Decarbonizing in a downturn: Can the mining & metals sector afford (not) to change?

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

Russia's actions in Ukraine fueled an unprecedented rally in mineral and metal prices earlier this year, with multiple metals breaking historical records. However, this rally was short-lived. Within six months, metal prices collapsed back to 2020 levels in the most volatile first half of the year. There are myriad factors that are lining up to cap mineral and metal prices in the coming months, the most significant of which, we believe, is the rapid deterioration of the global economy.

In recent times, the mineral commodities cycle has been out of synchronization with the global macro-economic cycle—this time the cycles appear to be converging. With the prospect of global downturn looming, we ask the question, "Is the mining & metals sector prepared?" Is the sector truly resilient to disruption in supply chain, inflationary pressures, headwinds on demand, increased funding costs and of course, the drive to net-zero? Or will China's fiscal and monetary policies and the latest legislative developments in US and EU regulation provide enough support to the sector so that miners and the rest of the supply chain can capably respond to market conditions? Can the ESG agenda and decarbonization projects contribute to the long-term sustainability of the sector itself?

We are thinking critically about what a downturn means and whether this could, in fact, be a major opportunity to distinguish the sector from its traditionally dominant counterpart, the oil & gas sector. We hope you find Mining & Metals 2022: Putting the Resilience Rhetoric to the Test a stimulating read.

The mineral commodities cycle, in recent times, has been out of synch with the global macro-economic cycle—this time the cycles appear to be converging

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

A steady supply of minerals critical to the energy transition must be ensured through the expected recession.

Mining & metals companies have been increasingly focusing on enhancing their environmental, social and governance credentials in recent years as part of the energy transition. But with a global recession looming, will they be able to maintain their commitment?

China is looking beyond its borders to maximize the returns from the minerals needed to make the energy transition happen.

Participants in the mining & metals supply chain will see many challenges—but also opportunities—in playing both offense and defense in an economic downturn.

Mining & metals companies can take advantage of low prices in the leveraged finance markets to manage their liabilities amid the expected recession.

Financial crime flourishes in a downturn, and the mining & metals sector is not immune to it. The sector faces a number of industry-specific risks, and will need to react to the ensuing likely surge in enforcement activity.

Mining & metals companies have been increasingly focusing on enhancing their environmental, social and governance credentials in recent years as part of the energy transition. But with a global recession looming, will they be able to maintain their commitment?

The mining & metals industry, often considered a villain in the context of environmental sustainability, is now seen as a critical part of the solution. Investors and consumers increasingly recognize the industry as not only a first source of emissions in the value chain, but as a provider of critical raw materials needed for the global energy transition.

The way in which mining & metals companies position themselves in preparation for the energy transition, particularly against the backdrop of an expected recession, will determine their sustainability, and could make or break their competitive advantage over the next decade. Boards should consider how to build on existing environmental, social and governance (ESG) frameworks to ensure they are future-proofed for, and resilient against, tomorrow's economic realities.

Ensuring that ESG is fully integrated into long-term business strategies as a means to add value, rather than seeing it as a discretionary cost to be cut, will be a critical component in this goal.

