Decarbonizing in a downturn: Can the mining & metals sector afford (not) to change?

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

Russia's actions in Ukraine fueled an unprecedented rally in mineral and metal prices earlier this year, with multiple metals breaking historical records. However, this rally was short-lived. Within six months, metal prices collapsed back to 2020 levels in the most volatile first half of the year. There are myriad factors that are lining up to cap mineral and metal prices in the coming months, the most significant of which, we believe, is the rapid deterioration of the global economy.

In recent times, the mineral commodities cycle has been out of synchronization with the global macro-economic cycle—this time the cycles appear to be converging. With the prospect of global downturn looming, we ask the question, "Is the mining & metals sector prepared?" Is the sector truly resilient to disruption in supply chain, inflationary pressures, headwinds on demand, increased funding costs and of course, the drive to net-zero? Or will China's fiscal and monetary policies and the latest legislative developments in US and EU regulation provide enough support to the sector so that miners and the rest of the supply chain can capably respond to market conditions? Can the ESG agenda and decarbonization projects contribute to the long-term sustainability of the sector itself?

We are thinking critically about what a downturn means and whether this could, in fact, be a major opportunity to distinguish the sector from its traditionally dominant counterpart, the oil & gas sector. We hope you find Mining & Metals 2022: Putting the Resilience Rhetoric to the Test a stimulating read.

The mineral commodities cycle, in recent times, has been out of synch with the global macro-economic cycle—this time the cycles appear to be converging

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

A steady supply of minerals critical to the energy transition must be ensured through the expected recession.

Mining & metals companies have been increasingly focusing on enhancing their environmental, social and governance credentials in recent years as part of the energy transition. But with a global recession looming, will they be able to maintain their commitment?

China is looking beyond its borders to maximize the returns from the minerals needed to make the energy transition happen.

Participants in the mining & metals supply chain will see many challenges—but also opportunities—in playing both offense and defense in an economic downturn.

Mining & metals companies can take advantage of low prices in the leveraged finance markets to manage their liabilities amid the expected recession.

Financial crime flourishes in a downturn, and the mining & metals sector is not immune to it. The sector faces a number of industry-specific risks, and will need to react to the ensuing likely surge in enforcement activity.

A steady supply of minerals critical to the energy transition must be ensured through the expected recession.

