Canada

The Canadian government continues to scrutinize foreign investments by state-owned enterprises and state-linked private investors, especially if from "non-like-minded" countries.

Now in its eighth year of publication, White & Case's 2024 Foreign Direct Investment Reviews provides a comprehensive look at foreign direct investment (FDI) laws and regulations in more than 40 countries worldwide.

In this edition, we continue to offer key datapoints that can help inform parties and their advisors as they evaluate the new set of challenges presented by FDI screening requirements in cross-border transactions that span multiple countries.

FDI screening is continuously evolving, in fact, maturing. Stakeholders in the process, in particular FDI regulatory authorities in allied countries, are communicating and learning from each other. It is imperative to stay on top of the FDI requirements as transactions—be it mergers and acquisitions, investments, public equity offerings, debt structurings or financial restructurings—are negotiated. Understanding the potential remedies that could be required for approval and proper allocation of FDI risk are key ingredients in avoiding unpleasant surprises related to timing, certainty and business plan execution.

The number of national FDI regimes and regulatory enhancements is growing around the world, particularly in Europe, with no harmonization in terms of process and timelines. FDI regulators, at least from allied nations, are collaborating and learning from each other.

FDI regulators interpret their jurisdiction and authority broadly, especially if they believe it is in the national interest. Many regulators have "call-in," "ex officio," or "non-notified" authority. There is increasing coordination in the European Union (EU) between FDI authorities with the support of the European Commission.

Despite increased regulation, most cross-border transactions are successfully consummated, although there has been an increase in the number of cases clearing with remedies.

The origin of the investor remains a key concern for Western regulators. For example, China and Russia are included more and more in the Committee on Foreign Investment in the United States' regular Q&A, asking broader and more invasive questions.

Investors conducting cross-border business need to understand FDI restrictions as they are today, and how these laws are evolving over time, to avoid disruption to realizing synergies, achieving technological development and integration, and ultimately securing liquidity.

The Canadian government continues to scrutinize foreign investments by state-owned enterprises and state-linked private investors, especially if from "non-like-minded" countries.

FDI, whether undertaken directly or indirectly, is generally allowed without restrictions or without the need to obtain prior authorization from an administrative agency.

Most deals are approved without mitigation, but the CFIUS landscape has continued evolving based on a combination of expanded jurisdiction, mandatory filings applying in certain cases, enhanced focus on a broad array of national security considerations, increased rates of mitigation, further attention on monitoring, compliance and enforcement, and a substantially increased pursuit of non-notified transactions.

The European Commission continues to be a driver of FDI screening across the EU, with Member States now moving toward coordinated enforcement.

The wide scope, low trigger thresholds and extensive interpretation of the Austrian FDI regime require a thorough assessment and proactive planning of the M&A process.

The Belgian FDI screening regime entered into force in July 2023. In its early days, investors and authorities alike are coming to grips with the new regime and the guidelines that help parties navigate it.

A bill contemplating the creation of a foreign direct investment screening mechanism in Bulgaria is currently before the Bulgarian parliament.

The new Czech Foreign Investments Screening Act took effect in May 2021, establishing the rights and duties of foreign investors and setting screening requirements for Czech targets.

The scope of the Danish FDI regime is comprehensive and requires a careful assessment of investments and agreements involving Danish companies.

Estonia's foreign direct investment screening mechanism entered into force on September 1, 2023.

French FDI screening continues to focus on foreign investments involving medical and biotech activities, food security activities or the treatment, storage and transmission of sensitive data. The nuclear ecosystem is subject to very close scrutiny.

Following numerous amendments over the past years, Germany's FDI review continued in full swing in 2023, with further significant updates expected in 2024.

FDI screening in Hungary – forever changing regulation, no change in its importance.

Italy's Golden Power Law is now more than 10 years old and is continuously expanding its reach.

The law in Latvia provides for sectoral FDI regimes for specific corporate M&A, real estate dealings and gambling companies.

All investments concerning national security are under the scope of review.

In 2023, Luxembourg adopted a national screening mechanism for foreign direct investments.

Malta's FDI regime regulates transactions that must be notified to the authorities and, in some cases, will be subject to screening.

The Middle East continues to welcome foreign investment, subject to licensing approvals and ownership thresholds for certain business sectors or in certain geographical zones.

The Netherlands, complementing its existing sector-specific regulations, has introduced a general investment screening mechanism to enhance the protection of its national security across a broader range of sectors.

The foreign direct investment regime in Norway is subject to upcoming changes, with further changes expected to come.

The Polish FDI regime – ambiguous rules, no blocking decisions and evolving market practice.

In Portugal, transactions involving acquisition of control over strategic assets by entities residing outside the EU or the EEA may be subject to FDI screening.

The Romanian regime regarding foreign direct investment appears to have become more stable in 2023, but continues to surprise.

