In December 2020, then-US president Donald J. Trump signed into law the Holding Foreign Companies Accountable Act (the "HFCAA"). This law is just one measure, among many, that have been promulgated by legislative and regulatory authorities in the United States ("US") amid a backdrop of increasingly heightened scrutiny of US-listed, China-based companies ("Chinese Listcos"). The HFCAA in particular threatens to cause delisting of Chinese Listcos from US securities exchanges and prohibit trading of their securities in the US "over-the-counter" ("OTC") market by 2024, if not earlier.

As a result, many Chinese Listcos are exploring alternate listings outside the US. The impact of US regulators' increased scrutiny on Chinese Listcos combined with current market conditions also make these issuers ripe targets for going private proposals from controlling shareholders and/or other market participants. A third possible pathway for Chinese Listcos could be voluntary delisting and deregistration in the US (i.e., going dark). In this article, we highlight some key features of the HFCAA and discuss some of the key legal considerations around the potential consequences and outcomes for Chinese Listcos.

1. The HFCAA

Under the HFCAA and its implementing rules, reporting issuers that are identified by the Securities and Exchange Commission (the "SEC") as matching certain criteria for three consecutive years would be subject to trading restrictions and additional disclosure obligations.

a. How does the HFCAA operate?

i. Singling out Commission-Identified Issuers: The criteria used by the SEC for identifying the issuers subject to the HFCAA center on whether the Public Company Accounting Oversight Board (the "PCAOB") (the body overseeing the audits of public companies in the US) has determined that the auditors of these issuers were not subject to full PCAOB inspection or investigation. More specifically, the so-identified issuers ("Commission-Identified Issuers") comprise any US-listed company who has retained an auditing firm with a branch or office that (i) is located in a foreign jurisdiction; and (ii) the PCAOB determines it is unable to inspect or investigate completely because of a position taken by an authority in that jurisdiction. Since the enactment of the HFCAA, the PCAOB has made jurisdiction-wide determinations in respect of auditing firms headquartered in (i) mainland China; and (ii) Hong Kong, covering all PCAOB-registered auditing firms in both jurisdictions. In March 2022, as companies started to file their annual reports (together with the required audit reports), the SEC began to identify numerous Chinese Listcos as Commission-Identified Issuers—156 Chinese Listcos conclusively and six Chinese Listcos provisionally as of the date of this article.1 Under the HFCAA, the SEC will repeat this exercise for annual reports filed for fiscal years 2022 and 2023.

ii. Trading prohibition: After a company is conclusively identified as a Commission-Identified Issuer by the SEC for three consecutive years, the SEC will issue an order prohibiting the trading of its securities on any US securities exchange or the OTC market, which will become effective four business days thereafter. Therefore, for a company that is a Commission-Identified Issuer for fiscal years 2021, 2022 and 2023 (based on its annual reports filed in 2022, 2023 and 2024, respectively), the earliest any trading prohibition would apply would be in 2024. However, the US Senate has passed a bill to accelerate the timeline under the HFCAA from three years to two years, and a similar bill has been introduced in the US House of Representatives.2 If either of these bills were to be signed into law, trading bans could occur as early as 2023.

iii. Delisting: Although the HFCAA does not mandate that securities subject to trading bans be delisted, and while neither NYSE nor NASDAQ has issued any statement in relation to the treatment of the securities of the Commission-Identified Issuers, we fully expect stock exchanges will delist Commission-Identified Issuers once trading bans are imposed. Under applicable exchange rules for NYSE and NASDAQ,3 if the relevant stock exchange has determined (at its discretion) that an issuer's continued listing raises public interest concerns, they can delist the issuer. For example, in 2021, NYSE delisted China Mobile Limited on the basis that it was no longer suitable for continued listing.4

b. What additional disclosure is required for Commission-Identified Issuers?

Once so identified, a Commission-Identified Issuer must submit documents annually (prior to its annual report) evidencing that it is not owned or controlled by a governmental entity in its auditing firm's jurisdiction.

In addition, a Commission-Identified Issuer must disclose in its annual report for each year that it is so identified: (i) the accounting firm that has prepared its audit report; (ii) the percentage of its shares owned by governmental entities in the foreign jurisdiction in which it is incorporated or organized; (iii) whether governmental entities in the same foreign jurisdiction as the issuer's accounting firm have a controlling financial interest in it; (iv) the name of any official of the Chinese Communist Party who is a member of the board of directors of the issuer or any of its operating entities, including if there are any variable-interest entities ("VIEs") among its operating entities; and (v) whether the articles of incorporation of the issuer (or equivalent organizational documents) contain any charter of the Chinese Communist Party, including the text of any such charter.5

c. What is the status of regulatory discussions around PCAOB inspection?

Regulators in China and the US are discussing possible resolutions to the impasse between the PCAOB and Chinese auditing firms. Practitioners remain optimistic that a suitable resolution will be achieved, but it remains to be seen whether an agreement will be reached before the clock runs out for Commission-Identified Issuers.