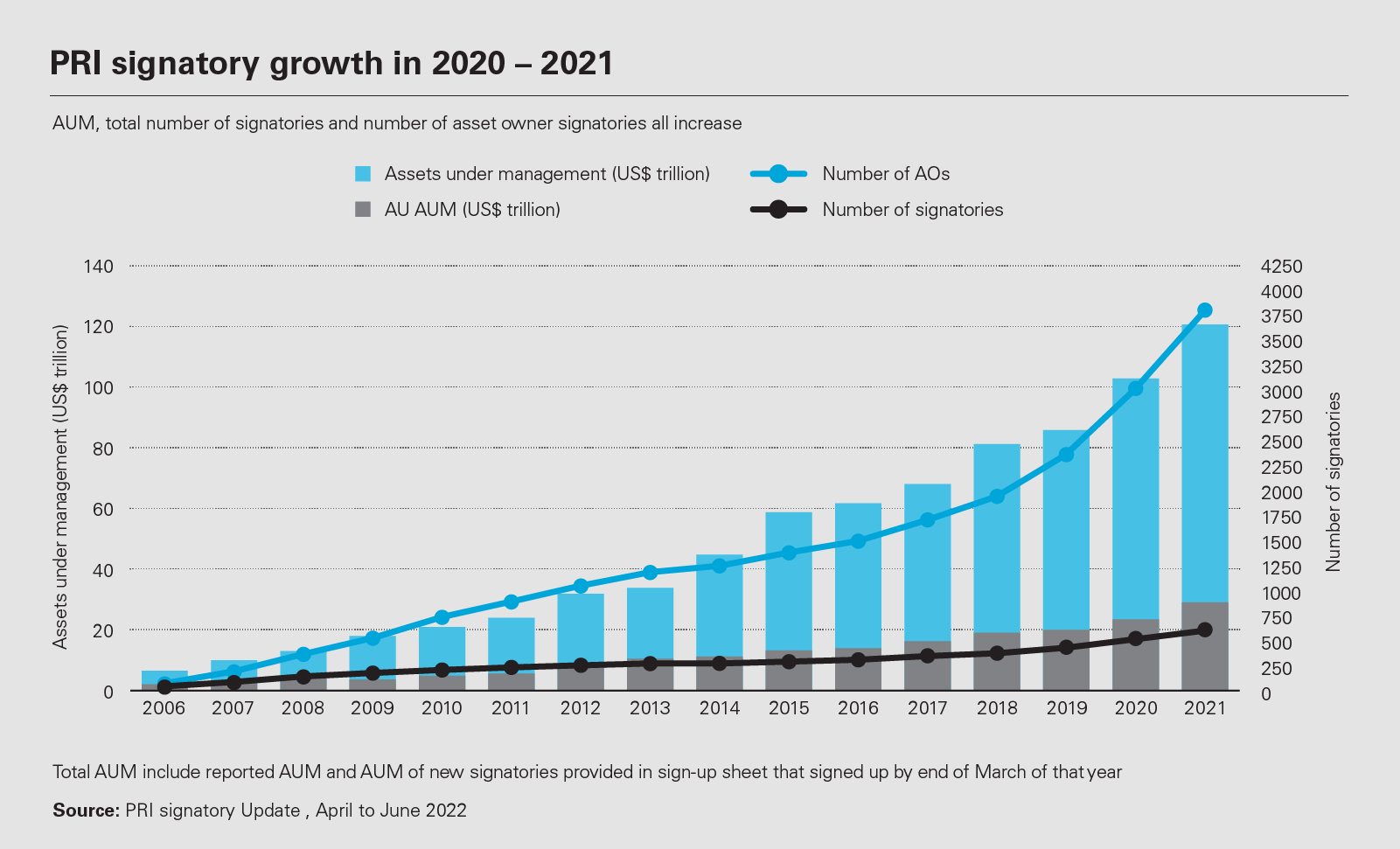

5,020

Signatories to the Principles of Responsible Investment as of September 2022

Source: PRI

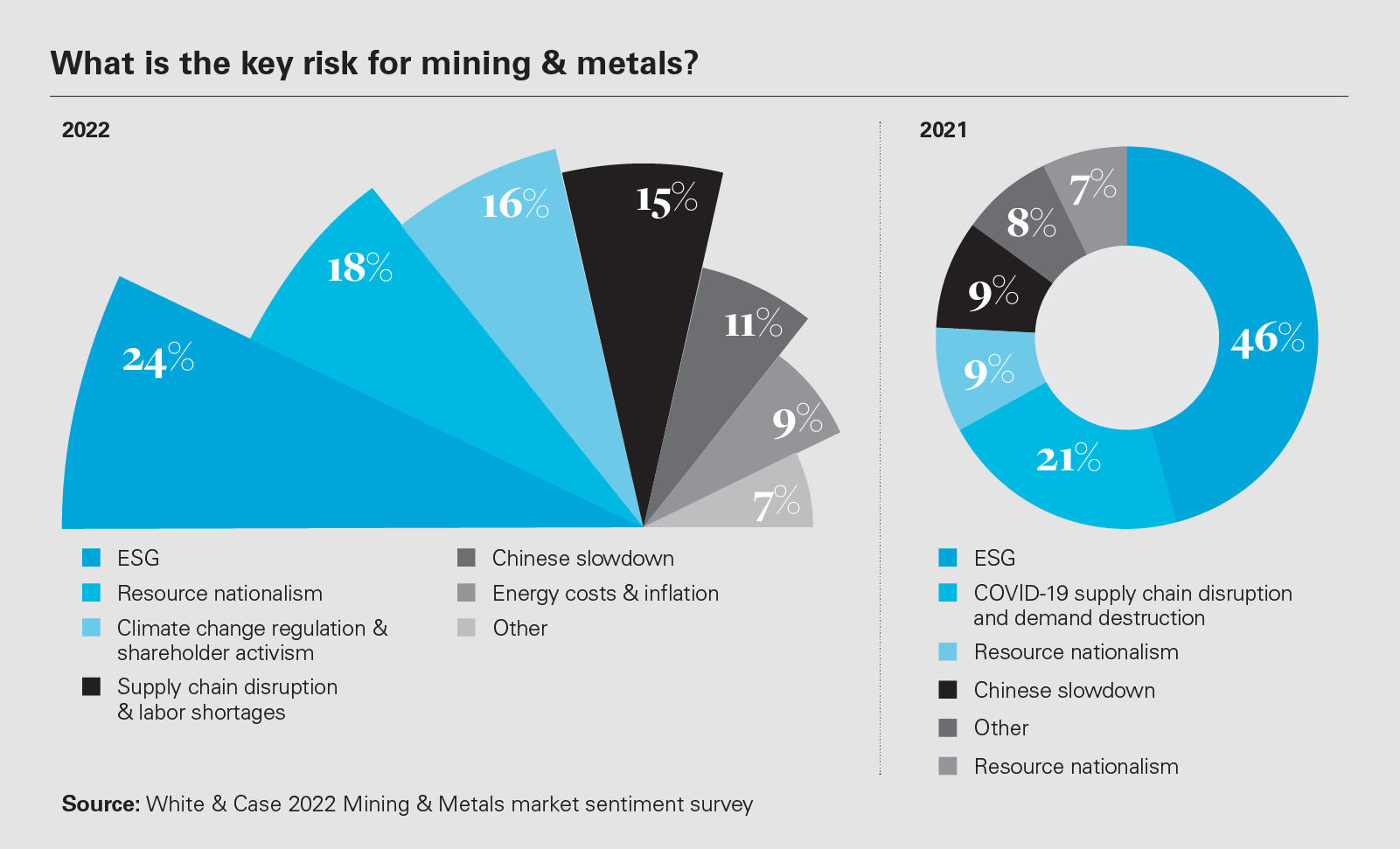

This will be the first real downturn where ESG is a focal point for stakeholders. In our 2022 Mining & Metals market sentiment survey, 24 percent of respondents viewed ESG issues as the biggest threat, rising to approximately 40 percent when climate-related activism and regulation is included. The perception of these risks may increase as the industry faces the anticipated global economic slowdown.

While The Economist recently argued that ESG investing "is a broken system [which] needs urgent repairs," it also emphasised that ESG seeks to make "firms and their owners accountable for their negative externalities." The high-profile ESG engagement priorities of BlackRock and State Street, as well as more than 5,000 investor signatories (as of April 2022) to the Principles of Responsible Investment, underscore the strength and breadth of investor commitment in this area, as do related proxy voting and activism trends.

ESG factors can create both risks and opportunities. Within the mining & metals sector, boards have been engaged in tackling a vast range of ESG issues for some time, including the approach to energy transition and greenhouse gas emissions, working conditions in supply chains, tailings management, worker and community health and safety, and compliance with ever-increasing reporting obligations.

However, during an economic downturn, leaders will need to decide which of these themes to prioritize, define the targets to be achieved, and set out expected timeframes—all against the backdrop of market and economic uncertainty.

Many still see an inherent trade-off between choosing a more sustainable future and achieving business growth and profit. They see ESG-related spending—a capital expense to reduce energy use, opting for renewable energy, paying living wages and so on—as purely cost, not investment.

Ahead of and during any recession, companies will be under considerable pressure to manage ESG factors while continuing to meet quarterly expectations. The deeper the challenge an executive team faces, the more tempting it becomes to cut corners, so boards must ensure governance standards remain aligned with market realities.

There is a growing body of evidence to demonstrate that taking ESG matters seriously is fundamental to resilience and long-term business success, as well as improving investment returns. Companies with strong ESG credentials have the ability to outperform peer groups and the wider market.

Mining & metals companies are spending heavily on efforts to reduce emissions or meet other targets, hoping for a payoff down the road. For example, investing in decarbonization requires significant upfront capital costs, but these can be offset through tax incentives and favorable financing terms. Decarbonization efforts can also improve energy efficiency, which has a direct impact on operating costs and margins, and reduce the risk of negative repercussions on a company's share price or regulator-enforced penalties.

63%

Of mining & metals investors said they would be willing to divest or avoid investing in mining companies that fail to meet their decarbonization targets or fail to pursue sufficient decarbonization activities.

Source: Accenture's Global Institutional Investor Study of ESG in Mining, 2022

Net-zero and the energy transition, along with the demand for energy transition technologies and minerals, will drive demand—and enormous annual growth in market value—for metals and critical minerals including nickel, lithium and copper. The shift to net-zero will require more mining, not less, and ESG drivers such as strong social licenses, responsible divestitures and tax transparency will all be critical for a company's continued success.

A global economic slump would mean a new wave of cost-cutting in mining & metals, in both operations and in capex, at a time of further spending commitments to meet increasing ESG demands from multiple stakeholders. Chief financial officers are under pressure overseeing companies' capital spending plans, as they enter unknown territory by allocating funds to projects that carry big price tags, cover long time horizons and yield returns that are sometimes hard to quantify.

Companies often make these investments before new regulations are proposed or consumer choices change, adding to the difficulty of finding the right balance. From a cost perspective, it is about balancing the trade-off between necessary expenditure and potential losses brought by ignoring or mismanaging ESG factors. ESG is no longer optional or a point of differentiation; it is now the minimum operating standard, especially in the mining & metals sector.

Once management determines the appropriate level of corporate investment in ESG in light of the expected returns or losses avoided during a recession, it then becomes critical for the company to communicate its approach to ESG priorities as part of its overall business strategy, through annual reports, proxy statements, sustainability reports or other public materials.

The 2022 Accenture Global Institutional Investor Study of ESG in Mining found 59 precent of investors want miners to aggressively pursue decarbonization and be market leaders in that effort. Approximately 63 percent of mining & metals investors said they would be willing to divest or avoid investing in mining companies that fail to meet their decarbonization targets or fail to pursue sufficient decarbonization activities.

This study found that environmental initiatives that are rated "important" by mining & metals investors in driving a significant valuation premium include lowering scope 3 emissions, targeting carbon neutrality by 2050, producing energy-critical metals and producing no coal. A substantial majority—seven out of ten—of the largest mining & metals companies are publicly aiming for carbon neutrality by 2050.

Other relevant factors included investing in revolutionary technology and digitalization, having an exceptional safety record, and diversifying the board, management and workforce.

Transitioning from "take, make and waste" to "take, make, recover and reuse" will enhance core revenue and maximize the value of end-of-life materials. Recycled materials will shift down the cost curve, reducing supply costs and hedging against volatility in raw material pricing. Likewise, companies can use their circularity processes to attract sustainability-focused customers.

Companies without a systematic approach to addressing material ESG gaps, or those who are unable to show an actual impact, are finding that it is more difficult to secure funding. This can also be a barrier to entry on stock exchanges, to obtaining permits or insurance coverage, attracting talent and maintaining a social license to operate.

For example, to be bankable, mine development projects will need to take into account ESG and sustainability best practice at every stage from inception to mine decommissioning, and throughout the supply chain. Mining & metals companies may also be unable to access other forms of capital in a downturn if they cannot convince investors that ESG remains a priority.

Robust and innovative corporate governance approaches are critical for getting on the front foot with ESG. In order to achieve defined ESG goals, it is important to embed ESG in organizational structures and operations. In this way, ESG should be seen as a competitive advantage and a source of value-add, rather than a risk to be tackled or a cost to reduce.

Nothing adds more value for us in the medium term than improving operational performance and recovering cost competitiveness versus our peers

Alberto Calderon

CEO, AngloGoldAshanti

Good governance is at the core of this, particularly in a downturn. AngloGoldAshanti CEO Alberto Calderon recently said: "Nothing adds more value for us in the medium term than improving operational performance and recovering cost competitiveness versus our peers."

There has been a shift from a focus on ESG compliance and reporting to bolder commitments with measurable targets, as well as greater transparency in reporting. Much of this has also been driven by increasing regulatory compliance obligations, such as the Task Force on Climate-Related Financial Disclosures.

Mining & metals companies should also move reporting from the global corporate level to a more granular, mine-site level. While many mining companies mention the UN Sustainable Development Goals in their sustainability reporting, few have actually integrated these targets into their business strategies, according to a Responsible Mining Foundation report that assessed 38 large-scale mining companies.

Reducing business risks around a company's ESG footprint can help reduce the likelihood of reputational damages, a loss of the social license to operate or regulatory costs. The latter can negatively impact share prices—the fatal dam collapse in Brazil and the destruction of ancient aboriginal heritage sites in Australia are clear examples of the potential consequences of getting it wrong.

A focus on the "G," and keeping ESG as a priority board agenda item, especially in a recession, can help manage costs, improve engagement with stakeholders, diversify supply chains, improve performance as compared to peers and help in the "war for talent," to build a sustainable and resilient business. In this way, mining & metals companies can make better long-term investment decisions, maintain stronger balance sheets, and see more consistent valuations and returns.

The path ahead for the social dimension is less clear than for decarbonization or energy and water efficiency, but equally critical. There is a range of social issues to consider and minefields to negotiate, including health and education, community access to clean water and sanitation, building respect in the workplace, working against bribery and corruption, and avoiding conflicts of interest. Importantly, the "S" is closely connected with how mining & metals businesses are managed.

Our 2022 Mining & Metals market sentiment survey identified local community impact, including human rights issues, as the area most likely to face scrutiny from investors and regulators related to ESG and sustainability issues. Tailings management and water usage were also cited as very important.

In positioning for the energy transition, maintaining a robust social license to operate is more essential than ever for success. The demand for critical minerals will outstrip supply in the near term.

To meet this shortfall, miners will have to develop more mines, often in previously unmined regions. As they seek to expand, companies will need to put even more effort into meeting community expectations and building trust.

Effective and proactive stakeholder engagement processes and enhanced relationships with communities will become critical for mining & metals companies

Businesses will also need to develop and embed appropriate policies, governance structures and tools to mitigate human rights risks within their operations and across their supply chains. There are already initiatives in this area, such as the Global Battery Alliance, which seeks to establish a social and responsible battery value chain, safeguarding human rights as well as promoting environmental sustainability.

As issues related to human rights, corruption, bribery and provenance play out at a macro level across the mining & metals sector, companies should ensure that their focus extends to the enterprise level as well. For example, while digitization and automation have opened up significant productivity possibilities for mining & metals companies, they can also put companies at greater risk of cyberattacks and privacy breaches. The proliferation of social media also increases the potential for reputational damage.

Tax collection continues to be a clear government priority, particularly with the need to fund fiscal deficits that were required to mitigate the impact of the pandemic. This will likely be even more heavily scrutinized in the throes of a recession.

Mining & metals companies should continue to prioritize tax transparency and governance as a key focus within the business, giving them the chance to highlight their significant financial contributions to their communities and the resulting improvements in education, infrastructure and so on.

Effective and proactive stakeholder engagement processes and enhanced relationships with communities will become critical. Monitoring and analysis of companies' involvement in ESG controversies is increasing as part of the risk assessment process, supporting investors in understanding where gaps may exist between public ESG commitments, and operational practice.

By putting these controls in place, companies can enhance and strengthen their reputations as valued and responsible partners in the regions in which they operate. This can serve to open up new opportunities and markets for miners looking to extend the life of mines, move into new jurisdictions and seek new leases.

ESG factors will inevitably shape the future landscape for mining & metals companies. If a business allows itself to become an ESG laggard, it is unlikely to survive, particularly if peers lead the way.