Russian laws regulating foreign investments have been considerably amended in 2023 to extend the scope of the laws as well as to strengthen control in this sphere.

The new Foreign Investments Screening Act entered into force in Slovakia on March 1, 2023.

Since May 31, 2020, certain foreign investments into Slovenian companies can be subject to foreign direct investments review. Incorporation of new companies and business units can also be screened.

Certain foreign direct investments in Spain are subject to scrutiny under the Law 19/2003 (Law on the movement of capital and foreign economic transactions and on certain measures for the prevention of money laundering). These restrictions started back in 2020 and, since then, additional formalities have been introduced, specifically by the new FDI regulation, which entered into force on September 1, 2023.

In December 2023, Sweden adopted and implemented a new FDI regime, meaning that a general FDI screening mechanism now applies in relation to investments in certain Swedish businesses.

Historically, Switzerland has been very liberal regarding foreign investments. However, there has recently been increased political pressure to create a more structured legal regime for foreign investment.

Making Türkiye an attractive investment destination continues to be a priority for the government.

Foreign direct investment is permissible in the UAE, subject to applicable licensing and ownership conditions.

The UK introduced new legislation governing FDI in 2022, which also captures domestic investment in certain sectors.

The Western Balkan region (Balkan countries out of European Union) remain increasingly accessible to foreign investment, without established Foreign Direct Investment ("FDI") screening mechanism, with limited requirements for licensing approvals and ownership thresholds, apart from specific sectors.

Australia's stringent foreign investment regulations, overseen by the Treasurer and FIRB, safeguard national interests and security. The framework, including the Foreign Acquisitions and Takeovers Act 1975 and recent updates like the Australia-UK Free Trade Agreement, emphasizes transparency and accountability, with new penalties and registration requirements enhancing oversight and compliance.

While restricting the data transfer relating to national security, China issued guidelines to further optimize its foreign investment environment.

India continues to be an attractive destination for foreign investment, ranking as the world's eighth-largest recipient of FDI in 2023.

Certain businesses related to "Specifically Designated Critical Commodities" have been designated "core" sectors subject to Japan's FDI regime, FEFTA.

The Republic of Korea continues to welcome foreign investment, with the government actively seeking to ease regulations and update the regulatory framework to be in line with global standards.

After a number of years of amendments under the OIA from 2018 to 2021, New Zealand has seen a period of stabilization of the overseas investment regime. However, following the recent election and change of government in New Zealand, further changes are expected to better support investments in build-to-rent housing developments.

Taiwan continues to promote FDI under a two-track screening mechanism for foreign and PRC investors.

The European Commission continues to be a driver of FDI screening across the EU, with Member States now moving toward coordinated enforcement.

Explore Trendscape

Our take on the interconnected global trends that are shaping the business climate for our clients.

Although the EU does not operate its own FDI screening mechanism, the European Commission (EC) continues to be a driver of FDI screening across the union, encouraging Member States to adopt and adapt their regimes, and to move toward coordinated enforcement. The EC also involves itself in Member States' screening via the EU coordination mechanism.

The current EU FDI Screening Regulation does not mandate that Member States must screen investments domestically. It does, however, encourage Member States to adopt screening regimes. Indeed, it provides a skeleton framework that has been relied on by newer members of the FDI club in the EU, prescribing a list of sectors that Member States may want to consider for these purposes, for example. These have been adopted into newer regimes, including those in Romania and the forthcoming regime due to come into force in Ireland.

The implementation of the Screening Regulation has also created an impetus for Member States to align themselves better with the regulation. For instance, Germany broadened and clarified the thresholds for mandatory review to align itself more with the Screening Regulation, and Hungary enacted legislation to harmonize its national regime with the Screening Regulation.

The other big impact of the Screening Regulation is the coordination mechanism that it created. Via this cooperation mechanism, Member States reviewing a foreign investment at the national level will notify certain transactions, thereby alerting all other Member States, and the EC, of the deal.

Other Member States and the EC can then provide comments to the "reviewing" Member State. The reviewing Member State retains the final say under its national FDI screening procedures. However, in practice, Member States will at least try to resolve the issues raised by the EC and other Member States. The cooperation mechanism also means that Member States with the power to call in transactions that do not meet its national notification thresholds will receive outline information on transactions that might have otherwise escaped their attention.

National FDI authorities take different approaches regarding the notification of deals under the Screening Regulation. Certain FDI authorities have systematically notified every transaction involving non-EU investors, while others do so under specific circumstances only.

The Screening Regulation also mandates that the EC produce an annual report on its implementation, which provides a useful snapshot of FDI screening trends and developments across the Union.

According to the EC's Third Annual FDI Report, published in October 2023, while 17 Member States submitted a total of 423 notifications in 2022, six (Austria, Denmark, France, Germany, Italy and Spain) were responsible for more than 90 percent of them.

The annual report shows that 20 percent of the cases notified via the cooperation mechanism in 2022 were multijurisdictional FDI transactions. These were focused on sectors including manufacturing (31 percent), information and communication technology (20 percent), professional activities (14 percent) as well as wholesale and retail (11 percent).

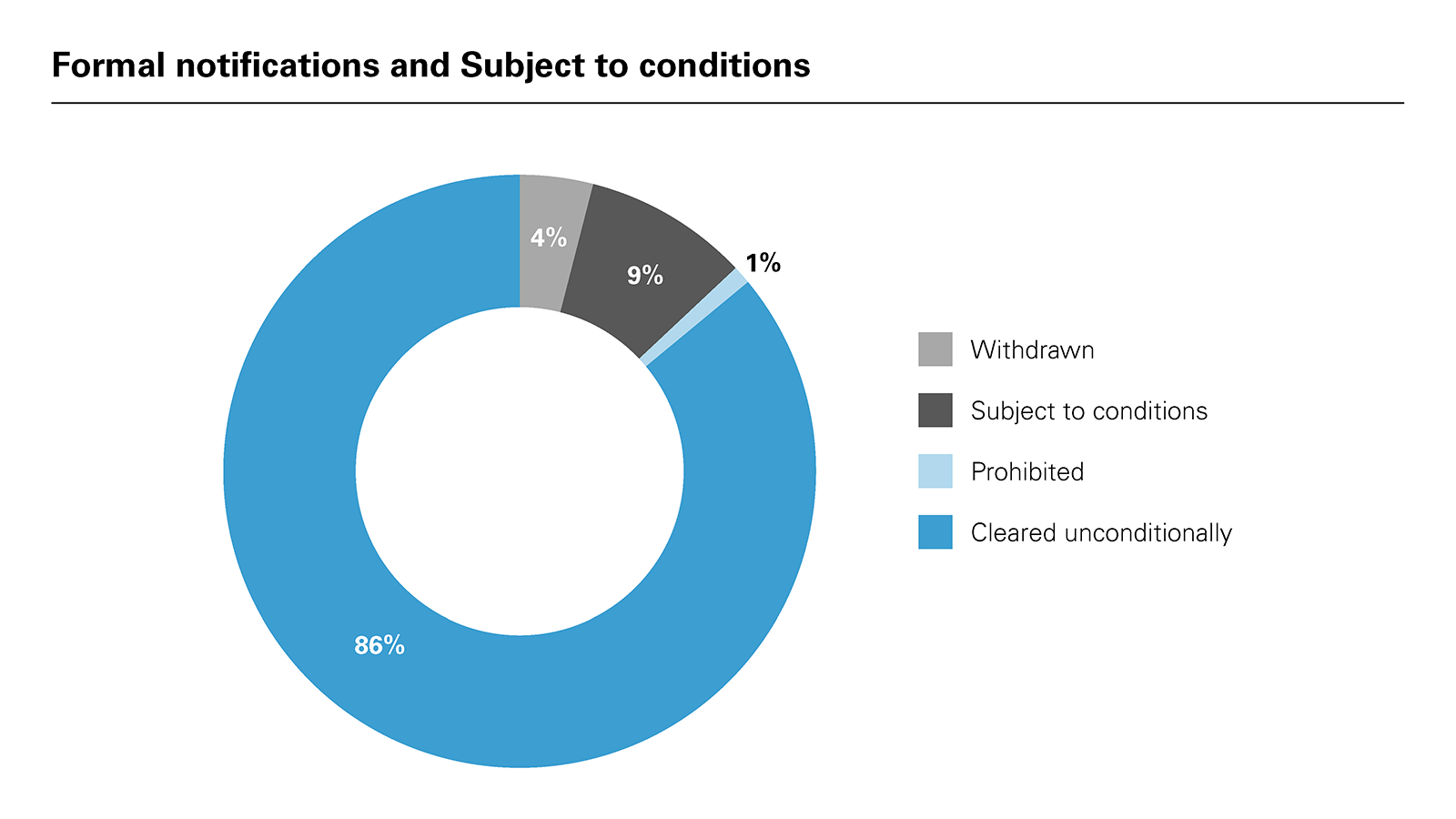

In terms of active regimes, the annual report also indicates that more and more transactions are being formally screened, no doubt at least in part as a function of the general move toward stringency. In 2022, 55 percent of all cases required formal review—up from 29 percent in the previous year. The good news, however, is that clearance remains the norm with 86 percent of notifications subject to formal screening cleared without conditions. An overview of outcomes is provided below.

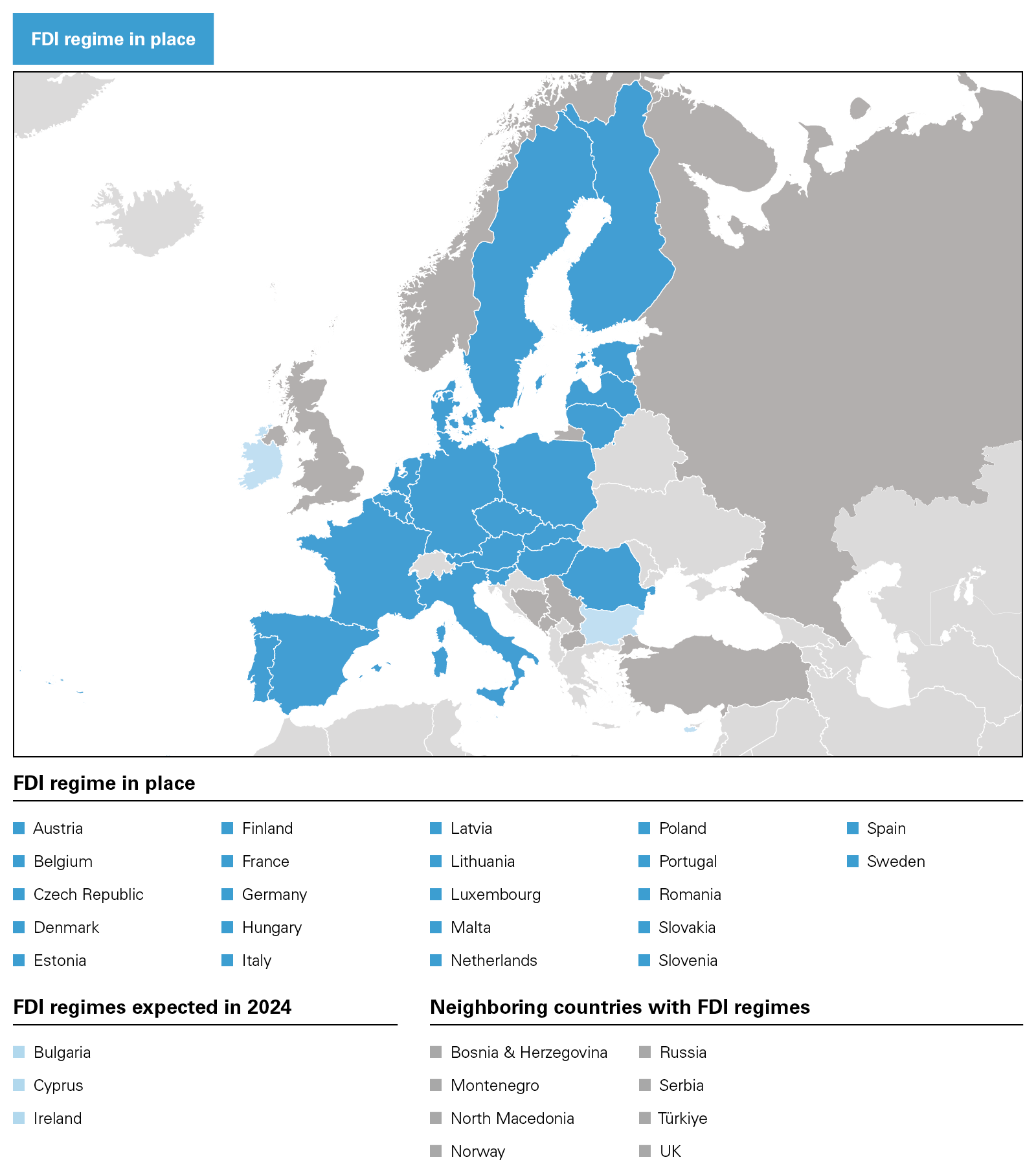

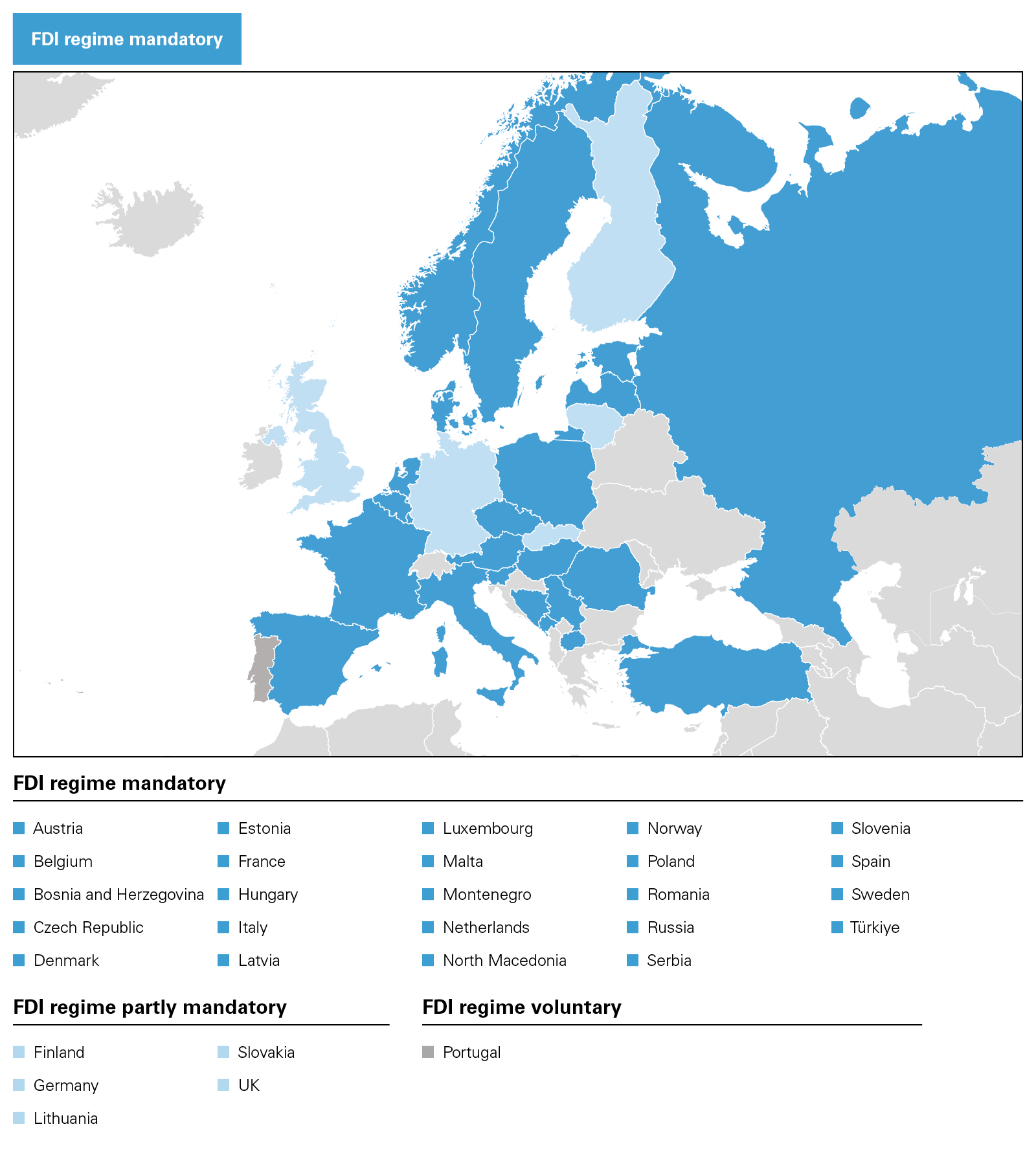

At the time of writing, 25 of the 27 EU Member States have a screening regime or are about to introduce one. The regimes differ widely in a number of areas, for instance whether they provide for mandatory or voluntary filings, and/or ex officio intervention rights of the government.

There are differing approaches to filing requirements, and whether there is a threshold related to the percentage of voting rights or shares acquired, a turnover-based threshold, or another type of trigger. Different Member States take differing views on which industries are viewed as "critical" and may trigger a filing obligation or government intervention, and whether the government has a right to intervene below the thresholds.

Some regimes are suspensory—providing a standstill obligation during the review—and others are not. Some cover only investments by non-EU or EFTA-based investors and others any non-domestic investor. The duration and structure of the proceedings, including whether clearance is subject to remedies such as compliance or hold separate commitments is possible, also varies.

Some regimes are truly hybrid, and the answer to these questions depends on the target's activities and other factors.

There is broad divergence among legislative regimes regarding whether they provide for mandatory filings, voluntary filings, ex officio investigations or a mixture thereof.

The German regime is illustrative. It provides for a mandatory filing requirement based on the target's activities, the size of the stake (voting rights) acquired and the "nationality" of the investor. If these thresholds are not met, the government may still intervene, and investors may hence consider making voluntary filings under certain circumstances.

For an ex officio investigation, there needs to be a direct or indirect acquisition of at least 25 percent of the voting rights of a German target, an increase of an existing stake above 40, 50 or 75 percent, or an acquisition of "atypical control" by a non-EU/EFTA-based investor—otherwise the government does not have jurisdiction to review the transaction. The regime provides for a standstill obligation where filings are mandatory, but not where they are voluntary.

Some regimes also give the parties the possibility to formally consult the authorities as to whether a specific transaction is covered by FDI rules—for example, Czechia, Spain or France.