Calling for continued China-US cooperation on audit oversight, China's primary securities regulatory agency, the China Securities Regulatory Commission (the "CSRC"), was recently reported to have indicated that "positive progress" had been made in talks on regulatory cooperation with US regulators.6 The CSRC issued a new draft rule regarding access to information by overseas regulators in April 2022, which appears to remove some obstacles to the oversight the PCAOB desires by providing that inspection or investigation of a Chinese Listco by overseas securities regulators and other competent authorities may be conducted "under cross-border regulatory cooperation" with CSRC and other Chinese government authorities providing necessary assistance.7 There have also been reports that Chinese regulators have informed auditing firms and Chinese Listcos to prepare for PCAOB inspections.8

On the other hand, the PCAOB commented on May 24, 2022 that market speculation about an imminent deal between the PCAOB and the CSRC was "premature."9 Recently, YJ Fisher, the Director of the SEC's Office of International Affairs, expressed similar cautious sentiment in a public speech, and stated that the US and Chinese authorities are engaging in constructive discussions, but it remains uncertain as to whether the PCAOB and Chinese authorities will reach an agreement.10 Furthermore, even if an agreement is reached by the PCAOB and Chinese authorities, the PCAOB would need to determine that it can complete inspections and investigations before any reassessment of its 2021 determination on non-compliant jurisdictions.

2. Alternative listing on the HKSE

Facing uncertainties on a resolution of the PCAOB issue and potential delisting risk, Chinese Listcos are actively exploring alternative listing venues and have sought secondary or dual-primary listings where permitted. Given the nexus between Hong Kong and mainland China, the Hong Kong Stock Exchange (the "HKSE") has been a natural option for many such Chinese Listcos. Based on our search of public records, after signing of HFCAA, 12 Chinese Listcos have completed a dual-primary listing or a secondary listing on the HKSE, making it the most popular dual listing venue for Chinese Listcos.

To qualify for a dual-primary or secondary listing on the HKSE, Chinese Listcos will typically first need to qualify as a "Grandfathered Greater China Issuer," which is defined under the HKSE listing rules (the "Listing Rules") as a company with its center of gravity in Greater China and was listed on NYSE, NASDAQ or the London stock exchange (a "Qualifying Exchange") on or before December 15, 2017, or, for companies with weighted voting rights ("WVR"), on or before October 30, 2020.11

a. What is a dual primary listing on the HKSE?

With a dual-primary listing on the HKSE, Chinese Listcos could concurrently list their shares on the HKSE in addition to their listing and registration in the US. The holders of American depositary shares ("ADS") of a dual-primary listed issuer could cause their ADSs to be converted into the ordinary shares and traded on the HKSE. If these Chinese Listcos delist in the US, it would not affect their primary listing status on the HKSE.

A dual-primary listing on the HKSE has the same listing requirements applicable to an IPO in Hong Kong. In addition, Chinese Listcos may pursue a dual-primary listing, retaining their existing WVR and/or VIE structures, as long as they can, among others, (a) demonstrate that it is an "innovative company" (e.g., operating internet related or other high-tech businesses);12 (b) have a track record of good regulatory compliance of at least two full financial years on a Qualifying Exchange;13 and (c) have (i) a market capitalization of at least HK$40 billion; or (ii) a market capitalization of at least HK$10 billion and revenue of at least HK$1 billion for the most recent financial year.14 Chinese Listcos without any WVR or VIE structures do not need to demonstrate that they are an innovative company in their dual-primary listing but would otherwise need to satisfy the listing qualifications under the Listing Rules. In addition, if Chinese Listcos adopt US GAAP in their financial reports, they will be required to provide a reconciliation statement to HKFRS or IFRS in their financial statements in the listing documents, accountants' reports, as well as any annual and interim reports.15

b. What is a secondary listing on the HKSE?

The HKSE codified the qualifications and requirements for secondary listings for overseas issuers in 2018, which include Chinese Listcos whose jurisdiction of incorporation is not Cayman Islands, Bermuda, Hong Kong or the PRC. For an issuer with a center of gravity in Greater China to qualify for a secondary listing on the HKSE, the issuer must have either: (a) a HK$3 billion market capitalization with a track record of good regulatory compliance for five full financial years on a Qualifying Exchange; or (b) a HK$10 billion market capitalization with a track record of good regulatory compliance for two full financial years on a Qualifying Exchange.16 The compliance track record requirements may be waived if the company is well-established and has a market capitalization significantly larger than HK$10 billion.17 A Chinese Listco with WVR will also need to meet the "innovative company" requirement and the same compliance track record and market capitalization/revenue test required for a dual-primary listing to maintain its WVR in connection with a secondary listing on the HKSE.18

Similarly, a secondary listed issuer's ADS holders could cause their ADSs to be converted into the ordinary shares and traded on the HKSE at any time. If these Chinese Listcos subsequently delist in the US, they would need to effect a primary conversion through one of the three pathways discussed below to be primarily listed on the HKSE.

c. Why is a secondary listing preferred by Chinese Listcos, and how can they convert from a secondary listing into a dual primary listing?

In general, Chinese Listcos may have their equity securities (e.g., ordinary shares or deposit certificates) listed and traded on a US securities exchange and, following a dual-primary listing or a secondary listing, on the HKSE. The equity securities will trade on the US securities exchanges and the HKSE independently.

The main advantage of a secondary listing over a dual-primary one is that certain customary waivers and exemptions from compliance with the HKSE Listing Rules are available only for secondary listings. These include waivers from requirements concerning audit and remuneration committee establishment, certain reporting and announcements, and certain continuing disclosure obligations.19 As an issuer applying for a secondary listing on the HKSE, it would be able to apply for customary waivers from compliance with certain listing requirements applicable to an IPO and the Hong Kong Takeovers Code. A Chinese Listco could achieve a listing on the HKSE more quickly and at lower cost through a secondary listing, as compared to a dual-primary listing.