In the event of an economic downturn, ESG projects may see some short-term erosion as businesses look to trim costs, but longer term, the focus on ESG issues will only be renewed and enhanced. If the mining & metals sector wants to be seen as leading the path to net-zero and achieving the energy transition, all stakeholders will need to put their ESG strategy front and center, with the same focus applied to ESG as to the extraction of minerals.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View image: What is the key risk for mining & metals? (PDF)

View image: What is the key risk for mining & metals? (PDF)

View image: PRI signatory growth in 2020 – 2021 (PDF)

View image: PRI signatory growth in 2020 – 2021 (PDF)

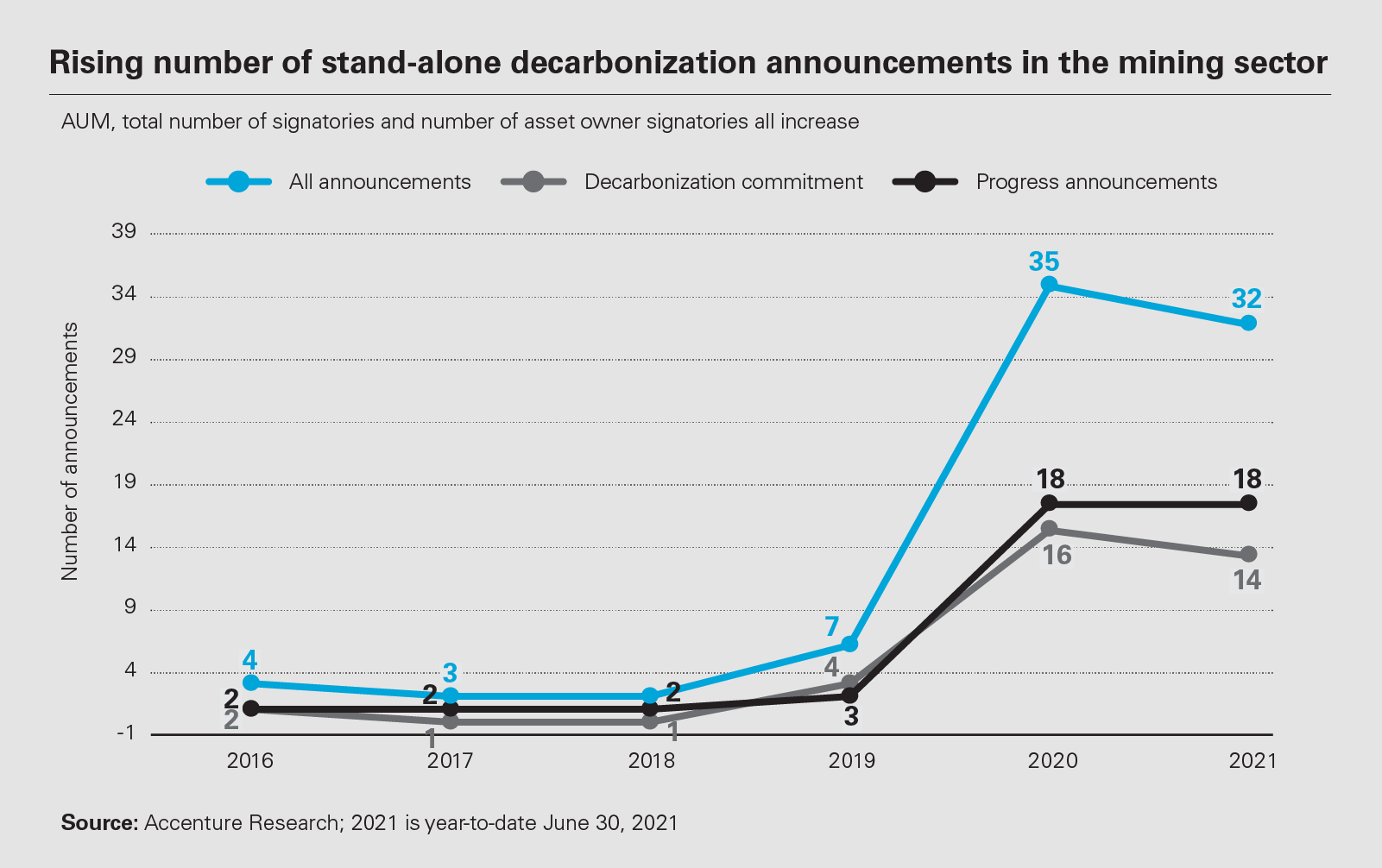

View image: Rising number of stand-alone decarbonization announcements in the mining sector (PDF)

View image: Rising number of stand-alone decarbonization announcements in the mining sector (PDF)