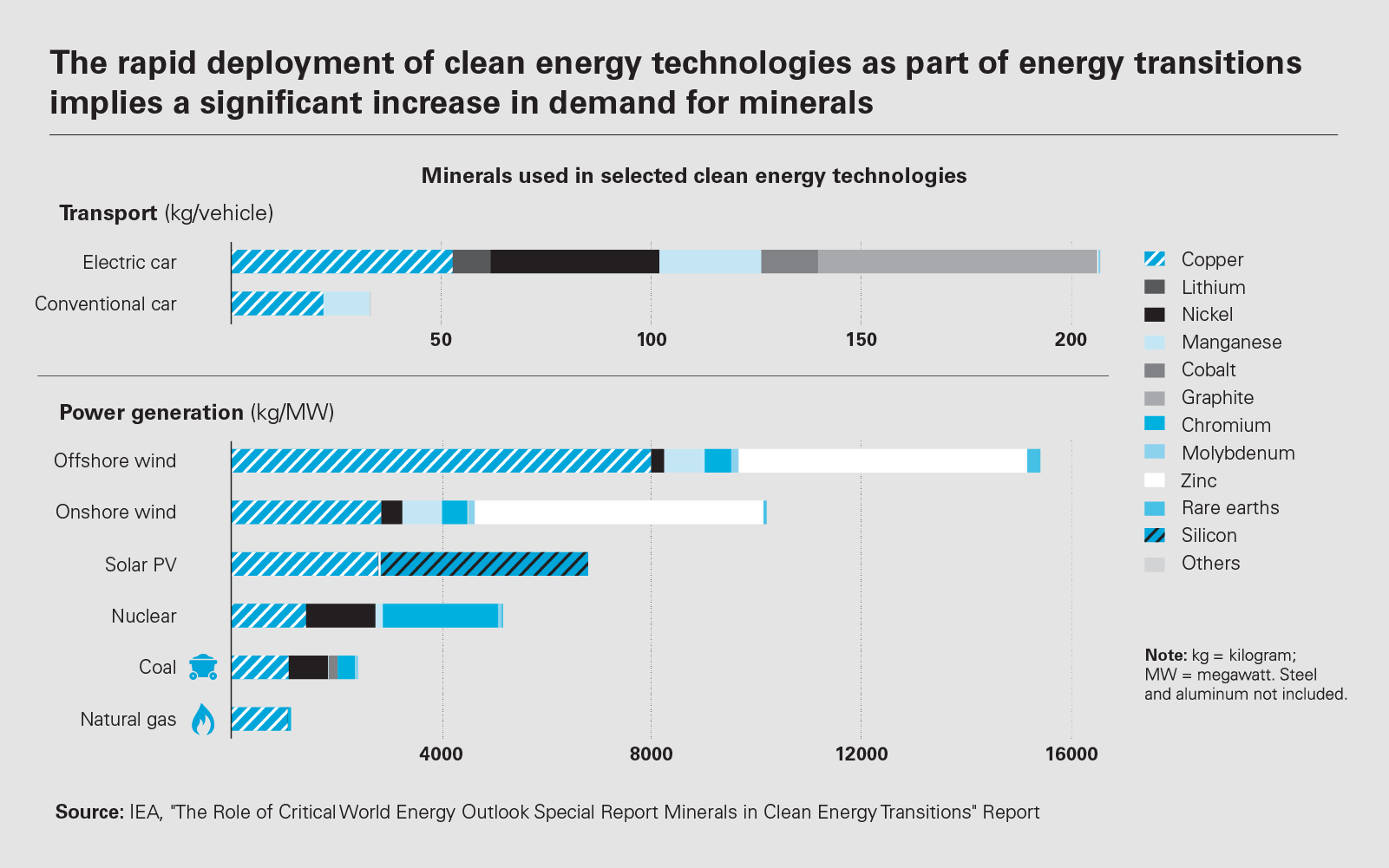

Technologies underlying the energy transition—including wind turbines, solar panels, electricity networks and electric vehicles (EVs)—rely upon sufficient access to critical minerals such as copper, lithium, nickel, cobalt, graphite, and rare earth elements.

As demand for these critical minerals skyrockets, and as governments increasingly view reliable access to these materials in national security as well as economic terms, bolstering supply chains has risen to the top of domestic policy agendas around the world. In order to support economies' transition to clean energy, governments are enacting policies to bolster domestic or friendly supply chains, often backed by significant funding.

Critical mineral production and processing is highly concentrated in a small number of countries, often with significant perceived political risk