Conversion to a primary listing can occur in one of the following three ways: (i) voluntarily, by submitting a primary conversion application to the HKSE with regard to the plan to carry out a primary conversion and any applicable waiver applications as a primary listed issuer; (ii) by delisting (either voluntarily or involuntarily) in its primary listing jurisdiction, an issuer will be automatically treated as having its primary listing on the HKSE; or (iii) by trading migration, if 55% or more of the trading volume by dollar value in the shares of a secondary-listed company takes place on the HKSE over the most recent financial year, the company will be required to convert its listing to a primary listing on the HKSE.20 However, as noted above, following a conversion from a secondary listing to a primary listing on the HKSE, waivers and exemptions that are applicable only to secondary listings will no longer be available and full compliance with the Listing Rules will be applicable following the migration.

3. Going private

The perfect storm of market conditions and the potential impact of the HFCAA has led to a rise in another common outcome for Chinese Listcos: "going-private" transactions. Many Chinese Listcos are controlled by one or a few founders or controlling shareholders, who can unilaterally determine (or at least veto) any take-over transaction. This voting power has parlayed into an opportunity for controlling stakeholders, who may team up with institutional investors looking to arbitrage depressed US valuations against a hopefully growing Asian market. Controllers typically achieve this by making an offer to the board of the Chinese Listco to acquire all of the shares not owned by them, and if the offer is accepted and successful, the issuer would delist and deregister its shares, becoming a private company. As a proposed buyer is often an affiliate of the issuer, these privatizations are conflict transactions, around which certain legal and commercial conventions have developed, often in ways that slightly diverge from counterpart practice in the US. We review some of the key features of these norms below.

a. What are some recent trends in going-private transactions of Chinese Listcos?

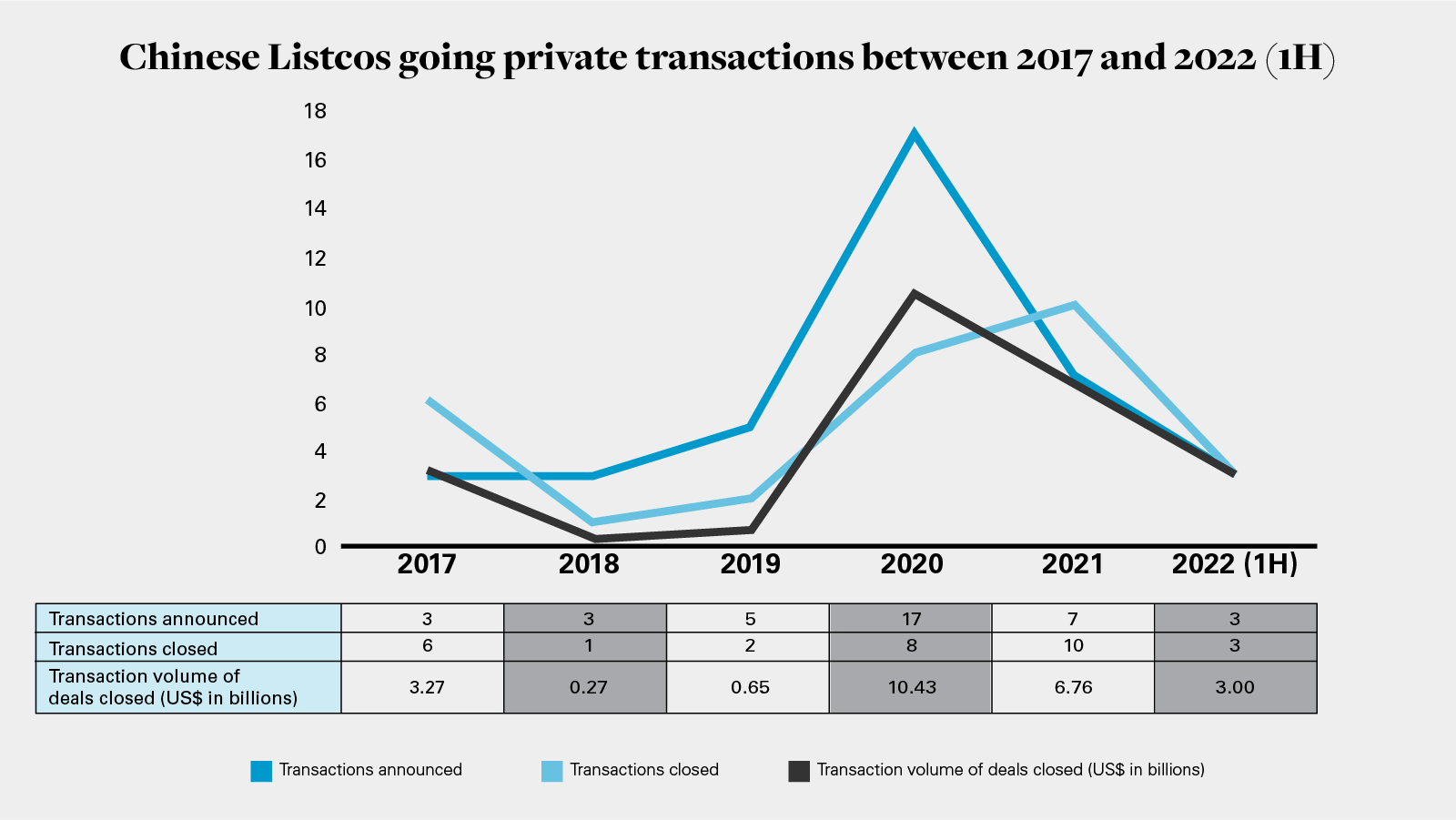

Overall, going-private transactions involving Chinese Listcos have been on the rise since 2019, as shown in the below chart. We saw a strong rebound of going-private activities of Chinese Listcos since 2019, which continued in 2021 and the first half of 2022.

