding consumer finance providers, rather than consumer loans (e.g., Deutsche Bank's £250 million debt funding facility for Abound)

- Expend venture capital on finance for underserved consumers (e.g., CommerzVentures' participation in MoneyFellows' pre-Series C funding round)

Consumer finance heavyweights:

- Snap up distressed assets (e.g., Klarna's acquisition of Laybuy's New Zealand assets)

- Recognise importance of sustainability prerogatives (e.g., Younited's acquisition of Helios)

- Deepen existing customer offering (e.g., Tide's acquisition of Onfolk)

Key drivers / challenges:

Diverse buyer / investor profile:

- Public markets: eleving, Enity and Younited were amongst the few financial services businesses to successfully enter the public equity markets in the last 12 months

- Venture capital: primarily participation in funding rounds, with the sweet spot being Series A to C in the last 12 months

- Multilateral development banks: targeting developing financial systems (e.g., IFC's equity investment in MNT-Halan)

Consumer finance providers partner to:

- Rapidly expand distribution channels (e.g., Klarna's 5 BNPL partnerships with Meta, Eurostar, eBay, JPMorgan Pay and GooglePay)

- Increase product suite (e.g., Klarna's debit card partnership with Visa)

- Deepen understanding of customer spending behaviours (e.g., Abound's and Argyle's respective open banking partnerships with D•One and Mastercard)

Trends to watch:

Appetite for growing verticals:

- Payroll finance on both sides of the Atlantic (e.g., Vistra's and Zellis' respective acquisitions of iiPay and Hastee)

- Personal loans (e.g., Lendable's partnership with Post Office)

- Credit card usage remains strong (e.g., Pliant, Mynt and Yonder all successfully executed funding rounds in the last 12 months)

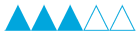

Our M&A forecast

Despite increasing regulatory scrutiny and high-profile insolvencies (e.g., Laybuy and Divido), lender and consumer appetite for BNPL is still growing. Success of Klarna’s long-awaited U.S. equity debut could be the spark which ignites exit hopes for larger consumer finance providers.

Consumer Finance – Publicly reported deals & situations

Healthy buyer/investor appetite

Deal highlight:

White & Case advised Bank of Jerusalem on its unsolicited, deal-jump bid to acquire Isracard, Israel's largest consumer finance and payment solutions provider.

Strategics (investments):

- CommerzVentures: Consumer finance, Participation in US$13 million pre-Series C funding round in MoneyFellows (May 2025)

- NatWest: Credit cards, Equity investment in Yonder (April 2025)

- Citibank: BNPL, Participation in €410 million debt and equity funding round in SeQura (November 2024)

- Stanbic Bank Ghana: Digital lending, Participation in US$10 million Series B debt funding round in Fido (September 2024)

Strategics (debt funding):

- Deutsche Bank: Consumer lending, Provision of £250 million debt funding facility to Abound (March 2025)

Strategics (acquisitions):

- Norion Bank/Walley: Consumer finance, Acquisition of Verkkokauppa.com's consumer financing business (June 2025)

- IBL Banca: Consumer credit, Acquisition of 60% of Fincentro Finance (February 2025)

- Barclays: Credit cards, Acquisition of Goldman Sachs' General Motors card business (October 2024)

Multilateral development banks:

- International Finance Corporation: Micro lending, Participation in US$157.5 million funding round in MNT-Halan (July 2024)

IPOs:

- Enity Holding: Mortgage lending, Nasdaq Stockholm IPO (June 2025)

- Eleving Group: Consumer finance, €29 million Nasdaq Riga Stock Exchange and Frankfurt Stock Exchange IPOs (October 2024)

De-SPACs:

- Iris Financial & Younited: Consumer credit, Business combination (October 2024)

UHNW:

- EAVISTA / Arif Babayev: Credit cards, Acquisition of 75.1% of Card Complete Service Bank (February 2025)

Conglomerates:

- Delek Group: Credit cards, Acquisition of Isracard (July 2025)

Private / venture capital:

- Rocketship, MITAA, Oneway VC and MoreThan Capital: Corporate credit card and financial management, Participation in US$19.8 million debt and equity funding round in Qashio (May 2025)

- Nclude Fund, Al Mada Ventures and Partech Africa: Consumer finance, Participation in US$13 million pre-Series C funding round in MoneyFellows (May 2025)

- Korelya Capital and Opera Tech Ventures: BNPL, Participation in €10 million funding round in Hokodo (April 2025)

- Illuminate Financial, Speedinvest, PayPal Ventures and Motive Ventures: Corporate credit cards, Participation in US$40 million Series B funding round in Pliant (April 2025)

- Blue Pool Capital, Hassana Investment Company, Wellington Management and STV: BNPL, Participation in US$160 million Series E funding round in Tabby (February 2025)

- Goodwater Capital, Ascension Ventures and Love Ventures: Mortgage brokerage, Participation in £14 million Series B funding round in Tembo (December 2024)

- Vor Capital, CNI and Incore: Corporate credit cards, Participation in €22 million Series B funding round in Mynt (December 2024)

- RTP Global, Repeat and Latitude: Credit cards, Participation in £23.4 million early-stage funding round in Yonder (September 2024)

- BlueOrchard Finance and FMO Investment Management: Digital lending, Participation in US$20 million Series B funding round in Fido (September 2024)

- Blue Owl Capital, Rho Capital Partners, The Olayan Group and Hollyport Capital: Payroll finance, Participation in US$120 million funding round in CloudPay (August 2024)

- Catalyst Romania Fund II, South Central Ventures and Lead Ventures: BNPL, Participation in €10 million Series B funding round in Leanpay (July 2024)

- Development Partners International, Lorax Capital Partners, Apis Partners, Lunate and GB Corp: Micro lending, Participation in US$157.5 million funding round in MNT-Halan (July 2024)

Consolidation of market share

Acquisitions:

- Zellis: Earned wages platform, Acquisition of Hastee (June 2025)

- Epassi: Employee benefits platform, Acquisition of VIP District (June 2025)

- LemFi: Consumer credit, Acquisition of Pillar (June 2025)

- Younited: Sustainable banking, Acquisition of Helios (May 2025)

- BTB Israel: Neo-lending, Acquisition of Loani (April 2025)

- Maseera: Consumer finance, Acquisition of ADVA (April 2025)

- The Western Union: FX, Acquisition of eurochange (April 2025)

- Isracard: Cashflow management, Acquisition of 30% of Bizi (March 2025)

- MFK Zaymer: Microcredit, Acquisition of 51% of MKK Sodeistvie XXI (March 2025)

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP