Decarbonizing in a downturn: Can the mining & metals sector afford (not) to change?

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

Russia's actions in Ukraine fueled an unprecedented rally in mineral and metal prices earlier this year, with multiple metals breaking historical records. However, this rally was short-lived. Within six months, metal prices collapsed back to 2020 levels in the most volatile first half of the year. There are myriad factors that are lining up to cap mineral and metal prices in the coming months, the most significant of which, we believe, is the rapid deterioration of the global economy.

In recent times, the mineral commodities cycle has been out of synchronization with the global macro-economic cycle—this time the cycles appear to be converging. With the prospect of global downturn looming, we ask the question, "Is the mining & metals sector prepared?" Is the sector truly resilient to disruption in supply chain, inflationary pressures, headwinds on demand, increased funding costs and of course, the drive to net-zero? Or will China's fiscal and monetary policies and the latest legislative developments in US and EU regulation provide enough support to the sector so that miners and the rest of the supply chain can capably respond to market conditions? Can the ESG agenda and decarbonization projects contribute to the long-term sustainability of the sector itself?

We are thinking critically about what a downturn means and whether this could, in fact, be a major opportunity to distinguish the sector from its traditionally dominant counterpart, the oil & gas sector. We hope you find Mining & Metals 2022: Putting the Resilience Rhetoric to the Test a stimulating read.

The mineral commodities cycle, in recent times, has been out of synch with the global macro-economic cycle—this time the cycles appear to be converging

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

A steady supply of minerals critical to the energy transition must be ensured through the expected recession.

Mining & metals companies have been increasingly focusing on enhancing their environmental, social and governance credentials in recent years as part of the energy transition. But with a global recession looming, will they be able to maintain their commitment?

China is looking beyond its borders to maximize the returns from the minerals needed to make the energy transition happen.

Participants in the mining & metals supply chain will see many challenges—but also opportunities—in playing both offense and defense in an economic downturn.

Mining & metals companies can take advantage of low prices in the leveraged finance markets to manage their liabilities amid the expected recession.

Financial crime flourishes in a downturn, and the mining & metals sector is not immune to it. The sector faces a number of industry-specific risks, and will need to react to the ensuing likely surge in enforcement activity.

Participants in the mining & metals supply chain will see many challenges—but also opportunities—in playing both offense and defense in an economic downturn.

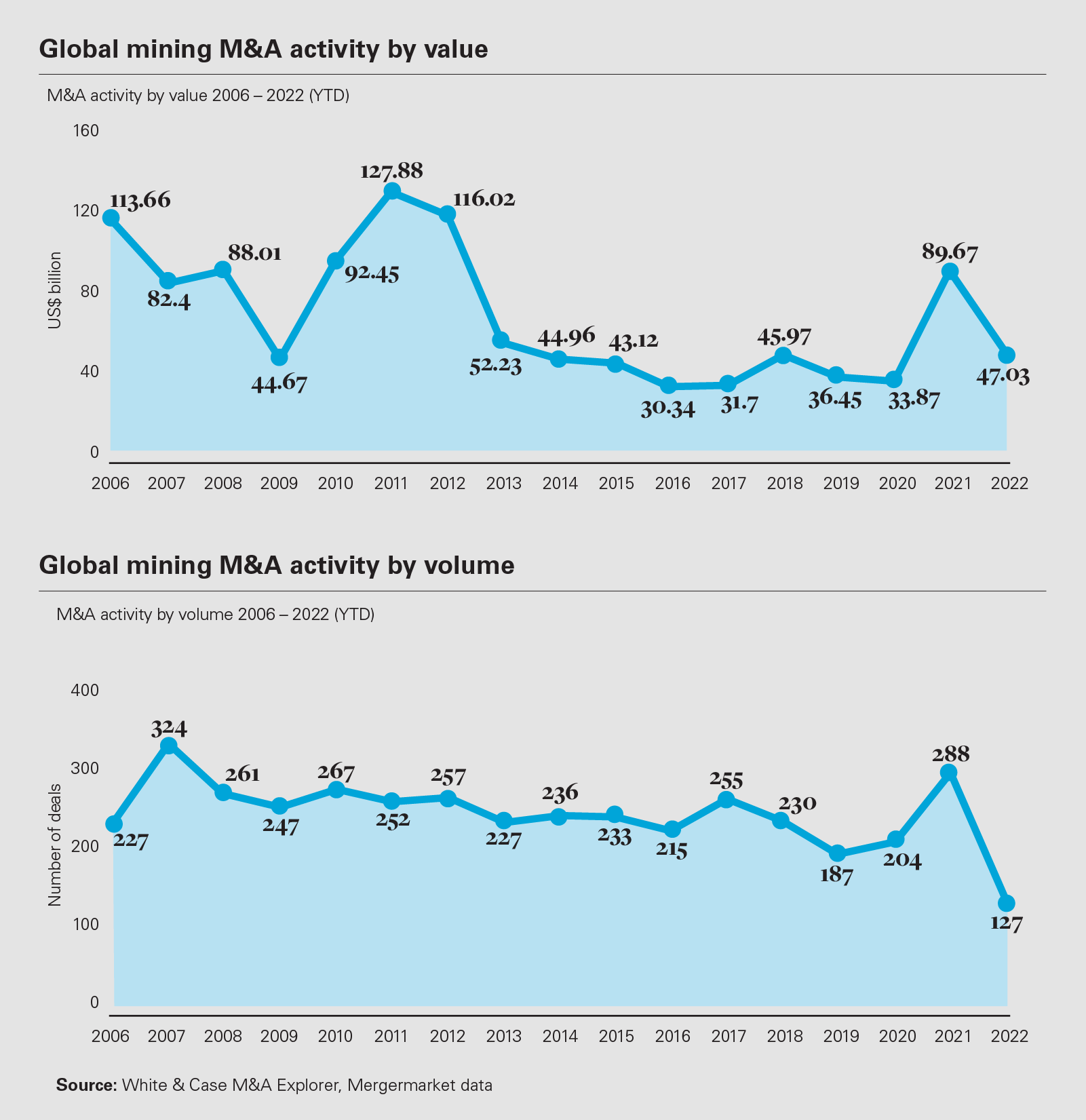

Despite the heady profits reported by many in 2021 and the first half of 2022, all participants in the mining & metals supply chain are likely to face considerable headwinds in the coming months.

Ongoing supply chain disruption, inflation, volatile markets, increased external funding costs and falling commodity prices in response to an expected global economic slowdown will have an impact on every participant. As inflationary pressures, combined with declining prices, impact the ability of mining & metals companies to meet their capital and operating expenditure requirements, companies should seek to ensure that they are maximizing their chances of raising additional capital.

On the flip side, and perhaps counterintuitively, off the back of strong commodity prices and a sustained period of relatively modest capital expenditure and M&A, an economic downturn may present those with stronger balance sheets with opportunities to make strategic acquisitions and pursue various growth options.

In a downturn, fortune favors the bold, with companies that make significant acquisitions outperforming those that do not

US$3.1bn

Rio Tinto's US$3.1-billion bid for Turquoise Hill Resources issued on

on August 24, 2022

It is never easy to raise financing for the mining & metals sector. With various funding lines now harder to access—at least in certain core mining markets—it has become all the more important to assess the key determinants for a successful financing.

Borrowers who successfully implement and demonstrate their ESG and sustainability initiatives become more attractive to investors and financiers alike. In light of a tightening of the capital markets in a potential economic downturn, ESG will become an even more important consideration to be able to attract investors and lenders.

For example, in circumstances where a project's economics may not meet the requirements of commercial bank lenders, attracting capital from a development finance institution will incur more onerous ESG requirements in order to comply with those institutions' mandate to promote sustainable development. Similarly, a borrower seeking support from export credit agencies will need to comply with the export credit agencies' ESG policies. Accordingly, when a financing involves a mix of commercial banks, development finance institutions or export credit agencies, some commercial banks will rely on the ESG requirements of the development finance institutions or export credit agencies.

In recent years, a nascent area for the mining & metals sector is the ability to access sustainability-linked financings. Previously, sustainability-linked financings were seen almost as a contradiction. However, with a growing recognition of the need for mining projects to drive the energy transition and shift to net-zero carbon, lenders—especially export credit agencies and the European banks that are traditionally large lenders to the mining project finance market—are now able to access previously unavailable internal pools of capital for sustainability or energy transition-linked financing.

Any assessment of a project's suitability for equity or debt capital markets financing will be assessed against the internal ESG criteria of each prospective investor, while credit approvals for a bank-financed project will typically require the project to comply with global environmental and social standards, which will also reflect the bank's own internal ESG policies.

Therefore, projects that meet ESG sustainable lending criteria are more likely to attract interest from a wider range of investors and financiers. This could include projects producing clean energy or energy transition minerals such as lithium, platinum group metals or manganese, or are aimed at achieving sustainability performance targets.