View full image: Chinese Listcos going private transactions between 2017 and 2022 (1H) (PDF)

View full image: Chinese Listcos going private transactions between 2017 and 2022 (1H) (PDF)

Please refer to the Appendix for more details on going-private transactions of Chinese Listcos that closed in 2020, 2021 and the first half of 2022.

i. Targets remain mostly incorporated in Cayman Islands

The jurisdiction of incorporation of the target dictates many features of a going private transaction – the fiduciary duties of the directors, litigation risk profile, shareholder approval requirements and deal structuring options, to name a few. Most Chinese Listcos have been incorporated in the Cayman Islands for a variety of reasons, often related to administrative ease, cost, familiarity and tax. As a result, many Chinese Listco going-private transactions have necessarily involved Cayman-incorporated issuers (approximately 74% of all such deals since 2020), and have thus continued to build on the accretion of legal norms and precedence for these types of transactions.

In the Cayman Islands, a merger can be effected with shareholder approval comprising 2/3 majority of the votes cast on the resolution by the shareholders present and entitled to vote at a quorate meeting. Compared to most US jurisdictions, where the threshold is typically a simple majority of all shares, this "super-majority" threshold has generally been accepted as a sufficient threshold for participants in these conflict transactions, without the need for an additional "majority-of-the-minority" condition, which is a staple of market practice in the US. This additional condition serves largely to help ensure a lower standard of review by courts in the US when participants are invariably subject to stockholder litigation. For these Chinese Listcos, this type of litigation has largely not been of concern. More importantly, as a practical matter, the controllers/buyers of these targets simply do not agree to cede the fate of what would otherwise be a foregone conclusion into the hands of others. One type of litigation, however, that has become ubiquitous in these transactions is the shareholder-initiated appraisal proceeding (discussed further below). Generally, the impact of these at times significant appraisal proceedings will unlikely shift the selection of jurisdiction for future Chinese Listcos.

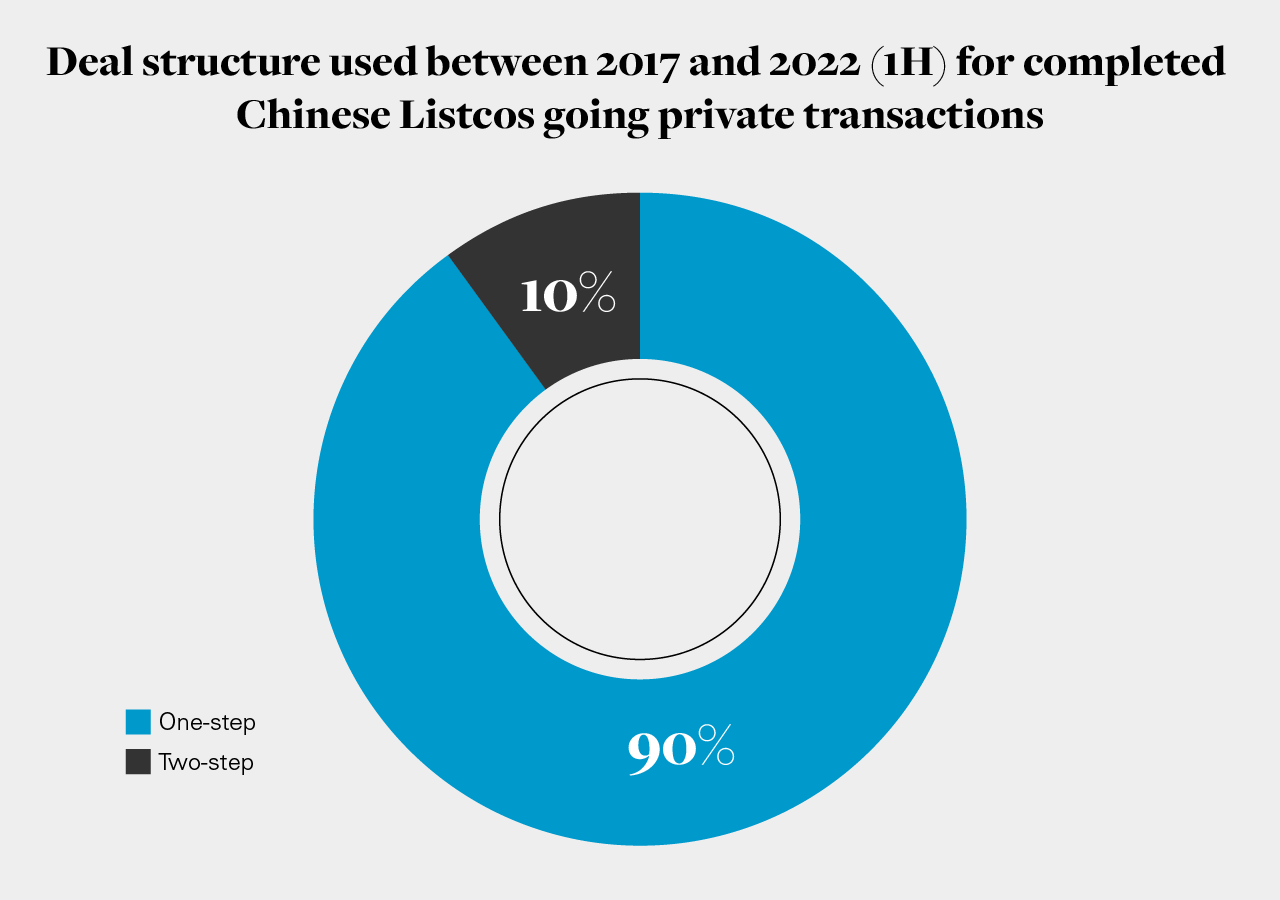

ii. Deal structure: one-step merger structure dominates

Going-private transactions are often structured as either a one-step or two-step merger:

- One-step: the buyer and the target agree to a merger via, typically, a "reverse triangular merger", which results in the target becoming a wholly-owned subsidiary of the buyer, subject to the requisite shareholder approval; and

- Two-step: the buyer, as a first step, launches a tender offer to the target's shareholders in which it will seek to acquire, typically, enough shares to allow it to definitively secure the requisite approval for a merger (often, in the form of a "short form" merger which can be achieved by a simple written resolution by the buyer after acquiring those shares), followed by the second-step merger to cash out those shareholders who do not tender their shares in the offer.