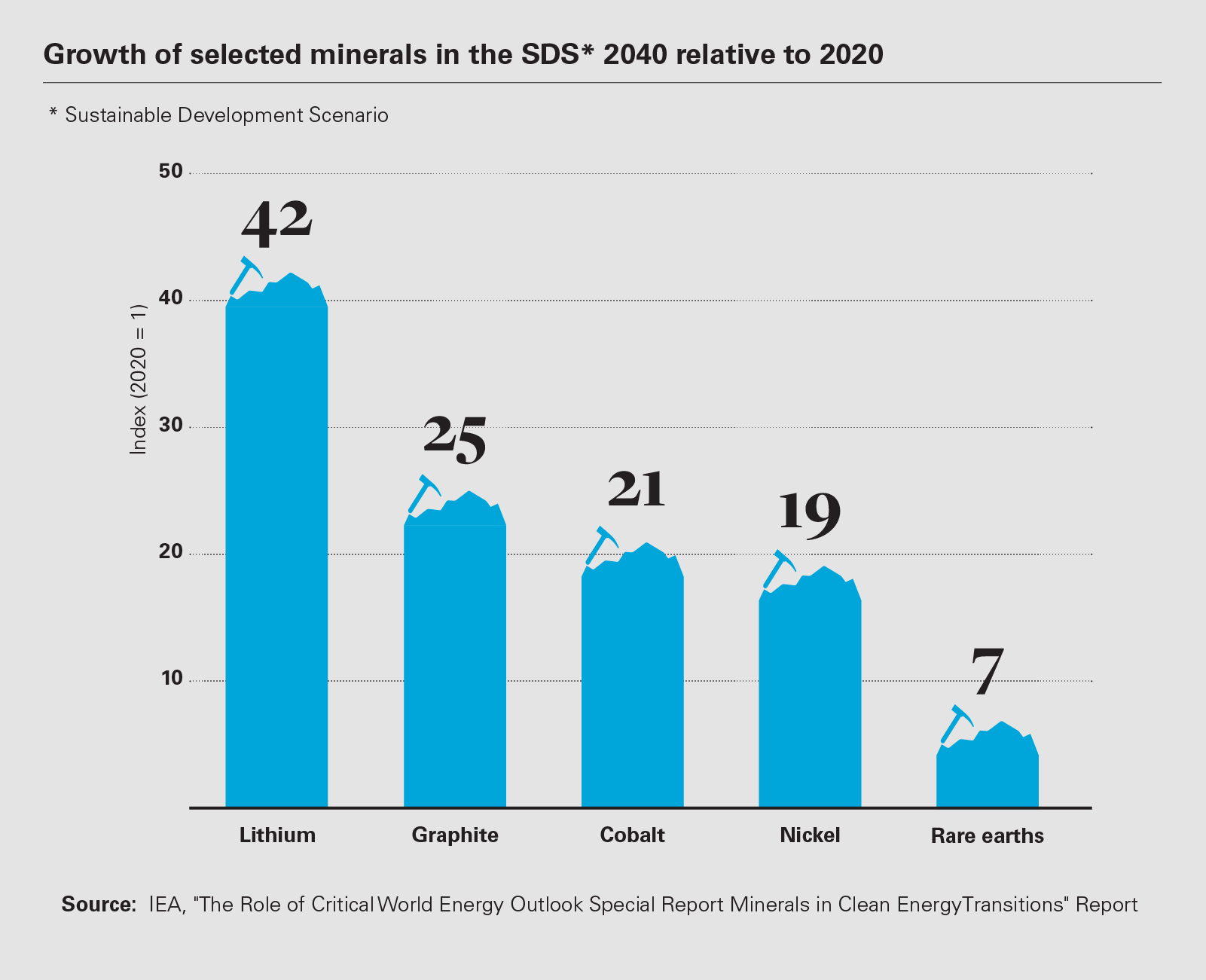

2m tons

Demand for lithium for use in lithium-ion batteries is expected to quadruple by 2030 to two million tons annually

Source: Market data

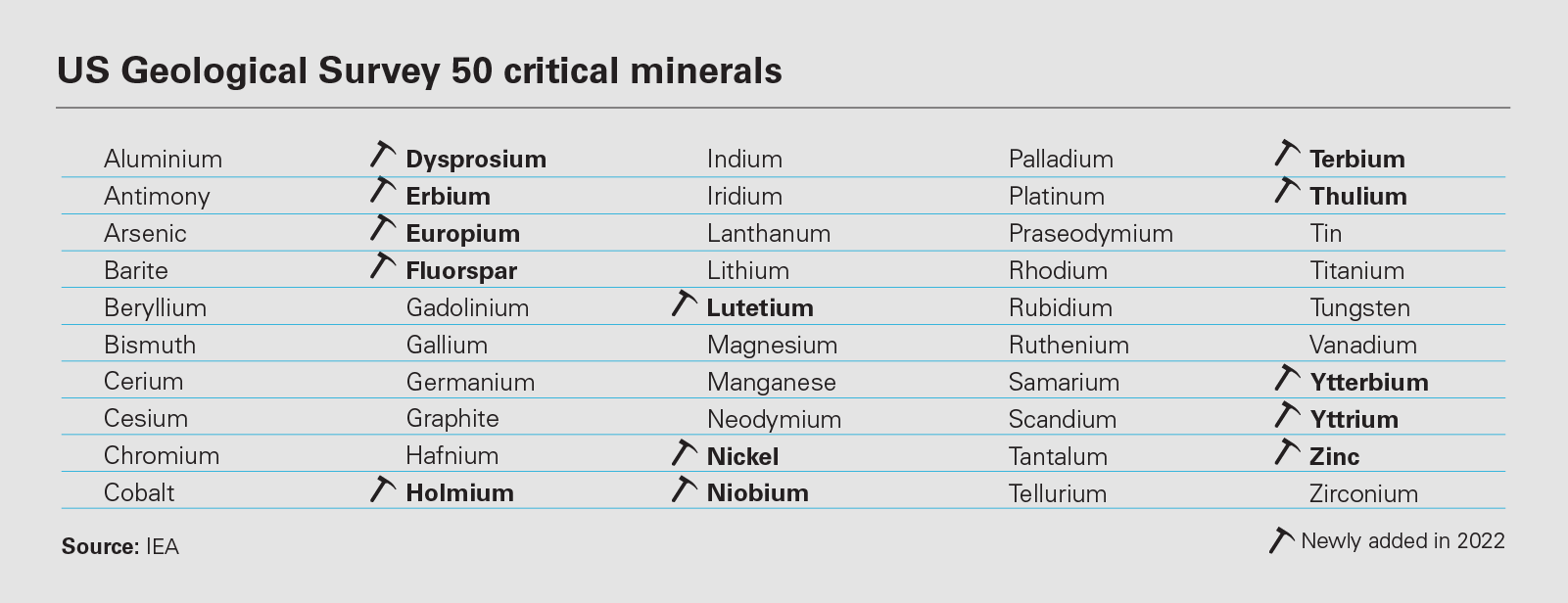

There is no definitive, global list of "critical minerals." The US Geological Survey issues an annual list, as defined by the US Energy Act 2020, drawn up using three evaluations. These include a quantitative evaluation of supply risk where sufficient data were available; a semi-quantitative evaluation of whether the supply chain had a single point of failure; and a qualitative evaluation when other evaluations were not possible.

Based on these criteria, the 2022 Final List of Critical Minerals includes 50 minerals, including aluminum, cobalt, graphite, iridium, lithium, magnesium, nickel, niobium, platinum, tin, titanium, tungsten and zinc. The White House said these minerals are "essential to economic or national security and vulnerable to disruption."

Other countries have different criteria of what defines a critical mineral, based on unique geological, trade and other contexts. As of 2020, 73 minerals had been identified as critical in 25 separate assessments.

Critical mineral production and processing is highly concentrated in a small number of countries, and often countries with significant perceived political risk. For example, rare earth elements such as neodymium and dysprosium—used in EVs, wind turbines and other technologies—are concentrated in China, Vietnam and Russia. A significant proportion of the world's cobalt is sourced from the Democratic Republic of the Congo.

Regardless of the location of the mines, China is the top processor of most critical minerals relevant to the energy transition, and also leads in the production of key intermediary products such as battery cells, polysilicon and wind turbine components.

A subset of these minerals are central to the energy transition, and are required in huge quantities. According to the International Energy Agency, because green power generation requires many times more mineral inputs than the fossil fuel-based equivalent, the average amount of mineral resources needed for a new unit of power generation capacity has increased by 50 percent since 2010. Alongside this, the share of renewables in new investment has also risen.

In order to keep pace with the projected growth of renewable energy production, EV sales and other elements of the global energy transition, the supply of critical minerals needs to expand rapidly. For example, demand for lithium, for use in lithium-ion batteries, is expected to quadruple by 2030 to two million tons annually, but at its current pace, mining capacity will fall short by 700,000 tons. Similarly, copper supply is projected to fall 4.7 million tons short of demand by 2030.

In addition to a desire to close the projected deficits, some governments are compelled to develop production capacity to mitigate potential geopolitical and economic risks inherent in certain critical mineral supply chains.

Investment in clean energy is, generally, a winning political issue. While the traditional energy sectors—and the communities reliant upon them—represent a powerful political constituency in many countries, most voters support at least a measured energy transition.

For example, the majority of Americans across the political spectrum support development of renewable energy sources, and two-thirds support incentives to increase the use of electric and hybrid vehicles.

The Biden administration has identified critical minerals as a key economic and national security priority and has moved quickly on the policy front to support these efforts. Polling also suggests broad popular support for the energy transition, and policies enacted to support it, in Europe, Canada and elsewhere.

As is often the case, it seems that political will follows public opinion. As long as advancing the energy transition is perceived as being politically popular, funding will continue to flow in that direction, regardless of the larger macroeconomic context.

As long as advancing the energy transition is perceived as being politically popular, funding will continue to flow, regardless of the larger macroeconomic context

August 16, 2022

US president Joe Biden signed the Inflation Reduction Act (IRA) 2022 into law

On August 16, 2022, US president Joe Biden signed the Inflation Reduction Act (IRA) 2022 into law. In addition to implementing core components of Biden's agenda on healthcare and tax reform, the IRA includes several funding provisions aimed at bolstering domestic and regional production of and demand for critical minerals—confirming that the US government is prepared to dedicate significant resources to the energy transition.

The IRA makes substantial revisions to the EV tax credit to require regional sourcing of critical minerals used in EV batteries. Section 13401 of the IRA revises the existing US tax credit of US$7,500 for purchases of new EVs. Eligibility for the revised credit, which will apply to both EVs and fuel cell or "clean" vehicles, will be contingent on the final assembly of the vehicle occurring in North America; initially, at least 40 percent of the vehicle battery's critical minerals originating from a US free trade agreement partner, or being recycled in North America; and specified percentages of the battery's components being manufactured in North America. Vehicles that satisfy this requirement will receive a tax credit of US$3,750.

The IRA will also provide an additional tax credit of US$3,750 if at least 50 percent of the battery's components are manufactured or assembled in North America—increasing to 100 percent by 2029. Additionally, after a short transition period, the IRA will make vehicles ineligible for the credit if the vehicle battery contains any critical minerals or components sourced from countries such as China and Russia.

The IRA introduces a new "advanced manufacturing" tax credit for domestic production of critical minerals. This tax credit would apply with respect to each eligible component that is produced by the taxpayer within the US and sold by the taxpayer to an unrelated person during the tax year.

Critical minerals are among the eligible components to which the tax credit would apply; the amount of the tax credit would be equivalent to 10 percent of the costs incurred by the taxpayer in producing the critical mineral. The new tax credit would also apply to several downstream products, including solar energy components, wind energy components, power inverters and battery components. The tax credit is projected to result in tax expenditures of approximately US$30 billion.

The IRA has additionally introduced a US$500 million appropriation for "enhanced" use of the Defense Production Act (DPA), which Biden recently invoked to support critical mineral production. The sponsors of the bill indicated that this appropriation is intended in part to support the president's recent action concerning critical minerals, which enabled the US Department of Defense to use DPA funds to encourage domestic mining and processing of such materials.

Finally, the IRA authorizes US$40 billion in loan guarantees under Title XVII of the Energy Policy Act of 2005. This enables the Secretary of Energy to make loan guarantees for projects that "avoid, reduce, utilize or sequester" air pollutants or anthropogenic emissions of greenhouse gases; and employ "new or significantly improved technologies" as compared to commercial technologies in service in the US. The authorization could bolster recent efforts to leverage the Title XVII program to support domestic production of critical minerals.

These new programs are in addition to existing loan and grant programs, such as under the Department of Energy's Loan Programs Office, which have recently been utilized for the first time to fund critical mineral processing projects in the US.

Australia's mining sector is vital to the country's overall economic health: it is the largest sector by share of national GDP, and minerals and fuels comprise more than half of all exports.

While Australia's top mineral products include iron ore, coal, gold and aluminum, the government has prioritized both the mining and processing of critical minerals and, because of its geological makeup, Australia is well positioned to capitalize on this. The country is already the largest global producer of lithium, providing half of the world's supply; the second-largest producer of cobalt; and the fourth-largest producer of rare earth elements.

In March 2022, the Australian government announced the 2022 Critical Minerals Strategy, seeking to grow the sector, expand downstream processing and meet future global demand. The strategy comprises three prongs.

To support private companies, the government established an AUD 2 billion critical minerals facility to provide financing to private companies. So far, the facility has provided loans to graphite mining and processing facilities and a rare earth elements refinery, among others.

The government also introduced the Critical Minerals Accelerator Initiative, meant to support early and mid-stage projects, with grants for feasibility studies, engineering design work, pilot testing, and other activities.

The strategy commits AUD 50 million in research and development funding through the new National Critical Minerals Research and Development Centre, and an additional AUD4 million to scope investment proposals for regional critical minerals hubs.

While not specifically allocating new funding, the government outlined additional international initiatives to cohere new global supply chains running through Australia, and attracting new foreign investment in the mining sector.

In addition, as part of the new AUD 15 billion National Reconstruction Fund, prime minister Anthony Albanese committed AUD 1 billion in investment through loans, equity, and guarantees for resources value-adding and mining science. Seen in the context of an overall lukewarm economic scenario, the continued allocation of funds to critical minerals and the energy transition demonstrates the Australian government's clear priorities.

The European Commission issued an Action Plan on Critical Raw Materials in 2020, which it said was focused on "actions to reduce Europe's dependency on third countries, diversifying supply from both primary and secondary sources, and improving resource efficiency and circularity while promoting responsible sourcing worldwide."

The action plan, which itself is aligned with the EU's Green Deal and Industrial Strategy plans, sets the framework for subsequent critical mineral-related policy measures, including the establishment of funding initiatives.

Europe contains significant deposits of certain critical minerals, detailed in the action plan. For example, Germany is a major producer of gallium, used in semiconductors and LEDs; Finland contributes half of the germanium consumed by EU countries, which is a component in fiber-optic technology; and France produces more than a quarter of the EU consumption of iridium, which goes into liquid crystal display screens.

However, the EU is a net exporter only of hafnium and indium, and remains highly dependent on China, Russia and other countries for most minerals necessary for clean energy technologies.

There exist EU-level financing opportunities for critical mineral projects, with more to come. The European Investment Bank offers financing to a range of industrial and energy projects, including those relating to the supply chain of critical raw materials needed for low-carbon technologies in the EU, and does not finance fossil fuel projects.

Significantly, a new European Raw Materials Fund is reportedly set to launch in 2023 with an initial investment of approximately €2 billion, and aims to devote €100 billion toward critical mineral production.

While details on the funding sources, timeline and eligibility criteria are not yet released, the fund could be an important continent-wide vehicle to support new mining and processing projects.

In addition, the EC is developing a Raw Materials Act, which would accelerate permitting and otherwise support European production of critical minerals. Whether or not the proposed act is tied to new funding programs, the keen legislative focus on strengthening supply chains for critical minerals points to the economic potential in Europe, as well as intensifying regional anxieties around overdependence on adversarial governments for these materials.

The EU-wide initiatives are bolstered at country level. For example, in France, the government has inaugurated a dedicated fund under the France 2030 investment plan to support critical mineral projects, which has thus far provided funding of €550 million to 40 projects.

In Spain, the Circular Economy Action Plan, backed by an investment package worth €1.5 billion, includes a plan to promote the reuse and recycling of raw materials in order to decrease the country's dependence on imports.

The US, Australia and the EU are not the only regions of the world that are spending enthusiastically on initiatives to support the domestic production and processing of critical minerals. In addition to the examples above, similar initiatives can be found globally.

For example, Canada has introduced a range of grant programs, and research and development spending. The UK published a critical mineral strategy in July 2022, which includes plans to allocate financial support to develop its minerals capabilities and rebuild the country's skills in mining and minerals.

Japan released its international resource strategy back in 2020, noting that there needed to be more investment in upstream equities, and develop infrastructure and human resources in this area.

Whether driven primarily by anxiety regarding Chinese dominance of critical mineral supply chains, or by a premonition of immense economic opportunity, funding and regulatory support for critical mineral development has risen to the top of the economic priority list, where it will remain for the foreseeable future, despite foreboding economic forecasts. Funding programs alone will not suffice, as permitting and other regulatory bottlenecks threaten to slow critical mineral mining projects.

However, given the political momentum, the participants in the mining & metals sector, especially those focused on the extraction and processing of critical minerals, are well positioned to not only survive, but thrive in the current macro-economic environment.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View image: US Geological Survey 50 critical minerals (PDF)

View image: US Geological Survey 50 critical minerals (PDF)

View image: The rapid deployment of clean energy technologies as part of energy transitions implies a significant increase in demand for minerals (PDF)

View image: The rapid deployment of clean energy technologies as part of energy transitions implies a significant increase in demand for minerals (PDF)

View image: Growth of selected minerals in the SDS* 2040 relative to 2020 (PDF)

View image: Growth of selected minerals in the SDS* 2040 relative to 2020 (PDF)