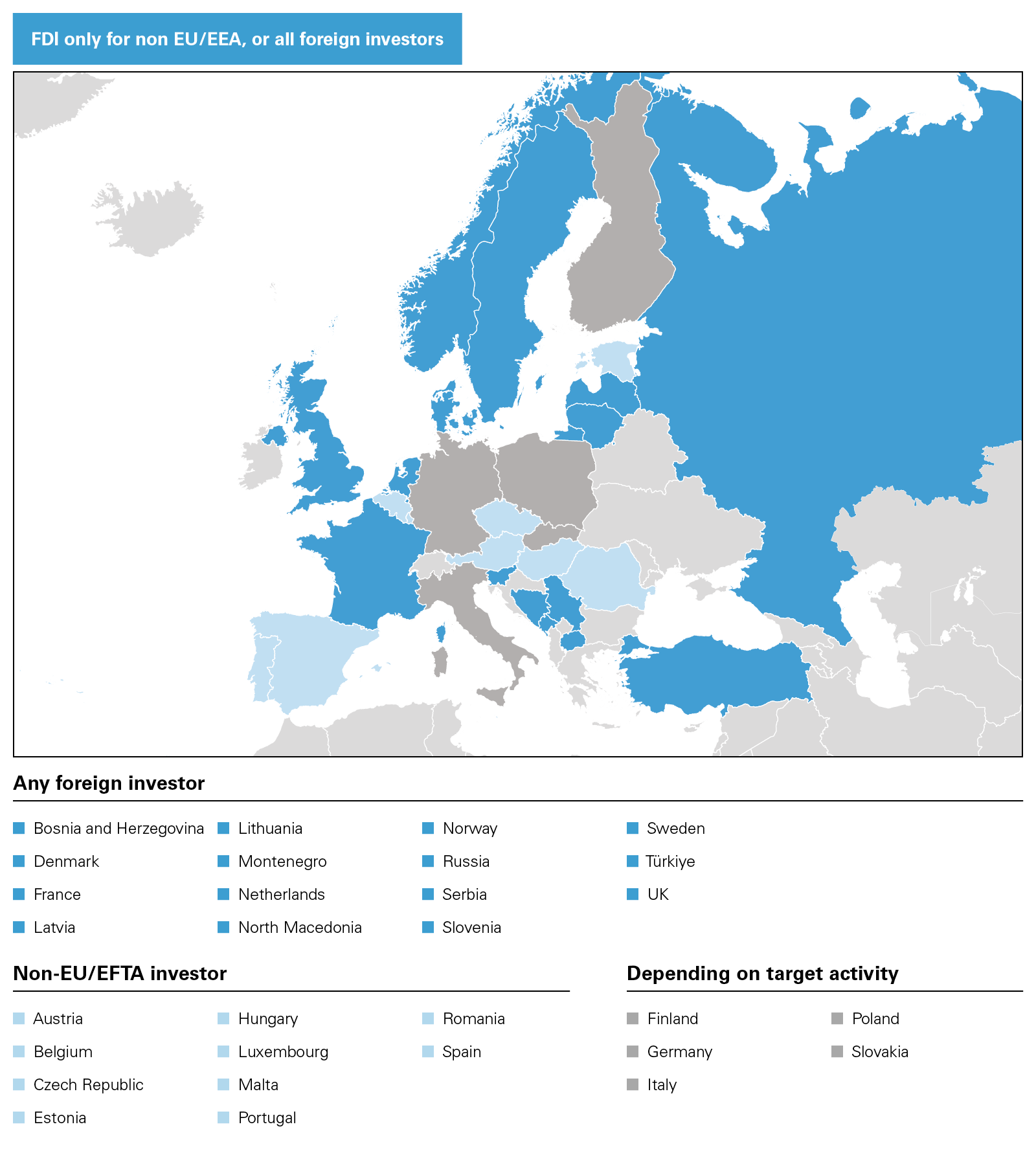

The various national regimes also differ in terms of whether they only cover investments by non-EU-based investors or any non-domestic acquirer. Some regimes are, again, hybrid.

For instance, the German regime scrutinizes investments by any non-domestic acquirer in the defense/crypto-tech sector acquiring at least a 10 percent stake, while in all other sectors, investments by EU or EFTA-based acquirers do not trigger a filing requirement and cannot be reviewed ex officio—although the government takes a very broad view as to whether an investor is non-EU/EFTA-based.

The French regime, for its part, captures acquisitions of control by any non-French investor, but minority acquisitions only if the investor is non-EU/EEA-based (having 25 percent of voting rights for all kinds of entities).

In contrast, the Spanish regime only captures acquisitions by non-EU/EFTA investors if they exceed a 10 percent share or control threshold, and the target is active in certain sensitive sectors. However, a filing is required irrespective of the target's activities if the investor meets certain circumstances: being government-controlled; being subject to sanctions or illegal activities; or having already invested in sensitive sectors in another Member State. In addition, EU/EFTA investors are required to make an FDI filing in Spain if the investment in Spain exceeds €500 million in a non-listed company or involves the acquisition of more than 10 percent of a Spanish listed company.

Similarly, the regimes in the Czech Republic or Belgium define "foreign investor" for filing purposes as one from a non-EU country.

Views across the US, Europe and elsewhere are converging to a consensus that so-called "sensitive" sectors need to be protected from what is being described in the US as "adversarial capital" in a more or less coherent way. This trend is displayed through both the lowering of thresholds that trigger FDI reviews and an expansion of what qualifies as a sensitive sector for purposes of FDI reviews, export controls and international trade compliance. As an example, Germany added 16 new case groups to its screening scope, while France supplemented the list of strategic sectors to extraction and processing of critical raw materials.

Sensitive sectors are no longer limited to the traditional sectors associated with national security at a macro level (defense, energy or telecom), but are now expanding to biotechnologies, hi-tech, new critical technologies, such as artificial intelligence or 3D printing, and data-driven activities. There is increased scrutiny in the EU of transactions involving access to patients' health data.

Moreover, the COVID-19 pandemic brought FDI into sharper focus and accelerated movement on a national level across Europe. Governments were concerned about foreign investors taking advantage of European companies being in distress and, of course, the crisis led the governments to add the healthcare sector to the sensitive industries. In line with the Screening Regulation, FDI screening is also expanding to the area of food security, which has become a priority concern in the EU. Investments in the agri-food sector are subject to review in several Member States such as Estonia, France, Germany, Italy, Latvia, Malta, Poland and Spain.

Finally, 5G technology has become a source of concern for certain Member States that had issued specific rules to ensure FDI screening in relation to 5G networks and equipment. In Italy, the government's "Golden Power" pre-clearance process is mandatory for contracts or agreements with non-EU persons relating to the supply of 5G technology infrastructure, components and services.

France introduced a specific ad hoc authorization process for operating 5G technology in French territory. In Germany, the Federal Network Agency has published a security catalog for telecoms and data processing, highlighting the critical nature of 5G networks, and the federal government has the ability to prohibit the use of certain components due to threats to public order and security, even where these have passed the technical certification process.

Despite the converging views as to what sectors are considered critical, the exact definition of critical activities may differ greatly between Member States—for example, whether only the production of the semiconductor value chain is covered, or also the required equipment, input materials or chip design.

Some national FDI regimes determine filing requirements or intervention rights based solely on the size of the stake acquired, and cover share deals and asset deals alike; others rely on different or additional factors, such as the target's revenues.

By way of illustrative example, in the healthcare sector, the German regime provides for a filing obligation for an investment by a non-EU/EFTA-based acquirer of at least 10 percent if the target is considered an operator of critical infrastructure (as defined in great detail, for example hospitals handling at least 30,000 inpatient cases/year or diagnostic and therapeutic laboratories handling 1.5 million orders/year; or at least 20 percent if the target develops or manufactures personal protective equipment; develops, manufactures or markets essential medicines; develops or manufactures medicinal products for diagnosis, prevention, monitoring, predicting, forecasting, treating or alleviation of life-threatening and highly infectious diseases; and develops or manufactures in vitro diagnostics relating to life-threatening and highly infectious diseases.

Prior approval is required in Austria only if the target company employs ten people or more, and if it has annual turnover or an annual balance equal to or more than an annual revenue of €2 million or more.

Even where transactions are out of the formal scope of the FDI regimes, Member States may be prepared to intervene through targeted measures. As an example, the German authorities intervened through a German state-owned company to acquire a minority interest in a biopharmaceutical company whose focus was on developing vaccines for infectious diseases like COVID-19 and drugs to treat cancer and rare diseases, in order to avoid its potential acquisition by any foreign investor.

Similarly, the German federal government decided to prevent a Chinese investor from investing in the power grid operator by arranging for an investment by a German state-owned company, because it did not have jurisdiction to block the deal under the then-pertinent FDI regime. The German government officially confirmed that the acquisition was aimed at protecting critical infrastructure for energy supply in Germany.

The duration of proceedings differs widely between jurisdictions. Generally, the process takes several months, and many feature a two-phase process (initial review period followed by in-depth review) and provide for stop-the-clock mechanisms, such as suspension based on information requests, or negotiation of mitigation requirements.

Blocking decisions on national security grounds remains an exception in most Member States. As noted above, the EC's 2022 annual report indicates that only 1 percent of all decided cases were eventually blocked by national authorities, while for a further 4 percent, the transaction was withdrawn by the parties.

Issuing a formal veto to a potential foreign investor may leave the target business without a new investor, as illustrated by a recent case in France. In October 2023, the French Ministry of the Economy, for the first time, formally vetoed the acquisition of Velan's French subsidiaries, Ségault and Velan, by the American group Flowserve. Ségault and Velan supply components for French nuclear-propelled submarines and nuclear power plants respectively. Following the French veto, Flowserve announced that it had abandoned its plans to take over Velan worldwide.

In November 2023, the Italian government prohibited the sale to the French group Safran of Microtecnica, Collins Aerospace's Italian subsidiary, citing national security concerns over the future of a "strategic" asset.

Clearance with "remedies" (mitigation agreements) is becoming customary in an increasing number of Member States. Remedies generally include maintaining sufficient local resources related to the sensitive activities; restrictions on the use of intellectual property rights or on the governance of the target company; mandatory continuation of sensitive contracts to ensure continued services; appointing an authorized security officer within the target company and reporting obligations; strict data protection obligations going beyond the GDPR; and so on. In extreme cases, national authorities may also impose mandatory disposal of sensitive activities to an approved acquirer.

According to the EC's 2022 annual report, the five main countries of origin of the 423 cases notified to the EC were the US (32 percent), the UK (7.6 percent), China (5.3 percent), Japan (5 percent); the Cayman Islands (4.8 percent) and Canada (4 per- cent). Russia accounted for less than 1.4 percent of the cases and Belarus 0.2 percent.

The investor origin continues to be one of the most relevant considerations in making the risk assessment. For example, Germany issued or threatened an increasing number of prohibitions on transactions originating from China and Russia.

That divergence in national approaches has led to headaches for multijurisdictional transactions in particular, as assessments and procedures continue to diverge. These will frequently require notification under the coordination mechanism, although in its 2022 annual report, the EC observed that this was "rarely" being done in "a coordinated and synchronized manner."

This lack of coordination is part of the driver for the EC's proposal for a new FDI screening mechanism, published in January 2024. The proposal will include mandatory requirements for all Member States to implement a national screening mechanism within 15 months of its coming into force, although, with a European election taking place in June 2024 meaning the proposal is unlikely to see adoption until the new legislative session, this may be a fait accompli by the time those requirements begin to bite.

Of more relevance are efforts at standardizing the timelines for the way that Member States will engage with the cooperation mechanism, as well as a prescribed minimum scope for national screening regimes.

In addition to the above, the EC also published in January 2024 a white paper on outbound investments. There is currently no monitoring of outbound investment flow outside of the EU; however, following open debates with Member States that started in spring 2023, including an expert group that was formed last July, the EC's findings in the white paper were that there are substantial knowledge gaps around the potential risks that could accompany relevant investments—for example in relation to potential misuse of EU technology and know-how in third countries—due to a lack of specific or systematic monitoring of outbound investments at the EU or Member State levels.

The EC acknowledged that this is a complex and sensitive policy area, meaning that a gradual approach is required to gather data and evidence on potential risks, and determine any policy response. The EC also underscored that before designing any specific policy measures, the EU would need to make full use of existing instruments first. Proposed next steps on a potential policy change include: a public consultation period throughout 2024; monitoring and review of current transactions throughout most of 2025; and the announcement of any need for a policy response by autumn 2025.

While the EU Screening Regulation is by and large an instrument of "soft law," it does add substantial complexity and uncertainty to security reviews performed at the Member State level. Essentially, the EU Regulation puts additional pressure on Member States to consider a broader range of security interests, which is likely to facilitate lobbying efforts from other stakeholders taking an interest in a transaction. Member States intensify their FDI screenings and keep a close eye on investments thanks to the EU Screening Regulation.

On the other hand, the European Court of Justice (ECJ) has been vigilant that national FDI screenings regimes would not be used as a protectionist tool within the EU. In its recent Xella Magyarország judgment (Case C 106/22), the ECJ states loud and clear that a protectionist measure taking the form of national FDI screening legislation will amount to an unjustifiable restriction of the fundamental freedoms protected under EU law.

As a result of the automatic information exchange system, we have seen an increasing trend of Member States' FDI authorities reaching out to the parties for non-notified transactions either before closing or after closing. In certain instances, authorities asked for the parties to file, which could impact the timeline of the deal.

Investors should make sure that a comprehensive multijurisdictional FDI assessment is carried out in transactions involving potentially strategic sectors and a variety of jurisdictions where the target business operates. Investors should also have a proper strategy in place to deal with multiple parallel notification processes in several Member States to ensure a consistent approach.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2024 White & Case LLP

View full image: Formal notifications and Subject to conditions (PDF)

View full image: Formal notifications and Subject to conditions (PDF)

View full image: FDI regime in place (PDF)

View full image: FDI regime in place (PDF)

View full image: FDI regime mandatory (PDF)

View full image: FDI regime mandatory (PDF)

View full image: FDI only for none EU/EEA, or all foreign investors (PDF)

View full image: FDI only for none EU/EEA, or all foreign investors (PDF)