The traditional wisdom in the US market is that a two-step transaction allows a buyer to complete an acquisition more quickly than a one-step transaction under certain, but not all, circumstances. Factors that affect this calculus include financing, regulatory approval and capitalization.

Because Chinese Listcos often have controlling shareholder(s) who already hold the requisite voting power to effect a merger unilaterally, there has generally been no need to acquire additional shares in a tender offer. These going-private transactions are also often highly leveraged, a factor which cuts in favor of a one-step transaction. However, for a brief period in the recent past, tender offers were used by some buyers who already held the requisite vote to effect a one-step merger to acquire enough shares to effect a short-form merger (which requires approval by 90% of the votes cast for Cayman Island targets). This phenomenon was largely driven by participants seeking to obviate the dissenter playbook on account of an ambiguity as to whether dissenters' rights applied in such short-form transactions – an ambiguity which has since been clarified by the courts in favor of the arbitrage/hedge funds (i.e., dissenting shareholders).

The figures below depict (i) these trends of one-step vs. two-step mergers; and (ii) the time lapse between signing and closing for going-private transactions of Chinese Listcos between 2017 and 2022.

View full image: Deal structure used between 2017 and 2022 (1H) for completed Chinese Listcos going private transactions (PDF)

View full image: Deal structure used between 2017 and 2022 (1H) for completed Chinese Listcos going private transactions (PDF)

View full image: Time between signing and closing of Chinese Listco going private transactions between 2017 and 2022 (1H) (PDF)

View full image: Time between signing and closing of Chinese Listco going private transactions between 2017 and 2022 (1H) (PDF)

b. What are some key legal issues in going-private transactions of Chinese Listcos?

i. Appraisal rights proceedings

Since 2017, all Chinese Listco going-private transactions involving Cayman Islands incorporated targets have resulted in appraisal claims under the Cayman Islands "fair value" statute. What started as a niche market for arbitrage and hedge funds looking to capitalize on these transactions where typical US plaintiffs' actions could not, has blossomed into a full-fledged cottage industry and, more practically, an unavoidable transaction expense for buyers.

Appraisal proceedings for Cayman-incorporated Chinese Listcos stole the spotlight in 2017 with the Grand Court in the Cayman Islands handing down the first judgment on the matter for a Chinese Listco in respect of Shanda Games, ruling that the fair value of the shares at issue was more than double the merger price. Before then, there had been only one other ruling in 2015, involving a non-Chinese company. Since Shanda Games, there have been only a handful of participants that actually chose to litigate and, therefore, there have only been a handful of rulings. The majority of these claims have settled confidentially. Since 2015, there have been 29 petitions filed with the Grand Court and only five of these petitions have made it to trial and judgment by the Cayman court. To date, all of these judgments have resulted in an uplift on the merger consideration (ranging from 1% to 80%). These judgments have not revealed any single rubric for how valuations are determined, which are inherently expert-driven and singular to the facts and circumstances of each case. Often, there has been a blended approach, combining a variety of valuation methodologies, including taking into account deal price, trading price and a discounted cash-flow analysis.

The conventional advice is for parties to ensure the deal process is absolutely rigorous and fair as to (i) price and (ii) process. Notably, where the approval of a transaction is a foregone conclusion and there is no vibrant market check process, the fairness of deal process and pricing is naturally questioned, and the probity of deal price or trading price as a factor in determining fair value is diminished; the inverse, however, has also been seen to be true.

The traditional legal protection for buyers has been to require a closing condition that not more than a certain percentage of shares have dissented. The condition theoretically will provide a buyer some leverage against a mounting dissenter bloc and potentially cap exposure, but buyers have increasingly been less successful in negotiating these protections (the condition has been observed in roughly half of applicable deals in recent history, with the threshold generally around 10%). We also do not see a correlation between having such a closing condition and the actual percentage of dissenting shares. While the concession may be argued as a quid pro quo for a buyer receiving absolute certainty in executing a deal, some buyers may take a more practical view –– that they will end up waiving the condition anyway and may be able to trade the ask for more quantifiable benefits such as a better deal price.

ii. Consortiums

Sponsors typically form consortiums to undertake larger transactions and to spread the risk associated with a particular going-private transaction among multiple sponsors. Sponsor consortiums will need to address certain pre-signing and pre-closing matters in a going-private transaction, including (i) financing allocations; (ii) transaction expense and breakup fee sharing; (iii) defaulting or leaving consortium members; (iv) regulatory approval; and (v) governance/control of the consortium (both pre- and post-deal).

Where management is also involved in the consortium, as is common in the case of Chinese Listcos, additional consideration should be given to how equity is "rolled", including alignment on tax planning and issues as between sponsors and management. The timing of any discussions between the consortium and other possible management participants, as well as discussions regarding future employment terms, compensation and benefits arrangements, needs to be carefully considered in light of the fiduciary obligations of the target's board of directors, as well as disclosure considerations for the transaction. To minimize conflicts of interest, discussions are sometimes postponed until later in the process, after price and other transaction terms have been finalized and, in certain circumstances, after receipt of shareholder approval.

iii. Special committees and deal dynamics

To date, most going-private transactions involving Chinese Listcos (and, in particular, Cayman-incorporated ones) have followed a fairly well-defined paradigm in terms of deal structuring, terms and process. Special committees, which are formed in response to receipt of offers from an affiliate/controller of the target, benefited from this consistency in several ways, as there is a clear understanding of what both the market and their fiduciary duties would dictate. However, as the market has grown and investors become more intertwined with the fabric of Chinese growth, sole-founder controlled issuers will and have begun to be less prevalent, in favor of jointly controlled enterprises between sponsors or sponsors and management. The shifting landscape may lead to differential dynamics for transactions in the future, potentially opening the doors to features that may have been considered anathema to the traditional going-private transactions in recent memory – robust market checks, interlopers, or others.

iv. Public disclosure considerations

A potential buyer may have disclosure obligations under Regulation 13D if the buyer is (i) a more than a 5% "beneficial owner" (i.e., persons who have or share voting or dispositive power over the relevant securities) or (ii) a group of shareholders that collectively "beneficially own" more than 5% of a class of registered equity securities of the target. The SEC requires that a Schedule 13D amendment must be filed promptly after the buyer forms a "plan" to engage in a transaction or makes a proposal for a potential transaction, which is not when a merger agreement is signed or a tender offer is commenced. A person who previously filed a Schedule 13G is generally required to file a Schedule 13D within ten days after it forms the intent to change or influence control of the target. Therefore, sponsors need to consider the timing of making a proposal or participating in a buyer consortium, taking account of these disclosure implications.

In the Schedule 13D, the buyer must disclose information relating to its identity, the source and amount of funds used to purchase the shares owned, the purpose of the purchases, any plans or proposals involving the target and any agreements or arrangements it has with respect to the shares. A party that has filed a Schedule 13D is required to amend it promptly to disclose any material (i.e., more than 1%) increase or decrease in the number of securities it beneficially owns, or any change in its investment intent.

v. Regulatory approvals

Going-private transactions may implicate regulatory approval requirements in the US, as well as regulatory requirements in China for Chinese Listcos. Outbound investments in offshore target assets by a Chinese investor is subject to a series of outbound investment approval, filing and reporting requirements with applicable Chinese government authorities, depending on the location and industry of the target assets, the investment amount and the identity and ownership structure of the Chinese investor. An outbound investment made by Chinese individual investors through onshore or controlled offshore vehicles will be subject to the filing or reporting mechanisms of the National Development and Reform Commission (NDRC) and the Ministry of Commerce (MOFCOM).

National security approval (including CFIUS), antitrust and other regulatory approvals that apply to going-private transactions are comparable with other private acquisitions, but substantive antitrust concerns are less likely to arise because, typically, continuity of control will be maintained. However, the increased scrutiny of regulatory bodies in the US of Chinese Listcos, including developments in CFIUS enforcement as evidenced by a number of failed transactions, such as Magnachip-Wise Road, may result in possible concerns for less traditional going-private transactions (e.g., where the Chinese Listco has some operations outside of China), and certainly should be an area of focus for traditional cross-border acquirers looking to pursue a US public acquisition.

With the advent of more proactive regulators and expanding regulation seen across many jurisdictions beyond China and the US, antitrust and foreign investment review implications across the target's geographic footprint will also warrant early attention when evaluating take-private transactions.

4. Going dark

Chinese Listcos can voluntarily delist their securities and deregister under the U.S. Securities Exchange Act of 1934 (the "Exchange Act"), provided they satisfy certain conditions. The most recent examples of Chinese Listcos going dark that we have seen include Didi Global Inc. and Huaneng Power Internal, Inc. Both companies announced shareholders' approval for delisting and filed for delisting in June 2022.21

a. Delisting: Delisting refers to the withdrawal of listing from a US national securities exchange. To voluntarily delist, an issuer needs to (i) provide a written notice to the relevant stock exchange announcing the intent to delist securities; (ii) publish a press release to provide notice of delisting and the intention and reasons for delisting, (iii) for NYSE-listed issuers, provide board resolutions authorizing the delisting; (iv) file a current report on Form 6-K (or equivalent) to announce the intention to delist, and (v) file Form 25 with the SEC to complete the delisting process. Form 25 automatically becomes effective and delist the securities of an issuer after ten days of filing, and terminates reporting obligations of such issuer under Section 12(b) of the Exchange Act after 90 days of filing, which is the reporting obligations by virtue of a class of securities being listed on a US national stock exchange.

b. Deregistration: Deregistration refers to the withdrawal from registration under the Securities Act and the termination of reporting obligations under the Exchange Act. Assuming they are qualified as foreign private issuers, Chinese Listcos may rely on Rule 12h-6 of the Exchange Act to deregister through a streamlined process when they meet the following criteria: (i) having been a reporting company for at least one year and filed or submitted all Exchange Act reports required for this period (including at least one annual report); (ii) not having made a registered offering in the US for the past 12 months (with limited exceptions); (iii) having maintained a non-US listing, which is its primary trading market, that constituted at least 55% of its trading in a recent 12-month period; and (iv) (a) the average daily trading volume (the "ADTV") of the issuer's shares during a recent 12-month period must not be greater than 5% of the ADTV of the issuer's shares on a global basis; or (b) the issuer has fewer than 300 holders who are US residents or fewer than 300 holders worldwide, on a date falling within 120 days of filing the requisite notice to the SEC; provided that there is a further 12-month waiting period if the issuer did not meet the 5% ADTV test when delisted.

5. Conclusion and outlook

As we are now in the second half of 2022, the regulatory landscape and scrutiny over Chinese Listcos are still developing and the forecast following this perfect storm remains unclear. While there is some measured optimism in the air, it remains paramount for Chinese Listcos and their advisors to continue to carefully assess potential options and their implications with vigilance. With more than 150 Chinese Listcos having been conclusively identified as Commission-Identified Issuers in 2022, it is certainly high time that Chinese Listcos consider their options and prospects of continued listing in the US and prepare to respond to further developments with utmost preparation. Across various market and regulatory factors, conditions are ripe for going-private transactions to be on the rise again in the second half of 2022 and in 2023.

Appendix

Going-private transactions closed in 2020, 2021 and 2022 (1H)22e

| No. | Target | Target jurisdiction | Merger consideration | Date of receipt of proposal | Date of definitive agreement | Date of completion | Merger structure | Buyer consortium | Debt financing |

|---|---|---|---|---|---|---|---|---|---|

| 1. | Gridsum Holding Inc. | Cayman Islands | US$41 million | July 16, 2019 | October 1, 2020 | March 25, 2021 | One-step | Management buyout (led by Chairman/CEO) | N/A |

| 2. | Changyou.com Limited | Cayman Islands | US$188 million | September 9, 2019 | January 24, 2020 | April 17, 2020 | One-step | Sohu.com Limited (controlling shareholder) | US$250 million term loan facility |

| 3. | Bitauto Holdings Limited | Cayman Islands | US$1.035 billion | September 13, 2019 | June 12, 2020 | November 5, 2020 | One-step | Hammer Capital Private Investments Limited, Tencent Holdings Limited (an existing shareholder) | N/A |

| 4. | China Biologic Products Holdings, Inc. | Cayman Islands | US$1.450 billion | September 18, 2019 | November 19, 2020 | April 20, 2021 | One-step | Management, Beachhead Holdings Limited, CITIC Capital Holdings Limited, Hillhouse Capital Management, Ltd., Parfield International Ltd., PW Medtech Group Limited, Temasek Life Sciences Private Limited | US$1.1 billion senior term loan |

| 5. | Jumei International Holding Limited | Cayman Islands | US$127 million | January 12, 2020 | February 25, 2020 (Tender offer launched on February 26, 2020) | April 14, 2020 | Two-step | Management buyout (led by Founder/Chairman) | US$116 million term loan |

| 6. | 58.com Inc. | Cayman Islands | US$7.135 billion | April 2, 2020 | June 15, 2020 | September 18, 2020 | One-step | Management buyout (led by Chairman/CEO) | US$2 billion senior term loan; US$1.5 billion cash bridge facility |

| 7. | China XD Plastics | BVI | US$40 million | May 8, 2020 | June 25, 2020 | Terminated due to insider trading | One-step | Management buyout (led by Chairman/CEO) | Debt financing contemplated but no disclosure |

| 8. | Newater Technology, Inc. | BVI | US$20 million | May 12, 2020 | September 29, 2020 | July 13, 2021 | One-step | Management buyout (led by Chairman/CEO/CFO) | N/A |

| 9. | Sky Solar Holdings, Ltd. | Cayman Islands | US$35 million | May 26, 2020 | N/A (Tender offer launched on July 6, 2020) | October 8, 2020 | Two-step | IDG-Accel (24.3%), Japan NK Investment K.K. (36.3%), Jolmo Solar Capital Ltd., Sino-Century HX Investments Limited (controlled by Chairman Hao Wu) | US$40 million term loan facility |

| 10. | China Distance Education Limited | Cayman Islands | US$166 million | June 8, 2020 | December 1, 2020 | March 18, 2021 | One-step | Management buyout (led by Founder/Chairman) | US$200 million senior secured term loan facility |

| 11. | Yintech Investment Holdings Limited | Cayman Islands | US$155 million | June 22, 2020 | August 17, 2020 | November 18, 2020 | One-step | Management buyout (led by Founder/Chairman) | N/A |

| 12. | Fuling Global | Cayman Islands | US$11 million | June 22, 2020 | September 1, 2020 | November 23, 2020 | One-step | Management buyout (led by Founder/Chairwoman) | N/A |

| 13. | SINA Corporation | Cayman Islands | US$2.449 billion | July 6, 2020 | September 28, 2020 | March 22, 2021 | One-step | Management buyout (led by Chairman/CEO) | US$832m and US$1.2 billion term loans |

| 14. | Sogou Inc. | Cayman Islands | US$2.135 billion | July 27, 2020 | September 29, 2020 | September 23, 2021 | One-step | Tencent Holdings Limited (controlling shareholder owning 52.3%) | N/A |

| 15. | 51Job Inc. | Cayman Islands | US$1.959 billion | September 17, 2020 | June 21, 2021 | May 6, 2022 | One-step | Management buyout (led by Founder) | US$550 million senior term loan facility; US$1.325 billion cash bridge facility |

| 16. | Wanda Sports Group Company Limited | PRC | US$99 million | September 30, 2020 | N/A (Tender offer launched December 23, 2020) | April 9, 2021 | Two-step | Dalian Wanda Group Co., Ltd. (controlling shareholder) | N/A |

| 17. | Acorn International, Inc. | Cayman Islands | US$53 million | August 18, 2020 | October 13, 2020 | January 29, 2021 | One-step | First Ostia Port Ltd (led by Founder/Chairman) | US$10 million loan |

| 18. | Ruhnn Holding Limited | Cayman Islands | US$166 million | November 25, 2020 | February 3, 2021 | April 20, 2021 | One-step | Management buyout (led by Founder and Chairman) | N/A |