Given the increasingly onerous investment and lending criteria from traditional sources of funding, along with a decreasing pool of commercial bank lenders that are willing to lend to mining projects, the past decade has seen a proliferation of alternative financing providers, including stream and royalty financing.

Stream and royalty providers typically have a higher risk/reward appetite compared to commercial bank lenders, and typically become involved in a mining project at an earlier stage of development, seeking a quasi-equity return on their investment. In any economic downturn, such sources of alternative financing are likely to become increasingly important, along with adopting a capital and financing structure that enables access to these funding sources.

When entering into any development stage stream or royalty financing, it will be particularly important for mining & metals companies arrangements that will need to be put in place alongside the stream or royalty, or in the future. A well-designed and documented capital structure, and the associated intercreditor arrangements, should permit any required future financings or hedging with minimal, if any, re-negotiation of the existing financing arrangements.

A recent example, a privately held and unleveraged platinum group metals producer, which is undergoing a comprehensive overhaul of its debt and equity capital structure. The purpose of the overhaul is to facilitate significant upcoming mine expansions, its commercialization of its processing technology over the coming years and to bring more flexibility in case of an economic downturn. The renewed capital structure includes a proposed IPO via a dual listing on the New York and Johannesburg stock exchanges, a multisource financing involving a combination of debt and stream financing, and revised offtake arrangements that underpin the next phase of the company's development, and debt and equity capital raisings.

A flexible capital structure has the additional benefit of helping a company that may be looking at strategic opportunities in a possible economic downturn. Although the macroeconomic headwinds faced by the mining & metals industry have brought price volatility, economic uncertainty and cost-cutting to the forefront of miners' attention, the current climate should drive a modest rebound in M&A activity and alternative investments into the sector from the decline in volume and value in 2022 so far.

In a higher interest rate environment with higher capital and operating costs, M&A is often preferred to organic growth, as it bypasses several up-front hurdles of in or near-production assets, such as the time required to make a mine operational, delays or overruns. Miners that are cash-deficient or have large upcoming project funding requirements are the obvious targets for potential acquirers, some of which may have been able to obtain significant and cheap funding lines during the recent period of consistently high prices and soaring profitability.

With the ability to acquire being stronger now than in past downturns, given the level of accumulated cash and mix of capital available (for some), there should be increased M&A activity by well-funded, cashed-up players using their deep balance sheet to try and acquire less well-funded miners at depressed valuations.

Indeed, recent research by the Harvard Business Review shows that fortune favors the bold in a downturn, with companies who make significant acquisitions outperforming those that do not, given that a short-term economic downturn is outweighed by long-term value creation during the expansionary phase of the economic cycle. This type of long-term outlook aligns with the well-documented need to produce vast quantities of metals to meet the growing production of EV and other climate change-related objectives.

One recent example of this is BHP's non-binding offer to acquire copper and nickel player OZ Minerals. BHP promised compelling value creation and certainty for OZ Minerals shareholders in the face of a deteriorating external environment and increased operational and growth-related funding challenges for the target company. The bid price was described as "opportunistic" by OZ Minerals and was promptly rejected by its board.

The differentiating factor for M&A success is the ability to overcome deal risks, not the economic climate. Within the mining & metals sector there are two "deal killers" —price, and unknown country risk—but companies can find ways to overcome these to get the "right" deal through.

When pursuing growth, miners should consider alternatives to traditional M&A, including joint ventures, minority investments in other miners, strategic alliances, royalty financing deals and streaming or off-taking agreements

The way OZ Minerals rejected the BHP bid is also often seen in the private M&A arena, and it shows how parties can have differing ideas on deal price. The bid-ask spread is largely driven by their own assumptions and forecasts.

From the purchaser's perspective, the price paid should appropriately reflect the risk of achieving the production rates or realizing the estimated resources and reserves. This is particularly important when there are significant cost pressures on the business, or historic underinvestment in capital expenditure. On the other hand, the seller wants the deal price to account for long-term value creation, including growth options on the basis that it can obtain the funding it needs to get to or ramp up production.

In public M&A takeovers, the acquirer is often required to improve consideration up-front. This recently occurred in Rio Tinto's cash bid for Turquoise Hill Resources. Rio Tinto announced the improved US$3.1 billion proposal a week after a special committee at Turquoise Hill rejected its initial US$2.7 billion offer, describing it as unfair to its minority shareholders.

Meanwhile Gold Fields improved its scrip offer to Yamana Gold shareholders by increasing the promised dividend payout and proposing a Toronto Stock Exchange listing to get shareholders to accept the contentious takeover.

In private M&A scenarios, there is likely to be a continuation of the now-established practice for deferred or contingent consideration mechanics, such as earn-outs or royalties and streams, built into a deal's approach to bridge the bid-ask spread. While not new—or specific to the mining & metals sector—deferred consideration is an important tool for dealmakers to bridge valuation gaps and address uncertainty, especially against the backdrop of extreme volatility in commodity prices.

Acquirers are also increasingly employing bespoke deferred or contingent consideration mechanisms being employed, tailored for a range of factors including country risk, commodity price risk, and operating cost and inflationary risk. If structured correctly, these mechanisms can also provide the additional benefit of incentivizing management and ensuring an aligned business transition.

Faced with increasing regulation and social and political risk, mining & metals sector participants increasingly have to factor in country risk when undertaking M&A. The recent nationalization of the lithium industry in Mexico, heightening geopolitical tensions and prominence of the social license to operate, highlights the very real risk that miners face when undertaking deals. These risks can be mitigated by imposing certain deal conditions.

However, there is a tension between seeking protection from these risks while keeping the deal attractive with a shorter time frame and low conditionality.

Miners will favor M&A where they have a current geographical presence and strong relationships with the government and local community. This may afford them a competitive advantage in emerging markets where other companies may shy away from risks they are unfamiliar with, or where miners are in an unfamiliar operating environment.

The Rio Tinto bid for Turquoise Hill has the added benefit for an acquirer with a deep balance sheet of seeing it deploy more capital into a world-class asset that it is already operating and knows well—removing some of the risks often associated with M&A.

Acquirers are also likely to take a proactive approach to M&A structuring to ensure that sustainability and social license concerns are addressed.

US$50m

BHP's investment into the Kabanga

Nickel project in Tanzania in January 2022

When pursuing growth, miners should consider alternatives to traditional M&A, including joint ventures, minority investments in other miners, strategic alliances, royalty financing deals and streaming or off-taking agreements.

Anglo American's recent deal with Genmin, an Australian Securities Exchange–listed iron ore exploration and development company with assets in central West Africa, is a prime example of an investment involving alternative structures. Anglo American signed a royalty arrangement with Genmin, with exclusive rights to negotiate project funding and offtake agreements. Genmin said that Anglo American was the "ideal potential partner", given its long history in Africa.

Earlier in 2022, BHP invested US$50 million into the Kabanga Nickel project in Tanzania via a US$40 million minority equity interest in Kabanga Nickel, as well as US$10 million in Lifezone Limited, the owner of the hydrometallurgical technology that will be used for the Tanzanian refinery. This deal not only gives BHP access to nickel but also innovative mining services which, if successful, can potentially be employed at scale across its projects.

Pursuing alternatives to traditional M&A can provide many benefits. These include reduced costs, as miners can pool complementary capabilities such as assets, technology and shared services in a way that mutually achieves inorganic growth without acquiring all of the liabilities attached with traditional M&A.

While traditional M&A takes time to deliver benefits, alliances offer a faster and more responsive way of disrupting the market through new value propositions. They can also offer better diversification, as miners can obtain exposure to an array of growth projects at an agreed cost, especially where emerging technologies or innovation projects are involved. These types of transactions also allow more junior miners to scale up with strategically important partners that would otherwise be too big to acquire.

Aside from entering into new joint ventures, companies may decide to minimize uncertainty by focusing on deals that they know or have experience with by increasing their economic interest or exposure to a known project. There are several notable examples of this, including First Quantum Minerals approving plans for a US$1.25 billion expansion of the company's Kansanshi copper mine in Zambia and Glencore's acquisition of the remaining two-thirds of the Cerrejón coal mine in Colombia from its equal JV partners, BHP and Anglo American.

Overall, the outlook for the mining industry remains uncertain in the second half of 2022, but opportunities remain to bolster capital structures and to pursue strategic M&A. For mining projects that can demonstrate their continued commitment to ESG, both conventional and a wider pool of capital will remain available, including from alternative finance providers.

For these companies, it will be imperative to carefully design a capital structure with future funding requirements in mind. In addition, in any economic downturn, the prospect of long-term value creation from strategic acquisitions or alternative investments during this period of uncertainty will ultimately lead to greater returns for companies.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: Global mining M&A activity by value (PDF)

View full image: Global mining M&A activity by value (PDF)