| 19. | Fang Holdings Ltd. | Cayman Islands | US$115 million | November 30, 2020 | N/A | Withdrawn on June 1, 2021 | One-step | General Atlantic LLC (existing shareholder) | N/A |

| 20. | China Customer Relations Centers, Inc. | Virginia | US$34 million | November 30, 2020 | March 12, 2021 | July 6, 2021 | One-step | Management buyout (led by Founder/Chairman) | N/A |

| 21. | Tarena International, Inc. | Cayman Islands | US$147 million | December 8, 2020 | April 30, 2021 | Withdrawn on November 15, 2021 | One-step | Management buyout (led by Founder/Chairman) | N/A |

| 22. | Secoo Holding Limited | PRC | US$188 million | January 11, 2021 | N/A | Withdrawn on May 23, 2022 | One-step | Management buyout (led by Founder/Chairman) | N/A |

| 23. | New Frontier Health Corporation | Cayman Islands | US$741 million | February 10, 2021 | August 4, 2021 | January 26, 2022 | One-step | Management buyout (led by Chairman) | US$500 million senior secured credit facility |

| 24. | China Zenix Auto International Ltd | BVI | US$57 million | August 10, 2021 | October 19, 2021 | January 28, 2022 | One-step | Management buyout (led by Chairman/CEO) | N/A |

| 25. | Hollysys Automation Technologies Ltd. | BVI | US$1.471 billion | September 12, 2021 | N/A | Withdrawn on January 24, 2022 | One-step | Loyal Valley Capital, Zhejiang Longsheng Group Co., Ltd. | N/A |

| 26. | iClick Interactive Asia Group Limited | Cayman Islands | US$580 million | September 24, 2021 | N/A | N/A | N/A | PAG Pegasus Fund LP, Oasis Management Company Ltd. | Debt financing contemplated in proposal |

| 27. | So-Young International Inc. | Cayman Islands | US$393 million | November 22, 2021 | N/A | N/A | One-step | Management buyout (led by Chairman and CEO) | Debt financing contemplated in proposal |

| 28. | Hailiang Education Group Inc. | Cayman Islands | US$368 million | December 23, 2021 | May 9, 2022 | N/A | One-step | Management buyout (led by Founder) | N/A |

| 29. | Glory Star New Media Group Holdings Limited | Cayman Islands | US$61 million | March 14, 2022 | July 11, 2022 | N/A | One-step | Management buyout (led by Founder/CEO) | Debt financing contemplated in proposal |

| 30. | VNET Group Inc. | Cayman Islands | US$1.184 billion | April 11, 2022 | N/A | N/A | One-step | Industrial Bank Co., Ltd., The Hina Group | Debt financing contemplated in proposal |

| 31. | Bluecity Holdings Ltd. | Cayman Islands | US$47 million | April 18, 2022 | April 30, 2022 | N/A | One-step | Management buyout (led by Founder) | N/A |

1 U.S. Securities and Exchange Commission, Provisional List of Issuers Identified under the HFCAA and Conclusive List of Issuers Identified under the HFCAA.

2 Accelerating Holding Foreign Companies Accountable Act, H.R. 6285, 117th Cong.§2 (2021).

3 See NYSE Listed Company Manual, §802.01D, and Nasdaq Listing Rules, §5810 (c)(1).

4 SEC Edgar System, Form 6-K of China Mobile Limited (January 8, 2021).

5 U.S. Securities and Exchange Commission, Form 20-F, item 16I(b).

6 China Securities Regulatory Commission, CSRC Official of Department of International Affairs Answered Reporter Question (March 31, 2022).

7 China Securities Regulatory Commission, Provisions on Strengthening Confidentiality and Archives Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments; April 1, 2022).

8 Reuters, Chinese regulators ask some U.S.-listed firms to prepare for audit disclosure (March 22, 2022).

9 Katanga Johnson, Reuters, U.S. regulators see deal with Beijing on audits as 'premature,' will continue to engage (March 24, 2022).

10 YJ Fischer, US Securities and Exchange Commission, Resolving the Lack of Audit Transparency in China and Hong Kong: Remarks at the International Council of Securities Associations (ICSA) Annual General Meeting (May 24, 2022).

11 Hong Kong Stock Exchange Main Board Listing Rules, Chapter 1, §1.01.

12 Hong Kong Stock Exchange, Hong Kong Stock Exchange Guidance Letter HKEX-GL94-18.

13 Hong Kong Stock Exchange Main Board Listing Rules, Chapter 8A, §8A.46.

14 Hong Kong Stock Exchange Main Board Listing Rules, Chapter 8A, §8A.06.

15 Hong Kong Stock Exchange Main Board Listing Rules, Chapter 7, §7.14.

16 Hong Kong Stock Exchange Main Board Listing Rules, Chapter 19C, §19C.05A.

17 Ibid.

18 Hong Kong Stock Exchange Main Board Listing Rules, Chapter 19C, §19C.05.

19 Hong Kong Stock Exchange Main Board Listing Rules, Chapter 19C, §§19C.11B, 19C.11C.

20 Hong Kong Stock Exchange, Hong Kong Stock Exchange Guidance Letter HKEX-GL112-22.

21 SEC Edgar System, Form 25 of Didi Global Inc. (June 2, 2022); Form 25 of Huaneng Power Internal, Inc. (June 27, 2022).

22 This table of going-private transactions closed in 2020, 2021 and 2022 (1H) is ordered in accordance with the date of receipt of proposal from buyers.

Ronny Ren (Legal Manager, White & Case LLP, Hong Kong) co-authored this publication

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP